NRGX - NRGX: Change In Mandate Should Drive A Valuation Rerating

2023-10-06 06:32:17 ET

Summary

- PIMCO's Tactical Credit Opportunities Fund is changing its investment mandate to focus on multi-sector credit with a reduced allocation to energy assets.

- The fund will be renamed the "Dynamic Income Strategy Fund" (PDX).

- The change in the structure, fee reduction, and other factors should lead to a partial valuation convergence with the rest of the PIMCO taxable CEF suite.

The other day PIMCO announced that its PIMCO Energy & Tactical Credit Opps ( NRGX ) fund will change its investment mandate to a multi-credit focus with a 25%+ allocation to energy assets (down from 80%+). As a result its name will become the "Dynamic Income Strategy Fund" (PDX).

It's not clear whether these energy investments will be credit or equity. NRGX uses the typical PIMCO formula it uses elsewhere such as in PGP and in its StocksPLUS mutual funds. In this format the fund uses index total return swaps for much of its equity exposure and adds an actively-managed credit overlay.

The point of this is that PIMCO admit they don't add much value in stocks but can add value in credit which sounds about right. In fact, a long-running trend on this service is that nearly all equity CEFs underperform their equity benchmarks over time, something much less common for credit funds.

Valuation Thoughts

The average PIMCO credit CEF premium is in the double-digits so we should see an improvement in valuation leading up to the conversion and possibly after.

Systematic Income

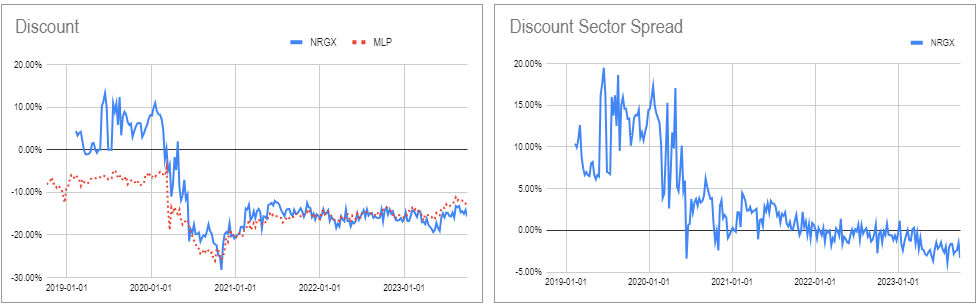

The view that PIMCO is converting the fund because it finds the wide discount embarrassing is off base. NRGX has been trading more or less in line with the MLP CEF sector in valuation terms. And while the MLP sector may not be a perfect peer group for NRGX, it's the best there is and it's surely a much better peer group than the other PIMCO taxable CEFs.

{kind=link}

The fund's total NAV return is well above the sector average and the benchmark ETF.

Systematic Income CEF Tool

Not only that but NRGX is actually the best-performing MLP sector CEF since its inception. While many other MLP CEFs crashed and burned in 2020, NRGX managed relatively well - its longer duration orientation and Treasury holding likely helped during the COVID period.

Systematic Income

A second driver of valuation rerating is that the fund is reducing its management fee from 1.35% to 1.25%.

Third, there is an almost guaranteed sizable increase in the distribution given the enormous difference between the fund's current NAV distribution rate and the much higher range of PIMCO's other taxable funds which feature distribution rates that are roughly 3x larger.

Systematic Income CEF Tool

Four, NRGX beats the other taxable PIMCO CEFs in total NAV terms since its inception. This is obviously not apples to apples given the different focus of NRGX and PIMCO credit CEFs. However, once NRGX becomes a credit CEF this distinction will likely escape many investors who will assume it has always been a credit CEF and view it favorably, leading to more demand for it.

Systematic Income

Finally, the fund is very likely to move from a quarterly to a monthly distribution which income investors are much more at home with. Quarterly distributions are the most common frequency in the MLP sector but very unusual in the credit CEF space. None of PIMCO's other CEFs have anything other than monthly distributions. This shift should further increase demand for the fund.

That said, we don't expect the valuation of NRGX to fully converge with the average of the PIMCO taxable funds. In other words, the "alpha" here is much less than the 20%+ valuation difference between the average PIMCO taxable CEF and NRGX.

Systematic Income

One, NRGX doesn't have as long a track record as the higher-valuation PIMCO CEFs. The more recently launched PDO and PAXS trade at the lowest valuations.

Two, its fee of 1.25% after the restructure will still be the highest in the suite shared only by PAXS with PDO not far behind.

This combination of short track record and high management fee mostly explains why PAXS and PDO valuations are among the lowest in the suite.

Systematic Income

Finally, NRGX will continue to have a sizable energy allocation. MLP CEF sector discounts remain at or near double-digit discounts so this dynamic will likely weigh on the NRGX discount as well.

High "Government" Position Is Not What You Think It Is

One thing to watch out for in the play-by-play is the "US Government Related" item on the fund's holdings website.

PIMCO

Investors might be led to believe that this refers to Treasury Bills or even "cash" and that an elevated amount of "US Government Related" holdings is somehow indicative of a fund planning to change its investment mandate. Let's parse through this confused logic.

First, let's show that this line item doesn't refer to Treasury Bills. Another PIMCO CEF PHK holds just over $2m in Treasury securities which works out to around 0.3% of its total portfolio despite showing 14.4% in the "US Government Related" item. What it does have to do is with a chunky $77.5m interest rate swap position which comprises most of this line item.

PIMCO

Second, let's show that "US Government Related" does not refer to "cash". There are different types of "cash" - one is repo, where the fund makes an overnight collateralized loan. As we discussed in a PIMCO weekly, PAXS has around 13% of its portfolio in Treasury repo but shows only 1% in "US Government Related".

Third, let's show that an elevated "US Government Related" line item is not indicative of a fund changing its investment mandate. In one way we already showed that with PHK which has had a double-digit amount here for a long time.

However, even if we go several years back to NRGX holdings we see that it has had a consistent double-digit Treasury allocation. In other words, a high level of Treasury holding is a core position of the portfolio and has been since inception. In fact the position was higher than it is now in the fund's first year and, hence, clearly not any sort of precursor to investment mandate change.

PIMCO

To sum up, investors should not use this particular portfolio line item as any kind of indication of T-Bills, cash or that the fund is going to change its investment mandate.

Takeaways

The change in the NRGX structure to a more traditional multi-sector credit focus is likely to lead to further valuation gains for several reasons, including a convergence with higher valuations of PIMCO's other credit CEFs, a drop in the fee, a likely increase in the distribution rate and others.

At the same time we don't expect the fund's valuation to fully converge with the rest of the taxable suite given its sizable energy allocation, short track record and other factors. Investors who are comfortable with a 25% energy allocation should consider NRGX (later PDX) for their taxable PIMCO CEF exposure.

For further details see:

NRGX: Change In Mandate Should Drive A Valuation Rerating