NTNX - Nutanix Finally Turned Profitable But Shares Aren't Cheap

2023-10-30 23:13:36 ET

Summary

- Nutanix has achieved its first profitable year and is on a sustainable path to profitability.

- The company has focused on large enterprise deals and partnerships to drive sales and upselling opportunities.

- Nutanix's customer count continues to grow, and they have a strong customer list with major companies.

- While we are positive about the company, and the shares are at the bottom of their trading range, the shares aren't cheap.

- The long-term uptrend itself depends partly on market sentiment, which isn't the best.

We used to write about Nutanix ( NTNX ), a leading cloud software provider, in a fairly distant past but finally gave up on the company as its path to profitability seemed endless.

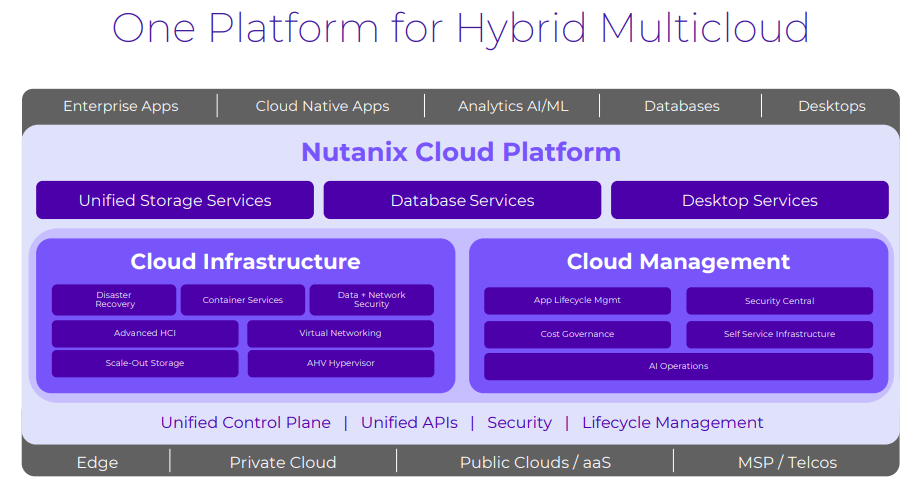

Nutanix provides a single software platform for managing all hybrid and multi-cloud applications and data, providing unified storage, database, and desktop services in order to support any application and workload. In a simple scheme from the 10-K :

{kind=link}

More interesting is that the company delivered its first GAAP profitable year and it looks like the company is now finally set to get on a sustainable profitable path.

How did they do that?

- Secular tailwinds from the digitization of business

- Shift towards a subscription model

- Focusing on large enterprise deals

- Focusing on partnerships to leverage sales

- Creating cross-selling and upselling opportunities

- Operational leverage

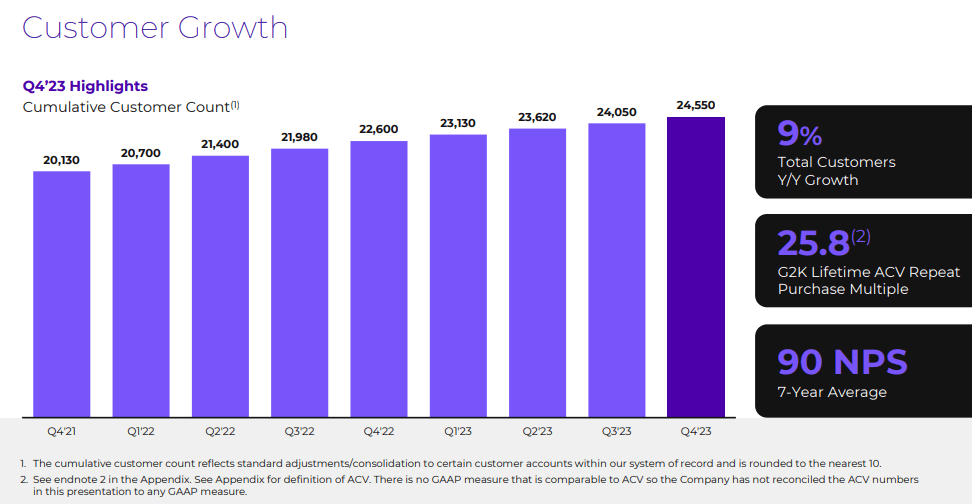

New customers

They have an impressive customer list already with some of the biggest companies around:

{kind=link}

And the customer count keeps growing nicely:

{kind=link}

They added 500 new logos in Q4 helped by seasonality and Broadcom/VMware troubles which made some companies look for a second source. From the Q4CC:

we closed multiple large deals with major enterprise and government customers. These wins demonstrate the strategic relevance of our platform to our customers’ key transformation initiatives and the success of our focus on landing these larger, more strategic transactions.

They didn't quantify ASPs for these larger deals, they did that at the Investor Day. Management mentioned DWP (the Department for Work and Pensions), the UK’s biggest public service department as a new customer in Q4.

And the company continued in Q1/24 where they left off in Q4/23 announcing a new big customer in the form of Micron .

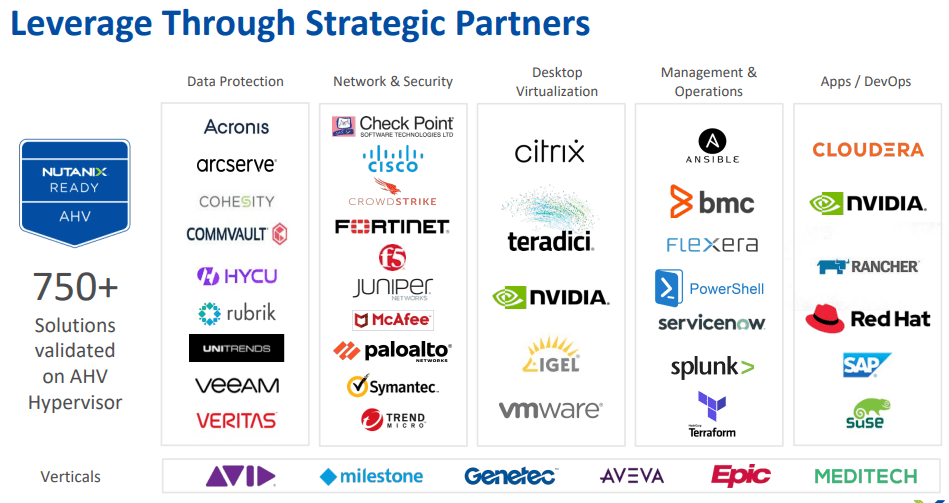

Partnerships

{kind=link}

The latest partnership is with Cisco , which integrates solutions, and a much bigger client base. Cisco sales force is getting compensated for Nutanix sales.

Upselling

Bigger deals with bigger customers involving more products are gradually driving ASPs higher. Some of the obvious add-on sales are cloud infrastructure and cloud management as ( Q4CC ):

Everybody who built the cloud also wants to operate the cloud

Other new products like NC2 (now available on Azure) which was the product that DWP chose and this is what DWP management said (Q4CC):

Nutanix NC2 allows DWP to seamlessly extend our on-premise footprint into public cloud, while avoiding the cost traditionally associated with lift and shift migrations. Furthermore, NC2’s cost effectiveness and ease of use enable us to maintain a layer of abstraction for our most critical workloads that avoids both platform and vendor lock-in.”

Other relatively new products like Unified Storage , Nutanix Central , Nutanix Vision , and the Nutanix database portfolio are also good upsell candidates. There were other product introductions (Q4CC):

meaningful new products in areas such as Kubernetes, data services and cloud management and defined our data services vision with Project Beacon to enable companies to build portable applications.

Another interesting new product is their GTP in a box .

AI

AI is generally a secular tailwind as it increases the demand for cloud computing in general and Nutanix has multiple products enabling these (Q4CC):

Today, we already have customers using our platform to deploy AI, often for inferencing on video or sensor data who are seeing the same agility, performance and TCO benefits from our platform as customers running other workloads.

More specifically, management notes that the training of large language models (inference) usually takes place in the cloud with public data but when companies actually implement AI they often prefer running it where the data is.

This is often on-premise (for privacy, safety, and compliance issues) and the company has developed a new product called GTP in a box, a turn-key solution to enable this, and noted considerable customer interest already.

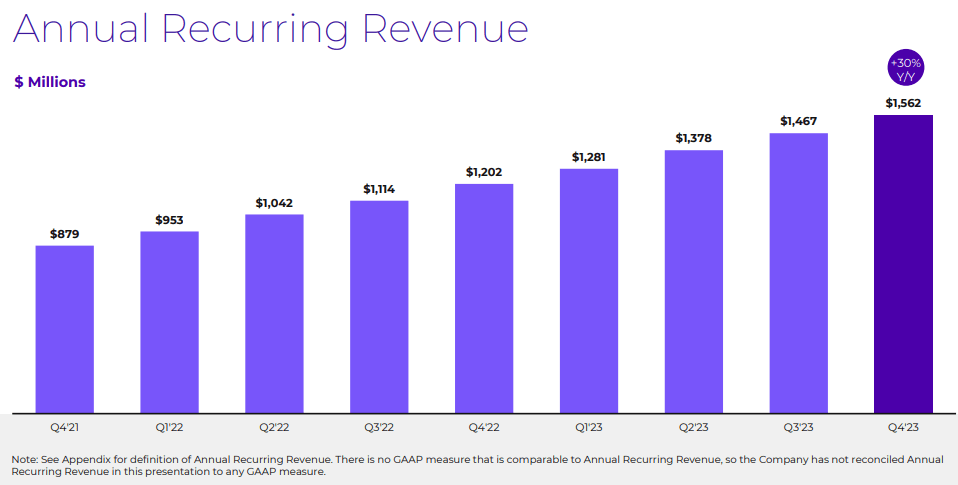

Subscription

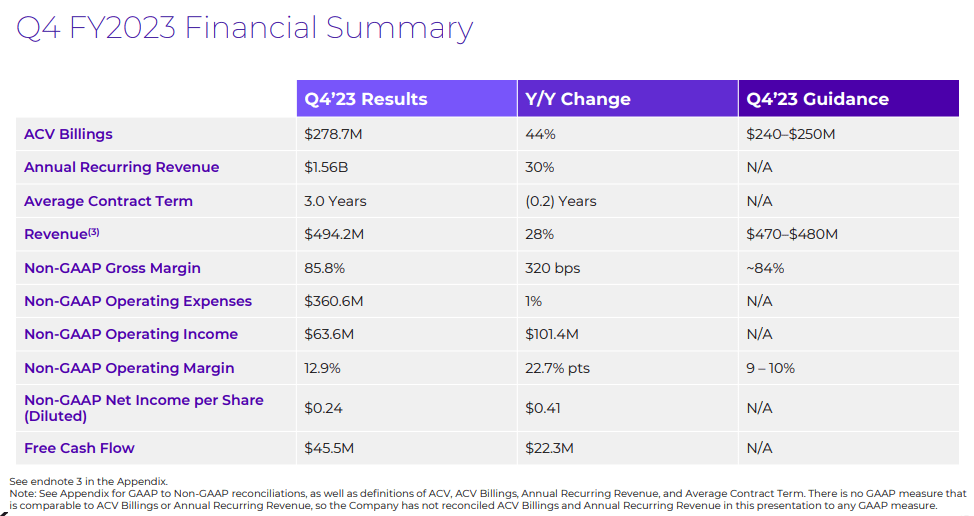

ARR (annual recurring revenue) +30% y/y to $1.56B at the end of Q4:

{kind=link}

The shift towards recurring revenue has been a drag on revenue growth as the subscription revenue arrives over 3 years (the usual contract length) instead of up-front all at once.

But once the majority of revenues come this way growth rates will converge (indeed, their FY24 guidance has both at +13%) and the benefit of subscription revenue is that it comes with higher gross margins:

There is some seasonal fluctuation as Q2 and Q4 are high-season revenue quarters while COGS and operating expenses don’t fluctuate as much over the year.

GRR (gross retention rate, excluding account expansion) at the end of FY23 was 90%a+, and NRR (net retention rate, including account expansion) was 123%, suggesting much revenue gains come from upselling.

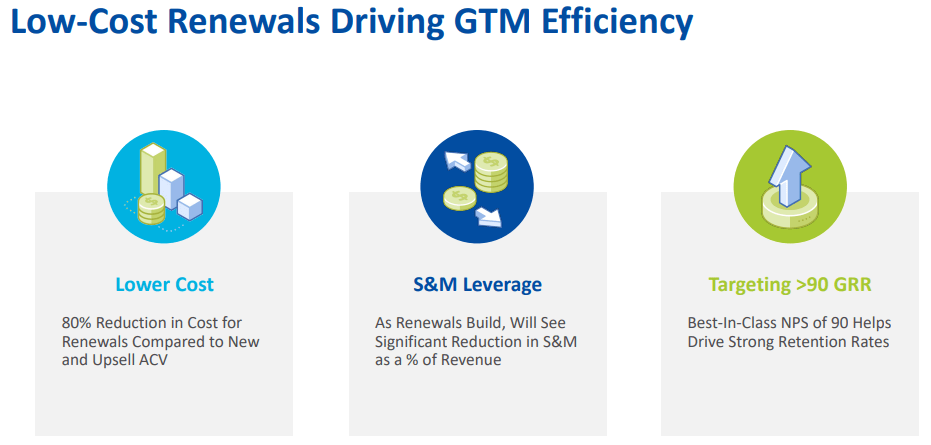

Operational leverage

The company managed to keep OpEx flat (even slightly down) in dollar terms, creating significant operating leverage:

One way this is achieved is through more efficient marketing, renewals especially are low-hanging fruit:

{kind=link}

For winning new clients they increasingly leverage the sales force and clients of partners, as we have seen above.

Finances

{kind=link}

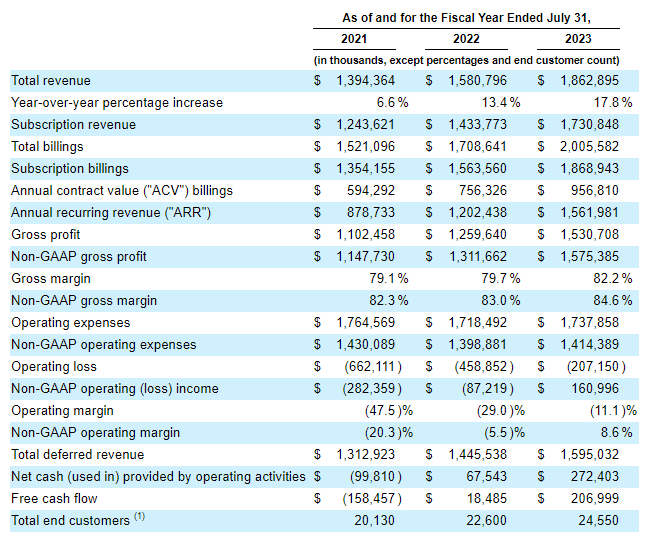

And for a longer-term perspective, from the 10-K :

{kind=link}

Some noteworthy items:

- ACV (annual contract value) billings were up 27% y/y led by the outperformance of their renewals business

- Renewals outperformed mostly due to better economics

- Renewals are growing but will slow down a bit due to one-time timing factors but reaccelerate in FY25

- ACV Q1/24 guidance down q/q but this is normal seasonality

- After keeping OpEx flat to down they're now making some targeted investments in go-to-market strategy and innovations.

- Cash and equivalents were $1.44B, up from $1.36B in Q3/23.

- The company pays just 2.5% interest on its ($750M) convertible note expiring in 2026 and just 0.25% on its ($575M) 2027 Notes so it's in no hurry to pay these off.

- The board approved a $350M share buyback program

- Stock-based compensation of $311.7M

- Interest cost $60.6M in FY23.

Guidance

FY24 guidance (Q4CC):

ACV billings of $1.075 billion to $1.095 billion, exceeding the $1 billion threshold and representing year-over-year growth of 13% at the midpoint; revenue of $2.085 billion to $2.115 billion, representing year-over-year growth of 13% at the midpoint of the range; non-GAAP gross margin of approximately 84%; non-GAAP operating margin of 11% to 12%; and free cash flow of $280 million to $300 million.

ACV billings are facing some temporary headwinds in FY24 due to timing issues (the shifting of some renewals from '24 to '23) but growth will accelerate again in FY25.

Longer-term, the growing mix of renewals over time as a proportion of total billings continues to be a driver of both billings growth and margin expansion.

Valuation

There are 239.6M shares outstanding and 65.6M to come from:

NTNX 10-K

That is, the company has a fully diluted market cap (at $35 per share) of $10.7B and an EV of $9.16B. Using the following analyst estimates:

- FY24 revenue $2.1B

- FY24 EPS $0.83 rising to $1.18 in FY25 (ending in July)

The shares sell at 4.36x EV/S but the earnings multiples are steep (46 for FY24 and 32 for FY25).

FinViz

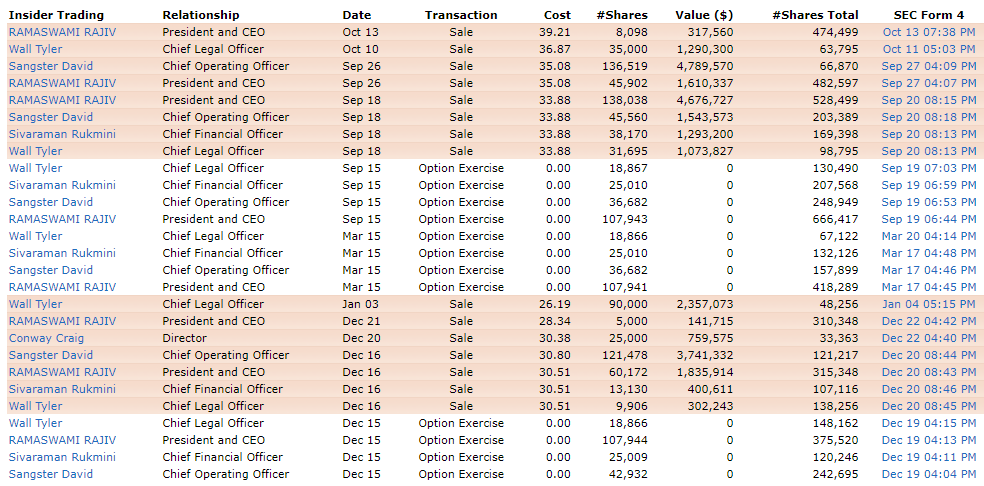

There has been substantial insider selling recently:

{kind=link}

Conclusion

The wait was long but the company finally managed to produce non-GAAP black figures for the year (FY23, which ended in July). Given reliable subscription growth and new products like GTP in a box producing rising ASPs and combined with a considerable amount of operating leverage we see financials improving.

But there are a few provisos:

- The shares are pretty expensive.

- ACV growth will decline to 13% in FY24 and OpEx will grow at 7%, so FY24 will produce much less operating leverage compared to FY23.

- With the recent troubles in the Middle East, macro uncertainties could easily worsen.

The upshot : The shares have reached the bottom of the rising trend channel so it's tempting to take a position here, but the uptrend itself depends to a significant extent on market circumstances.

Rising bond yields in particular have put a damper on market sentiment so we would not go full in here, and there has been substantial insider selling which dampens our enthusiasm a little further.

For further details see:

Nutanix Finally Turned Profitable, But Shares Aren't Cheap