NSA - NSA: An Update On Higher-Yielding Self-Storage

2023-11-19 08:07:18 ET

Summary

- The author owns shares in both Public Storage (PSA) and National Storage Affiliates (NSA), despite both being in the red.

- The author has increased their exposure to the self-storage sector due to attractive valuations, focusing on NSA and PSA.

- NSA is a good company with a better yield than PSA, but is expected to have a decline in FFO over the next two years.

Dear subscribers,

I recently updated on Public Storage ( PSA ) - and now I'm also going to update on National Storage ( NSA ). I own shares in both of these businesses. Both of my holdings are currently in the red, but this does not bother me particularly. Much of the market is going in the red these days, and my worry or concern is making sure that I invest capital at attractive rates with a good long-term upside , not necessarily what happens in the next few months or so.

When last reviewing National Storage Affiliates , I made a point of not, at the time, having massive exposure to the self-storage space. Since that time, I've allowed myself increased exposure based on attractive valuations. I've taken advantage of companies, including NSA, dropping as the pressure on the market has increased. I'm not talking about the self-storage market specifically, but all markets.

My choices here have been NSA and PSA - and these are also the primary investments I continue to focus on in this sector.

In this article, I'll show you why I continue to view these as favorable choices even on a forward basis.

National Storage - Not as qualitative as PSA, but still a good company with an even better yield

There are a few key differences between NSA and PSA. One of the primary relevant ones is that NSA, unlike PSA, isn't estimating growth for the next two years, but an FFO decline.

NSA's facilities and capacities exist pretty much across the entire USA under a mix of wholly owned and JV properties - 1,100 of them to be exact, amounting to 71.5M square feet of storage space. The lion's share of that space is found in the west and east, with more in Texas and the states adjacent to Texas.

While the idea that NSA was facing fundamental or foundational issues was dispelled by the 1Q23 and the most recent set of overall earnings results, there are fewer ideal plays and trends at work here, that seem to make sure that NSA is going to be declining low to mid-single digits in FFO over the next 2 fiscal years, including 2023E, with an emphasis on a front-loaded FFO decline in 2023.

2024E is currently estimated, due to rates and other trends, to bring about a 0.38% decline - more of a rounding error than anything else.

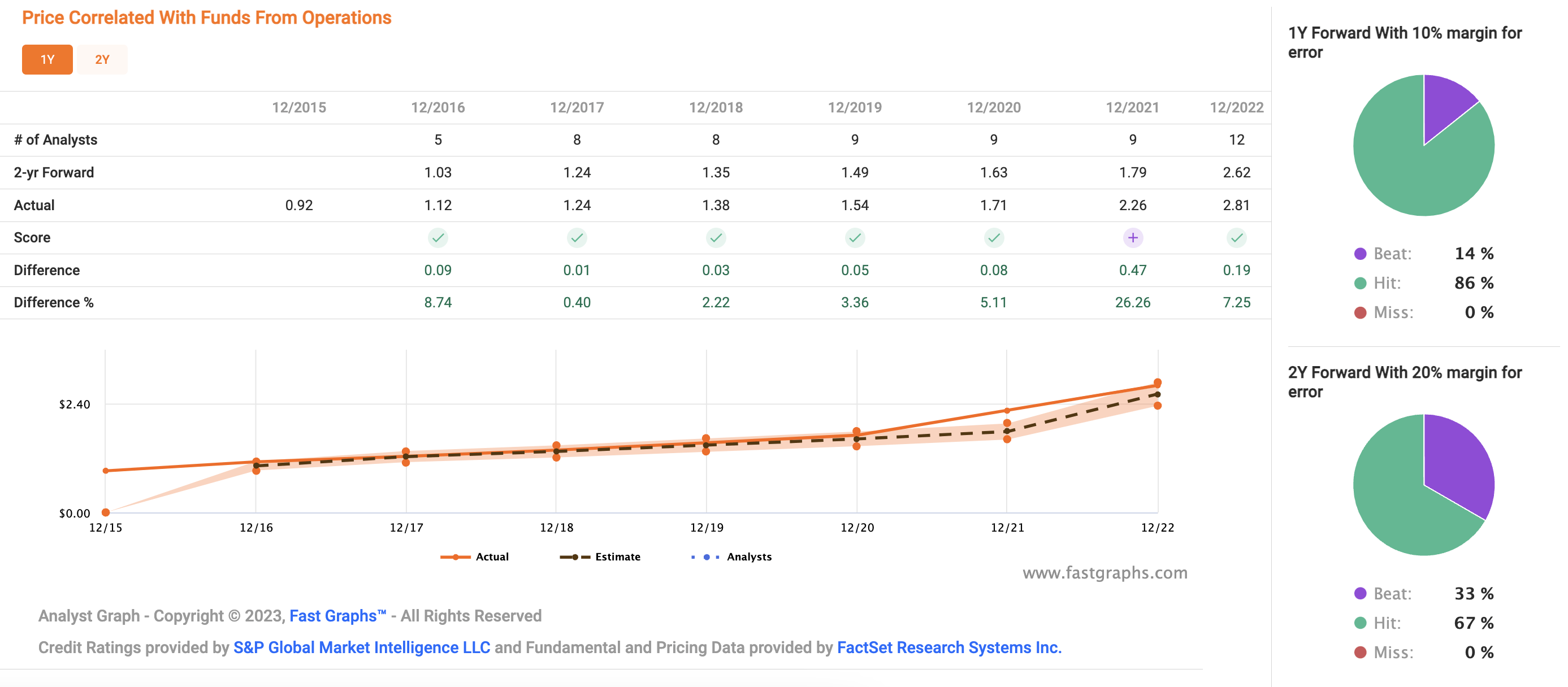

NSA has some of the same appealing trends as PSA, with a tendency to outperform/beat or at least manage its estimates - though NSA has far less history of doing so than the former has.

NSA Forecast accuracy (F.A.S.T graphs)

{kind=link}

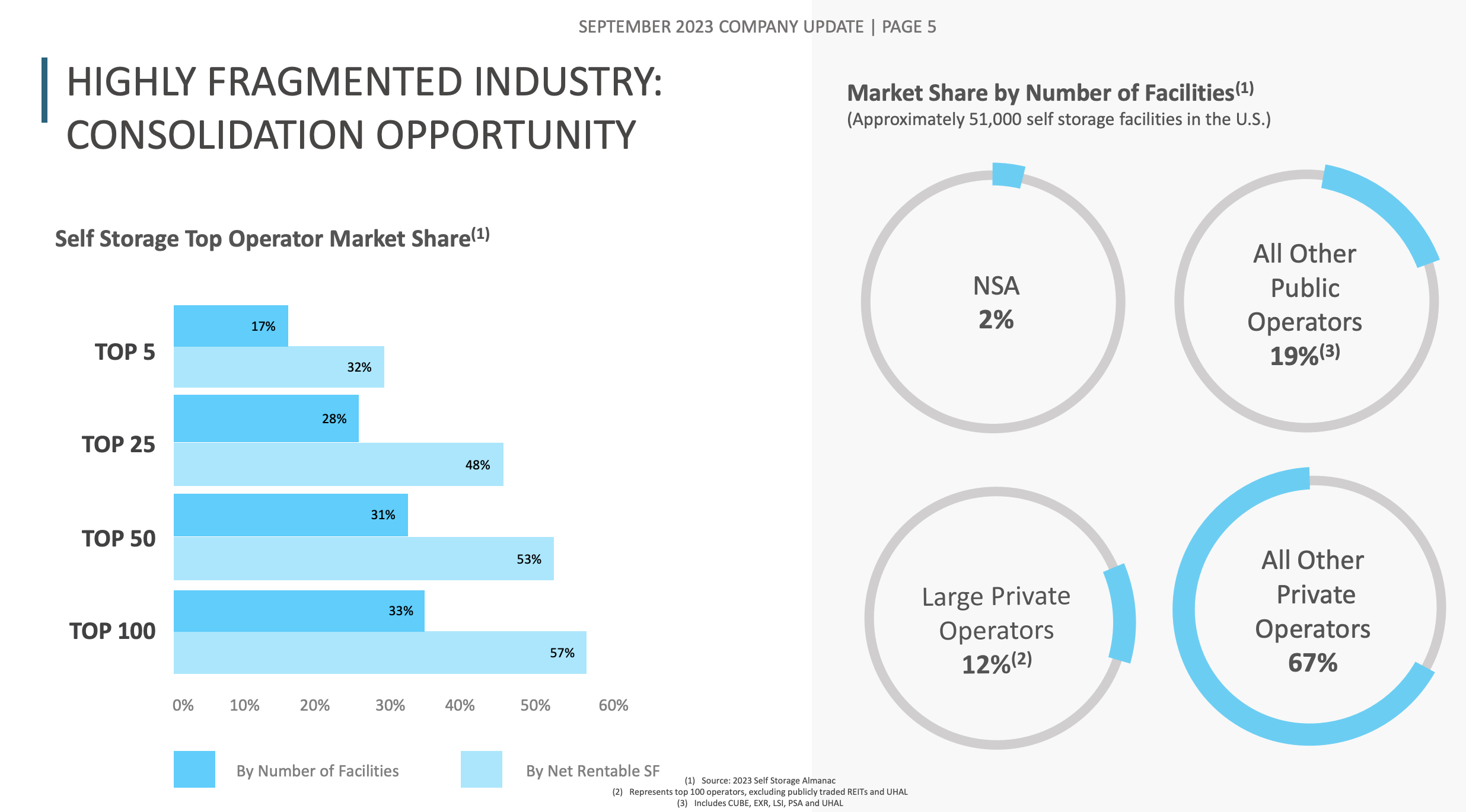

The two companies are very comparable. NSA is basically worse, slightly, in every metric compared to PSA, except in a few such as yield. It's a good example of how woes in a sector impact those players with significant scale far less than those lacking any sort of scale. I'm not saying NSA doesn't have scale, but I am saying it has far less than PSA.

NSA is barely 2% of the self-storage sector - but most operators in this sector are private. Even with PSA included, public operators only account for 19% of the entire market.

{kind=link}

The arguments that "work" for other self-storage businesses, certainly work for NSA as well. It's a far more resilient sector than most other REIT sectors. It has in fact proven this for almost 30 years - and NSA is part of this trend. The only sectors in REITs that can even be remotely compared to self-storage is Industrial and Apartments in terms of their RoR and low volatility.

As of 2Q23, NSA manages over $9B of TEV, with a 2.8% same-store revenue growth YoY, and a 3.4% NOI same-store growth with a 90% occupancy rate, while declining 4.2% in FFO per share YoY. This is more or less in line with the current expectations of an overall decline for the company.

The dividend is higher. At the current valuation, we're approaching 7.8%, which makes this comparable to many high-yielding appealing stocks. If you already have full positions in those stocks, and consider the company safe, then this business can certainly qualify as an investable business here, almost on yield alone.

The notion that NSA is going to see a significant fundamental decline is one I am strongly opposed to. Nothing in the numbers or estimates implies this. Small declines and pressure, more than other companies due to scale, yes. Significant and fundamental turn making the dividend unsustainable and growth impossible, absolutely not. That's not where we are.

It's worth noting that we've seen non-trivial declines in occupancy, with 450 bps declines, and changes in street rates approaching double digits - but so far, the stickiness of the company's properties, rents, and other customers are keeping results at a high level. Its focus is on growing markets like the sun belt, and the lack of a double-digit L.A exposure such as PSA also helps.

Risks mentioned in some analyst commentaries are concerned with the company's valuation given the current risk-free rates and the guidance decline we've seen during this year. These are valid notes if perhaps slightly more on the short- to mid-term than for the long term. In the longer term, I believe the company's appeal will cause a valuation reversal.

Also, given the current valuation, which is close to 5x P/FFO lower than that for PSA, I believe the discounting for this company should be "done" here. In my work, I don't even estimate it going back up to a premium such as the one we're seeing for PSA - I forecast it at significantly lower rates, and that's something that becomes even more necessary now given the estimates for the next 3 years in terms of returns.

The foundation for what made the company an attractive investment is not only still present, it's increased from the last time around given the significantly lower valuation here.

We're starting to get an impact forecast accuracy for what the OpEx increases will end up in.

Here is the valuation we have for the company, and what we can see as the thesis here.

National Storage Affiliates - a lot to like at 10x P/FFO.

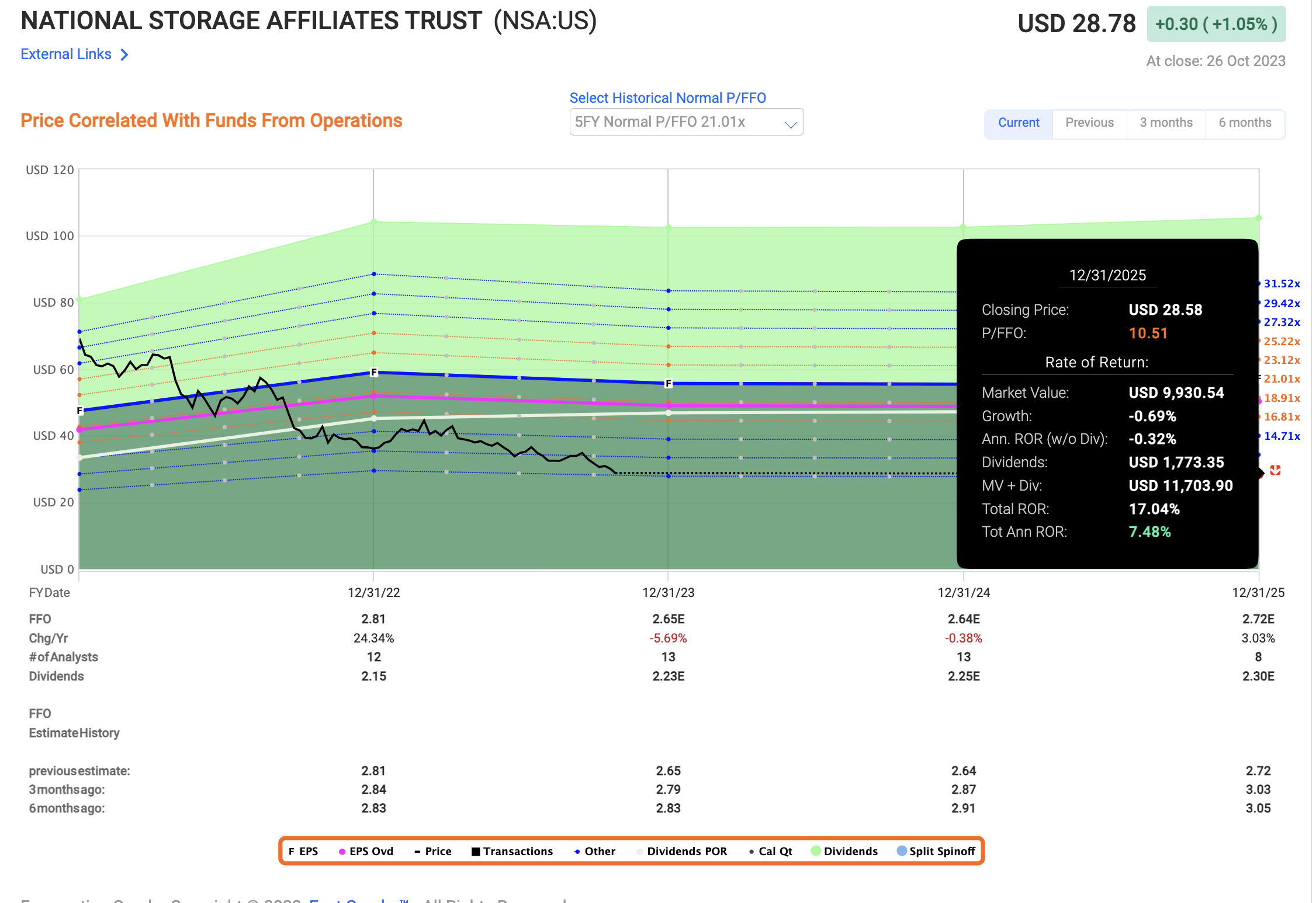

NSA is currently trading at a measly 10.7x. Thanks to the yield, which comes at a relatively good coverage ratio - not market-beating, but not anywhere I would consider it in danger at 84% in terms of current FFO, which includes a 5.7% FFO decline for this year. This means that even if you were to forecast NSA at a lower P/FFO than it's trading today, you would not be losing money.

{kind=link}

And before you say that 7% isn't interesting to you, that's based on a lower actual forward P/FFO than we're currently having.

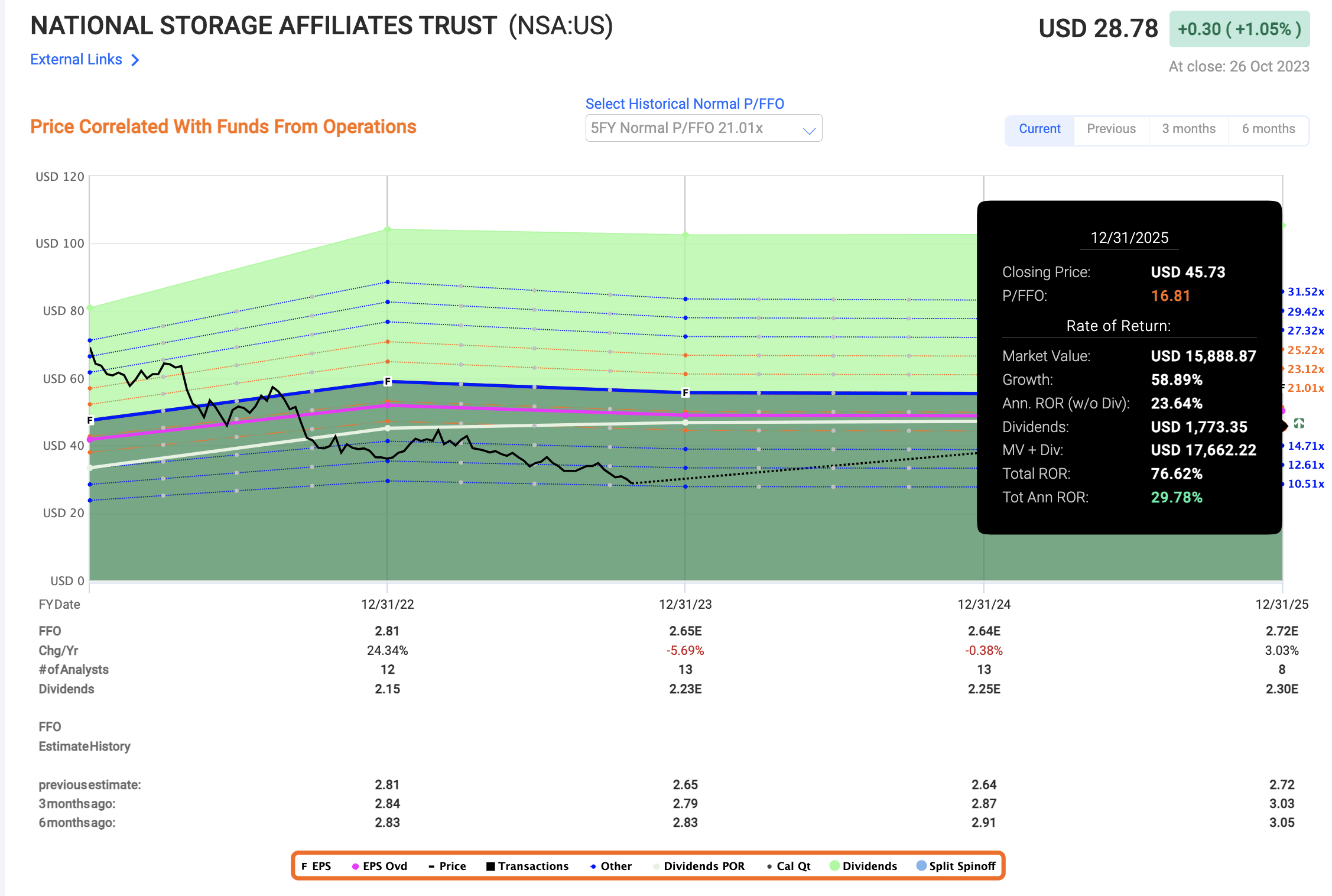

The upside, in case of any sort of reversal, is obviously more attractive here. I won't tell you that I consider the company worth a significant premium - in fact, I'll estimate it below 15x P/FFO, compared to 20x+ which I give for Public Storage - but even on a 14.7x P/FFO, the comparable upside here on current estimates is almost 23% per year, or 56% RoR until 2025E, with an implied share price of $41/share. My estimated share price for the long term is even higher than that, at $50/share, which puts us slightly above 17x, meaning we're discounting somewhat to PSA, but not as much implying a 30% annualized RoR until 2025E.

I justify this by saying that NSA has never failed to meet an estimate and seems to have an actual good chance of beating estimates. I justify it by saying that while macro is problematic, and a 4%+ occupancy decline is significant, the company doesn't seem to be declining much more than that here, and the 5% seems to be indicative here.

Every indication is that NSA continues to show substantial discounts at this level. There isn't much to be said as to a continued bearish or negative case here, with a further downside. It could happen - valuations can disconnect, during times, completely from their historical levels. I don't see a reason for this, however. This doesn't mean it won't happen, but it means I consider it unlikely at this point.

If we start seeing the types of valuation disconnects that we might see in the office sector at times, then I'll be very interested in adding more here. It's important for me to be clear that I'm not buying big chunks - as with many companies and many sectors, I'm adding relatively slowly here.

We're currently in a downward spiral in a non-trivial manner. While I have no doubt that we'll see a turnaround, what exactly will be the catalyst and when it comes, that's less clear. NSA has seen 1-year returns of negative 27% here, which is significant.

{kind=link}

Analysts have gone sour very quickly on this company. Back when I started covering the company, a high-end PT of $73/share and an average of $61 was the standard for S&P Global.

Today we are down to a high of $38/share and an average of 34. Despite the company being very cheap for what it offers, only 2 analysts are at "BUY" here - compared to the 6 prepared to "BUY" the company when it was trading at over $41/share.

I could slightly adjust my price target here - but for now, I'm sticking to it, because these negative trends were actually something I accounted for in my initial estimate.

For now, NSA is a "BUY" with what I see to be a significant undervaluation.

Thesis

-

NSA is the "smaller sibling" of market leaders like PSA. It operates in the same sector but has a better yield and more upside due to a more compressed overall valuation.

-

NSA may be a higher risk/reward play than PSA and similar REITs, but it also would be unfair to characterize the company as a somehow "excessively risky" investment. Its portfolio and sector have outperformed for years, and I forecast the self-storage industry to make money for decades to come - there is little to suggest this is going away, even if it's going down in growth.

-

Based on this, I would call NSA a "BUY" with a PT of $50/share, but no more than that. I'm not changing my PT as of this article.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I believe NSA fulfills every single investment criterion I hold, even without a CR, and that makes it a "BUY". I'm buying more NSA here, and slowly expanding my self-storage exposure.

For further details see:

NSA: An Update On Higher-Yielding Self-Storage