BUD - Nurture Ambev S.A. But Don't Gulp It

2023-06-26 12:13:48 ET

Summary

- Ambev S.A. is rated a hold by us for retail value investors due to its near 52-week high share price, potential dividend cuts, and growth challenges.

- The beverage company faces headwinds from macroeconomics, aggressive competitors, and higher costs in the industry.

- Despite strong analyst ratings, we believe Ambev's current investment outlook is less favorable for small investors.

Taste Is Flat

Ambev S.A. ( ABEV ), a beer brewer and distributor of beverages and food items, appears to us a less valuable investment for retail value investors than for those with greater risk tolerance. Despite strong enthusiasm for the stock, we rate it a hold at the present time.

Small investors need to consider 4 factors: can we buy at a reasonable price, are we able to sell at a higher price in a reasonable amount of time, can we collect a fair dividend yield while owning the shares, and is the company in a growth mode and/or essential industry. In our opinion, Ambev does not excel as a potential opportunity at this time. The share price is near its 52-week high; we do not foresee any significant events or earnings driving the price significantly higher in the next 8 months; the dividend might be slashed; and growth will suffer from macroeconomics, aggressive competitors, and higher costs.

The Company and Industry

Ambev S.A. products include beers, soft drinks, other non-alcoholic beverages, and food products. Brands include Skol, Brahma, Antarctica, Brahva, Budweiser, Bud Light, Beck, and Belgian beer Leffe. The company sells bottled water, isotonic beverages, energy drinks, coconut water, powdered and natural juices, and ready-to-drink teas under the Gatorade, Lipton Iced Tea, Fusion, Pepsi-Cola, Canada Dry, Squirt, Red Rock, Red Bull, Seven Up labels. The company headquarters is in São Paulo, Brazil, and operates as a subsidiary of Anheuser-Busch InBev SA/NV ( BUD ).

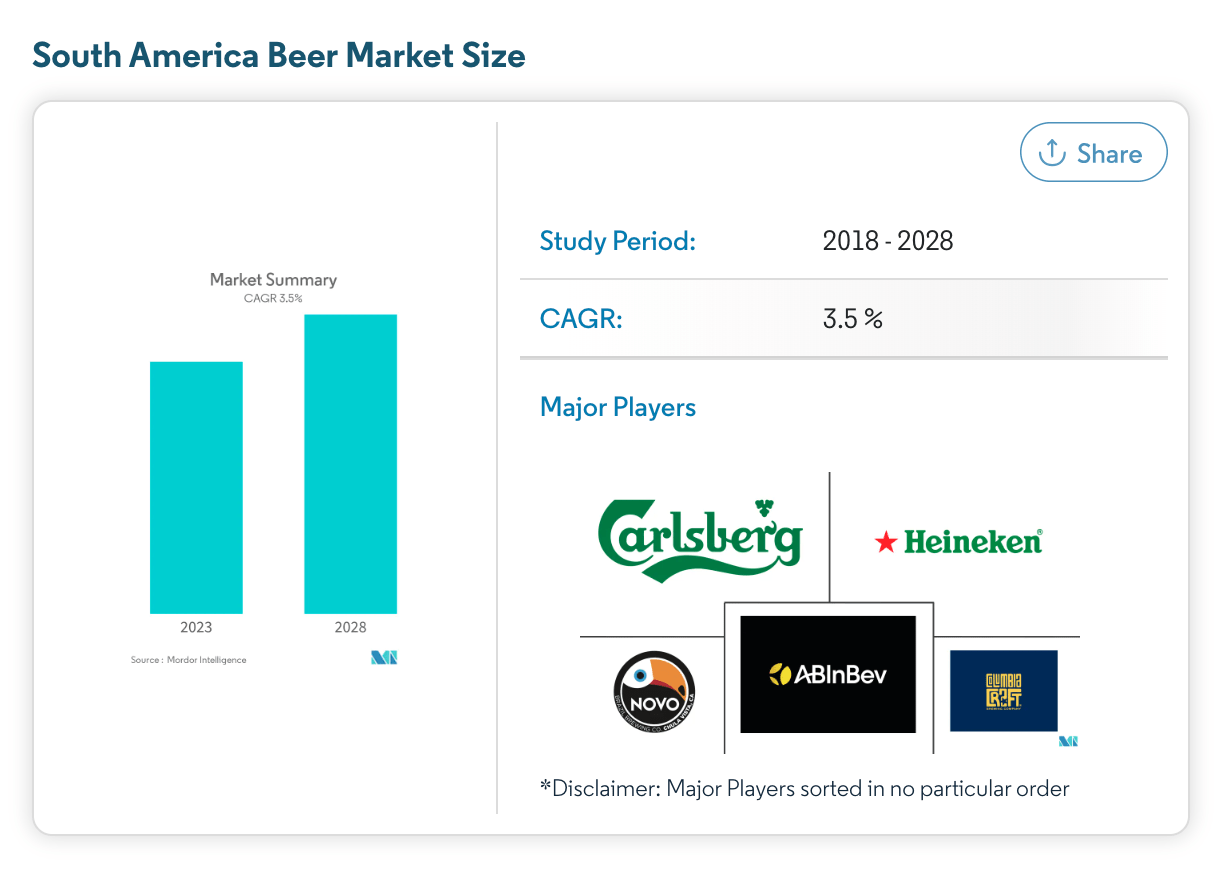

The food and beverage industry is expected to grow at a CAGR of 7% through 2025. The beer market by comparison is forecast to grow at a CAGR of 5.44%. The South American beer market CAGR growth is forecast lower through 2028, though beer is the preferred beverage of South Americans.

Beer Market (mordorintelligence.com/industry-reports/south-america-beer-market)

{kind=link}

Other headwinds the beverage industry faces being based in Brazil are higher costs (Brazil's inflation rate is 4.2%) and stiffer regulatory controls from the new populist government.

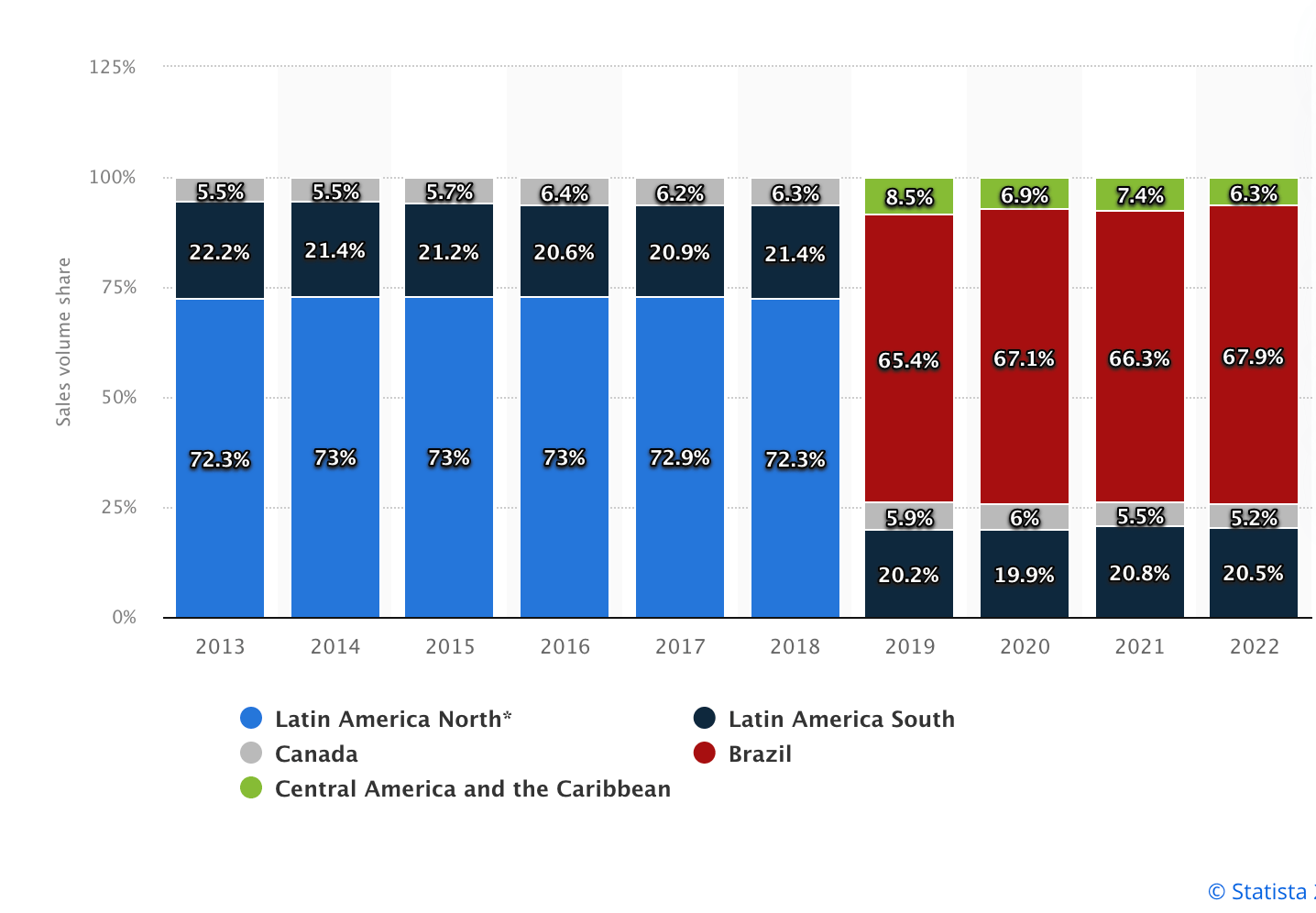

Ambev's market for the last decade is charted here:

Ambev Markets (statista.com/statistics/589594/ambev-sales-volume-share-worldwide-business-segment/)

{kind=link}

Dividend Warning

Ambev's current dividend yield is 4.51% compared to 3.8% for the industry average yield. The dividend yield has enticed investors, but I don't think it is safe or consistent. It is paid once during the year usually in January. Dividend payments have accounted for much of the total shareholder return over the past few years.

Ambev's dividend payout ratio is 81% of earnings and +94% of cash flow. We do not believe it is well-covered by cash flow. If revenue, volume, cash flow and earnings slip, or other priorities arise like a stock buyback program, it is the dividend yield that might be cut to preserve cash. Seeking Alpha's dividend grading system rates the dividend safety a D- currently.

Dividend Grades (seekingalpha.com/symbol/ABEV/dividends/dividend-safety)

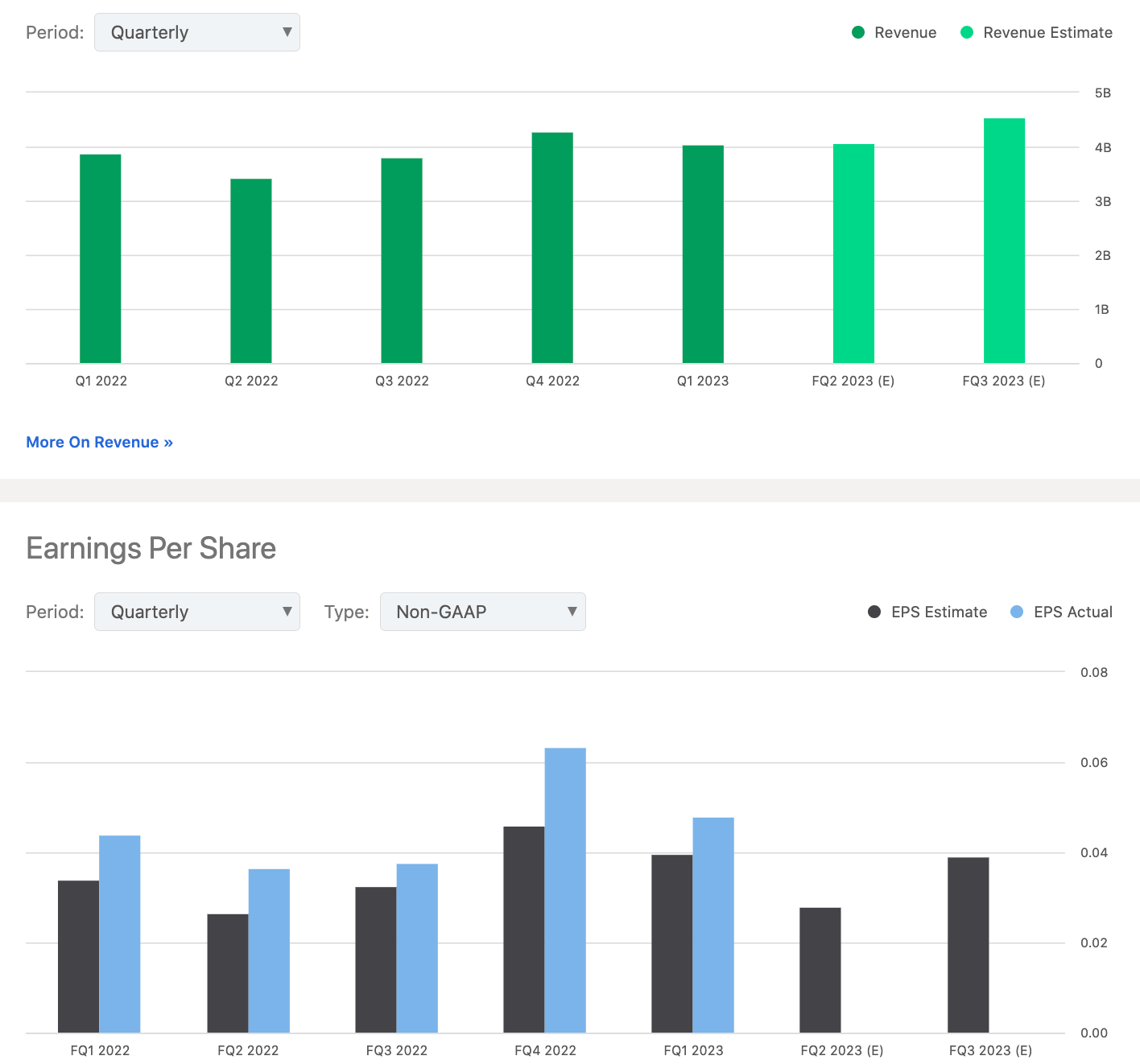

Other issues take the fizz out of the investment picture for us. Currently, Ambev's PE ratio is 18.24. Q1 '23 revenue of $4.05B was more than Q1 '22 but fell short of Q4 '22. Likewise with its earnings. We expect earnings to be $0.03 to $0.04 per share for Q2 '23, i.e., about the same Y/Y. The next earnings report is anticipated on July 27, '23.

We do not foresee improvements in outcomes for revenue and earnings from those reported last May. Revenue for the quarter rose 11.3% Y/Y, EBITDA and gross margins grew. But most worrisome for the future of the dividend is that "cash flow from operating activities declined."

Top of the Glass Share Price

During the pandemic and through the first half of FY '21, shares sold for under $3 each. The stock price hit +$3.50 in the second half of 2021 and hedge funds started taking positions. They steadily increased their holdings through Q1 '23. Funds bought 21.3M shares last quarter but one-third fewer funds own shares in Q1 2023 (15) any time since FY '21 (20).

{kind=link}

Regarding the share price, it closed last week near its 52-week high of $3.24 per share after tumbling to less than $2 during the pandemic. Before that, it touched $7 per share. It is already up 27% over the last 12 months and 23.5% YTD. However, the share price is down +32% over 5 years.

The boost may come from analysts who overwhelmingly assess the stock as a worthwhile buy and strong buy, same as the SA Quant Rating. The company's market cap is $51.06B. Its PE ratio of 18.24 is lower than the industry PE average of 21. It is about the same as the behemoth Anheuser-Busch which has a market cap topping $113B. Ambev's debt-to-equity ratio is 0.9%; it holds more cash than debt and assets far exceed liabilities.

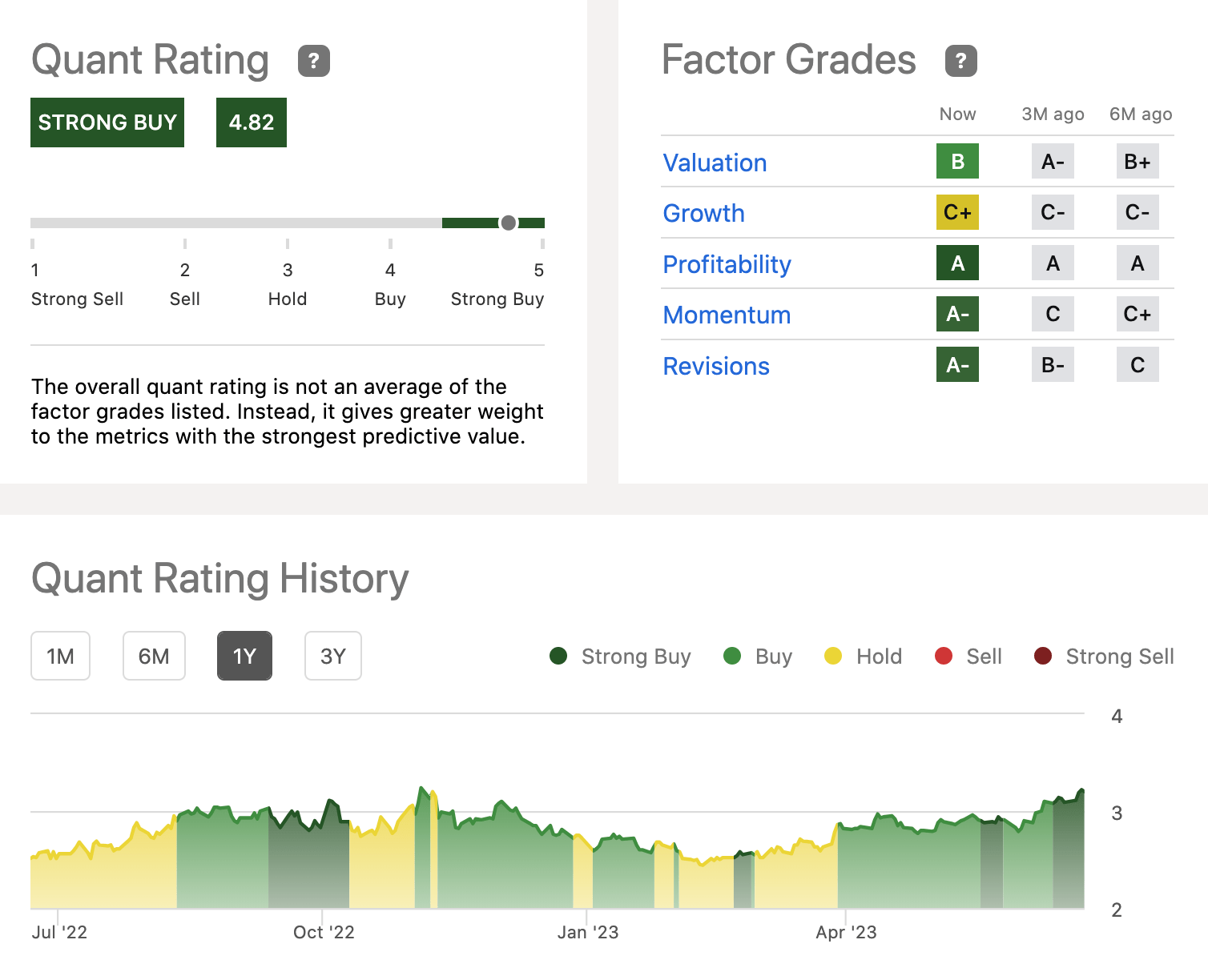

Except for expecting moderate growth, Seeking Alpha's Factor Grades are strong:

Quant Rating/Factor Grades (seekingalpha.com/symbol/ABEV/ratings/quant-ratings)

{kind=link}

Last Sip

In a better economic climate, the shares of Ambev S.A. might once again reach an average price target in 2024 of $4 or higher. It is not likely to move up much this year from near to its current high unless the company beats earnings estimates; it has in nearly 8 of the last 9 quarters. Second, Ambev S.A. intends to buy back 13M shares or 0.3% of its outstanding shared capital through November 24. But we believe these issues are already factored into the higher share price and will not move the stock higher enough going forward. There are headwinds.

In their talk with shareholders per Q1 '23, management noted cash flow from operations declined Y/Y "driven mostly by payables," tax matters, expensive tax persistent litigation, and customer acquisition costs from "market competitors really intensifying promotional activities." The company might have hedged costs for commodities allowing for better margins and profits in the past, but reports are to expect higher prices in key beverage commodity items, wage inflation, and energy costs. Bottled beverage sales might sink from rising prices. We do not want to see the portfolios of retail value investors sink, so we tag Ambev with a hold rating at this time.

Finally, because this is a foreign-based company, consult a tax accountant before any stock is bought or sold.

For further details see:

Nurture Ambev S.A. But Don't Gulp It