NUS - Nu Skin: A High-Risk/High-Reward Turnaround Play Worth The Risks

2023-06-26 05:48:47 ET

Summary

- Demand is currently weak due to lower consumer purchasing power as a consequence of inflation.

- Strong inflationary pressures are also negatively impacting profit margins, which remain depressed.

- The company has recently launched three new products, including the Beauty Focus Collagen+ skin care supplement, the ageLOC Meta nutritional supplement, and ageLOC LumiSpa iO.

- Nu Skin has historically performed buybacks to reward long-term shareholders, with the total number of shares outstanding declining 15.27% during the past 10 years.

- The dividend is not safe as it used to be, and buybacks should remain paused for a long time, so prepare for being patient.

Investment thesis

Nu Skin's ( NUS ) operations have been slowly weakening for quite a few years, but challenges have recently intensified as inflationary pressures are causing not only increased production costs but also weaker demand. Profit margins are declining along with volumes, and this is causing a lot of pessimism among investors. In addition, increasing concerns of a global recession as a consequence of recent interest rate hikes are already beginning to be reflected in consumer demand and in the share price, which has fallen by 77% from all-time highs reached in January 2014.

Despite this, debt remains at sustainable levels and very high cash and equivalents should allow a significant reduction. In addition, unusually high inventories should allow the management to apply temporary reductions in production capacity in order to convert inventories into cash, with which the company should be able to keep investing in profitability, growth, and further acquisitions. Still, I highly encourage to make a dollar-cost averaging approach as macroeconomic challenges are significant and the company has a strong cyclical nature.

A brief overview of the company

Nu Skin is a global developer and distributor of premium-quality beauty and wellness solutions. The company was founded in 1984 and currently sells its products in approximately 50 markets worldwide, enjoying a market cap of $1.60 billion. Nu Skin has rewarded shareholders over the years through growing dividends and share buybacks, and due to the cyclicality of its operations, I believe there are two acceptable ways to invest in Nu Skin: by buying shares in tumultuous times in order to obtain high capital returns once optimism returns to shareholders, or buy at low prices to hold the shares and enjoy a higher dividend yield on cost.

{kind=link}

The company operates under three main brands: its beauty brand, Nu Skin; its wellness brand, Pharmanex; and its anti-aging brand, ageLOC. Under these brands, it mainly develops, manufactures, and sells skin care devices, cosmetics, personal care products, nutritional supplements, and weight management systems. Nevertheless, Nu Skin is constantly launching new products to the market in order to adapt to changes in consumer habits, but has performed very badly in recent years as operations have weakened significantly while new risks derived from the current macroeconomic landscape are arising.

Currently, shares are trading at $32.11, which represents a 77.15% decline from all-time highs of $140.50 on January 13, 2014, and a 63.69% decline from more recent highs of $88.68 on August 3, 2018. Certainly, it is a very significant decline that makes it necessary to analyze the different aspects that have raised so much pessimism among investors.

First, profit margins have suffered in recent years causing a deterioration in cash from operations as net sales remained stagnant for years due to a high dividend, aggressive share buybacks, and increased debt that has caused a rise in interest expenses. This increased debt is the result of these high capital payouts for shareholders, as well as some recent minor acquisitions as the company has been recently acquiring other companies in order to develop and introduce new products in the market and thus unblock sales growth, and although the company has ample inventories, converting them into actual cash will not be an easy task as sales remain stagnant amidst a potential global recession as a consequence of recent interest rate hikes to contain high inflation rates.

Recent acquisitions

In the first quarter of 2016, the company acquired 70% of Vertical Eden, an early-stage company in the warehouse growing market, based in Alpine, Utah, that includes specialized technology in remote programming and management of the entire crop growing cycle for $3.3 million, and during the second quarter of the same year, it acquired the remaining 30% for $12.5 million. Later, during the third quarter, it acquired certain assets of Dr. Dana Beauty for $7 million, which include trademarks, product formulas, and other intellectual property primarily related to nail treatment.

In February 2017, the company acquired a 35% membership interest in Treviso, a personal care product manufacturer, for $21 million in cash and shares (which were later repurchased by Nu Skin). One year later, in January 2018, the company acquired the remaining 73% ownership in Innuvate Health Sciences, which owns a 92% interest in a nutritional product manufacturer, for $23.5 million, and a month later, it also acquired the remaining 65% ownership in Treviso for $83.9 million in cash and shares (that were later also repurchased). Also during the same month, the company also acquired L&W Holdings, a packaging supplier company, for $25 million in shares (which were later repurchased).

The acquisition spree continued in December 2020 as the company acquired 3i Solutions (Ingredient Innovations International Company), a developer and manufacturer of ingredients for consumer markets through proprietary encapsulation technologies, for $15.7 million in order to create new product formulas and increase the performance of the company's existing formulations in beauty and wellness.

And lastly, in April 2021, the company acquired Mavely, an emerging social commerce platform that streamlines customer acquisition and social selling, for $16.8 million in order to increase social selling capabilities to Nu Skin brand affiliates.

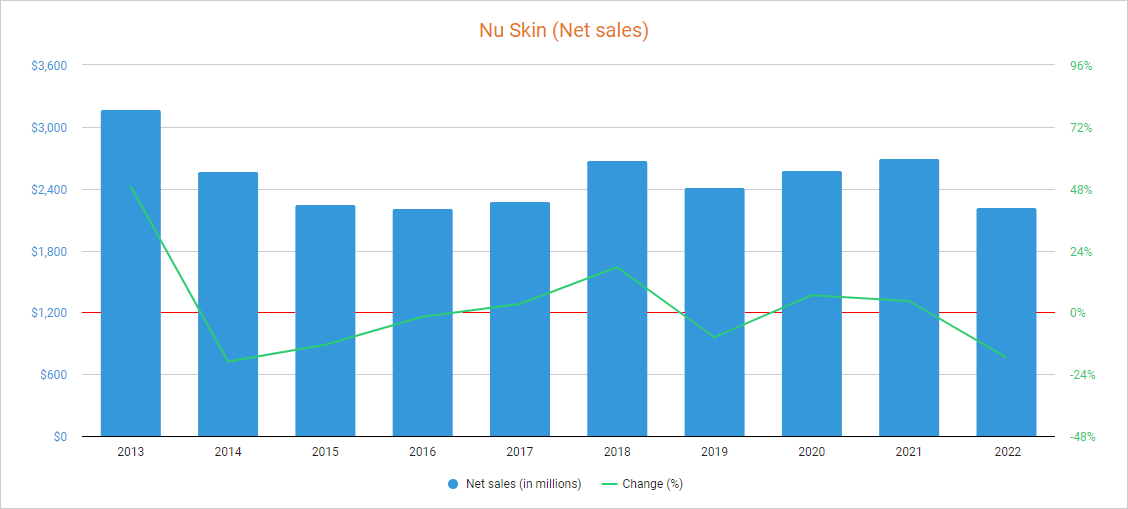

Net sales are expected to remain weak

Since 2016, the company has been (more or less steadily) increasing its net sales through acquisitions and product launches, but they declined by 17.44% in 2022 due to strict coronavirus-related restrictions in China, weakening purchasing power among consumers due to inflationary pressures, headwinds from the war between Russia and Ukraine, and a 5% impact on foreign exchange rates compared to 2021. Growing recessionary concerns have also increased caution when it comes to the use of money by consumers, which is currently causing weaker demand. Nevertheless, in 2022, Rhyz Investments, which is the investment firm of the company, provided 7% of the company's overall revenues.

{kind=link}

Continuing with weakening demand, net sales declined by 20.41% year over year during the first quarter of 2023 (and by 7.81% quarter over quarter) due to the macroeconomic obstacles mentioned and a 4% negative foreign exchange impact due to a stronger-than-usual dollar. In this regard, net sales are expected to decline by 6.28% in 2023 as headwinds are expected to be long-lasting, but slightly recover in 2024 as they are expected to grow by 2.87% compared to 2023, which is a very mild recovery .

The company has recently launched the Beauty Focus Collagen+ skin care supplement and the ageLOC Meta nutritional supplement that helps support metabolic health, and is currently launching ageLOC LumiSpa iO, an advanced skin treatment and cleansing device with clinically tested positive results for skin softness, smoothness, brightness, and radiance. And during the first quarter of 2023, it began working on the launch of TRMe, a personalized weight management system, in key Asian markets, including South Korea and Mainland China among others.

Also, the company expanded its operations in Peru in 2019 as it has experienced strong volume sales in Latin America, and China is expected to start providing higher sales soon boosted by covid-related restriction liftings. Using 2022 as a reference, 23% of net sales take place in the Americas, whereas 16% take place in Mainland China, 16% in Southeast Asia/Pacific, 12% in South Korea, 10% in Japan, 9% in EMEA, and 7% in Hong Kong and Taiwan, which means the company has a strong geographical diversification. Still, the recent sharp decline in the share price has caused a sharp drop in the P/S ratio to 0.767, which means the company generated trailing twelve months' net sales of $1.30 for each dollar held in shares by investors.

This ratio is 37.89% lower than the average of the past 10 years, and represents a 75.75% decline from the highs of 3.167, reflecting growing shareholder pessimism and lower expectations as net sales are expected to remain weak while a potential recession as a result of recent interest rate hikes threatens to further weaken the company's operations at a time when it finds itself with relatively high (but manageable) levels of debt. Also, profit margins have recently declined as a consequence of inflationary pressures and weak volumes, which is putting the balance sheet under some pressure.

Margins keep deteriorating

Although it is true that the company has managed to maintain positive profit margins over the years, these have gradually weakened due to weak demand and, more recently, inflationary pressures, which has directly affected its ability to generate cash from operations, and thus, caused a significant increase in the dividend cash payout ratio. In this regard, the trailing twelve months' gross profit margin currently stands at $71.32%, whereas the EBITDA margin is at 9.77%.

During the first quarter of 2023, the company reported a gross profit margin of 72.25%, and an EBITDA margin of 8.90%, which means the company remains profitable but profitability is weakening even further mainly due to the mentioned ongoing inflationary pressures and weakening demand. Currently, the company is performing cost-cutting initiatives as its objective is to recover some margins and reach a gross profit margin of 73.5% to 74%, but recessionary concerns are calling into question the feasibility of meeting profitability targets as demand could weaken even further in a recessionary economy, which would represent a significant issue for Nu Skin as the company needs to generate stronger cash from operations in order to be able to keep investing in growth and profitability initiatives to turn operations around.

The balance sheet is very strong

Luckily, the balance sheet is very strong thanks to cash and equivalents of $230 million, which makes its long-term debt of $420 million very manageable.

Furthermore, although cash and equivalents have significantly declined since 2021 due to recent acquisitions, strong share buybacks, and dividend expenses, inventories have increased to $366.54 million as the company hasn't been able to sell all the products it manufactured due to weak demand. This means that it will be necessary to reduce production capacity in order to convert part of said inventories into actual cash in order to be able to reduce its debt levels or, failing that, continue acquiring companies, launching new products, and investing in optimizing its operations in order to improve profit margins in the long run.

Even so, it will not be easy to do so in a macroeconomic scenario marked by losing purchasing power of consumers since the company will have to significantly reduce production capacity with the risk that this entails in terms of reduced profit margins as a result of more unabsorbed labor, which would put the dividend under even more pressure.

The dividend is not as safe as it used to

The company has raised its dividend payout for 22 consecutive years, and the latest raise took place in February 2023 as the management declared a quarterly dividend of $0.39 per share, which represents a 1.30% increase compared to the prior dividend. In this regard, dividend growth has slowed in recent years due to weakening profit margins and low sales growth.

Still, the recent increase in the cash payout ratio as a consequence of lower cash from operations has caused a drop in the share price significant enough to raise the dividend yield to 4.83%, which is significantly higher than the average of the past 10 years as investors expect very low growth rates in the foreseeable future.

In the following table, I have calculated the company's cash payout ratio by calculating what percentage of cash from operations has been allocated to the dividend and interest expenses since in this way one can get an idea of the company's ability to cover the dividend through actual operations.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| -$56.5 |

| $322.1 |

| $275.3 |

| $302.6 |

| $202.7 |

| $177.9 |

| $379.1 |

| $141.6 |

| $108.1 |

| Dividends paid (in millions) |

| $81.4 |

| $81.2 |

| $78.4 |

| $76.1 |

| $80.6 |

| $82.2 |

| $78.4 |

| $76.3 |

| $77.0 |

| Interest expenses (in millions) |

| $5.7 |

| $7.9 |

| $15.6 |

| $22.2 |

| $21.8 |

| $19.2 |

| $13.1 |

| $11.2 |

| $10.4 |

| Cash payout ratio |

| - |

| 27.66% |

| 34.11% |

| 32.49% |

| 50.52% |

| 57.00% |

| 24.14% |

| 61.79% |

| 80.85% |

As one can see, the company has historically been conservative with the use of cash as the cash payout ratio has been very low most of the time, but lower cash from operations has caused a dramatic increase in the cash payout ratio to 80.85% in 2022.

As for the past quarter, cash from operations was -$22.1 million (vs. $7.5 million during the same quarter of 2022) as inventories increased by $16.8 million and accounts receivable by $12.6 million while accounts payable declined by $4.5 million, which means the dividend pressure is increasing even further despite the fact that the company reported a positive net income of $11.4 million. In this regard, the company urgently needs to convert its inventories into actual cash and improve profit margins, which does not depend exclusively on its efforts, but also on the improvement of the current macroeconomic context. It is important to note that in addition to covering interest expenses and dividend payments that add up to around $90 million per year, the company must cover over $60 million of annual capital expenditures, so it should be generating over $150 million in cash from operations (cash from operations was $ 108.1 million in 2022).

Therefore, the margin to continue raising the dividend is drying up as the company is currently struggling to cover the current dividend, and I would not expect any significant raise until demand and margins normalize, which is the price that investors will have to pay in the short and medium term in exchange for a higher-than-usual dividend yield on cost.

Share buybacks are stopping

The total number of shares outstanding declined by 15.27% during the past 10 years as the company has historically performed buybacks in order to reward long-term shareholders. This means each share represents a growing size of the company over time, which improves per-share metrics and should eventually be reflected in the share price once operations show clear signs of improvement.

Still, the company didn't buy back any shares during the first quarter of 2023 as cash from operations is not allowing to cover annual dividend payouts, interest expenses, and capital expenditures, and therefore, it can be expected that buybacks will continue to be paused both in the short and medium term as improving profitability and keeping debt under control should currently be a top priority.

Risks worth mentioning

Due to the historical cyclicality of Nu Skin's operations and the current complex macroeconomic environment, I consider investing in Nu Skin to be a high-risk/high-reward turnaround play at current prices. Even so, below I would like to highlight the risks that I consider most important to consider, especially in the short and medium term.

- The first and (in my opinion) most important risk that investors should be aware of is the materialization of a potential global recession due to recent interest rate hikes as demand could slow even more. This would not only affect volumes but also profit margins due to unabsorbed labor.

- The second risk that I would like to highlight is related to profit margins. The company has been suffering from declining profit margins for many years, so once high inflation rates stabilize long enough for pricing to catch up with production costs, the management will need to continue applying ongoing cost-saving initiatives. In addition, it will be important for the company's future to invest in some optimization of operations and achieve some sales growth in order to be able to sell its products with higher profit margins.

- It is also important to note that the company could have serious difficulties in partially emptying inventories due to weak demand, so cash from operations could remain weak in the foreseeable future.

- The company could pause or even cut the dividend as it needs to preserve as much cash as possible in order to survive current and potential headwinds.

- Foreign exchange rates could continue negatively impacting performance for as long as the U.S. dollar remains strong.

- In my opinion, buybacks should remain paused for quite some more quarters due not only to weak operational performance but also due to global economic uncertainties.

Conclusion

You only need to look at the performance of its share price to realize that Nu Skin's operations are not having a good time. Profit margins have slowly declined in recent years, and inflationary pressures are currently putting extra pressure on the company's ability to convert sales into actual cash due not only to increased production costs but also to declining demand derived from losing purchase power among consumers. To this must be added negative FOREX headwinds, and despite recent acquisitions, sales have declined significantly in 2022, and are expected to decline again in 2023. Recent acquisitions are aimed to get the needed capabilities to develop new products and improve Nu Skin's own products, and while sales are currently depressed due to macroeconomic headwinds, they were picking up, albeit at a slower pace, in the 2016-2021 period.

In this regard, net sales are expected to start increasing again in 2024, and China's coronavirus-related restriction liftings should help in the foreseeable future. In addition, the balance sheet is very robust thanks to very high cash and equivalents and inventories, and the current headwinds should be, in my opinion, temporary as they are directly linked to the current global macroeconomic landscape. For these reasons, I consider that Nu Skin is a high-risk/high-reward turnaround play worth the risks at current prices. Nevertheless, I highly recommend averaging down from current share prices as the company's operations are very cyclical and the global economy is currently suffering high volatility periods.

For further details see:

Nu Skin: A High-Risk/High-Reward Turnaround Play Worth The Risks