IYR - NRO: Real Estate At A Discount With A Very High Yield

2023-08-30 16:49:25 ET

Summary

- The Neuberger Berman Real Estate Securities Income Fund Inc provides a high level of current income and acts as a store of wealth against inflation.

- The fund's portfolio consists primarily of common stock and preferred securities, which offer higher yields than other investments.

- The fund has a low exposure to the struggling commercial office sector and employs leverage to boost its effective yield.

- The fund currently has a very attractive 12.48% yield and it appears to be able to sustain it.

- The fund is trading at an enormous discount on the net asset value.

The Neuberger Berman Real Estate Securities Income Fund Inc ( NRO ) is one of the most well-known real estate-focused closed-end funds, or CEFs, in the United States. The real estate sector has been under the microscope lately due to the impact that rising interest rates have had on many landlords and the ongoing vacancy crisis in the commercial real estate sector. These are both, directly or indirectly, events that were caused by the COVID-19 pandemic, as the enormous amount of money-printing sparked the inflation that forced the Federal Reserve to raise interest rates, and the lockdowns caused many companies and employees to realize the benefits of remote work. Despite these problems, though, there can be some good reasons to purchase real estate today.

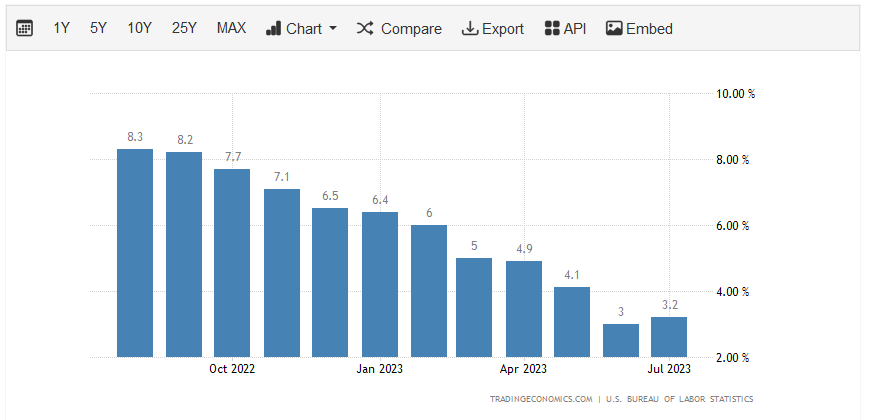

One of these reasons is that real estate acts as a store of wealth that can protect your portfolio against the ravages of inflation. While we are all aware of the four-decade-high levels of inflation that have been pervasively raising prices across the economy, the problem seems to be showing no signs of stopping. Last month, the year-over-year inflation rate actually ticked up, following a period of steady declines:

{kind=link}

The Neuberger Berman Real Estate Securities Income Fund could help protect your portfolio against the declining purchasing power of your wealth that this inflation has created. I stated this in my last article on this fund. However, that article was published back in January, so naturally several things have changed since then. This article will focus specifically on these changes as well as provide an updated analysis of the fund’s finances. Let us revisit this fund and see if it makes sense to purchase shares today.

About The Fund

According to the fund’s webpage , the Neuberger Berman Real Estate Securities Income Fund has the objective of providing its investors with a high level of current income. This makes a certain amount of sense considering the name of the fund, but its portfolio does not really conform with this objective. This is because the fund’s assets are primarily invested in common stock. As we can see here, 62.80% of the fund’s assets are currently invested in common stock, although it does have a substantial amount of exposure to preferred securities:

CEF Connect

The reason why the fund’s focus on current income does not really make sense considering this portfolio is that common stock is generally considered to be a total return vehicle, not an income one. While it is true that real estate investment trusts usually have a higher yield than many other things in the market, the Dow Jones U.S. Real Estate Capped Index ( IYR ) only yields 2.95% today. That is less than a money market fund, and as such is not particularly impressive from an income perspective. The fund’s large position in preferred stock is certainly in line with its current income objective though, as preferred stock delivers the overwhelming majority of its investment return via dividend payments to investors. It also usually has a higher yield than common equity issued by the same company. As such, it boosts the income credentials of this fund and probably gives the fund a higher income than it would have if it solely invested in common equity.

As I pointed out in my previous article on this fund, the presence of the preferred stock will somewhat weaken our inflation protection thesis. This is because the core of that thesis revolves around real estate appreciating in value along with all other real assets that are limited in supply during such an environment. It is only the common stock that is directly linked to the value of the real estate, though. The preferred stock is simply priced based on interest rates, so its capital gains are limited. Thus, in order to fully achieve the wealth preservation effect, we would want to have a portfolio consisting of 100% common stock in real estate investment trusts. This fund’s portfolio will be better at producing income than such a portfolio, but it will not be as good at providing us with an inflation hedge. Potential investors should keep this in mind when evaluating whether or not to invest in this fund as a way to protect themselves against the loss of purchasing power that comes with inflation.

Here are the largest positions in the fund today:

CEF Connect

There have been surprisingly few changes here since we last discussed this fund. The only significant change is that Starwood Property Trust ( STWD ) was removed from the largest positions and replaced with Equity Residential ( EQR ). Otherwise, there have been some significant weighting changes, but the companies themselves are the same as what we saw before. These weighting changes may have been caused by one company outperforming another company in the stock market, and do not necessarily represent the fund actively making trades to change its weightings. The fund only had a 27.00% annual turnover during the most recent reporting period, so we can see that it is probably not engaging in too much trading activity. After all, that is a pretty low annual turnover for a closed-end fund.

As mentioned in the introduction, some investors have been looking at the real estate sector with a wary eye lately due to some of the problems facing it. One of these problems relates to the commercial office sector, which I discussed in a recent article :

“The COVID-19 pandemic caused a lot of companies to adopt remote work policies and many of them found that it was better just to keep these policies in effect after the lockdowns were lifted, as the companies already had the remote work infrastructure in place. This allowed them to save a great deal of money by not renewing office building leases and the like. In addition, employees seem to be happier with the remote work arrangement and they have been increasingly opting to stay in the suburbs or even rural areas and avoid many of the big cities. This is terrible for office building owners, as cities like San Francisco now have office building vacancy rates approaching 30%.”

Naturally, a high vacancy rate makes it extremely difficult for the building owner to cover the mortgage on the property. We have already seen a few large defaults on commercial mortgages due to this. Fortunately, this fund should be somewhat insulated from these problems. As we can see here, only 5.68% of the fund’s assets are invested in the office space:

Fund Fact Sheet

This is the only real estate sector that has been struggling with vacancy problems. The remaining sectors have been holding up reasonably well. As the fund’s office exposure is relatively low, we should not need to worry too much.

As mentioned in the introduction, the other major factor that has been weighing on real estate is the Federal Reserve’s monetary tightening policy. As mortgage interest rates rise, some properties that would have been marginally profitable to purchase no longer are. After all, the rent has to cover the mortgage payment and all of the other expenses associated with the property. The higher the interest rate on the mortgage, the higher the monthly payment. Thus, the higher the rent has to be to cover the property expenses. If the market cannot sustain the needed rent, then the property is no longer a good investment. The price of the property needs to decline in such an instance to bring the mortgage payment down to a level that is compatible with the amount of rent that can be generated by the property. This does not affect the ability of real estate to serve as a store of value though, since the higher rates generally mean that the currency itself is worth more than it was in a low-rate environment. Over the long term, real estate should hold its value in the face of inflation because it is in limited supply and requires real human or mechanical effort to construct or improve.

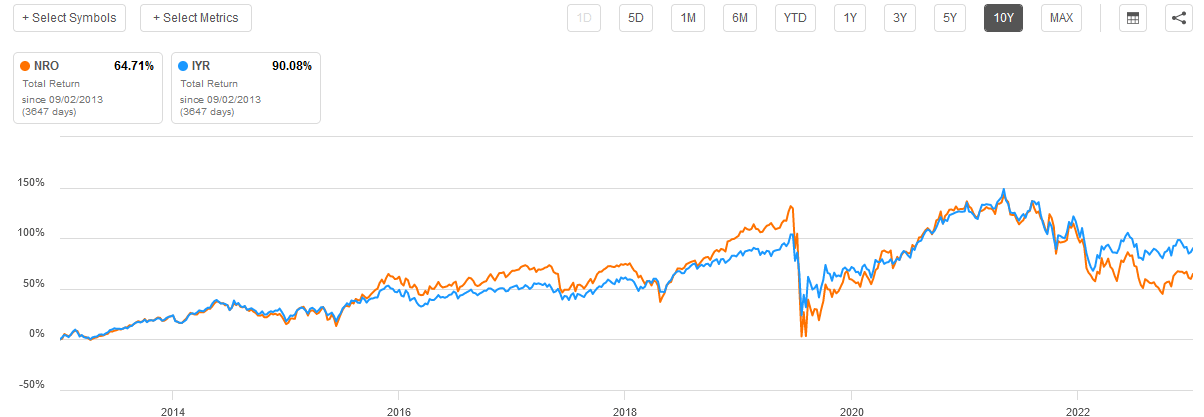

There is no perfect index to compare the Neuberger Berman Real Estate Securities Income Fund against for benchmarking. We could use the Dow Jones U.S. Real Estate Capped Index, but as that index exclusively tracks the common stock of real estate investment trusts, or REITs, it is not a perfect comparison for a fund that is splitting its investment portfolio between common and preferred stock. As might be expected, the Neuberger Berman Real Estate Securities Income Fund has underperformed the index on a total return basis over the past ten years:

{kind=link}

We get the same result over any period of time except for the past five days. The Neuberger Berman Real Estate Securities Income Fund has consistently underperformed the index. This is to be expected though, since common stock outperforms preferred stock over the long term and the index is entirely common stock. The preferred stock owned by the closed-end fund reduces its total return over any extended period.

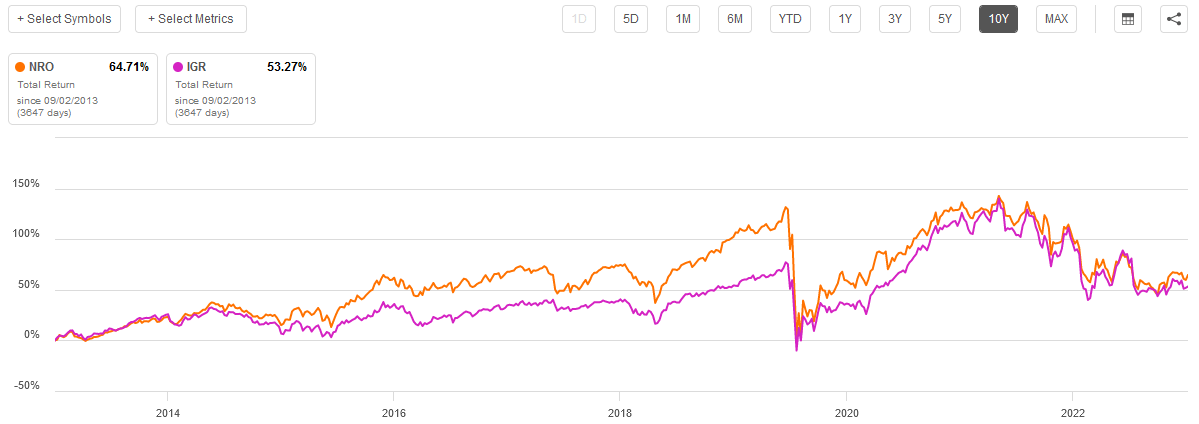

We could also compare this fund against another closed-end real estate income fund such as the CBRE Global Real Estate Income Fund ( IGR ). Here, the Neuberger Berman Fund performs pretty well. As we can see, it outperformed the CBRE Fund over the past ten years on a total return basis:

{kind=link}

This was not a consistent trend, though, as the CBRE Fund outperforms the Neuberger Berman one over both the trailing three and the five-year periods. Thus, it is somewhat difficult to derive any conclusion from these results.

While past performance is certainly no guarantee of future results, we can say that the index is by far the best investment if you do not care about the yield and just want the maximum possible performance. It should also be a bit better at wealth performance. However, the Neuberger Berman Fund is definitely an option if earning a high level of income while still getting some wealth preservation is important.

Leverage

One of the strategies employed by the Neuberger Berman Real Estate Securities Income Fund is the use of leverage. I explained this in my last article on this fund:

“Basically, the fund borrows money and then uses that borrowed money to purchase common and preferred securities issued by real estate investment trusts. As long as the total return of the purchased securities is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the fund’s portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk.”

As of the time of writing, the fund’s levered assets comprise 27.34% of the total portfolio. This is a bit more than it had the last time that we discussed it but overall, it is not too bad. The fund’s leverage is still much lower than most other closed-end funds. As such, the balance between the risk and reward here is probably acceptable. We should not have to worry too much about the fund’s leverage right now.

Distribution Analysis

As mentioned earlier in this article, the Neuberger Berman Real Estate Securities Income Fund has the objective of providing its investors with a high level of current income. In order to achieve this goal, the fund is purchasing both common and preferred shares of real estate investment trusts. These securities tend to have somewhat higher yields than most other things in the market, although they are not as impressive income vehicles as they used to be. The fund then applies a layer of leverage to boost the effective yield of the portfolio.

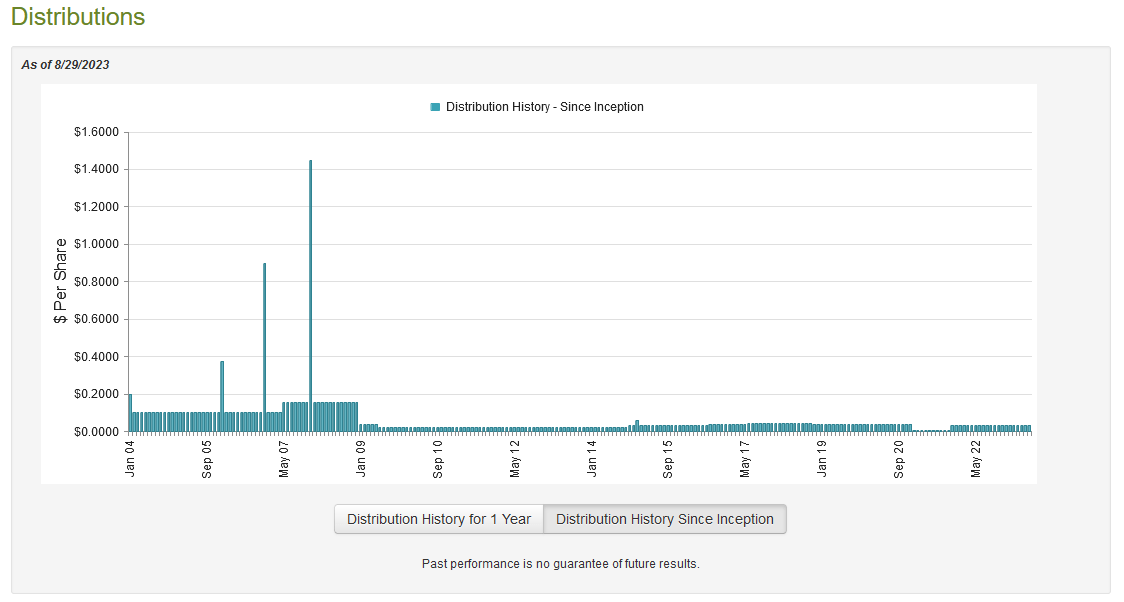

Finally, as is the case with all funds, it pays out the majority of its investment profits, net of expenses, to the shareholders. As such, we can probably assume that this fund will have a reasonably solid yield itself. This is certainly the case, as the fund pays a monthly distribution of $0.0312 per share ($0.3744 per share annually), which gives it a 12.48% yield at the current price. This is certainly an impressive yield, but unfortunately, any time a fund’s yield approaches levels such as this, it is a sign that the market expects that the distribution will be cut. A distribution cut would not be unheard of for this fund, as it has cut the payout several times in the past:

{kind=link}

The fact that the fund’s distribution has bounced around so much over its history might be a problem for any investor who is seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. However, anyone purchasing the fund today will receive the current distribution at the current yield and will not be affected by any actions that were taken in the past. As such, the most important thing is to ensure that the current distribution is sustainable as the market does not believe that it is.

Fortunately, we have a fairly recent document that we can consult for the purpose of our analysis. The fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. This is nice because the fund will have already weathered several months of the challenging environment for real estate companies, so we should be able to get a good idea of how well it is doing.

During the six-month period, the fund received $6,417,864 in dividends along with $126,647 in interest from the assets in its portfolio. Once we net out the money that the fund had to pay in foreign withholding taxes, we see that it had a total investment income of $6,541,803 during the period. The fund paid its expenses out of this amount, which left it with $4,180,168 available for shareholders. Unfortunately, that was not nearly enough to cover the $8,883,727 that the fund paid out in distributions during the period. That could be rather concerning as the fund’s net investment income is clearly not enough to cover its distributions.

Fortunately, the fund managed to generate some capital gains during the period to make up the difference. It reported net realized losses of $7,984,917 but this was more than offset by $14,798,957 net unrealized gains. Overall, the fund’s net assets increased by $2,110,481 after accounting for all inflows and outflows during the period. This fund’s distribution appears to be reasonably safe, although its net assets are still down substantially from November 1, 2021:

| 6Mo. Ending April 30, 2023 |

| FY Ending October 31, 2022 |

| Beginning of Period |

| $161,125,509 |

| $249,023,065 |

| End of Period |

| $163,235,990 |

| $161,125,509 |

We do not want the fund’s assets to decline further, but for now it seems to be okay. The biggest problem would be if the Federal Reserve keeps raising interest rates and pushing down the price of income-producing securities like the ones in which this fund has significant exposure. Chairman Powell stated that this might be a possibility in his speech from Jackson Hole last week.

Valuation

As of August 29, 2023 (the most recent date for which data is available), the Neuberger Berman Real Estate Securities Income Fund has a net asset value of $3.36 per share but the shares trade for $3.00 each. This gives the shares a 10.71% yield at the current price. This is not as attractive as the 12.22% discount that the shares have had on average over the past month, but frankly a double-digit discount on net asset value is a reasonable price to pay for any fund. Thus, the price seems to be right if you want to pick up some shares today.

Conclusion

In conclusion, real estate could be a way to protect your wealth against the ravages of inflation. This is because real estate shares many of the same qualities as other things that go up in price during periods of inflation. In particular, real estate is in limited supply, and it cannot be printed out of thin air like fiat currency. Rather, real estate can only be constructed or improved through real human or mechanical effort. The Neuberger Berman Real Estate Securities Income Fund is one easy way to invest in real estate and earn a high level of income. It is not quite as good at wealth preservation as an all-common stock fund would be, though. The fund’s price and yield are certainly acceptable right now, so it might be worth considering for a portfolio.

For further details see:

NRO: Real Estate At A Discount With A Very High Yield