NTNX - Nutanix: Leading The Charge With AI Deals To Drive Upside In 2024

2023-12-19 09:18:20 ET

Summary

- Nutanix is a strong choice for investors looking to enter the market rebound, with room for further upside in 2024.

- The company benefits from increased interest in automation and AI adoption, with potential for growth in AI-related use cases.

- Still trading at just ~4x current-year revenue, I view NTNX stock as having at least 20% more upside through mid-2024.

With markets soaring to YTD highs, many value-conscious investors are asking the same question: is it too late for me to move cash off the sidelines and throw money into the market rebound? My answer, of course, is no: but it requires thoughtful stock picking. In particular, we need to focus in companies that still have room to run from a valuation perspective, and have catalysts for growth in 2024.

Nutanix ( NTNX ) is a fantastic choice in this regard. The hyperconverged infrastructure software company has been on a tear this year as it executed very strong top line trends amid a challenging year for IT. Up more than 75% year to date, I still believe there is more upside for next year.

I last wrote a bullish note on Nutanix, when the stock was trading closer to $36 per share. Even with the strong rally since then (which has been in concert with other mid-cap tech stocks rallying on the back of lower interest rate expectations), I think Nutanix’s stock outperformance has been accompanied by both encouraging and new growth drivers as well as meaningful profit expansion.

AI is by now a bit of a tired conversation in the markets, and the top “obvious” plays like C3.ai ( AI ) and Palantir ( PLTR ) have already seen a substantial boom and bust cycle this year. But I also think companies like Nutanix that enjoy tangential benefits to AI adoption have plenty to benefit from increased interest in automation as well.

Nutanix management believes that AI will be deployed close to where the data is stored. And that’s what Nutanix is all about: building a fast infrastructure around data that can be rapidly used for analytics. In Q1, Nutanix started selling its “GPT in a Box” solution; and to a federal agency leveraging it for a crime detection use case, no less (which harkens very strongly to Palantir’s functions). Going forward, I see many more of these use cases driving continued demand for next-gen data platforms like Nutanix - especially for those organizations that want to run AI apps outside of the cloud and in their own data warehouses.

For all these reasons, I remain quite bullish on Nutanix. As a reminder to investors who are newer to this name, here is my full updated long-term bull case on Nutanix:

-

Category leader in the hybrid cloud- Though the buzzword "cloud" grabs all the media attention in the software industry these days, the reality is that many companies, especially those in complex or highly regulated industries, will never entirely move their systems into the cloud. Nutanix is a champion of the "hybrid cloud" strategy, in which some of a business's assets are in the cloud and others are in on-prem environments. For the on-prem assets, Nutanix's hyper-converged technology ensures that customers get the same performance and agility benefits that users receive in the cloud. Most companies today employ some sort of hybrid cloud strategy - meaning Nutanix products are widely applicable to all IT departments.

-

AI potential- Nutanix management believes AI applications will run where the data is housed. Already, the company has signed on major deals involving AI and GPT-related use cases.

-

Software-first- Earlier on in Nutanix's lifespan, the company sold server devices as its primary business, with its proprietary software overlaid as a "package solution." Now, Nutanix sells only software. This has dramatically raised its margin profile while also making it more palatable for companies who only want to consume software to run on their own hardware.

-

Annual recurring revenue at the forefront of Nutanix's sales focus- At the beginning of Nutanix's fiscal 2021, the company made the earth-shaking decision to incentivize its sales staff based on ACV and not TCV. In the past, Nutanix's account executives sold longer-term contracts and incentivized customers with bigger discounts because they were paid based on the value of the total deal. What's important for Nutanix and for investors, however, is how much Nutanix can rake in annually and for each customer's lifetime. So Nutanix shifted its sales compensation in line with this priority and began paying its sales teams based on ACV - and this has yielded very strong results in growing both ACV and ARR.

-

Prioritizing profitability- The company hit pro forma profitability for the first time in FY23 and is eyeing further gains ahead in FY24 on the back of a ramping gross margin profile.

In spite of these strengths, I continue to think that Nutanix trades cheaply. At current share prices near $46, the company trades at a market cap of $11.24 billion. After netting off the $1.44 billion of cash and $1.22 billion of convertible debt on Nutanix’s most recent balance sheet, the company’s resulting enterprise value is $11.02 billion.

Meanwhile, for the current fiscal year FY24 (the year for Nutanix ending in September 2024), Wall Street analysts are expecting the company to generate $2.48 billion in revenue, representing 17% y/y growth. This puts Nutanix’s valuation at 4.4x EV/FY24 revenue.

In my view, Nutanix’s combination of top-line growth catalysts (including and especially AI-driven use case expansion) plus high gross margins that are yielding strong profit gains merit at least a 5.5x revenue multiple for the company, implying a $57 price target for the stock and ~23% upside from current levels.

Stay long here and keep riding the recent upside trends.

Q3 download

Let’s now cover Nutanix’s latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

Nutanix Q3 earnings summary (Nutanix Q3 earnings release)

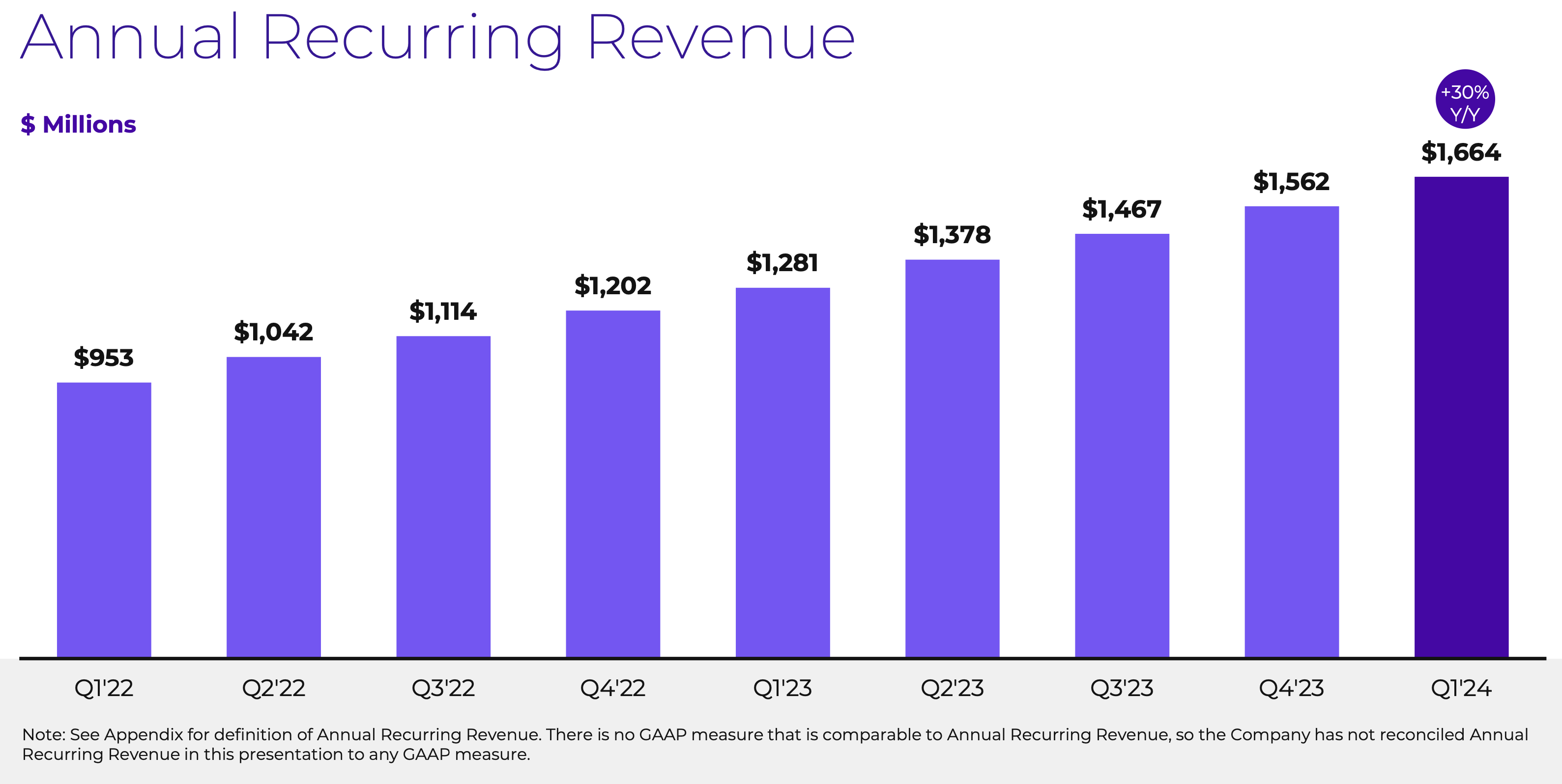

Nutanix’s revenue grew 18% y/y to $511.1 million, well ahead of Wall Street’s $500.8 million (+15% y/y) by a three-point margin. The company also saw strength in ARR adds, growing 30% y/y to $1.66 billion - a $102 million sequential increase to the recurring revenue base, up from $95 million in the previous quarter.

{kind=link}

Nutanix ARR (Nutanix Q3 earnings release)

The company noted specific strength in the federal government sector in Q1, including the aforementioned GPT-in-a-Box deal: which was Nutanix’s first such win for the product with an existing large customer. It’s also comforting to note that public sector clients - which have a reputation for longer approval processes - have been quick to adopt new AI-related products, which is a harbinger for increased adoption to benefit calendar 2024 trends.

Nutanix has also been able to drive go-to market expansion through reseller partners. In particular, it has deepened its relationship with Cisco, whose sales team is now pushing a joint Cisco-Nutanix solution.

Still, the company is noting some overhang of macro impacts, and is also expecting some of these effects to linger into next year. Per CFO Rukmini Sivaraman’s remarks on the Q1 earnings call:

Similar to last quarter, we saw a modest elongation of average sales cycles, relative to the year ago quarter […]

We are seeing continued new and expansion opportunities for our solutions, despite the uncertain macro environment. However, as we mentioned previously, we have continued to see a modest elongation of average sales cycles. Our fiscal year '24 new and expansion ACV performance outlook assumes some impact from these macro dynamics. Second, the guidance assumes that our renewals business will continue to perform well.

And a reminder that while our available to renew, or ATR pool, continues to grow year-over-year, it is growing at a slower pace in fiscal year '24, but is expected to reaccelerate in fiscal year '25, based on our current view.”

Note that the comment on higher renewal base starting in FY25 is a great leading indicator for continued strong growth trajectory.

From a profitability standpoint, pro forma gross margins hit a sky high level of 85.9%, up 250bps y/y. Note that one of the common misconceptions of Nutanix - based on its earlier post-IPO business model - was that it sold commoditized hardware. Now with margins approaching 90% and towering over most of the software sector, it’s difficult to argue that Nutanix is anything but a software company.

Pro forma operating income of $79.5 million also notched a 15.5% margin, up from just 2.3% in the year ago quarter. Needless to say, Nutanix is truly showing the profitability potential of a more mature software company that has slowed down opex growth and is capitalizing on strong expansions/renewals.

Key takeaways

Choosing companies with both a reasonable valuation and clear catalysts for outperformance in 2024 is a critical strategy for outperforming the markets next year. Though Nutanix has already recorded plenty of gains this year, there’s still room to go even further.

For further details see:

Nutanix: Leading The Charge With AI Deals To Drive Upside In 2024