NUS - Nu Skin Is Here To Stay

2023-04-04 01:04:33 ET

Summary

- The company showed strength in its business model despite decline in revenues.

- The Chinese economy is showing signs of recovery, and healthcare spending in the markets the company serves is still strong.

- The market sentiment and management outlook are pessimistic to neutral. We think the current valuation is attractive.

Investment thesis

Nu Skin Enterprises, Inc. ( NUS ) faced headwinds due to the COVID lockdown, which disrupted its direct sales operation. The company was able to secure a nice positive margin while revenue declined in the high teens to mid twenty. The management provided a conservative outlook. Based on the latest data and our analysis below, we think the business should recover sooner than expected and its business model is still solid. The market sentiment is pessimistic to neutral. We think NUS stock is a buy at its current valuation.

Company profile

Nu Skin Enterprises, Inc. develops and distributes a comprehensive line of premium-quality beauty and wellness solutions in approximately 50 markets worldwide. The company operates in the direct selling channel, primarily utilizing person-to-person marketing to promote and sell its products.

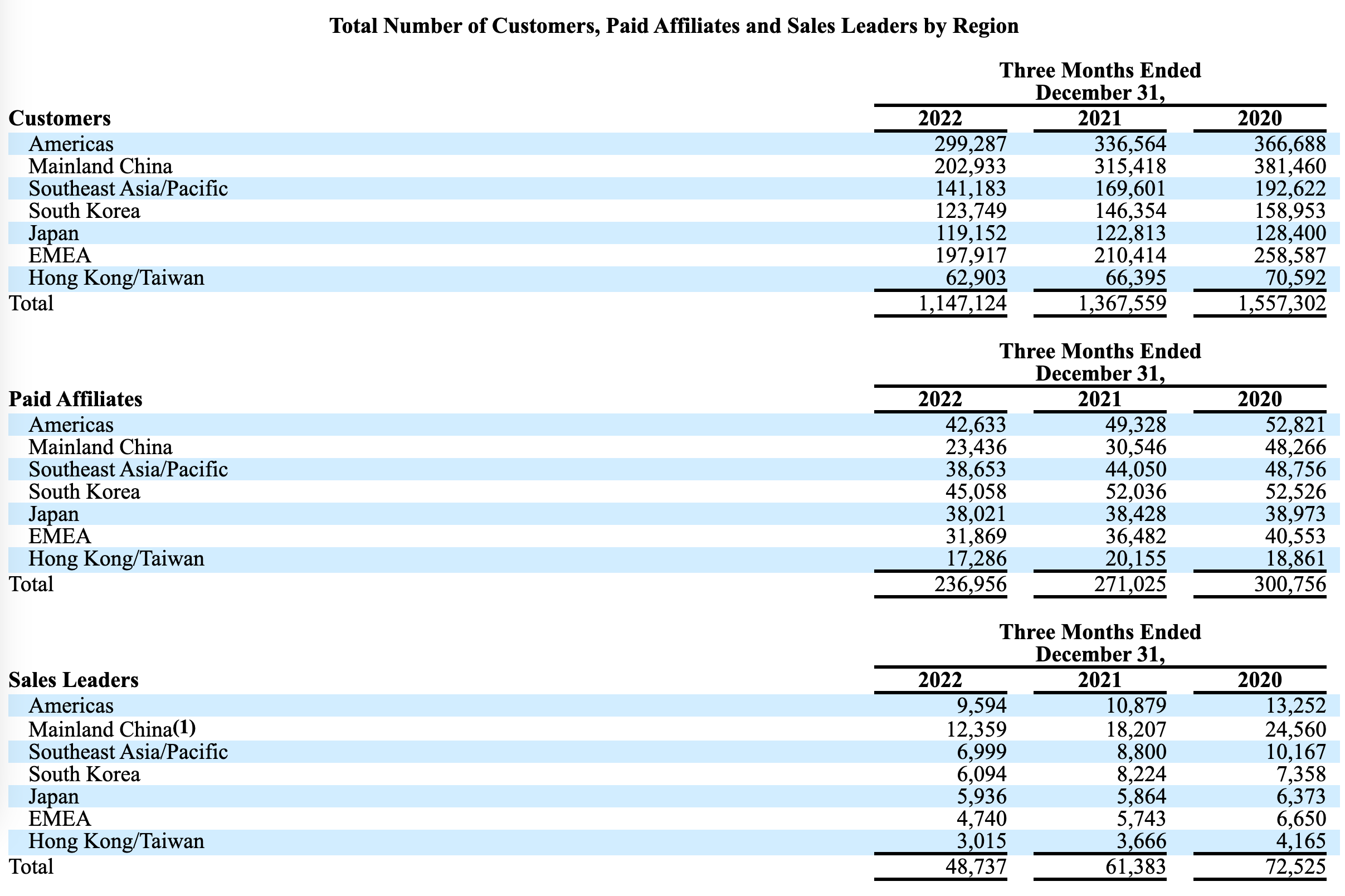

Customers, paid affiliates and sales leader breakdown (Company's filing)

{kind=link}

{kind=link}

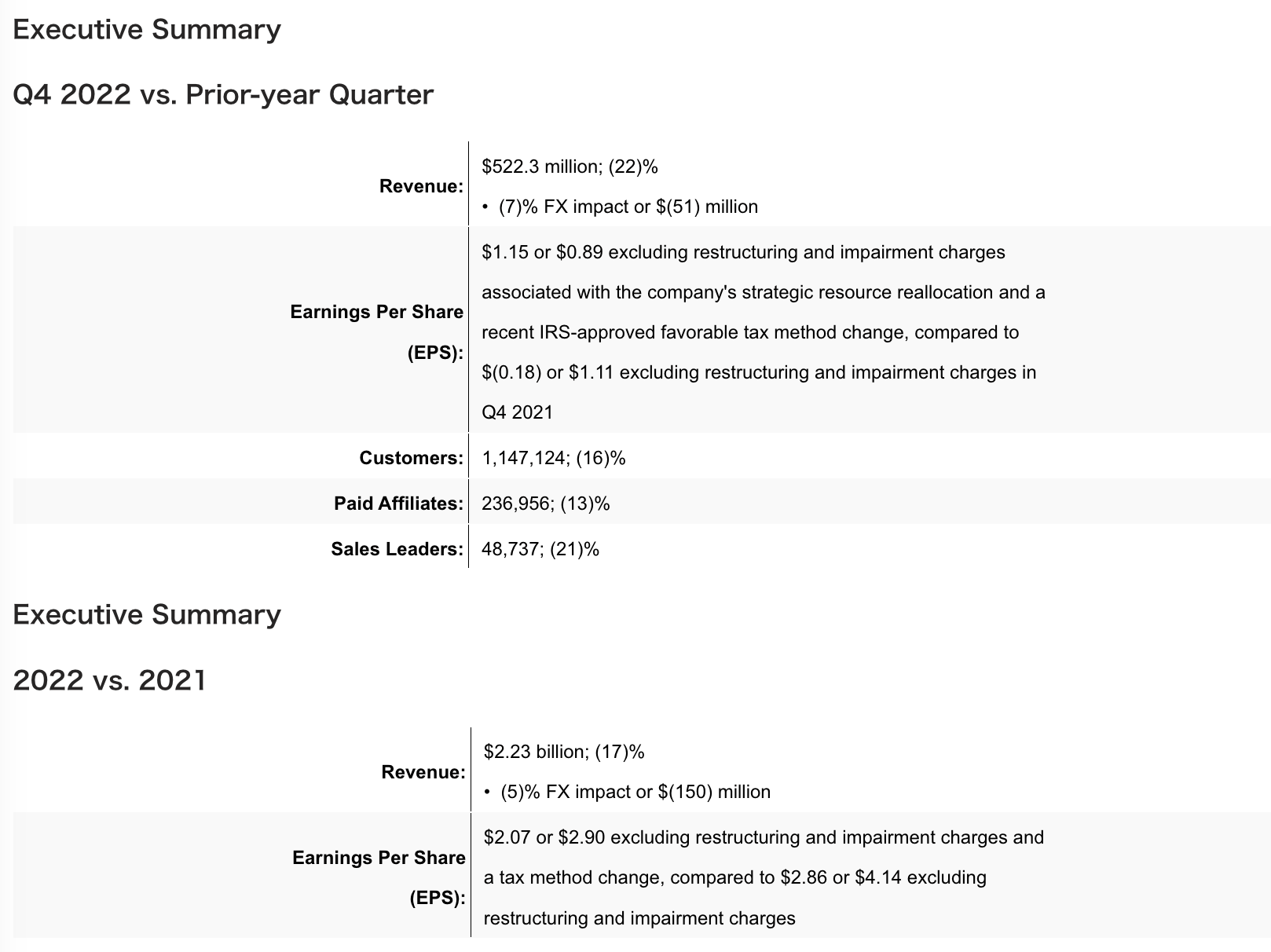

Key takeaways from Q4 2022 earnings:

Despite financial and operating metrics both dropping by mid-teen to high twenty areas, the company was able to secure a great adjusted operating margin(excluding restructuring and impairment expenses) at 8.6% in Q42022, down from 10.5% in Q42021.

{kind=link}

The management mentioned that China market was still challenging. They expected to take time to rebuild the team and business will remain difficult in the first half of 2023.

Our Mainland China business continues to be challenged by COVID-related factors that are negatively impacting our selling and promotional activities. This is reflected in our decline in revenue and other KPIs.

While China has been lifting restrictions and opening up in recent weeks, it has also led to a large surge in COVID infections. As a result, we anticipate the first half of the year to remain difficult. As we return to more typical business activities in China, we need to rebuild our salesforce, which will take time to revitalize momentum.

Our initial 2023 guidance assumes the global macro environment remains challenging in the near term, improving throughout the year.

The management projected its revenues to decline in the first half and gradually return to growth in the second half.

{kind=link}

We have the following comments on Q42022 earnings:

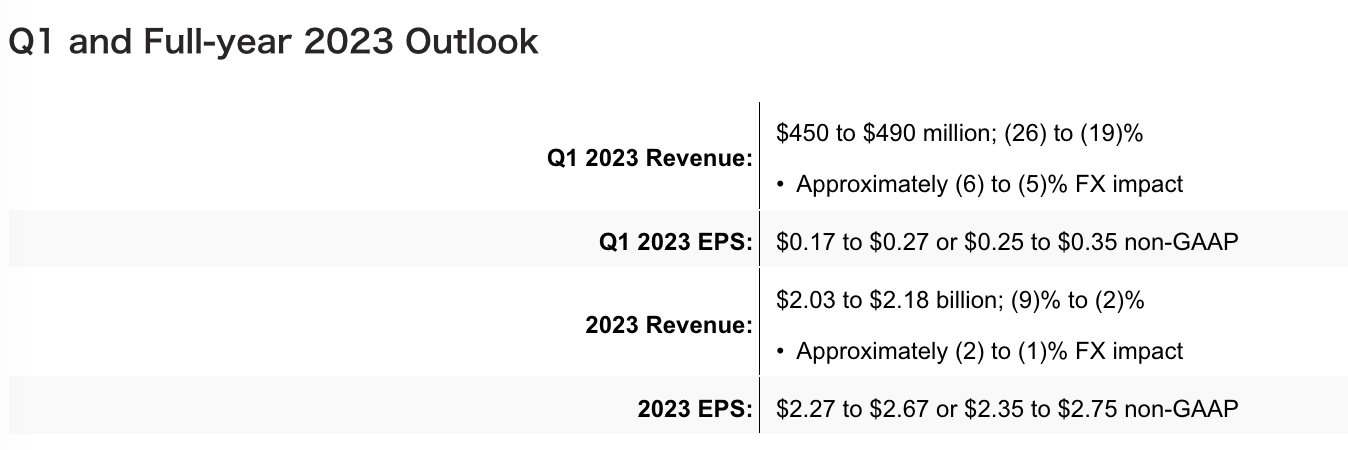

- The company was able to maintain a great adjusted operating margin (excluding restructuring and impairment expenses) at 8.6% in Q42022, even though its revenues decreased by 22%. It still projected a POSITIVE $0.17-$0.35 non-GAAP EPS in Q12023 even though the revenues will decrease by 19% to 26%. This demonstrates the resilience of its business model.

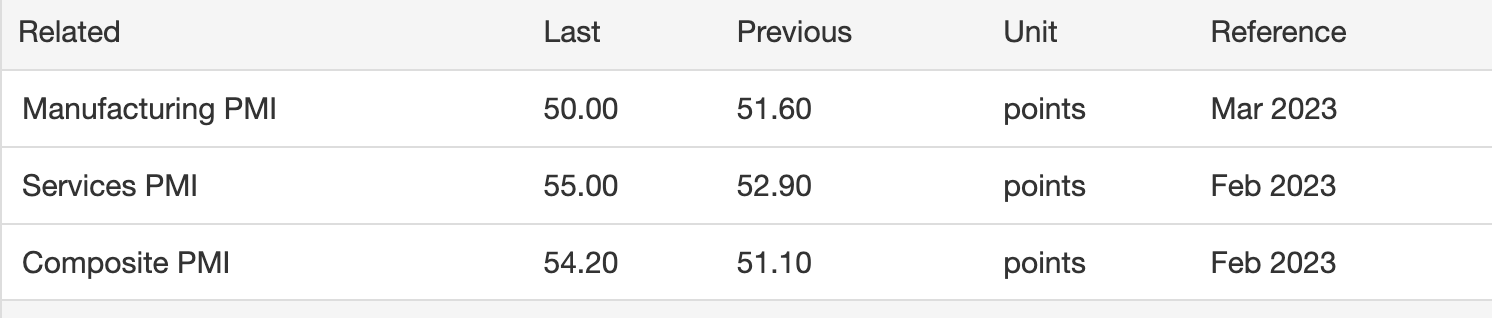

- The management was worried that the resurgence of COVID cases in China could post a challenging macro environment. However, China Caixin Manufacturing PMI and Services PMI already came back to 50 and 55 in Feb and Mar 2023, respectively, above the 50 levels. The resurgence of COVID cases in China was relatively short and it seemed to have limited impacts on the economy of China so far.

{kind=link}

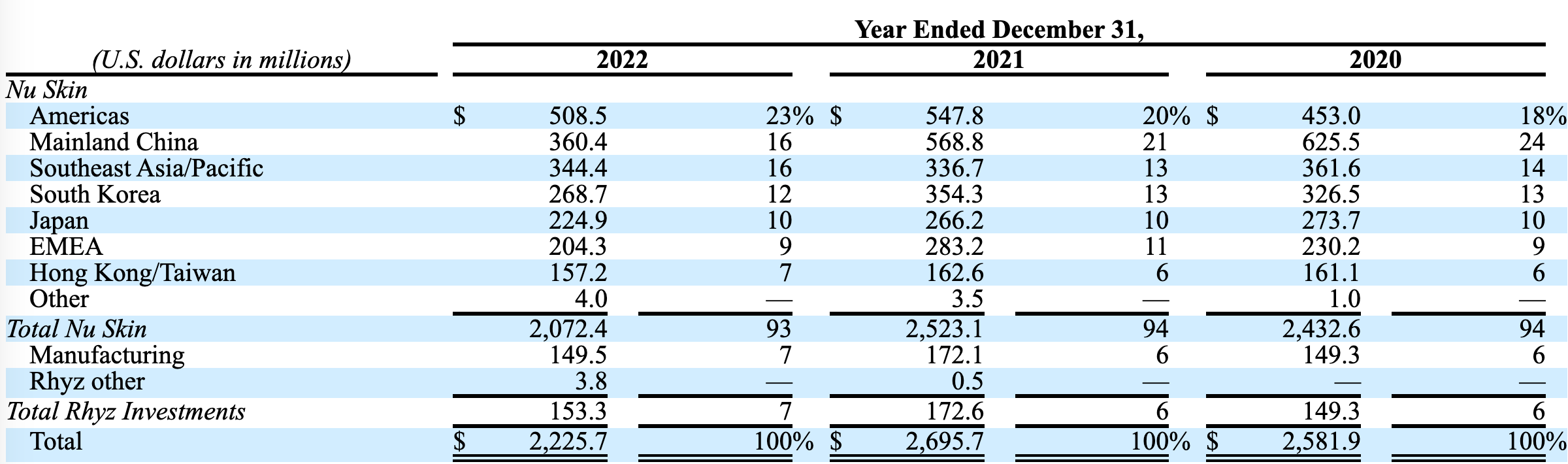

The company has an extensive geographic presence in Asia. No country contributed more than 17% of its total revenues in 2022. The company's diversified presence across multiple countries helps to reduce the risks associated with regulatory changes.

Healthcare spending is quite strong in the U.S. and China

The U.S. Health & personal stores retail sales continued to grow at 8% yoy and 0.9% mom, largely outpacing the growth of total retail sales by data from the US Census Bureau.

{kind=link}

It is the same situation in China. Traditional Chinese and western medicines retail sales grew by 19% in Jan-Feb 2023 and 12% in 2022. Although it might be mostly attributed to the COVID situation in China, we can still draw the conclusion that Chinese consumers' spending power for this category is still strong. The company's direct sales business was largely impacted by the lockdown in China. However, as long as the sector is still growing, the company should continue to invest and grab shares.

{kind=link}

{kind=link}

Valuation and catalysts

Its stock price is close to the mid-to-bottom range of its 10-year history.

Stock chart ( Seeking Alpha )

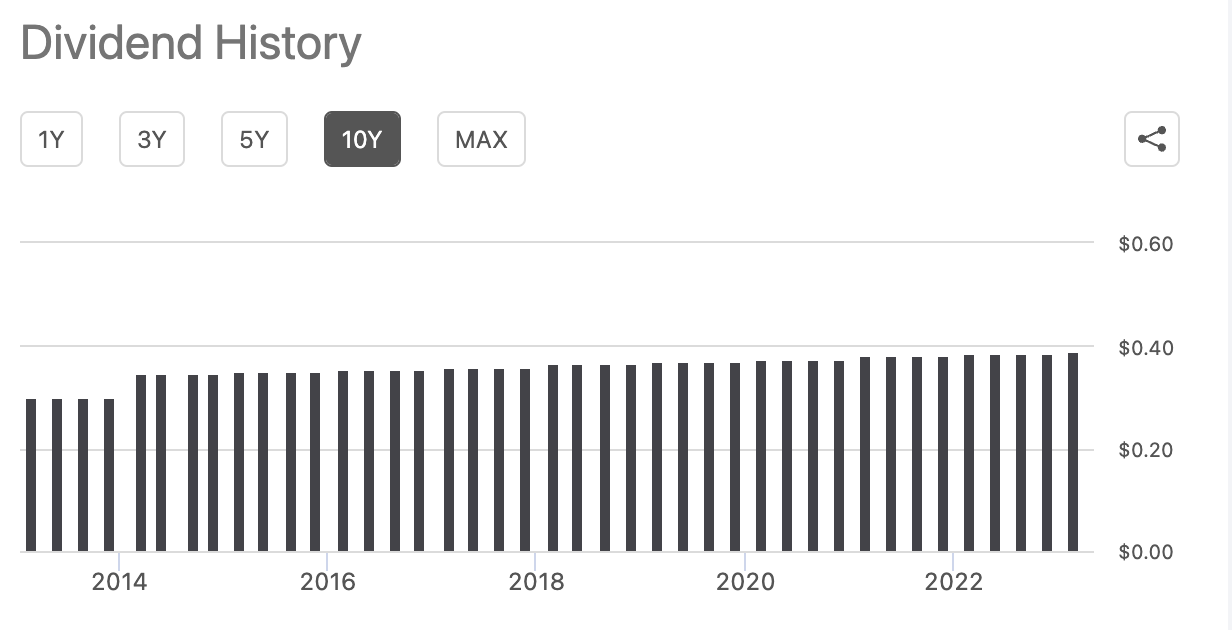

The company has steadily increased its dividends in the past 10 years from $1.2 to $1.5. The dividend yield is at 3.93% and the payout ratio was 41%.

{kind=link}

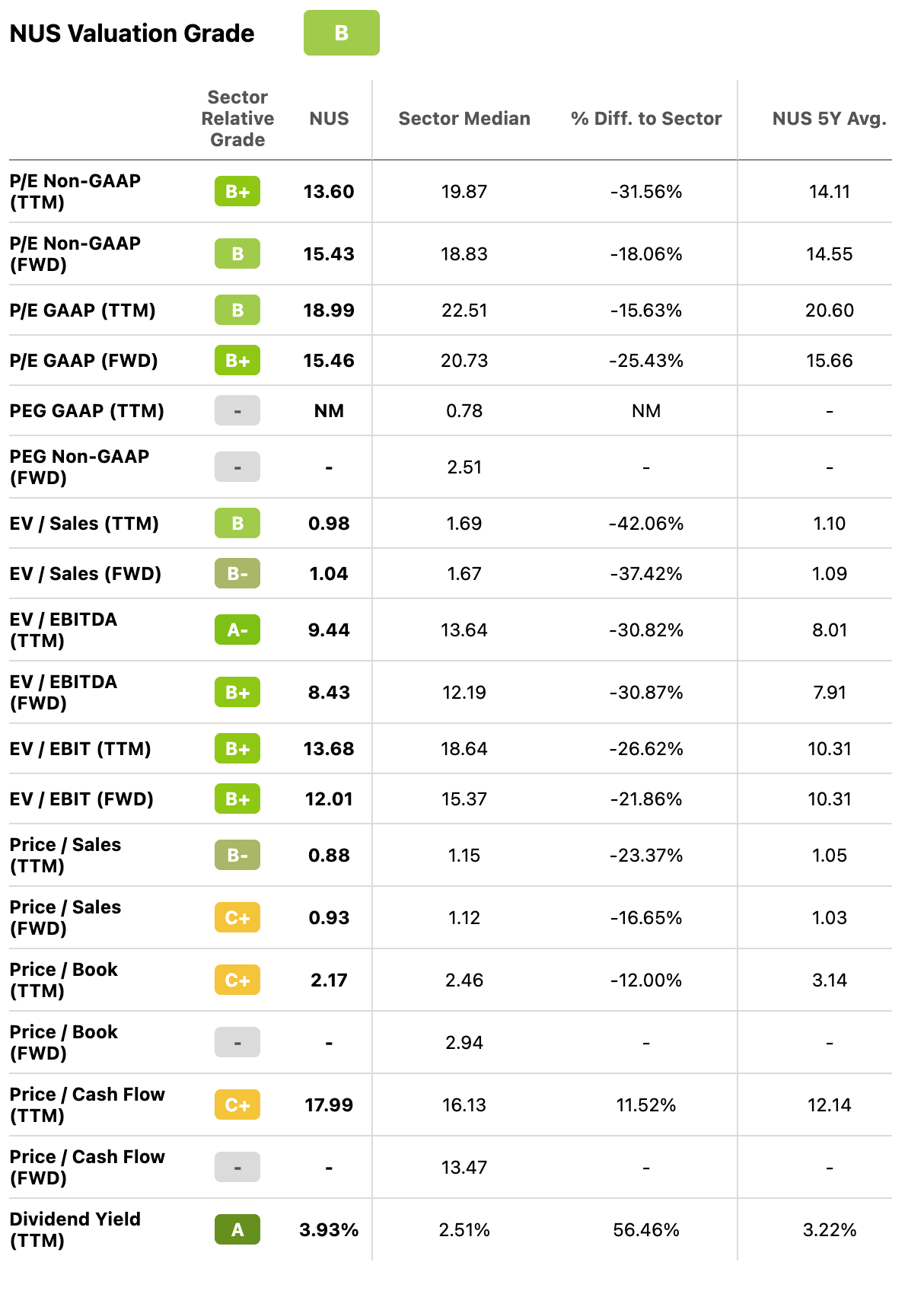

Its P/E and EV/EBITDA are lower than the sector median and slightly lower than its 5-year historical average. P/Cash flow is somewhat expensive compared to the sector or historical level.

{kind=link}

Market sentiment from SA authors is relatively bearish, while Wall Street maintains neutral ratings.

Stock ratings ( Seeking Alpha )

We think the overall valuation multiple is reasonable and current market sentiment and management's conservative outlook can be reversed once the company beats its guidance. Thus, financials and management tone in the future earnings release can be catalysts for the stock to rise.

Regulation risk

Because of the ban on the multi-level commissions business model in Mainland China, the company implemented a direct sales business model in China. The multi-level commission's structure plays role in relationship building. Although other markets currently don't have strict regulations regarding the multi-level commission structure, there are still potential risks in the future.

However, not all countries are against multi-level commission marketing("MLM") practice. For example, MLM is legal in the united states. MLM companies provide individuals with the opportunity to start their own businesses and earn income by selling products or services to consumers. As long as the company operates within the law and does not engage in the fraudulent practice, it is a profitable business and creates jobs and value for the economy.

For further details see:

Nu Skin Is Here To Stay