T - NRO: Real Estate Makes Sense But This CEF Has Some Serious Flaws

Summary

- Inflation has been reducing the purchasing power of money and investors need a good store of value, such as real estate.

- Neuberger Berman Real Estate Securities Income Fund invests in a portfolio of real estate securities with the goal of providing a high level of current income and some capital appreciation.

- The portfolio appears geared toward a strong economy, not the likely hardships that we will face in 2023.

- The 11% yield is very attractive, but the fund probably cannot sustain it.

- The valuation is attractive, but it may be best to wait before buying Neuberger Berman Real Estate Securities Income Fund.

One of the biggest problems facing most Americans today has been the pervasive inflation that has been driving up the prices of food, energy, and many other items. This has caused many people to have to take on second jobs or perform odd tasks to obtain the extra money that they need to pay their bills or otherwise finance their lifestyles. As investors, we have another problem caused by inflation that we have to contend with.

In response to the high inflation, the Federal Reserve has reversed the incredibly loose monetary policy that has dominated the economy over the past decade and is now raising interest rates in an effort to combat it. This has had the effect of pushing down richly-valued asset valuations, which is a double hit for many of us since we are depending on our portfolios to support our lifestyles. Thus, we have a situation in which our assets are dwindling and expenses are rising. This has naturally left many investors scrambling to find a place in which they can protect their money and its purchasing power.

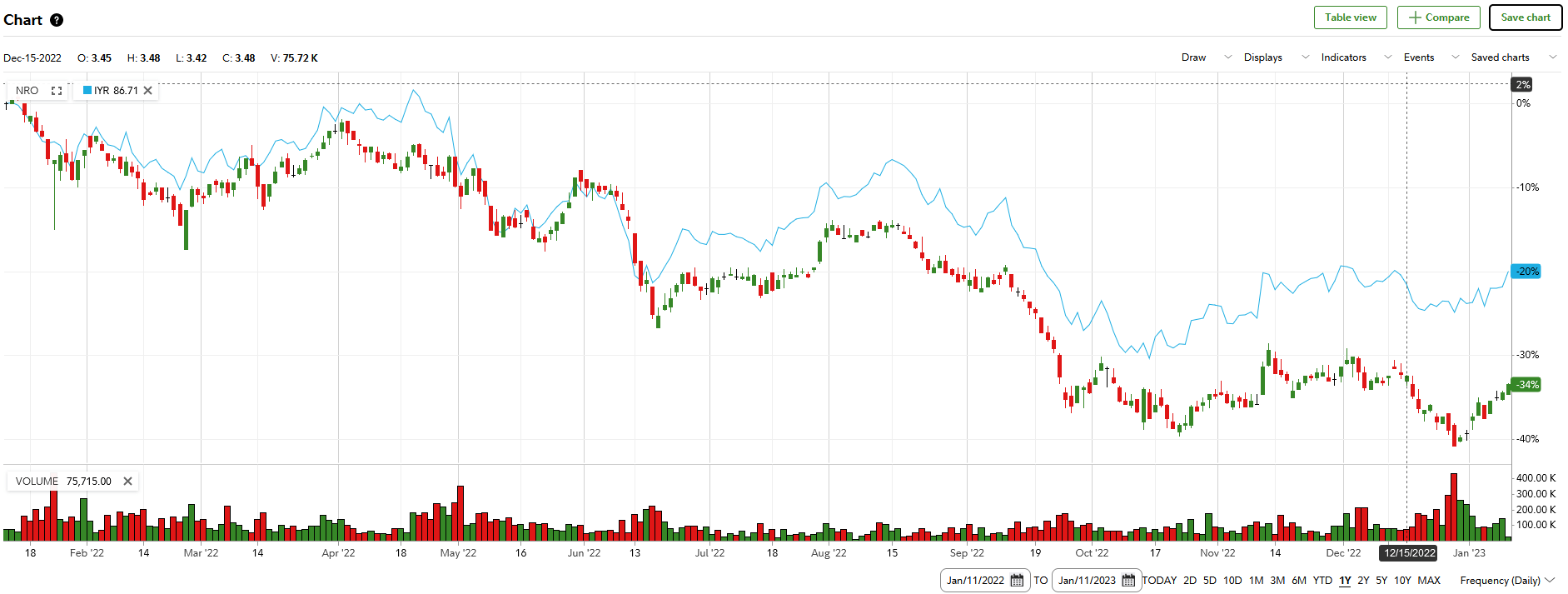

One potential option is real estate. Admittedly, this will not be the first option that many would consider as rising mortgage rates have decreased the value of real estate in many areas of the country. In fact, it was one of the hardest-hit sectors by the market decline of 2022 as the Dow Jones U.S. Capped Real Estate Index ( IYR ) is down 20.56% over the past twelve months. However, this is likely only temporary as real estate possesses a number of characteristics that should allow it to work pretty well as a store of wealth over the long term. In addition to this, real estate can be leased out to tenants so it can provide a fairly reliable source of income to help cover the rising expenses that come with the inflationary environment.

One great way to gain exposure to real estate is by investing in a closed-end fund that specializes in the sector. These funds provide easy access to a professionally-managed portfolio of real estate investment trusts that can usually deliver a higher yield than any of the underlying assets. In this article, we will discuss the Neuberger Berman Real Estate Securities Income Fund ( NRO ), which is one closed-end fund ("CEF") that falls into the category. As of the time of writing, the fund boasts a remarkable 11.08% yield and trades for a reasonably attractive price.

I have discussed this fund before, but several months have passed so obviously a few things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s financial condition. Therefore, let us proceed onward and see if this fund could prove to be a good fit for your portfolio today.

About The Fund

According to the fund’s webpage , the Neuberger Berman Real Estate Securities Income Fund has the stated objective of providing its investors with a high level of current income. This is admittedly somewhat surprising, since real estate is frequently considered to be a total return vehicle. After all, when we purchase real estate, we are generally hoping to generate income by leasing it to tenants and capital appreciation from the value of the building going up. With that said, the fund is targeting capital appreciation as a secondary objective so it is likely that management recognizes this dual mandate. In keeping with its name, the fund aims to achieve this objective by investing in real estate securities. It does not specifically state what these real estate securities are, however. Real estate investment trusts ("REITs") typically issue debt, preferred equity, and common equity, so presumably all of these would qualify as real estate securities.

In fact, a closer look at the fund reveals that it does invest in all of the different security types that are issued by real estate investment trusts. The fund’s portfolio currently consists of both common and preferred equities:

CEF Connect

The fund currently does not own any debt issued by real estate companies, but presumably, it is not barred from doing so. The current mixture of both common and preferred equity is quite nice to see, though. This is because of the advantages provided by each security type. Preferred equity will almost always have a much higher yield than the common equity issued by the same company. However, preferred equity also does not have the capital gains potential of its common equity cousin because it is a fixed-income security. It is common equity that would ultimately provide the wealth preservation effect since this is the security that we would expect to best reflect the actual value of the real estate. The fact that the fund is mixing both security types thus provides us with a pretty good mix of income and capital gains potential. This is something that we can appreciate for the purposes of our thesis.

The largest positions in the fund’s portfolio will likely be familiar to anyone that follows the real estate sector. Here they are:

CEF Connect

We see here a variety of real estate types, but by far the two largest positions are both cellular tower real estate investment trusts. American Tower ( AMT ) and Crown Castle ( CCI ) are not exactly what most people think of when they picture a real estate company. These companies do not own buildings that people can live, work, or shop in. Rather, they own cellular towers located all around the United States and internationally, which they then lease out to communications companies like AT&T ( T ) that are looking to expand the reach of their cellular networks.

When we consider how important smartphones are in most of our lives, this is a good business to be in, and it is one of the reasons why these companies have performed pretty well in the market over the past decade. Admittedly, though, I am not so sure that having them as the two largest positions in the fund is the best idea. While those two are among the largest holdings of every real estate-focused closed-end fund, they usually do not have such a high weighting.

We also see here Simon Property Group ( SPG ) and Tanger Factory Outlet Centers ( SKT ), which are both retail real estate investment trusts. One trend that we have seen over the past year is that inflation has been straining the budgets of many consumers. In fact, a recent survey shows that 81% of Generation Z members and 77% of Millennials have taken on or thought about taking on work in the gig economy just to ensure that they do not run out of money to pay their bills. In addition, the United States is widely expected to enter into a recession during 2023. This is not the kind of environment that favors discretionary spending or retail. While these real estate companies are not directly reliant on the strength of consumers, their tenants are certainly dependent on it to pay rent. As I have pointed out before, approximately 40% of small businesses are no longer able to pay their rent , so it is likely that we will see some financial trouble among retail real estate owners at some point.

There have been surprisingly few changes to the fund’s largest positions over the past three months. In fact, the only change is that Equity Residential ( EQR ) was replaced with Tanger Factory Outlet Centers. I must admit that I would prefer to see Equity Residential, as consumers are far more likely to pay the rent on their homes than they are to go shopping during times when money is tight. The fact that there have been few changes is somewhat nice to see, though, as it implies that the fund may have a relatively low annual turnover. This is certainly true, as its 27.00% annual turnover is on the low side for an equity fund.

The reason that this is nice to see is that trading stocks or other assets costs money, which is ultimately billed to the fund’s shareholders. This creates a drag on the fund’s performance that makes things more difficult for its management. After all, the fund’s management will need to generate sufficient returns to cover these expenses as well as match the performance of the index. This is a very difficult task to accomplish and it is one of the biggest reasons why most actively-managed funds fail to beat their benchmark indices. This one is no exception as it has underperformed the iShares U.S. Real Estate ETF ( IYR ) by 14% over the past year:

{kind=link}

With that said, the Neuberger Berman Real Estate Securities Income Fund does have a substantially higher yield that helps to reduce the performance difference between the two. However, an investment in the real estate index a year ago would still have a higher value today than the same investment into the Neuberger Berman Real Estate Securities Income Fund. This is, however, an imperfect comparison because the index fund does not include any real estate preferred securities. Preferred securities trade based on interest rates, just like bonds do. Thus, the rising interest rates that we saw over the past year would have a negative impact on the preferred securities held by the fund and by extension its market price.

Real Estate As A Hedge Against Inflation

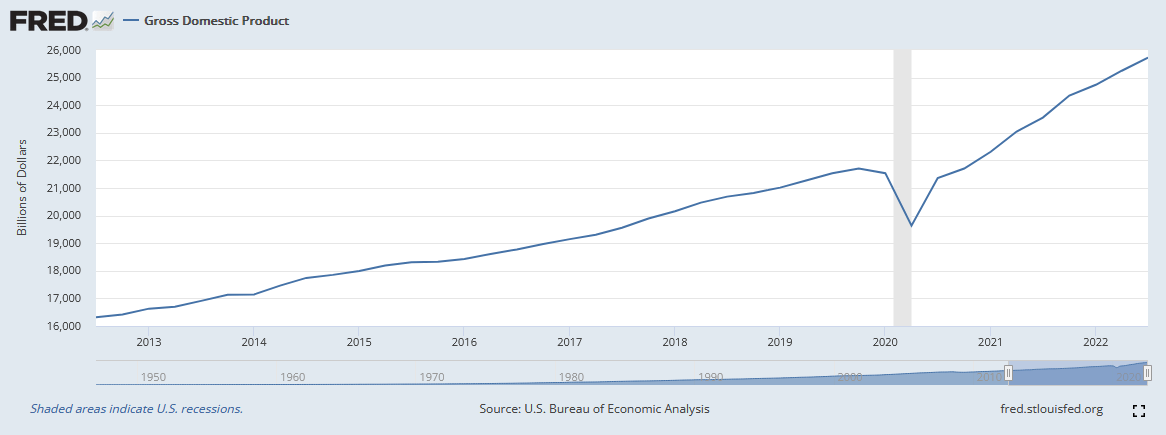

As I have stated throughout this article, one of our biggest reasons for including real estate in our portfolios is the protection that it can provide against the ravages of inflation. In order to understand the reason for this, it is critical to understand the cause of inflation. Economists generally state that inflation is a naturally occurring phenomenon. However, it is actually caused by the money supply growing faster than the production of goods and services in the economy. This has been the case over the past decade, which we can see by comparing the gross domestic product to the money supply.

This chart shows the gross domestic product, which measures the production of goods and services in an economy, for the United States over the past ten years:

{kind=link}

As we can see here, the gross domestic product of the United States went from $16.31954 trillion in the third quarter of 2012 to $25.723941 trillion today. That works out to an increase of 57.63% over the ten-year period. This is not too shabby.

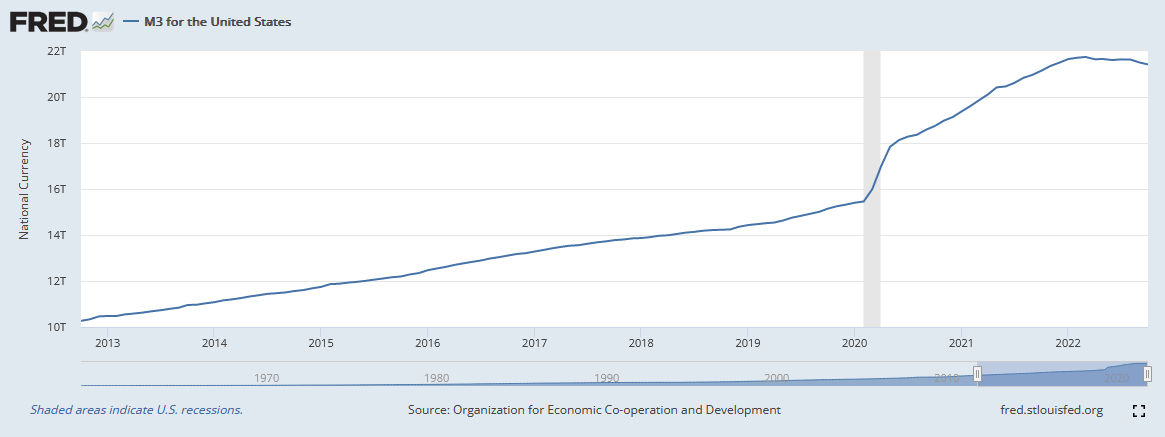

This chart shows the M3 money supply, which is the most comprehensive measure of the supply of money in the economy, of the United States over the same period:

{kind=link}

As shown here, the M3 money supply went from $10.2673 trillion in October 2012 to $21.4152 trillion in October 2022. We can see the effects of the Federal Reserve’s monetary tightening in 2022 as the money supply began to decrease but overall, the trend was very strongly positive, with the money supply increasing dramatically in 2020 and 2021 as the government unleashed unprecedented amounts of stimulus in response to the COVID-19 pandemic. The money supply increased by 108.58% over the ten-year period, obviously substantially more than the productive growth of the economy.

This is the very definition of an inflationary environment. This is because the amount of money available to purchase each unit of economic output has increased. Real estate shares many of the same characteristics as everything else that increases in price during inflationary times. In particular, real estate is in limited supply and it requires real human or mechanical effort to create or improve. Unlike fiat currency, a person cannot just push a button on a computer and cause an island to appear or a house to suddenly be created out of thin air. Thus, as the money supply increases, more money will be available to purchase each unit of real estate and it should therefore hold its value reasonably well over the long term.

Leverage

Earlier in this article, I stated that closed-end funds have the ability to employ certain strategies that can give them a higher yield than any of the underlying assets boasts. One of the strategies that are employed by the Neuberger Berman Real Estate Securities Income Fund is the use of leverage. Basically, the fund borrows money and uses that borrowed money to purchase real estate securities. As long as the yield of the purchased securities is higher than the interest rate paid on the borrowed money, the strategy works pretty well to increase the overall yield of the portfolio. As the fund can borrow at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This is one possible reason why the fund has underperformed the index so severely over the past year. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund’s leverage above a third of its assets for this reason. The Neuberger Berman Real Estate Securities Income Fund meets this requirement as its levered assets only comprise 26.15% of the portfolio. Thus, despite the negative impact that the leverage certainly had on it over the past year, the fund is striking a fairly reasonable balance between risk and reward.

Distribution Analysis

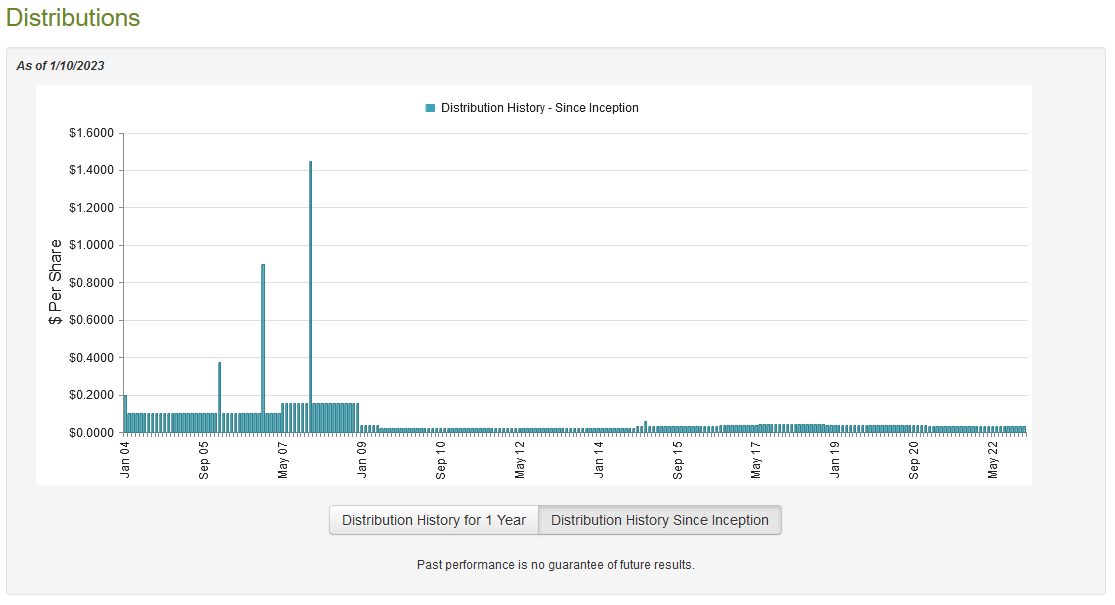

As stated earlier in this article, the primary objective of the Neuberger Berman Real Estate Securities Income Fund is to provide its investors with a high level of current income. In order to achieve this objective, it invests in a levered portfolio of real estate securities, which themselves tend to have a fairly high yield. As such, we might assume that the fund will boast a fairly impressive yield itself. This is indeed the case as the fund currently pays out a monthly distribution of $0.0312 per share ($0.3744 per share annually), which gives the fund an 11.08% yield at the current share price. Unfortunately, the fund has not been particularly consistent above this distribution over the years as it has been reducing it since 2018 but it has maintained its current level since early 2021:

{kind=link}

This somewhat disappointing distribution history might be something of a turn-off for those investors that are looking for a safe and secure source of income with which to use to pay their bills and finance their lifestyles. However, it is important to keep in mind that anyone purchasing the fund’s shares today will receive the current distribution and the current yield so the past is not really that important.

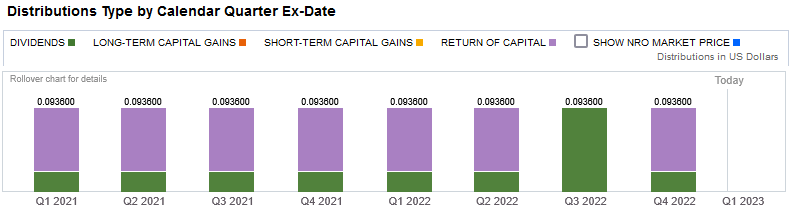

One potential point of concern though is that the fund has been making a large number of return of capital distributions recently:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital. One of these is the distribution of unrealized capital gains, which is something that the fund might do. Thus, we should have a look at the fund’s finances in order to determine how sustainable its distributions are likely to be.

Fortunately, we have a very recent document that we can consult for that purpose. The fund’s most recent financial report corresponds to the full-year period ending October 31, 2022. This is a much more recent report than we had available the last time we looked at the fund and the date works pretty well since it should be able to provide us with a great deal of insight into how well the fund handled the first few rate hikes, which were overall the most damaging to stock market valuations. During the full-year period, the fund received a total of $8,704,669 in dividends and $18,208 in interest from the assets in its portfolio. Once we net amount a very small amount of money that the fund had to pay in foreign withholding taxes, it had a total income of $8,720,691 over the year. The fund paid its expenses out of this amount, which left it with $4,229,355 available for investors. This was nowhere close to enough to cover the $17,764,507 that the fund actually paid out in distributions during the period. At first glance, this is quite likely to concern any reader as the fund’s income is insufficient to maintain the distribution.

However, the fund does have other methods that it can use to obtain the money that it needs to pay for the distribution. One of these methods is by earning and paying out capital gains. As might be expected though, the fund failed miserably at this task during the period. It did manage to achieve net realized gains of $5,661,644 but this was more than offset by $80,085,703 net unrealized losses. Overall, the fund’s assets went down by $87,897,556 during the period. This is concerning as it is very clear evidence that the fund’s distribution is not sustainable. In fact, its net investment income and net realized capital gains together were insufficient to cover the distribution. This might explain why the fund has a double-digit yield right now as there certainly looks like the distribution might be cut if the market does not improve in the very near future. Considering that the United States will almost certainly enter a recession during 2023, that is an unlikely prospect.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return from it. In the case of a closed-end fund like the Neuberger Berman Real Estate Securities Income Fund, the usual way to value it is by looking at the net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. That is fortunately the case with this fund today. As of January 10, 2023 (the most recent date for which data is currently available), the fund had a net asset value of $3.57 per share but the shares only trade for $3.47 a piece. This gives the shares a 2.80% discount to the net asset value at the current price. This is nowhere near as attractive as the 8.48% discount that the shares have averaged over the past month. Therefore, it might be a good idea to wait and see if the discount increases before purchasing shares of the fund.

Conclusion

In conclusion, the theme of the Neuberger Berman Real Estate Securities Income Fund is generally a good one, as real estate can serve an important role in a portfolio as both a store of wealth and a provision of income.

However, I can see a few flaws with this fund. In particular, the fund does not appear to be very well-positioned for the likelihood of economic hardships in 2023 based on the current positions in its portfolio. Perhaps most importantly, though, Neuberger Berman Real Estate Securities Income Fund is failing to cover its distributions and may be forced to cut in the near future. The Neuberger Berman Real Estate Securities Income Fund does have a reasonably attractive valuation, but it still might be better to wait for a bigger discount before buying in. Overall, I would take a pass on this one for now until the conditions improve.

For further details see:

NRO: Real Estate Makes Sense But This CEF Has Some Serious Flaws