NUSI - NUSI: An Inefficient Way To Manage Downside Risk

2023-11-14 18:16:59 ET

Summary

- The Nationwide Nasdaq-100 Risk-Managed Income ETF aims to provide exposure to the Nasdaq-100 along with downside protection.

- NUSI uses a rules-based options trading strategy to generate income and reduce downside risk.

- NUSI has underperformed the Nasdaq 100 since its inception but has delivered lower levels of volatility.

- NUSI has not performed well on a risk adjusted basis and suffered a particularly challenging 2022.

- Investors should instead consider a diversified risk mitigation strategy including tail hedging, reduced equity exposure, and lower beta equity exposure.

ETF Overview

The Nationwide Nasdaq-100 Risk-Managed Income ETF ( NUSI ) seeks to provide investors with an income solution that targets high current income with a measure of downside protection.

NUSI follows a rules-based options trading strategy that seeks to produce high income using the Nasdaq-100 Index. The fund seeks to provide downside protection by using a constant, fully financed market hedge that seeks to reduce downside risk.

NUSI currently has $409 million in net assets and charges an expense ratio of 0.68%.

NUSI allows investors to participate in some degree of upside related to the movement of the Nasdaq-100 while experiencing significantly less risk. That said, NUSI has proved a very inefficient way to reduce risk as the total return since inception has been just 17% of the total return realized by QQQ while NUSI's average volatility has been ~51% of QQQ. For this reason, investors should consider alternative risk management strategies and avoid owning NUSI.

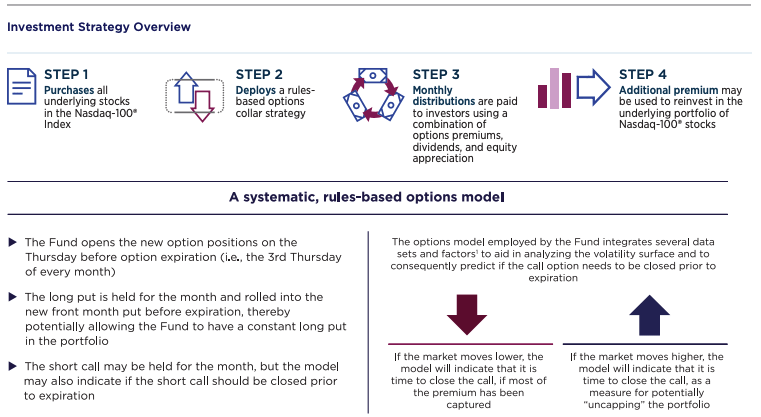

Investment Strategy Overview

As shown below, NUSI first purchases all the underlying stocks in the Nasdaq-100 and then implements a rules-based options collar strategy. This means the fund sells upside calls and uses the premium to purchase downside puts. The fund uses an active approach to consider which call options should be closed prior to expiration.

Each month NUSI distributes a combination of option premiums, dividends, and equity appreciation. Any additional premium may be used to reinvest in the underlying portfolio of Nasdaq-100 stocks.

I view this strategy unfavorably given option supply and demand market dynamics. I believe selling calls has become a crowded trade given the number of ETFs that have come to market with strategies that look to sell calls to generate additional income. The result of this is that option premiums for calls are lower than they otherwise would be and selling them does not make a lot of sense. Similarly, many ETFs have come to market over the past few years with a focus on buying puts to provide downside risk mitigation. For this reason, puts are more expensive than they otherwise would be and buying them has become very expensive. Evidence of this dynamic can be seen in the weak performance that NUSI has experienced since inception.

{kind=link}

Management Fee

NUSI has an expense ratio of 0.68%. To put that into context, the average expense ratio for an actively managed equity mutual fund is ~0.66% and the average equity ETF expense ratio is ~0.16%. Comparably, the Global X NASDAQ 100 Collar 95-110 ETF ( QCLR ) charges a total expense ratio of 0.25% while the Global X NASDAQ 100 Covered Call ETF ( QYLD ) charges a total expense ratio of 0.60%. Thus, NUSI appears to be priced towards the higher end of the range for similar products.

Historical Performance Summary

NUSI launched in December 2019 and has significantly underperformed the Nasdaq 100, which can be proxied using the Invesco QQQ Trust ETF ( QQQ ). Since inception, NUSI has delivered a total return of 14.5% compared to a total return of 84.1% delivered by QQQ. While this level of underperformance is troubling, the goal of this fund is to provide downside protection and thus it makes sense to consider the relative level of realized volatility for NUSI vs QQQ.

Since inception, NUSI has delivered an average realized trailing 30-day volatility of 12.93% compared to 24.9% for QQQ. This suggests that NUSI has in fact offered a smoother ride than QQQ. However, it should be noted that while NUSI has on average realized ~51% of the volatility of QQQ it has only achieved 17% of the total return achieved by QQQ. Thus, NUSI has proved a fairly inefficient way of reducing volatility.

The most similar product ETF on the market currently to NUSI is the Global X NASDAQ 100 Collar 95-110 ETF ((QCLR)) which launched in August 2021. Since QCLR launched, it has outperformed NUSI by 11.96% while realizing a similar average level of volatility. Thus, while the historical return history is limited NUSI has performed significantly worse than QCLR on both an absolute and risk-adjusted basis.

2020 Performance

In order to get a better understanding of how NUSI has performed under different market environments it makes sense to look at relative performance on a yearly basis.

2020 was an interesting year to analyze given the sharp covid sell-off and ensuing rally. During the initial covid related sell-off NUSI did a very solid job of providing downside protection. The fund's collar strategy worked well as downside puts provided protection and NUSI experienced only modest losses while QQQ plunged. However, NUSI failed to significantly participate in the upside rebound.

Overall, 2020 was not a disaster as NUSI provided investors solid protection during the sharp sell-off early in the year while allowing investors to participate in some of the upside related to the significant rally later in the year as NUSI captured 38% of QQQ's total return for the year.

2021 Performance

Similar to 2020, 2021 relative performance for NUSI was not a disaster as NUSI captured ~35% of the total return delivered by QQQ for the year while experiencing less volatility.

2022 Performance

2022 was an abysmal year for NUSI and highlights certain challenges related to NUSI's risk mitigation approach. NUSI delivered a total return of -28.3% compared to a total return of -32.5% delivered by QQQ.

The reason that NUSI failed to provide better risk reduction in 2022 is that the market sell-off was relatively slow and steady. The result of this is that NUSI's put protection was ineffective as the market did not sell-off fast enough for NUSI puts to go significantly in the money.

NUSI opens new option positions on the 3rd Thursday of each month. Put positions are held for the month and rolled into the new front month put before expiration. The result is that NUSI was spending a significant amount on put options which did not provide massive payoffs but rather small or no gains as the Nasdaq-100 did not fall quickly enough for these options to pay off in a big way.

The takeaway here is that while NUSI can provide significant risk mitigation in certain market environments (e.g. the first few months of 2020) it is not effective all the time. The result is that during a year such as 2022 investors may experience more downside participation than anticipated based on historic average realized volatility of NUSI compared to QQQ.

Forward-Looking Outlook

I believe NUSI will continue to deliver weak risk-adjusted performance going forward. Part of this view stems from the fact that I believe the option market supply and demand dynamics will continue to make selling calls and buying puts a less attractive trade going forward than historical back testing would suggest. Another part of my view is that markets are more likely to experience slow and steady declines compared to rapid declines. I believe the crash we experienced related to COVID in 2020 is a less likely market experience than the slow and steady decline experienced in 2022. Thus, I believe NUSI is unlikely to face a favorable market environment going forward.

Alternative Risk Management Techniques To Consider

NUSI is a reasonably well-thought-out ETF which tries to reduce downside risk for investors while allowing for upside participation.

To some degree, NUSI has succeeded in that it has been able to provide significant downside protection which can be seen in a historical average realized volatility which is only 51% of QQQ. However, this reduction in volatility and risk has proved very expensive. Since its inception in December 2019, NUSI has delivered just 17% of the total return realized by QQQ.

Risk mitigation is generally a good idea and, in my opinion, investors should consider a combination of options including some of the below:

Tail hedging: investors can allocate a small percentage of their portfolio (generally 0-1.5% each year to purchasing deep out of the money put options.) This strategy does an excellent job at protecting the portfolio in the event of a fast market crash.

Reduced equity exposure in favor of other assets: a simple approach to reduce equity risk in the portfolio is simply to reduce the percentage allocated to equities while increasing allocations to other assets such as bonds or gold.

Focus on defensive equities: this approach involves selecting individual securities or ETFs that target lower-risk areas of the market. Typical examples include utility, healthcare, and consumer staple stocks. While these sectors may experience downside in a market sell-off they tend to go down less. I recently highlighted a few favorite defensive blue chip equities and ETFs here:

USMV: A Solid ETF For Volatility Reduction

H&R Block: A Defensive Blue Chip Buy

Elevance Health: A High Conviction Blue Chip Buy

Conclusion

NUSI offers one way for investors to participate in some degree of upside related to the movement of the Nasdaq-100 while experiencing significantly less risk. However, NUSI has proved a very expensive way to reduce risk as the total return has been just 17% of the total return realized by QQQ (since NUSI's inception.)

NUSI is most effective as a risk mitigator during a fast sharp market decline such as the decline in early 2020. NUSI is least effective as a risk mitigator during a slow and steady market decline such as the decline in 2022.

Investors looking to position defensively should consider a small allocation to tail hedging, reducing the overall level of equity risk in the portfolio, and focusing on more defensive segments of the stock market.

For further details see:

NUSI: An Inefficient Way To Manage Downside Risk