NRGX - NRGX: PIMCO's Energy Efforts Attractive Discount

2023-03-16 22:15:43 ET

Summary

- NRGX is an energy fund offered by PIMCO, a fixed-income specialist, so it would appear outside their expertise.

- However, it isn't your everyday energy fund either, and it incorporates some fixed-income exposure and all the derivatives that come along with PIMCO funds.

- The fund's deep discount has remained fairly persistent, which means it remains attractive, too.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 15th, 2023.

PIMCO is a fixed-income specialist, with most of its funds being quite popular and well-known. More specifically, their closed-end funds have become a go-to for a lot of investors to gain exposure to their fixed-income expertise and manage the fixed-income portion of their portfolios. I'm included in that, as I own a couple of different PIMCO funds.

However, they also have an energy-focused fund that launched a few years ago. This one doesn't get nearly as much love, and perhaps rightfully so, but it remains interesting nonetheless. That fund is the PIMCO Energy and Tactical Credit Opportunities Fund ( NRGX ).

The fund's large discount means it continues to be a fairly attractive option to gain some energy exposure. That being said, it isn't your usual energy fund, either. As has come to be expected for PIMCO funds, they actually have some fixed-income exposure here and are packed full of derivative contracts of all colors that we've come to know and love.

The energy sector was the big winner of 2022, which helped provide NRGX with some fairly attractive returns. Since our last update , though, things have changed quite materially. The environment rapidly changed, too, with banks under significant pressure. That's helped take down investments across the board, not just NRGX.

NRGX Results Since Previous Update (Seeking Alpha)

With panic usually comes opportunities. It usually comes down to when a risk pays off; if it ever does, it can take weeks or years. While I'd advocate for always taking a dollar-cost average approach, it seems more appropriate than ever in these sorts of volatile periods.

The Basics

- 1-Year Z-score: -0.33

- Discount: 16.15%

- Distribution Yield: 6.12%

- Expense Ratio: 1.68%

- Leverage: 14.68%

- Managed Assets: $932 million

- Structure: Term (anticipated liquidation date on January 29th, 2031)

NRGX's investment objective is "to seek total return, with a secondary objective to seek to provide high current income." They attempt to achieve this through a "flexible strategy by focusing on investments across the full value chain, capital structure and liquidity spectrum of the energy markets."

They will "invest, under normal circumstances, at least 80% of its assets in investments linked to the energy sector and in investments linked to the credit sectors." To be structured as a registered investment company [RIC], they will allocate no more than 25% to MLPs in their portfolio. That's where the futures contracts can help juice that exposure up without breaking the rules.

...derivative instruments that provide economic exposure to these types of investments. To the extent the fund obtains exposure to MLPs through the use of total return swaps ("MLP swaps"), it expects to hold cash and cash equivalents and/or high quality debt instruments in an amount equal to the full notional value of such MLP swaps.

The fund is leveraged but is much more moderately leveraged than we typically see with other PIMCO funds. As is often the case with PIMCO funds, NRGX's leverage is through reverse repurchase agreements. Still, the total expense ratio goes up to 2.55% when including leverage expenses, and upside potential becomes amplified just as much as the risk for downside potential is amplified. A mild amount of leverage simply makes this risk relatively milder.

The fund incorporates interest rate swaps to minimize and hedge the rising rates we had been experiencing in 2022. In addition to interest rate swaps, the fund incorporates long and short futures contracts to hedge against energy prices, both crude oil and natural gas.

On top of this, we have total return swaps on equity indices and individual securities. They hold plenty of common stock names, but these total return swaps boost their actual exposure to MLPs considerably. They also had some outstanding total return swaps on a few REITs. This really highlights that despite having "energy" in the name, the fund is a smorgasbord of exposure but with an overweight allocation to energy.

Performance - Attractive Discount

With that type of exposure, it becomes quite difficult to find some peers worth comparing it against. It really stands in a league of its own. That being said, there is one fund that sort of resembles at least the broader focus of NRGX. That fund is the Tortoise Power & Energy Infrastructure Fund ( TPZ ). TPZ takes an approach of investing in energy and infrastructure with a split between equity and fixed-income exposure. So while it's certainly a stretch trying to call these two 'peers,' it can give us some idea of how well or poorly NRGX is performing.

YCharts

When comparing the funds since NRGX's inception, NRGX has come out on top so far. At least, on a total NAV return basis, that's really clear. On a total share price return basis, it isn't so evident. That's simply because the fund went to a deep discount when TPZ had already been at a deep discount. I think it's also important to note that this outperformance hadn't started to happen until 2022 when energy really started to take off. I believe that's where the added exposure of derivatives started to pay off for NRGX relative to TPZ.

NRGX's discount has also remained deep for most of the duration of the fund's life. It certainly doesn't get the same love that most of the other PIMCO CEFs do, as they often trade at premiums. At the same time, it would appear that the discount has sort of found a bottom. There are times such as 2020 with the pandemic that can push it lower, but for the most part, it's been bouncing around this level for now.

YCharts

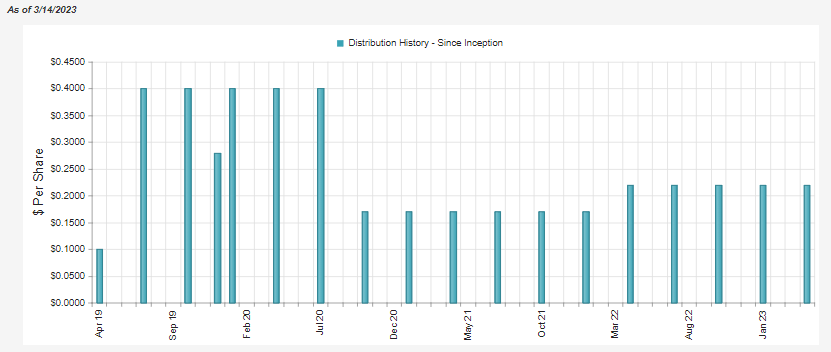

Distribution - Slow To Increase

The fund cut its distribution shortly after being launched once that pandemic hit; that isn't that unusual as most other energy funds did the same. In fact, some energy funds suspended distributions for a period. Meaning once again, if we look at 'peers,' NRGX had performed similarly to a basket of energy CEFs.

{kind=link}

That being said, they've been fairly slow to raise back. They've only raised once since cutting. That's made the fund's distribution yield fairly low, at 6.12%. On a NAV basis, it's a slim 5.13%. So naturally, one would suspect they would have room to raise their distribution. With their latest semi-annual report , they have the distribution well-covered between income and realized gains.

However, it isn't covered through net investment income alone, meaning that it will require capital gains to have it covered. Even as energy names are raising their dividends, it isn't likely going to be enough where NRGX will start to cover its distribution solely via NII.

{kind=link}

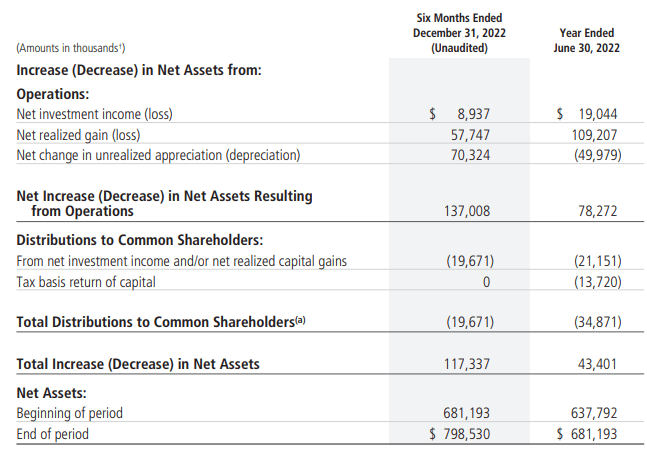

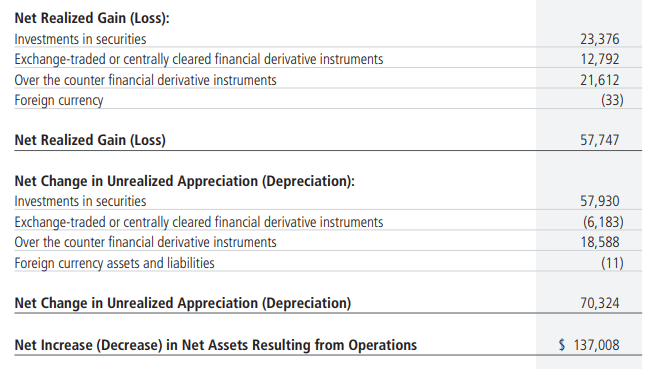

Regarding capital gains, that's one area where the derivatives have paid off handsomely for NRGX. The last semi-annual report contributed to $34.404 million of the $57.747 million in realized gains listed in the breakdown above. That alone covered the distribution paid to investors.

{kind=link}

Those are the types of gains that can be achieved even during down markets, which provide a pool of potential capital gain generation going forward.

For tax purposes, investors are likely to see return of capital distributions, even in good years. This is because MLPs generally distribute out a large portion of their own distributions as ROC; therefore, that can get passed through onto the investors holding NRGX shares. With losses realized in previous years, they can also use those carryforwards against future gains. This is why it becomes more important to watch the NAV to see if the fund supports its distribution.

NRGX's Portfolio

When looking at the fund's asset allocation, we see that the largest exposure is to equity positions. However, as mentioned previously, this is a more unusual energy fund in that we also see meaningful exposure outside of just energy equity positions.

NRGX Top Asset Exposure (PIMCO)

The fund carries the largest exposure to pipelines and independent E&P plays. In that case, that's more reflective of most energy CEFs, as a concentration to primarily pipelines/midstreams generally is the main focus of these types of funds. They tend to be less sensitive to energy prices due to their fixed-fee contracts. That being said, they aren't completely sheltered from energy prices. We've had enough energy crashes now in the last decade to see midstreams and MLPs crash along with what should be considered riskier energy plays.

NRGX Top Sector Exposure (PIMCO)

Over time, an investor just wanting some general energy exposure was better off with an ETF such as the Energy Select Sector SPDR ETF ( XLE ) rather than a basket of MLPs that could be achieved with Alerian MLP ETF ( AMLP ). Of course, it's a different story if you're an income-focused investor. XLE's 3.94% yield compared to AMLP's 8.05% will make AMLP look more appealing.

YCharts

Back to NRGX more specifically, though, as we saw above, U.S. Government related debt was the largest exposure. That remains the case on a regular basis because, with the total return swaps, they are essentially covering the notional value of those swaps through these cash equivalents.

The Fund currently expects, under normal circumstances, to obtain significant exposure to MLPs through the use of total return swaps (“MLP swaps”), and to hold cash and cash equivalents and/or high quality debt instruments in an amount equal to the full notional value of such MLP swaps.

Unfortunately, as banks are finding out, Treasuries aren't really as safe or attractive as they might have once appeared. NRGX is carrying $180.7 million, or roughly 22% of its portfolio, in instruments with a coupon of 1.125% as of December 31st, 2022. Selling these would result in a loss as the fair value of these has now dropped relative to the cost of these at $202 million.

NRGX Treasury Exposure (PIMCO)

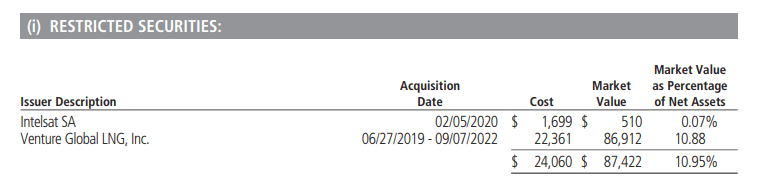

Besides the U.S. debt obligations, another top holding includes Venture Global LNG. Venture Global is restricted security, so seeing this continually be a large holding isn't unusual. The cost of their investment in this name was $22.361 million. At the end of December 2022, they noted that the market value was $86.912 million.

It's a level 3 security, so the valuation will always be a bit suspect. This position alone makes up almost the entirety of the fund's level 3 security exposure. However, given that it has a focus on LNG, it should be providing some value to the fund.

They noted that this position, in particular, "contributed to absolute performance as the security posted positive returns." When we last saw the valuation of this security, it was $50.929 million at the end of June 30th, 2022 . As noted in their report, this position has produced no income for the last twelve months. Therefore, the returns will come only from appreciation in valuation.

{kind=link}

Restricted securities aren't something to ignore, though, as they can provide huge windfalls or losses. One position that NRGX had in a big way was Rivian Automotive ( RIVN ). These were preferred stocks that were then converted to a common stock position. We touched on this more previously, but it was a restricted security, and they couldn't offload in time as most EV plays slid swiftly.

The investment cost was $9.429 million and was worth $63.115 million at the end of 2021 . Presumably, because they were restricted, they continued to hold the original 608,688 shares through June 30th, 2022. At that time, the valuation dropped to $15.668 million. It wasn't until after that time and before the September 30, 2022 holdings that the position was sold down to 303,188 shares.

As of their last reported holdings list, they continued to hold 303,188 shares worth $5.588 million. That was down from the $9.978 million it was valued previously as shares of RIVN have continued to sink.

NRGX RIVN Position (PIMCO)

So to be fair, the losses from this position probably weren't much relative to the initial cost. It was more so that they couldn't capitalize on a much juicier profit. Shares have also continued to sink from this 2022 reporting. Assuming they've held the same number of shares, the value would be closer to $3.963 million today.

YCharts

The RIVN position also helps highlight another point of how loose this fund can be in terms of an "energy" fund.

Conclusion

NRGX is an energy fund from PIMCO. A bit unusual for a fixed-income manager to be working in the energy space. However, it's as much of a "black box" as most of the other PIMCO funds nonetheless. When saying it's a black box, it isn't that we don't know what the underlying holdings are doing, but given their flexibility and active management, we don't know what types of exposure the fund may have at any one time. That's true of all CEFs, as they are actively managed, but with the PIMCO tending to use a plethora of derivatives regularly, it becomes more of a reliance on management to do the right thing.

All that being said, the fund's discount is attractive despite the fund's fairly low distribution rate. If you are looking for some energy exposure that also includes some fixed-income exposure and find PIMCO management appealing, this could be the fund to achieve that.

For further details see:

NRGX: PIMCO's Energy Efforts, Attractive Discount