DTM - NTG: This 8.65%-Yielding Midstream Fund Is Trading At A Huge Discount

2023-08-24 08:07:42 ET

Summary

- Tortoise Midstream Energy Fund is a closed-end fund that primarily invests in midstream companies, offering a diversified portfolio for investors.

- The fund currently yields 8.65%, slightly higher than the Alerian MLP Index, but not as much as desired.

- NTG has seen a respectable 3.43% year-to-date return and could see price appreciation if oil prices continue to rise.

- The fund's portfolio is primarily allocated to natural gas infrastructure companies, which have better growth potential than crude oil ones over the coming years.

- The distribution appears to be sustainable and the fund is currently trading at an enormous discount to its intrinsic value.

The Tortoise Midstream Energy Fund ( NTG ) is a closed-end fund that invests primarily in midstream companies. While it is, admittedly, not one of the most popular funds in the sector, it does come from a fund house that has long been known for its master limited partnership and midstream infrastructure funds. These funds can prove quite attractive for retirees or others who are looking to include midstream companies in their retirement accounts because they overcome some of the tax problems of doing this. That is, however, not as important a benefit as it once was due to the fact that many midstream companies have restructured into corporations themselves so they no longer have the tax problems that accompany the master limited partnership structure. The biggest benefits are the fact that the fund can offer any investor a diversified portfolio of midstream companies and that it can employ certain strategies that allow it to boost the effective yield of its portfolio.

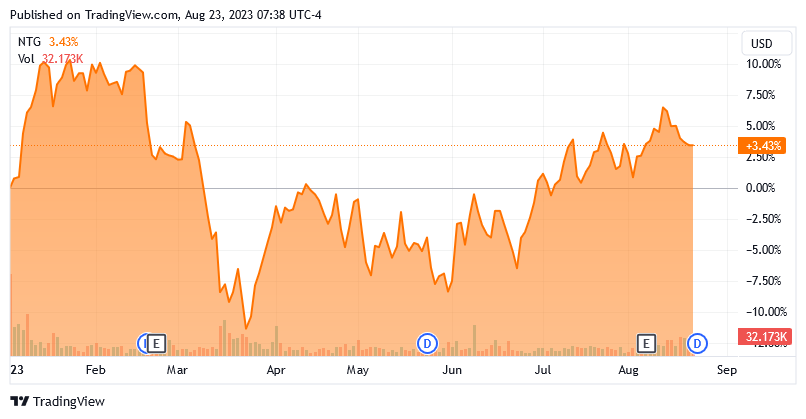

Unfortunately, right now the fund only yields 8.65%, which is a bit more than the 8.13% of the Alerian MLP Index ( AMLP ), but the difference is not as much as we would like. The fund is up a respectable 3.43% year-to-date though, so investors in it have gotten a nice total return so far:

{kind=link}

Admittedly, it is not as good of a performer as the S&P 500 Index ( SPY ) has been so far this year, but it does not aim to be as this fund delivers a much higher proportion of its total returns in the form of its distributions. It could certainly see some price appreciation if oil prices keep rising, however, which seems likely to be the long-term scenario.

As some readers likely recall, we previously discussed this fund back in April. Our overall conclusion at that time was that the fund appeared to be a fairly good way to add master limited partnerships and midstream energy corporations to your portfolio without having to deal with all of the tax hassles. The fund also boasted a 9.35% fully covered yield at the time. While the yield is a bit lower now, the fund might still be a reasonably good addition to a portfolio today. Let us investigate this, focusing specifically on the changes to the fund's portfolio since that time and updating ourselves with the new financial information that the fund released recently.

About The Fund

According to the fund's webpage , the Tortoise Midstream Energy Fund has the objective of providing its investors with a high level of total return. That is not particularly surprising, considering that the fund's portfolio is invested primarily in common equities. We can see that here:

CEF Connect

As we can clearly see, the fund's portfolio is currently 98.82% invested in common equity with only small allocations to preferred and cash. This is not unusual for a midstream energy fund as midstream companies are one of the few types of companies that issue preferred equity to any significant degree. The fact that the fund includes preferred equity does not bring it any particular advantages over an all-common equity fund, however. One reason for this is obviously that the preferred allocation is too small to make a noticeable difference. The second reason is that the common equity of midstream companies frequently boasts higher distribution yields than the preferred equity issued by the same company. This is the only sector in which this is the case. For example, Crestwood Equity Partners ( CEQP ) yields 9.51% but the preferreds ( ceqppr ) yield 8.95% as of the time of writing. Up until recently, this was also the case with NuStar Energy ( NS ) and its preferred units, but now that the Series C preferreds (NS.PR.C) are floating rate, they have a higher yield. The takeaway here is that the inclusion of preferred units in the fund does not really boost its income compared to owning the common equity of many of these companies.

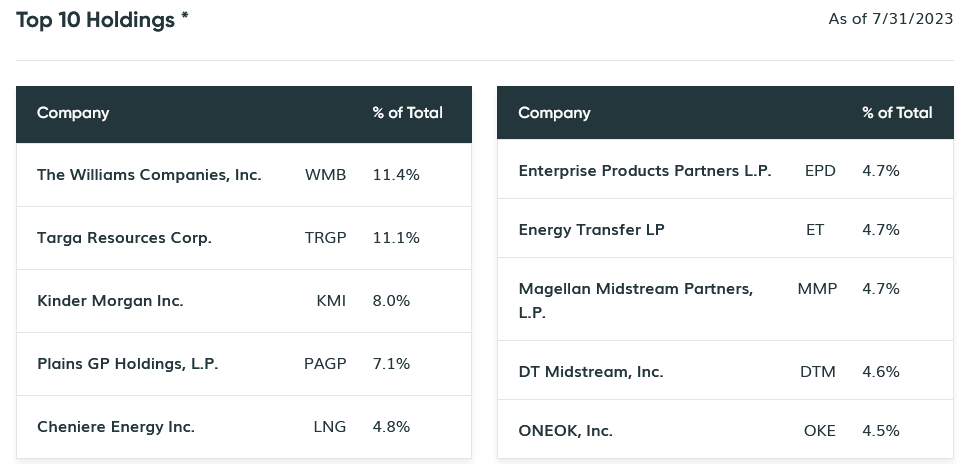

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing midstream partnerships and corporations both on Seeking Alpha and my service. As such, the majority of the companies that comprise this fund's largest positions will likely be somewhat familiar to most readers. Here they are:

{kind=link}

I have discussed every company on this list multiple times over the past decade or so here at Seeking Alpha. The one exception to this statement is Plains GP Holdings, L.P. ( PAGP ), but that is just the general partner of Plains All American Pipeline ( PAA ). I have discussed the latter company many times over the years. As such, most of these companies should be familiar to regular readers.

For the most part, the fund has made some good selections here with the companies that comprise its largest positions. The Williams Companies ( WMB ), Targa Resources ( TRGP ), Cheniere Energy ( LNG ), and Energy Transfer ( ET ) are all positioned to deliver growth over the coming years as natural gas demand rises both domestically and abroad. We have discussed this trend numerous times in the past, but in short, utilities are using natural gas turbines to supplement unreliable renewable sources of energy. The United States is one of the few nations that has sufficient natural gas reserves to meet the demand growth that will come about as a direct result of this trend. All of the companies mentioned are among the biggest pipeline operators or natural gas exporters in the United States and so all should see rising demand for their services going forward. Please refer to my articles on each individual company for more information.

There have been relatively few changes to the fund's positions since we last discussed it back in April. In fact, the only major changes were that Canadian midstream giants Pembina Pipeline ( PBA ) and Enbridge ( ENB ) were both removed from the fund's largest positions. In their place, we see Magellan Midstream Partners ( MMP ) and DT Midstream ( DTM ). There have also been a number of weighting changes, but that could be caused by one company outperforming another in the market. It is not necessarily a sign that the fund is actively trying to change its weightings. However, the fund still has a 72.67% annual turnover, so it is not particularly low for a midstream fund. I described the importance of this in my last article on the company:

The reason that this is important is that it costs money to trade stocks or other assets, and these costs are billed directly to the fund's shareholders. That creates a drag on the performance of the portfolio and makes management's job more difficult. After all, the fund's management must generate sufficient returns to cover these added expenses and still have money left over for other purposes. That is something that very few management teams manage to accomplish on a consistent basis, which results in most actively-managed funds underperforming their benchmark indices over the long term."

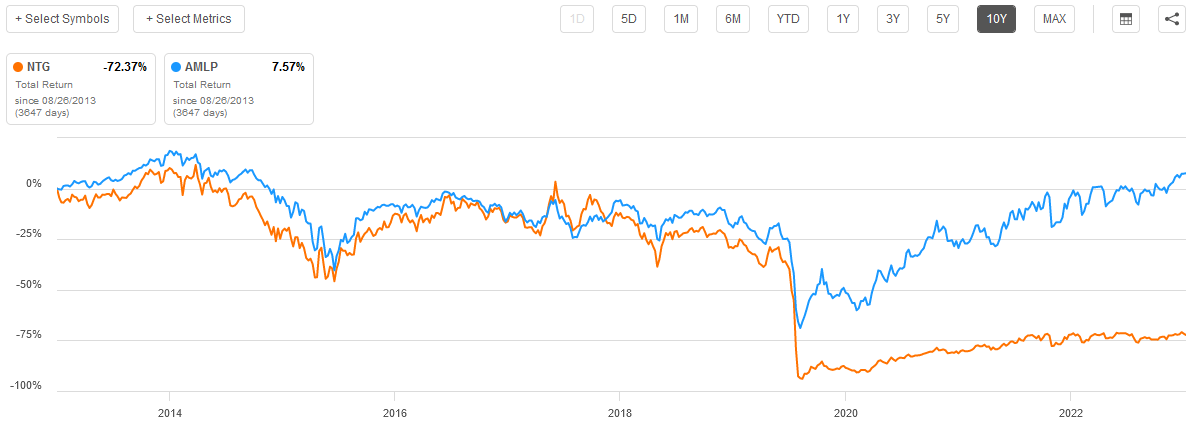

For its part, the Tortoise Midstream Energy Fund has underperformed the Alerian MLP Index by quite a lot over the past ten years. This chart shows the total return of both assets over the period:

{kind=link}

The Tortoise Midstream Energy Fund delivered a negative 72.37% return over the period, which is incredibly discouraging no matter how you want to consider it. We can see though that virtually all of that underperformance was caused by the fund's precipitous decline in 2020 when the pandemic hit and crashed energy prices. Prior to that event, its total returns were pretty similar to the index. That has been the case since then as well. Here is the three-year total return chart:

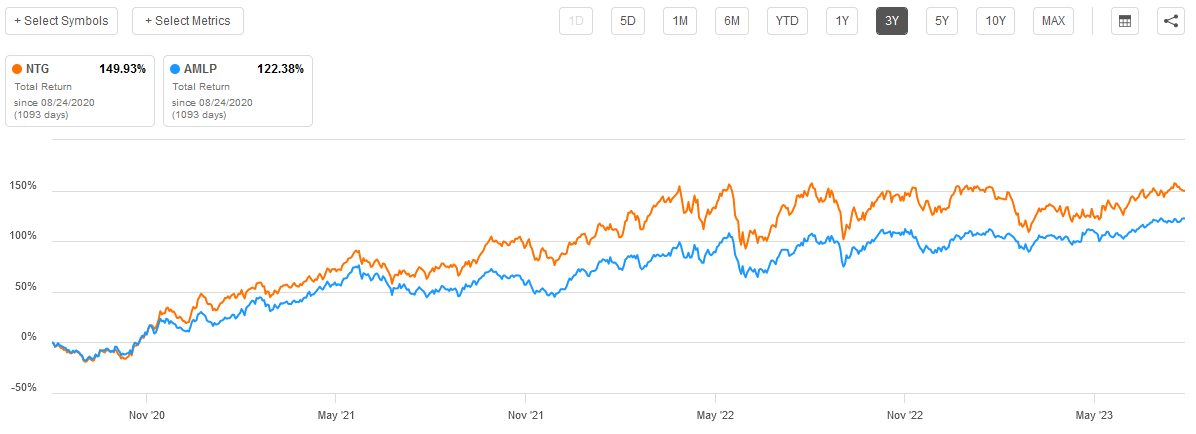

{kind=link}

Here we can see that the Tortoise Midstream Energy Fund managed to beat the Alerian MLP Index over the period. Both the 2020 underperformance and the outperformance since then were probably at least partly due to the closed-end fund's use of leverage, which boosts both gains and losses. We will discuss that more later in this article.

One other important thing to note is that the Alerian MLP Index is not a perfect benchmark index for the Tortoise Midstream Energy Fund. One reason for this is that the Tortoise Fund includes midstream corporations that are not going to be included in the index. That can affect performance significantly since most activist investors (such as Elliott Investment Management) believe that corporations outperform master limited partnerships overall. This is mostly due to the fact that large institutional investors, such as most mutual funds, have restrictions on their ability to invest in master limited partnerships. That reduces the demand for these companies relative to midstream corporations. When this is combined with the fact that the Trump corporate tax cuts reduced the tax appeal of master limited partnerships, it should be fairly obvious how there would be very different performance differences between the two types of business structure. The Alerian MLP Index does not include midstream corporations, but the Tortoise Midstream Energy Fund does. That results in the two assets having different performance characteristics, so it is not a perfect benchmark.

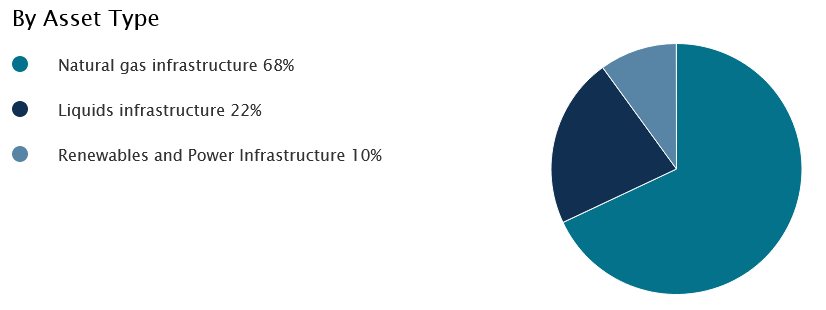

As was mentioned earlier, many of the assets that comprise the fund's largest positions are much more heavily focused on the natural gas space than the crude oil space. This should be immediately obvious to anyone that is familiar with the midstream sector. That extends throughout the rest of the fund as well:

{kind=link}

I am certainly not opposed to this. As I have pointed out numerous times, natural gas midstream companies will probably make better long-term investments than crude oil ones going forward. However, the market seems to realize this as well, and as such crude oil midstream companies tend to have higher yields. For example, consider the largest positions in the fund's portfolio:

| Company |

| Product |

| Current Distribution Yield |

| The Williams Companies |

| Natural Gas |

| 5.17% |

| Targa Resources |

| Natural Gas |

| 2.39% |

| Kinder Morgan ( KMI ) |

| Diversified/Both |

| 6.55% |

| Plains GP Holdings |

| Crude Oil |

| 6.42% |

| Cheniere Energy |

| Natural Gas |

| 0.95% |

| Enterprise Products Partners ( EPD ) |

| Diversified/Both |

| 7.58% |

| Energy Transfer |

| Diversified/Both |

| 9.56% |

| Magellan Midstream Partners |

| Crude Oil |

| 6.37% |

| DT Midstream |

| Natural Gas |

| 5.11% |

| ONEOK ( OKE ) |

| Diversified/Both |

| 5.89% |

We can clearly see that most of the companies that are exclusively natural gas tend to have lower yields than the ones that handle both natural gas and liquids or liquids exclusively. This is almost certainly because the market realizes that natural gas is likely to deliver more forward growth. After all, midstream companies are frequently priced based on their yield as opposed to metrics like price-to-earnings or price-to-cash flow. The fact that the fund is investing in both of them with a preference to natural gas seems to imply that it is trying to get growth while maintaining its crude oil exposure for the income potential. That is not a bad strategy right now, particularly considering that it needs to beat the 5% yield of a money market fund in order to be at all attractive to income-seeking investors.

Leverage

As stated earlier, the Tortoise Midstream Energy Fund employs leverage, which is a commonly used strategy by closed-end funds to boost their yields. I provided an explanation of how this works in my previous article on this fund:

In the introduction to this article, I stated that closed-end funds like the Tortoise Midstream Energy Fund have the ability to generate a higher yield than any of the underlying assets actually possess. One way through which this is accomplished is the use of leverage. In short, the fund borrows money and then uses this borrowed money to purchase the common equity of master limited partnerships [and midstream corporations]. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As the fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is somewhat less effective today with rates at 6% than it was eighteen months ago when rates were basically 0%. This is because the difference between the borrowing rate and the yield that the fund can obtain from the purchased asset is a lot narrower than it once was.

However, the use of debt in this fashion is a double-edged sword. This is because equity boosts both gains and losses. This could, therefore, be one reason why the Tortoise Midstream Energy Fund tends to decline much more than the index during periods of market weakness. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I usually like to see a fund's leverage remain under a third as a percentage of its assets for this reason."

As of the time of writing, the Tortoise Midstream Energy Fund has levered assets comprising 21.68% of its portfolio. This is actually a bit lower than the last time that we discussed the fund, which is probably due to the increase in the value of midstream assets over the past few months. As was the case before, this is a very reasonable balance between risk and reward. We should not really be too concerned here.

Distribution Analysis

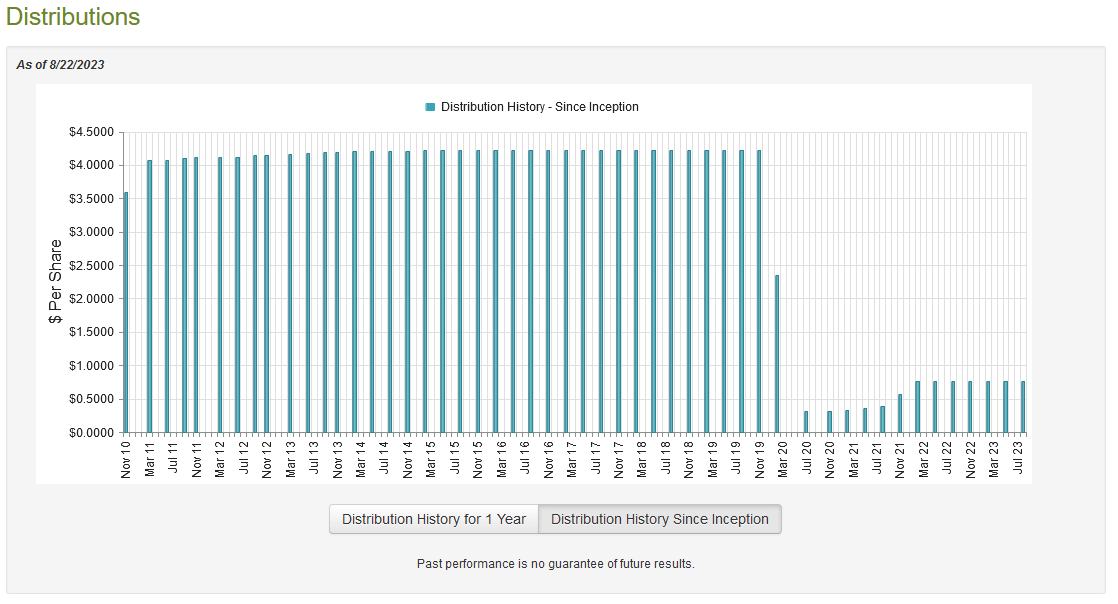

The Tortoise Midstream Energy Fund has the objective of providing its investors with a high level of total return. However, most midstream companies tend to be somewhat limited as far as capital gains go. This is partly due to the market not favoring traditional energy stocks in general and partly because the capital-intensive nature of their business limits their growth potential. As such, most of these companies provide the majority of their capital returns via direct payments to their investors. The fund naturally recognizes this, and even states on its webpage that the majority of its total return will be provided via distributions. The fund collects high yields from the assets in its portfolio and pays them out to its own shareholders. When we consider that the fund is using leverage to boost the effective return of its portfolio, we can naturally expect it to boast a very high yield. That is certainly the case, as the Tortoise Midstream Energy Fund pays a quarterly distribution of $0.77 per share ($3.08 per share annually), which gives it an 8.65% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over the years:

{kind=link}

The fund was actually doing reasonably well in terms of consistency until 2020 when it cut the payout sharply. The fund's reasons for doing this were quite reasonable (and explained in my previous article), but it still might prove to be something of a turn-off to anyone who is seeking a safe and secure source of income to use to pay their bills and finance their lifestyles. The fact that the fund has not returned its distribution to its previous level is perhaps even more disheartening, although it is quite understandable considering that its heavy losses in 2020 reduced the assets that it can use to generate returns.

Naturally, though, the most important thing for anyone buying today is the fund's ability to sustain its current payout. After all, if you purchase the fund today then you will not actually be affected by the fact that the fund has cut its payout in previous years. Let us investigate this.

Fortunately, we do have a remarkably recent document that we can consult for this purpose. The fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is therefore one of the most recent reports available from any closed-end fund. It is also newer than the report that we had available to us the last time that we discussed this fund, so it should give us a better idea of how well the fund has been performing recently and how sustainable its distribution is likely to be.

During the six-month period, the Tortoise Midstream Energy Fund received $2,314,827 in distributions from master limited partnerships, $5,691,880 in dividends, and $176,544 in interest from the various assets in its portfolio. Of this, we have to net out those distributions that were considered a return of capital, as well as all foreign withholding taxes that the fund had to pay during the period. When we do that, we see that the fund reported a total investment income of $4,251,225 during the six-month period. It paid its expenses out of this amount, which left it with $1,043,923 available for shareholders. As might be expected, that was nowhere close to enough to cover the distributions that the fund paid out during the period, which totaled $8,255,696. This is something that might be quite concerning at first since the fund did not have enough net investment income to cover its payouts.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. As already mentioned, the fund received substantial return of capital distributions during the period. These are not included in net investment income, but they still represent money coming into the fund. The fund might also have some capital gains that can be paid out. Fortunately, it did have some success at this as the fund reported net realized gains of $9,419,378 during the period. That was offset by $39,183,425 net unrealized losses, but the fund's net investment income plus net realized gains were still enough to cover the distribution. The real problem here is that the fund's assets declined by $36,975,820 after accounting for all inflows and outflows during the six-month period. That completely wiped out the asset increase that the fund managed to deliver in 2022 from the strong energy price environment. On December 1, 2021, the Tortoise Midstream Energy Fund had net assets of $200,841,388 but this was down to $200,045,803 on May 31, 2023. Overall, that decline probably is not a big deal and the distribution should be reasonably safe but we still want to keep paying an eye on the fund to ensure that this is the case.

Valuation

As is the case with most midstream infrastructure funds, the Tortoise Midstream Energy Fund is currently trading at a very large discount to its net asset value. As of August 22, 2023 (the most recent date for which data is currently available), the fund has a net asset value of $41.98 per share but the shares currently trade for $34.67 each. That gives it a 17.41% discount on net asset value at the current price. This is an enormous discount that is better than the 16.83% discount that the shares have averaged over the past month. The price certainly looks right here.

Conclusion

In conclusion, the Tortoise Midstream Energy Fund continues to be a decent performer that has managed to outperform the Alerian MLP Index during the post-pandemic period. The fund appears to be focused on growth, considering that the majority of its assets are invested in natural gas infrastructure. The distribution yield is a bit higher than the index and it appears to be sustainable going forward. When combined with the very large discount, it might be reasonable to think about this fund today.

For further details see:

NTG: This 8.65%-Yielding Midstream Fund Is Trading At A Huge Discount