NRO - NRO: Not Yet Time For This REIT CEF Despite Its -14% Discount

2023-11-10 11:49:21 ET

Summary

- Neuberger Berman Real Estate Securities Income Fund Inc is a REIT common and preferred equity CEF.

- The fund has outperformed its peers in 2023 but has still posted a negative total return so far this year.

- The fund's 14% yield is unsupported, with a high ROC utilization. Unless the wider markets recover in the next few months expect a cut here.

- The fund's wide discount to NAV is a reflection of the fund's performance and structural issues of unsupported high distributions. Do not expect a narrowing in the discount until the second half of 2024.

- The CEF has a 28% leverage ratio and a 23% standard deviation when utilizing a three-year look-back.

Thesis

Neuberger Berman Real Estate Securities Income Fund, Inc. (NRO) is a REIT equity closed-end management investment company. The fund's primary investment objective is high current income, with capital appreciation as a secondary goal. The fund contains a mix of common and preferred equity, and layers of leverage on top of its holdings. The portfolio managers at NRO take a distinct investment approach incorporating fundamental analysis combined with traditional on-site real estate analysis and meetings with company management.

NRO is an aggregator with leverage on top, and its returns are going to be driven by the REIT sector performance. REITs have been dragged down in the past year by higher interest rates, with all sectors in significant drawdowns. In this tough environment, NRO has performed better than expected, beating many peers:

From a total return perspective, the Cohen & Steers Total Return Realty Fund (RFI) is the worst performer, followed by the Vanguard Real Estate ETF (VNQ) and the Real Estate Select Sector SPDR Fund ETF (XLRE). NRO's performance is surprising given its leverage factor but explained through its low allocation to the worst hit sector, namely office REITs, which account for only 6% of the fund's collateral pool.

The main risk factor for REITs, especially for REIT aggregators, is constituted by rates. With the Fed now in a neutral stance, and with the Fed Funds futures market pricing rate cuts as soon as mid-2024, the future looks brighter for the asset class going forward. However, despite a negative performance in 2023, we are yet to see capitulation in the sector. Capitulation refers to the indiscriminate selling of the asset class on the back of a violent risk-off move in the wider markets. We saw a taste of that back in October 2022, when the sector saw a significant pull-back:

While we have given up all the sectoral gains from the 2020/2021 low rates environment, we feel the asset class will need to see an increase in risk premiums as well in order to call a bottom. As a leveraged vehicle, NRO will amplify such a move, as we can see in the fund's performance in 2020, when it experienced the deepest drawdown when compared to its peers.

NRO has done well in 2023 when compared to its peers based on its equity selection, and that comes down to a good job done by the portfolio management team but has a close correlation to the overall sector and will exhibit a larger than usual drawdown in a market risk-off scenario due to its beta.

The CEF has a very large discount to NAV of -14%, but do not expect a narrowing here until the overall asset class is back in a bull market, which we only expect towards the end of 2024. We fully discuss the discount and its drivers in the section below.

Investors who already own this name should Hold here since they have already experienced the brunt of losses from higher rates. New money contemplating the sector and the fund should wait for a bottoming out process. There is no need to rush into a name at this stage of the cycle when treasuries yield over 5% and REIT equity returns are not set for measurable gains until the Fed cuts.

Analytics

- AUM: $0.13 billion.

- Sharpe Ratio: -0.06 (3Y).

- Std. Deviation: 23 (3Y).

- Yield: 14%.

- Premium/Discount to NAV: -14%.

- Z-Stat: -1.47.

- Leverage Ratio: 28%.

- Effective Duration: n/a

- Composition: REIT Common & Preferred Equity

Holdings

The fund holds a mix of common and preferred equity:

Assets (Fund Fact Sheet)

Currently, 62% of the portfolio is made up of common stocks, while 35% is composed of preferred equities. From a sectoral standpoint, the vehicle has a good mix:

Sectors (Fund Fact Sheet)

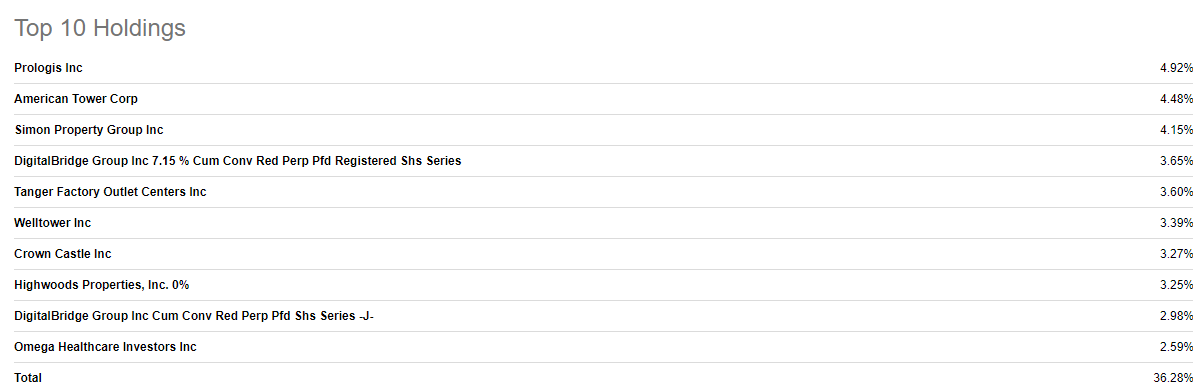

The largest sectoral allocation is to 'Diversified' at 9.93%, followed by 'Shopping Centers' at 9.28%, with Simon Property Group ( SPG ) a large holding in this portfolio at 4.2% of the fund. The fund holds a sizable position in the preferred shares from DigitalBridge Group ( DBRG ), which makes up over 6% of the collateral pool.

The top holdings in the fund are as follows:

{kind=link}

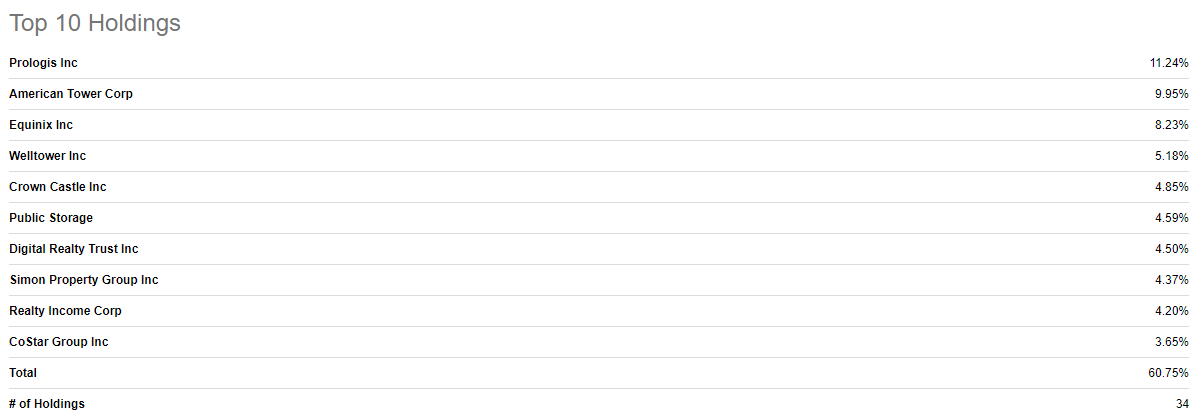

NRO's top holdings composition is not that different from plain vanilla ETFs such as the Real Estate Select Sector SPDR Fund ETF which contains similar single names:

{kind=link}

Both the CEF and ETF have Prologis (PLD) as the top holding, with the CEF having a 4.9% concentration while the ETF clocks in an 11.2% exposure. American Tower Corporation (AMT) is the second holding in both funds, again with the ETF taking a more concentrated position. The only notable difference between the two instruments is the presence of preferred equity in the NRO top holdings, as outlined above regarding the fund's mandate and composition.

Where should fair value reside

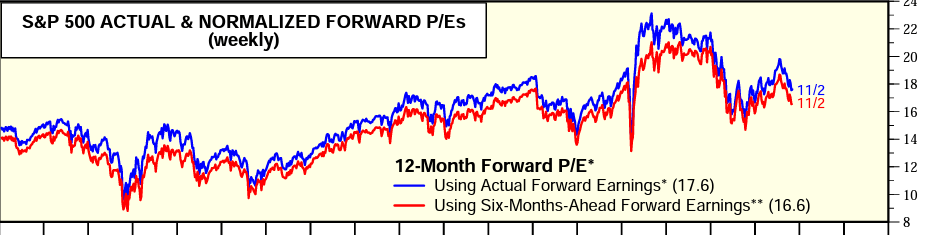

The portfolio's value as measured by its P/E ratio is still high at a level above 20x:

Valuations (Morningstar)

After the zero rates environment that characterized the 2020/2021 period which created a bubble in real estate, we are seeing a sustained unwind occurring. We should see valuations contract to move them closer to the overall index at 18x:

{kind=link}

Premium/Discount to NAV

The vehicle is currently trading at a large discount to net asset value:

The fund is a CEF that exhibits a high correlation from a discount perspective to overall performance. When the asset class is bid and performs well, the CEF has a very narrow discount to NAV. Conversely, on the back of underperformance, the discount widens. Do not expect a narrowing here until there is a well-established recovery in the asset class itself, which we expect for the end of 2024.

A CEF with a wide discount to NAV is not an opportunity to buy in itself. The beta to the asset class risk factors needs to be analyzed, as well as the pro-forma view of the sector.

Distribution - managed, but not covered

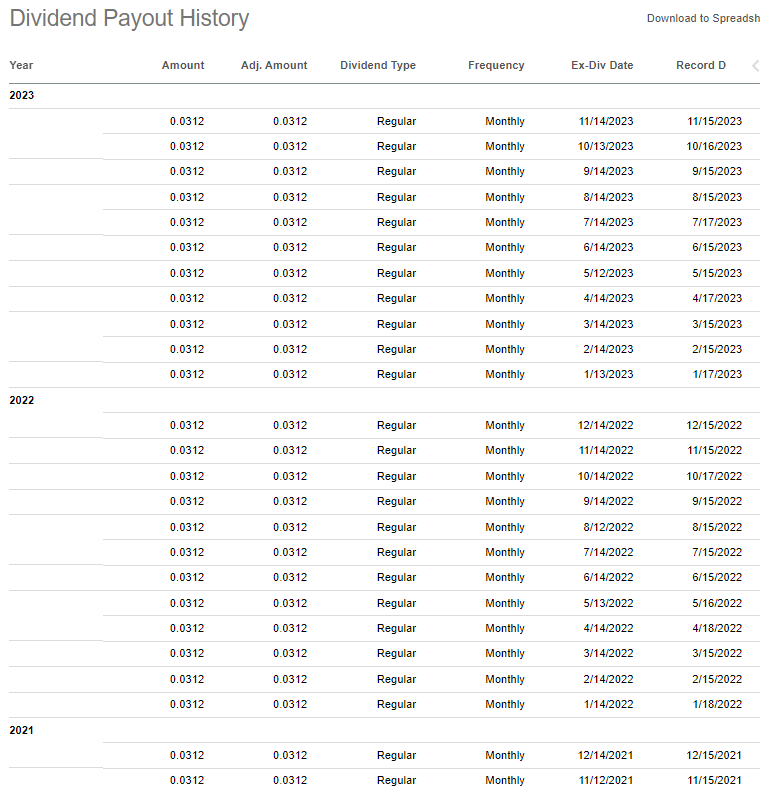

The fund has a managed distribution plan that targets $0.0312 per share of common stock, distributed monthly. The fund has been steadfast in paying out the targeted distribution in the past three years:

{kind=link}

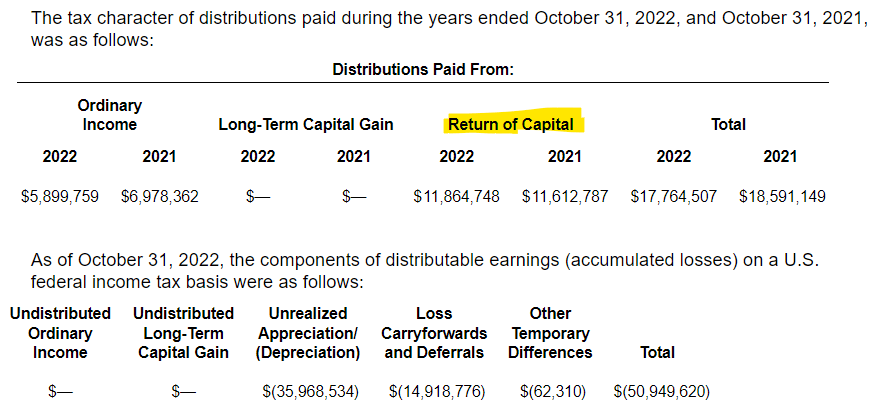

The distribution is not currently supported given the underperformance in the underlying equities making up the collateral, but the fund has done a decent job of managing the return of capital usage in the past decade:

If the REIT sectoral performance does not improve soon expect a potential dividend cut here. Outside the 2022/2023 period when the market experienced a significant drawdown, the vehicle managed its NAV in a $4.8 to $6.0 per share range. Maintaining an unsustainable distribution for a long period of time will result in permanent damage to the fund's future returns via permanently lower NAV levels. Even during 2021 when the REIT market was not in a drawdown the fund was utilizing ROC:

ROC Usage (Semi-Annual Report)

{kind=link}

This aspect correlates well with the fund's discount. The market is telling managers that it expects a poor long-term performance if current distribution metrics are kept without an improvement in the REIT sector and respective returns.

What is the forward take for NRO?

We view the CEF as having passed its worst stretch, but not a buying opportunity yet. We believe the asset class is bottoming but has not capitulated yet, with yet another significant market risk-off move in the cards. The CEF's discount to NAV will persist to trade at wide levels until a sustained recovery in the fund and asset class, a recovery which we do not expect until the end of 2024. The fund is a higher-than-normal beta play on the sector, and does a good job of transforming REIT sectoral returns into a steady high dividend yield, although its current managed distribution is not supported and will need to be cut to keep the NAV within its historic range.

Is this a good sectoral recovery play? How to monitor the name?

Just like any financial instrument, NRO is driven by risk factors. The main ones here are interest rates and P/E ratios. We are going through a monetary tightening cycle via higher rates and balance sheet run-off, which inexorably will be followed by monetary loosening. We had a similar story in 2018 when the Fed moved rates higher, only to cut in 2019. NRO had a very robust performance as the Fed cut:

{kind=link}

The CEF was up 47% in 2019 after a deep negative performance when rates were moving higher in 2018. Given its leverage, the CEF outperformed the vanilla ETF XLRE:

{kind=link}

XLRE was up only 28% during the Fed easing, given its lack of leverage.

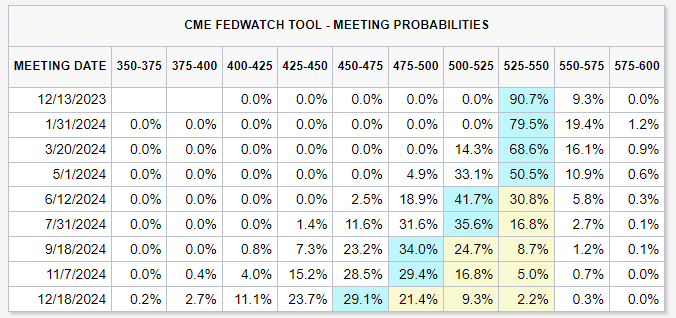

The move in valuations and price will occur once the Fed starts cutting. Currently, the market is pricing the first cut for June 2024:

{kind=link}

The fund is best to be re-visited in mid-2024 for a revised view on outlook and pro-forma price performance.

Conclusion

NRO is a REIT equity CEF. The fund has a blend of common and preferred equity with a 28% leverage ratio on top. We believe that with rates now in a neutral stance the worst is behind the asset class, but we have not bottomed yet.

The CEF has a very large -14% discount to NAV due to its overdistribution and underperformance from an asset class standpoint. Expect the wide discount to persist until the fund aligns its distribution with the asset class performance and we see a bottoming in the sector. We do not expect a positive performance from a discount narrowing until the end of 2024. Furthermore, the fund's dividend yield is not supported, and we expect a cut here if the REIT asset class does not recover in the next few months (we do not expect a recovery until the end of 2024).

While NRO has done a good job to avoiding the worst REIT sector in 2023, namely office REITs, the fund is still down in 2023 on a total return basis (i.e. dividends included). While its large discount and high yield might be appealing, they do not represent a buy signal but are symptomatic of structural and asset class issues. If you are already in the name, keep Holding since the bulk of the drawdown is behind us, while new money would do well to wait until the first Fed cut to enter this CEF and benefit from both an asset class recovery and discount narrowing.

For further details see:

NRO: Not Yet Time For This REIT CEF Despite Its -14% Discount