NUS - Nu Skin: 50% Downside Is Possible In 2023

Summary

- Our residual valuation model suggests that Nu Skin is overvalued by approximately 50%.

- Despite re-openings in China, Nu Skin's operations remain exposed to cyclical risks.

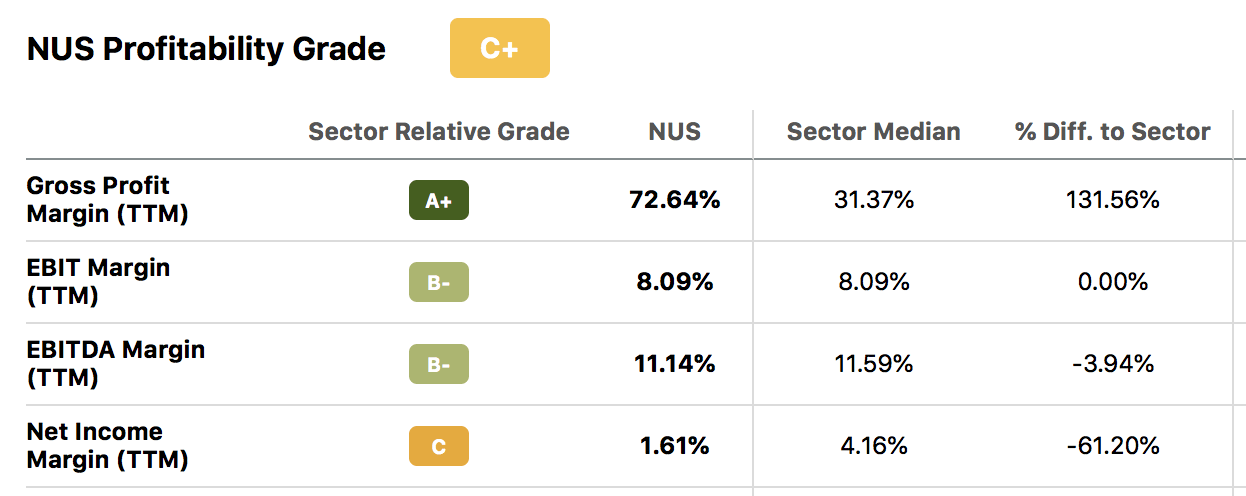

- The company's net margins are poor, and earnings crash risk is a regular feature.

- The stock's technical features imply that it could rebound in 2023. However, it presents an isolated case with little substance in the broader context.

Given re-openings in China and the company's recent earnings release, we thought an update on Nu Skin ( NUS ) would be prudent. Today's article assumes a valuation-based viewpoint with key operating updates phased into the analysis. Furthermore, the stock is assessed from a technical angle, which reveals a valuable juxtaposition.

So, without any further delay, let's jump into the analysis!

Operational Update

Since our latest coverage , Nu Skin delivered its third-quarter earnings results, which has left the market looking for direction. During its latest quarter, Nu Skin's revenue slumped by 16.1% year-over-year , and its gross margin receded to 67.7% versus 72.7% the year before.

Despite the firm's receding gross margins, we'd like to convey that the enterprise's normalized gross margin of 72.7% should take preference as its incurred restructuring charges and impairments can be considered abnormal.

Nu Skin's management sees challenging times ahead in 2023, stating that macroeconomic headwinds and currency translation risk could dent its prospects. The C-Suite's narrative shouldn't come as a surprise because consumer discretionary goods are exceptionally cyclical, which combined with 2023's recession risk could result in challenging times for the company.

A long-term concern that we have about Nu Skin relates to three of Porter's Five Forces, namely threats of new entrants and pricing power over customers. There's little doubt that Nu Skin's "social sales program" has been successful; however, it's a low barriers to entry concept, and we might easily see other brands with more lucrative product ranges doing the same in the coming years. Furthermore, the company's gross margins are robust; however, it needs to expand its gross profit in absolute terms to deliver better EBITDA, EBIT, and net margins. The only way to do this is to cut input costs or/and exercise higher product prices. Price elasticity is high in the cosmetics business, and it's unlikely that Nu Skin can sell at any higher than it currently is.

Inflation will likely ease some of the company's costs. Yet, more than a few percentage points are required for the firm to offer better residual value to its shareholders.

{kind=link}

Seeking Alpha

A final qualitative consideration is Nu Skin's earnings crash risk. Evidence suggests that stocks of companies with earnings crash risk struggle to garner long-term momentum and often lead to disappointing price returns.

{kind=link}

Seeking Alpha

{kind=link}

Seeking Alpha

Valuation – Residual Income Model

The residual income valuation model is considered an alternative to the renowned free cash flow model. The model is highly regarded in the financial world and often produces accurate price targets.

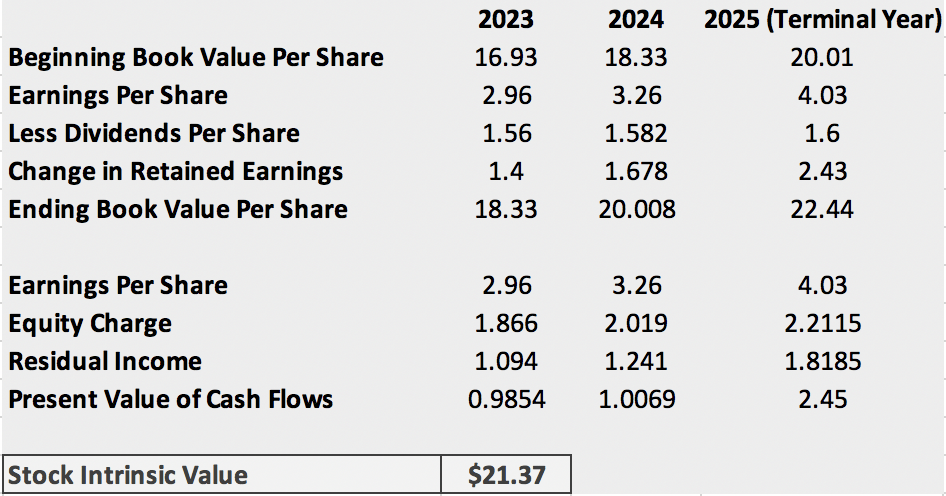

Our model indicates that Nu Skin stock is severely overvalued, with an intrinsic value per share worth merely $21.37. Even a margin of safety doesn't bring the asset's intrinsic value up to its traded stock price, which is currently above the $40 handle.

{kind=link}

Author's Calculations

Please consider that this model doesn't guarantee a price target. Instead, it's merely an indicator.

Here's how we constructed the model:

- Firstly, we used Seeking Alpha's database to determine Nu Skin's book value per share by dividing the stock's market price by its price-to-book ratio.

- After that, we pulled analysts' earnings-per-share targets from the same database, which we utilized to set a base for retained earnings. We subtracted the stock's annual dividend from its earnings-per-share to figure out the change in retained earnings. Take note that we assumed a 1.35% dividend CAGR, in line with historical growth.

- The change in residual earnings was added to the beginning book value per share. This acted as a foundation for determining the absolute equity charge (investors expected return) per share.

- Nu Skin's 11.02% cost of equity (CAPM) was derived from YCharts. The CAPM was multiplied by the beginning book value of each year to determine an equity charge.

- The residual income for each year was determined, whereafter, year 1 and 2 was discounted with the CAPM (we adjusted the CAPM for time). Although year 3's cash flow was adjusted using the same time-adjusted CAPM, we first determined a terminal value with the following formula: residual income in year 3/(1.CAPM - Persistence Factor)(1.time-adjusted CAPM). We used a persistence factor of 0.50, as we believe Nu Skin's 8.22% market share could result in its earnings remaining above industry standard into perpetuity.

- Our intrinsic value of $21.37 suggests we believe investors' future residual value will be lower than what the market currently believes.

- For more information about the residual income model, visit this link .

Potential Counterargument

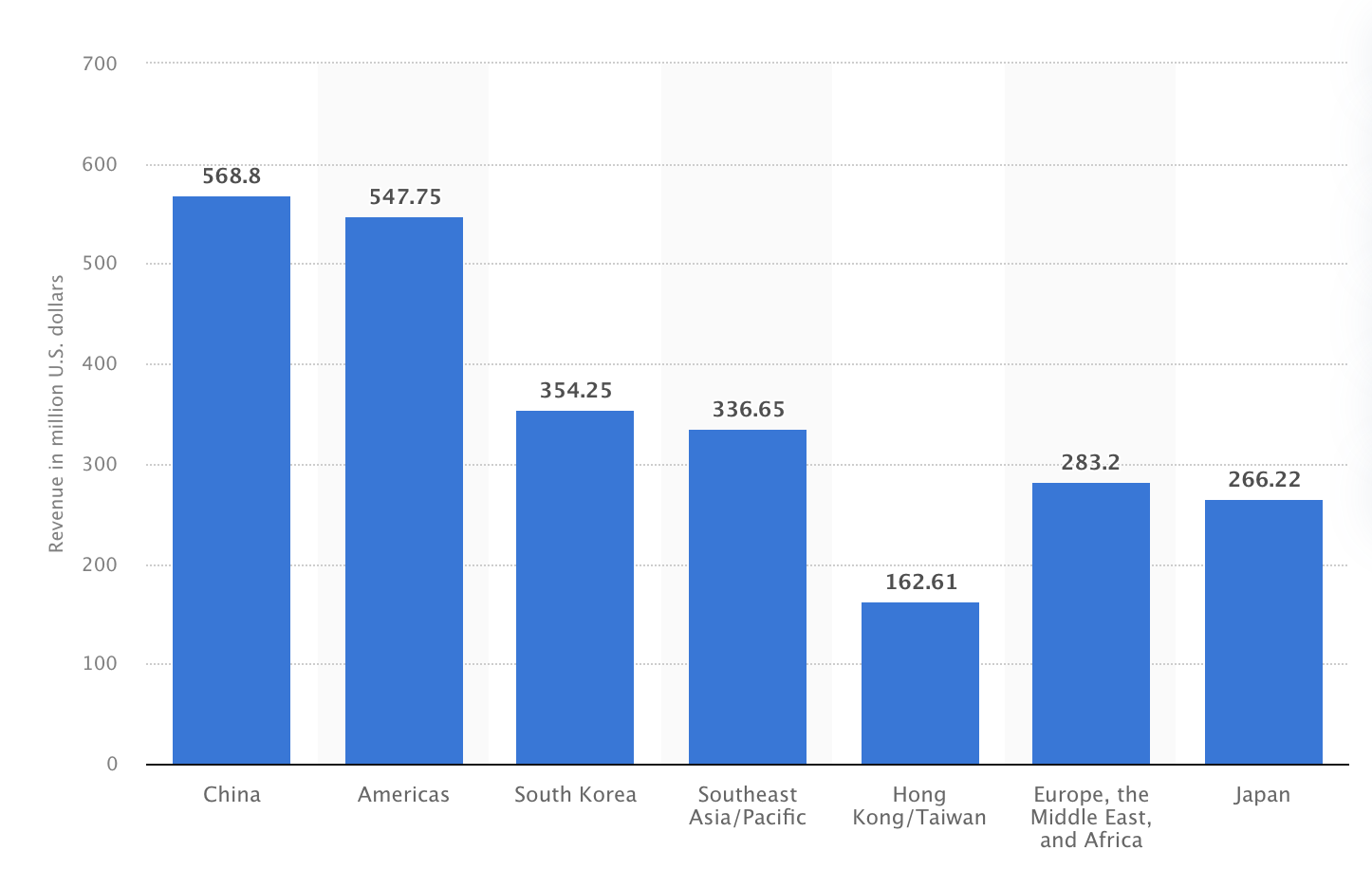

There's no debating the fact that Nu Skin is faced with numerous challenges. However, some positives are baked into the company's operating trajectory. For example, re-openings in China could play a significant role as the majority of the entity's revenue stems from China. A rejuvenated Chinese economy and a proclivity of consumers to spend on aesthetic items might certainly bolster Nu Skin's prospects.

{kind=link}

Revenue By Region (2021) (Statista)

Furthermore, the company's "Nu Vision 2025" goal remains intact. Integration of its new affiliate sales product LumiSpa iO with existing hot product lines such as ageLOC Meta and Beauty-focused Collagen+ could ramp up the firm's product-specific revenue potential.

Lastly, the stock received technical support towards the end of 2023 by trading above its 10-, 50-, and 100-day moving averages. Thus, implying a potential recovery in 2023.

{kind=link}

Seeking Alpha

Final Word

Our follow-up analysis of Nu Skin concludes that the stock is significantly overvalued. We believe the firm presents a lack of residual value to its shareholders, which could lead to a significant drawdown in the company's stock price, especially considering its added earnings crash risk.

For further details see:

Nu Skin: 50% Downside Is Possible In 2023