NPCT - NPCT: New Multi Asset Fixed Income CEF

Summary

- NPCT is a multi-asset fixed income CEF that IPO-ed in 2021.

- The vehicle is down more than -43% since issuance on a total return basis.

- The fund runs a high duration profile of 11.7 years, which gives it a high sensitivity to rates.

- The vehicle is currently trading at a 14% discount to net asset value.

- This article covers CEFs from our suite of products - we focus on macro portfolio allocation, CEFs, and yield-generating options strategies, targeting overall yearly portfolio returns of 9%+.

Thesis

Nuveen Core Plus Impact Fund ( NPCT ) is a fairly new fixed income CEF from the Nuveen suite. The fund IPO-ed in April 2021, and has not fared well since issuance, being down more than -50%.

If an investor looks at historic CEF performances, they will notice a funny commonality - they all tend to lose money in the first 1-2 years. A CEF usually prices at $20/share but usually ends up lower. Not all CEFs are created equal, of course, but since launch the management team has a certain pressure to allocate capital, irrespective of timing, which might not be optimal for the ultimate investor. Reviewing very well established managers such as PIMCO or BlackRock ( BLK ), especially on the fixed income side, gives a good glimpse into this incipient vehicle behavior. Again, our view here is that the manager experiences significant pressure to put cash to work in order to justify the charged fees, and in the process of doing so it invests at sub-optimal periods.

NPCT is a multi-asset fixed income CEF, spanning the global fixed income spectrum:

The Fund may invest up to 50% of Managed Assets in below investment-grade investments (rated BB+/Ba1 or lower at the time of investment or unrated but judged to be of comparable quality) but no more than 10% in investments rated CCC/Caa or lower at the time of investment (or unrated but judged to be of comparable quality). The Fund can invest without limitation in investments of foreign issuers, with no more than 30% of Managed Assets in investments of foreign issuers located in emerging market countries

Source: Fund Fact Sheet

Currently the fund has fairly even allocations among investment grade bonds, high yield securities and emerging markets debt, with narrower sleeves allocated to preferred securities and commercial mortgage backed securities. The fund runs a very high duration of 11.7 years, which has been partially responsible for its horrendous -40% total return performance this year.

We are not huge fans of multi-asset CEFs because they have very dispersed risk factors. In NPCT's case the main performance driver have been rates, but the CEF runs credit risk and political risk as well through its holdings. We are just continuously amazed at the investor base that buys into CEF IPOs because they are generally such a bad idea and have overwhelmingly generated loses. An investor needs to see a bit of fund track record to understand a portfolio manager's investment/trading style and general allocation preferences, especially for a multi-asset fund. By definition, multi-asset funds give managers a substantial amount of latitude in choosing the asset class allocations, and thus the risk sleeves the fund runs.

We believe we are going to see a recovery in risk assets in 2023, and NPCT will be part of that wave. However, we do not expect the discount to narrow much, and we are keen to see a distribution that is more aligned to the actual cash-flows produced by the portfolio.

Holdings

The fund takes a multi-asset approach:

Top Sectors (Fund Fact Sheet)

We can see the vehicle has an even split among investment grade bonds, high yield corporates and EM debt, with smaller allocations to preferred securities and CMBS debt.

The portfolio rating quality is reflective of the asset class split:

Credit Quality (Fund Fact Sheet)

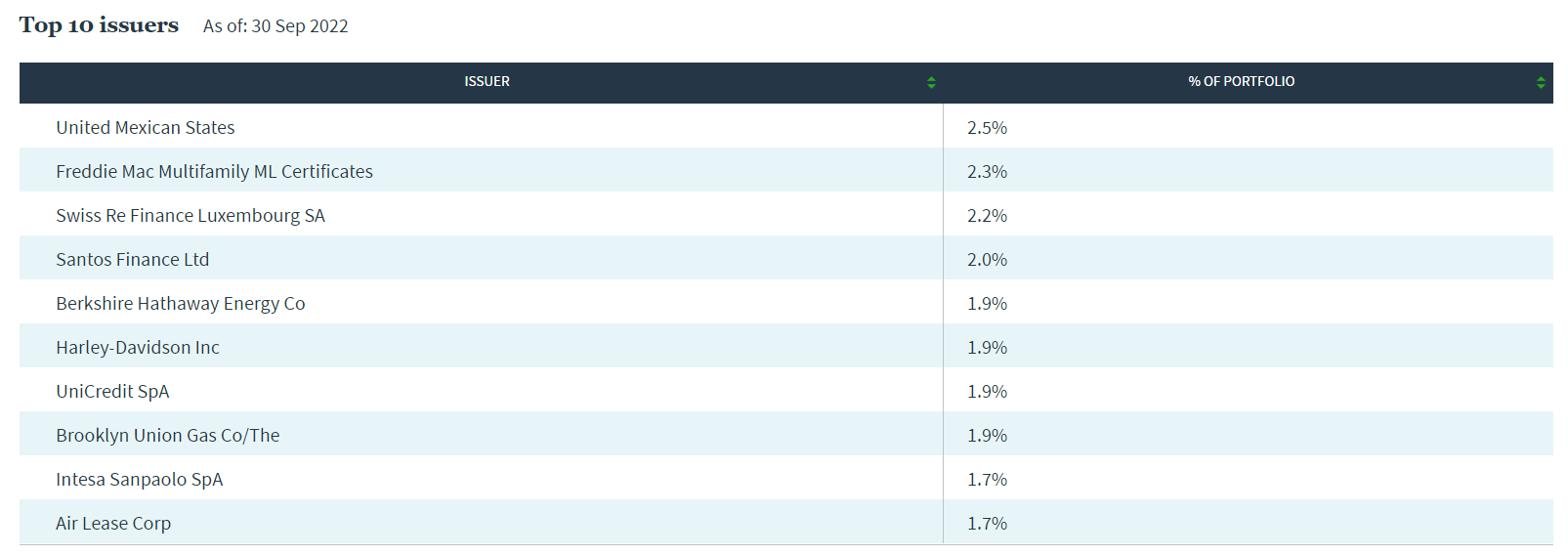

The fund has a granular build, with individual issuer exposures sub 3%:

{kind=link}

The fund runs a very high duration profile:

Characteristics (Fund Fact Sheet)

While the total number of holdings is fairly tight at 131, the fund is fairly long duration.

Performance

The fund is down an astounding -40% year to date:

{kind=link}

On a total return basis the fund is down more than -43% since issuance:

{kind=link}

Duration and credit spreads have been the main drivers for the move here.

Premium / Discount to NAV

In its short life, the CEF has mainly traded at a discount to net asset value:

The reason behind this trading pattern is the lack of performance and fund identity. As mentioned above, it is always difficult for new multi-asset CEFs to assert themselves, especially on the back of a poor overall market set-up. The discount will persist in the future, and it will only compress once the fund is able to post consecutive quarterly positive performances. The Jerry Maguire quote comes to mind here, namely the "Show me the money!" phrase.

Distributions

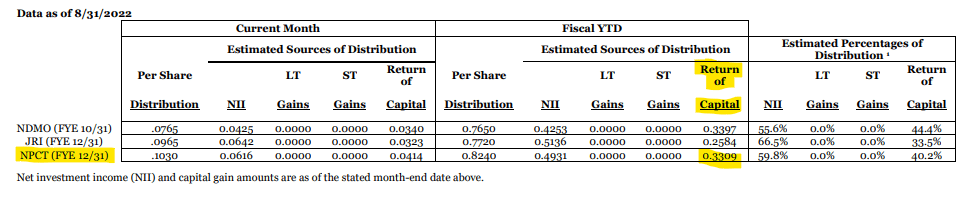

The fund has a 12% yield, which is not covered:

{kind=link}

We can see that year to date more than 33% of the distribution was made up of return of capital. Expect a true cash-flow yield here of around 8%. Sometimes CEFs can compensate the lack of interest income via short or long term capital gains obtained through their trading activity. Given the fact that the fund IPO-ed at the top of the market, none of the purchased securities seem to offer capital gains, thus the utilization of ROC.

Conclusion

NPCT is a new fixed income CEF from Nuveen. The fund takes a multi-asset fixed income approach that currently has even allocations among investment grade debt, high yield bonds and emerging market debt, with smaller sleeves allocated to preferred securities and CMBS bonds. The vehicle IPO-ed in 2021, and has had a very poor performance since issuance due to the violent rise in rates in 2022. The fund has a high duration of 11.7 years and a balanced credit risk profile given its cross-asset allocation. Given its lack of a positive historic performance, the CEF is currently trading with a 14% discount, which we expect to persist. The fund has a 12% current yield which is unsupported. Expect an 8% yield from the underlying leveraged collateral, with the rest being composed of ROC. We believe 2023 will see a recovery in risk assets, with NPCT included. However there will be no boost from the narrowing of the discount.

For further details see:

NPCT: New Multi Asset Fixed Income CEF