NTNX - Nutanix Earnings: This Business' Cash Flows Sizzle 23x Forward Free Cash Flows

2023-11-30 07:46:12 ET

Summary

- Nutanix simplifies IT infrastructure by combining storage, computing, and networking into a single platform, improving efficiency and performance.

- The company is priced at a reasonable valuation of 23x next year's free cash flows, with potential for 11% to 14% CAGR growth in fiscal 2025.

- Despite near-term challenges from competition and macroeconomic uncertainties, Nutanix's innovative approach and growth potential make it an attractive investment opportunity.

Investment Thesis

Nutanix ( NTNX ) simplifies IT infrastructure by combining storage, computing, and networking into a single, integrated platform. It helps organizations manage and scale their data centers more efficiently, reducing complexity and improving overall performance. Essentially, Nutanix streamlines the way businesses handle their IT resources for enhanced productivity. To put this slightly more technical, Nutanix allows its customers to hyperconverge their data, from on-premise to the cloud or across a multi-cloud environment.

According to my estimates, Nutanix is priced at about 23x next year's fiscal 2025 (ending in July 2025) free cash flows. If we presume, as I do, that Nutanix could grow by around 11% to 14% CAGR next year, this would be a very reasonable entry point for new investors to this name.

Rapid Recap,

Back in September, I said in a bullish analysis ,

Nutanix may not be a well-known name, but it makes up for that by being an exciting investment opportunity.

This is an exciting investment opportunity, as Nutanix is annualizing on a forward run-rate $2 billion in revenues. Further, the company still has some growth left and its valuation isn't stretched. There is a minor pesky detraction to the bull case, that I will expand upon soon. But in sum, there's a lot to like here.

Michael Wiggins De Oliveira work on NTNX

Since that time, the stock has been a strong performer, clearly beating the S&P 500 ( SPY ).

And yet my thesis remains as it did then. This is an exciting opportunity, but it's not a blemish-free investment thesis. So, let's get to it!

Nutanix's Near-Term Prospects

Nutanix offers a comprehensive enterprise cloud solution through its Nutanix Cloud Platform, allowing organizations to adopt a consistent cloud operating model across various environments.

Originally a pioneer in hyperconverged infrastructure, Nutanix has evolved into a software-focused company, providing a fully-fledged hybrid cloud solution.

Their platform simplifies workload management, supports diverse applications, and enables seamless transitions between on-premises and public cloud environments. Operating on a subscription-based model, Nutanix's versatile solution encompasses a scale-out architecture, enterprise-grade data services, and infrastructure flexibility for running diverse workloads.

Moving on, Nutanix CEO Rajiv Ramaswami described during the earnings call Nutanix's success due to its strategic focus on federal business "Our federal business is typically strong in our first quarter, and this one was no exception." The partnership with Cisco ( CSCO ) also shows early promise, with a joint solution made generally available, leading to several wins.

The company's foray into artificial intelligence with GPT-in-a-Box is gaining traction, as evidenced by its first win with a federal agency. Ramaswami emphasizes the broader perspective, stating, "We see this win as a great example of our ability to partner with the largest and most demanding companies in the world." Nutanix's commitment to innovation is further underscored by enhancements to its cloud platform to strengthen ransomware attack defenses.

Despite the positive momentum, Nutanix faces near-term challenges. The competitive landscape, especially with the recent acquisition of VMware by Broadcom ( AVGO ), introduces uncertainties. Ramaswami acknowledges this, stating, "The timing and magnitude of these deals [influenced by the VMware-Broadcom transaction] is unpredictable." Moreover, the macroeconomic backdrop adds complexity, with a modest elongation of average sales cycles observed.

Rukmini Sivaraman, in addressing the uncertainties, mentions, "As we continue to grow, the absolute dollar number of backlog would also increase over time."

While federal business contributes significantly, the reliance on it introduces seasonality risks. Additionally, the near-term challenges are heightened by potential pricing and support level issues arising from the competitive landscape. As Sivaraman points out, "There continues to be certainly a lot of concerns around all the stuff we've talked about in the past, pricing, increased pricing, potentially dropping support levels, et cetera." These challenges underscore that its strong results are far from guaranteed.

Revenue Growth Rates, A Discussion of Fiscal 2025

{kind=link}

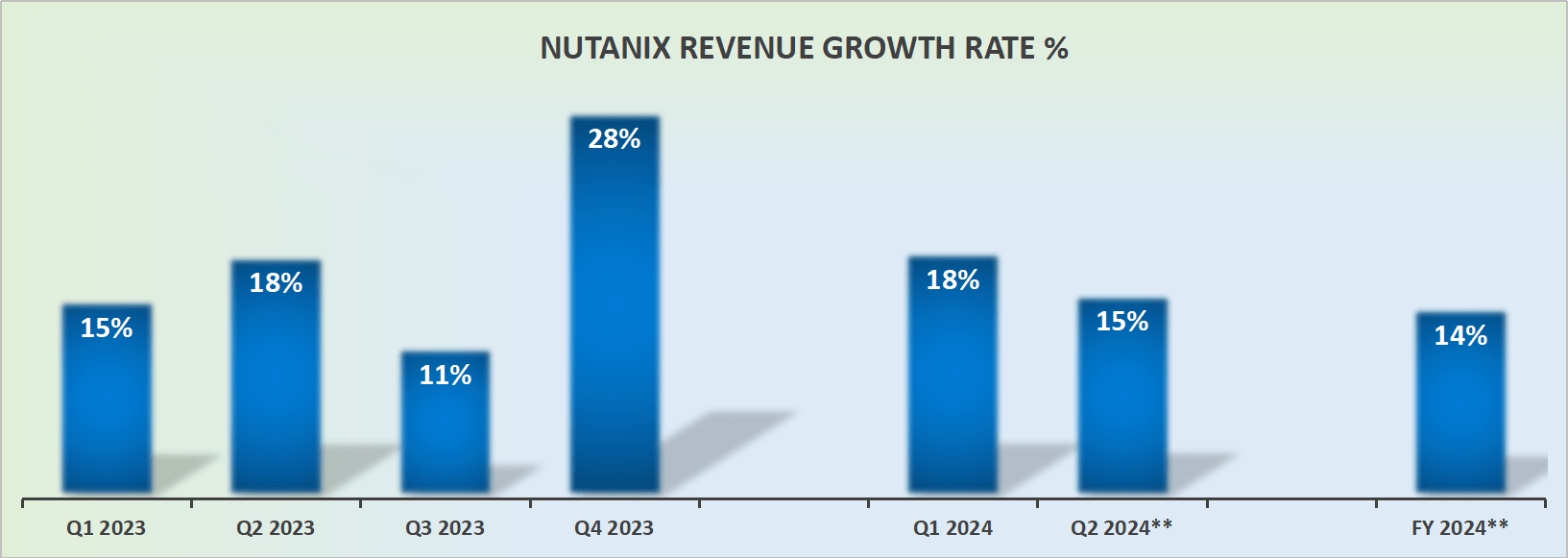

Now, allow me to get to the main blemish of this investment thesis. Nutanix's growth rates have a history of being spotty. It's difficult to make the case that this is a long-term secular growth story.

Even though it clearly has the narrative du jour, the fact remains that its outlook for fiscal 2024 was not raised.

Plainly, its guidance for fiscal 2024 (ending in July 2024), is for Nutanix to deliver 14% CAGR in the best-case scenario.

If we follow that line of thought further, this would mean that fiscal 2025 (ending in July 2025) would probably see this growth rate decelerate slightly further.

How much deceleration should we expect to see, of course, that's the critical question. Incidentally, keep in mind that from fiscal 2019 to fiscal 2022, those 4 years, Nutanix didn't deliver more than 14% CAGR for those years as a whole.

Therefore, I believe it's both prudent and reasonable to expect to see some level of deceleration in fiscal 2025. Moreover, Nutanix's carries about $1.2 billion of debt. Yes, it does hold $1.4 billion of cash, but its significant convertible notes sum will need to be tackled at some point. This means that there's little flexibility left in Nutanix's balance sheet for it to be able to make any large needle-moving acquisitions.

Nonetheless, I still expect Nutanix to deliver about 11% to 14% CAGR next year. A range that I believe is fair and reasonable, and leaves me with some room for error.

NTNX Stock Valuation -- 24x Next Year's Free Cash Flows

In my previous analysis, I concluded by saying,

With an attractive valuation, around 30x forward free cash flows, and a commitment to share repurchases, Nutanix presents a compelling investment opportunity, despite some debt-related considerations.

Accordingly, the best news to come out of this fiscal Q1 2024 earnings report is that Nutanix increased its free cash flow profile substantially. As we headed into its fiscal Q1 2024 results, it had guided investors towards $300 million of free cash flow at the high end.

And now, just 90 days later, Nutanix meaningfully increased its free cash flow outlook for fiscal 2024 towards $360 million at the high end.

Naturally, this surfaces two questions. Firstly, given that we are only at the start of Nutanix's fiscal year, what's going to be possible in the next quarter or the one after?

Given this dramatic bump in its free cash flow guidance this year, I wouldn't be surprised if the free cash flow figure at the end of this fiscal year actually ended closer to $380 million.

In practical terms, this would imply a jump of 84% y/y in its free cash flows. That's clearly an impressive number.

And now, the second question, what's likely to be Nutanix's free cash flow figure next fiscal year? Could its free cash flow increase by a further 20% y/y?

Of course, the bulk of the cost-cutting made this year will not be repeatable next year. But at the same time, there still would be some level of positive operating leverage built into the business.

Consequently, I believe that Nutanix could next year deliver approximately $460 million of free cash flow.

This implies that Nutanix is priced at roughly 24x forward free cash flow. This is a valuation that for me, doesn't appear stretched whatsoever.

Of course, the main consideration here would be that next year Nutanix could continue to deliver about 11%-14% CAGR.

In my previous analysis, I said,

[...] Management believes that it has more than enough cash and believes that its best use of cash is to repurchase its stock. As such, Nutanix has announced an open-ended $350 million share repurchase program.

During the earnings call, management noted that it only bought back $18 million worth of stock and that there's still an open share repurchase program ongoing. This means that there's a significant possibility that there could be more share repurchases coming at some point in the next twelve months.

If Nutanix used its total share repurchase allocation that's left, this would return to a further 2% to 3% of its market cap to shareholders. Thereby providing a further boost to investors' returns.

The Bottom Line

In conclusion, I find Nutanix to be a compelling investment opportunity, characterized by solid growth rates and reasonable valuation metrics. The company's innovative approach to IT infrastructure, seamlessly integrating storage, computing, and networking, positions it as a leader in streamlining data center management.

Despite facing near-term challenges arising from the competitive landscape and macroeconomic uncertainties, Nutanix's growth potential remains robust. I project its growth rates for fiscal 2025, ranging from 11% to 14% CAGR, providing a solid foundation for investment.

Noteworthy is the valuation at 23x next year's free cash flows, signaling an attractive entry point.

The increased free cash flow outlook for fiscal 2024 and the potential for continued positive operating leverage contribute to the favorable valuation, making Nutanix a compelling prospect for those seeking a balance between growth potential and financial stability.

For further details see:

Nutanix Earnings: This Business' Cash Flows Sizzle, 23x Forward Free Cash Flows