NS - NuStar Energy Starts Building A New Financial Structure

2023-11-09 03:14:37 ET

Summary

- NuStar Energy has eliminated its Series D Preferred issue and laborious distribution, marking a new start for the company.

- The company reported $180 million of total EBITDA in the third quarter, with strong performance in the pipeline segment.

- NuStar has plans for growth in low carbon ammonia and other markets, with a focus on the Permian region.

NuStar Energy ( NS ) transformed itself over the past year eliminating the egregious Series D Preferred issue and with it, the laborious distribution. It is a monumental achievement, a game changer, a new start. In the past, our articles included attempts at balancing incoming cash, investor distributions and other cash expenses. In NuStar Energy: Taking A Slow And Possibly Safer Investment Road , the focus was on investor patience. The company operates a very valuable model with slow growth, but safe distributions. It has in the past been a perfect proxy for selling covered calls at appropriate prices to greatly enhance overall yield. That attribute might be changing under the new structure. Put on the hard-hat and come with us to the site for a pristine view.

The 3rd Quarter & 2023

We generally begin, our articles by reviewing the last quarter and guidance for the balance of that year. NuStar reported:

- $180 million of total EBITDA in the third quarter, a slight increase year over year. (The pipeline segment EBITDA was particularly strong, up 10% year over year.)

- DCF for the quarter equaling $93 million with a coverage ratio of 1.84.

- Refined product segment generating dependable revenue.

- The FERC index, the inflation index, added benefits to almost all of the pipelines.

- Permian crude flows averaging 523,000 barrels per day, down year over year.

- October flows averaged 533,000 showing continued improvement.

- Permian average flows for the December quarter should average around 540,000.

- Issued common equity raised $222 million used to finish purchasing the Series D Preferred.

- Guidance for the year of $720 - $740 million in EBITDA.

- Leverage closing the year below 4 within the business target.

With respect to capital, NuStar guided at $120-$130 million for 2023; $40 million for the Permian, $25 million for the West Coast and $25 million for an ammonia pipeline.

Growth in Low Carbon Ammonia & Others

The company now targets two markets for growth of yet to be determined value, West Coast renewable product storage and connecting the ammonia system to OCI state-of-the-art ammonia products facility located in Iowa. The ammonia startup date is scheduled for January of 2024. In January, NuStar, also, plans to announce a project with another major ammonia producer. The first ammonia project is being slated as "healthy return, low capital project."

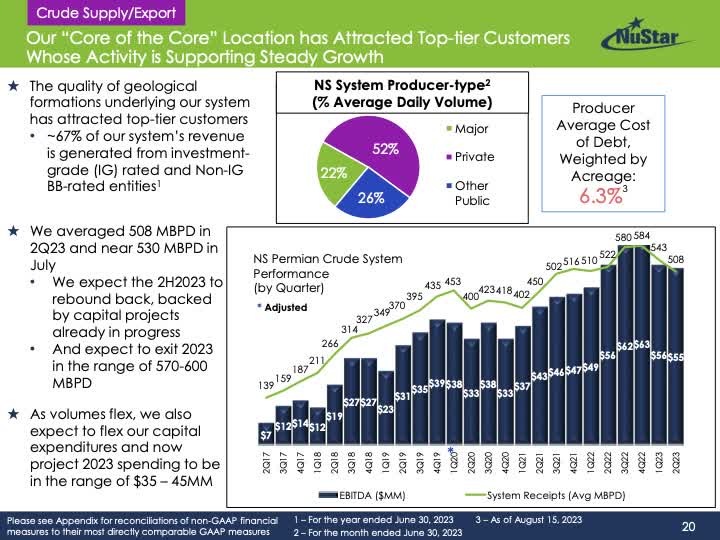

A third continued investment in the Permian likely adds EBITDA of a more predictable value. From a slide in the last presentation , details concerning EBITDA in the Permian follows.

{kind=link}

In 2022, values climbed to above $60 million quarterly before falling back into the middle $50 million during 2023. Investments are continuing and expectations for 2024 might produce values more equal to 2022. If reached, growth from the Permian will be in the $30-$50 million range.

Cash Flows

With the damaging Series D gone, a more flexible business model appears. From the 2022 annual report is a chart showing cash flows for the year. It is important to note that the interest payments for debt is already subtracted from the EBIDTA in determining cash from operations.

NuStar Energy

Cash from operations, the most important long-term source of cash, was $527 million. EBITDA in 2023 is likely to be similar. Growth in the Permian and other sources might increase 2024 EBITDA by $50 million plus. The next table summaries possible cash flows for 2024.

| Cash Flow Outlays (Millions) |

| Estimate: Cash from Operations |

| Revolver Interest Expense (7.9%) |

| Preferred |

| Common |

| Difference |

| 2024 |

| * $527 + $50 = $575 |

| $25 ** |

| $35 *** |

| $200 **** |

| $315 |

* Used 2022 similar with 2023 per the 3rd quarter report plus growth.

** The revolver contains approximately $335 million.

*** Series A (9,060,000 units outstanding as of September 30, 2023 and December 31, 2022) 218,307 218,307, Series B (15,400,000 units outstanding as of September 30, 2023 and December 31, 2022) 371,476 371,476, Series C (6,900,000 units outstanding as of September 30, 2023 and December 31, 2022), The 3-month LIBOR rates is now approximately 5.75% .

**** Common limited partners (125,895,543 and 110,818,718 units outstanding as of September 30, 2023 and December 31, 2022, respectively)

The estimated $300 million plus cash is drastically higher than past years. This is transformative and management with its two major spending needs, capital and debt reductions, has some flexibility. In the past, levels of capital equaled approximately $150 million, which leaves $150 million plus for debt reduction. In our view, until the revolver is paid off or an equivalent thereof, we don't see any distribution increases. Any meaningful increase might be two years away or more. With respect to valuation, it hasn't changed with the overall debt structure still in need of a level of repair. But we also don't see any decrease in the distribution. Cash flows are more than ample for it to continue at $1.60 per year.

Risks & Reward

Describing risk is always a difficult task. An economic risk continues with all investments. Projected Permian flow rates lagged in 2023 below more optimistic projections. This sector is a critical part of NuStar. But, for investors, the 2022 and 2023 results might have been a plateau, not a peak.

In our view, we don't see any distribution increases for at least a few years. Management must still address the debt within its revolver. What we expect is a company much better poised for growth and the ability to more quickly pay down its debt, thus NuStar still requires investor patience. The level of growth remains uncertain outside of the Permian Basin. More detail will come beginning in January with regard to expected investment returns for the ammonia project and management's expectations for 2024.

In the meantime, we plan to gather in the $1.60 distribution while selling covered calls at strike prices of $17.5 or $20. We rate this company a strong buy at current pricing near $17s. The new structure is under construction, but not yet completed.

For further details see:

NuStar Energy Starts Building A New Financial Structure