NTNX - Nutanix Q1 Earnings: Shares Spike On Strong Guidance

2023-05-26 08:15:00 ET

Summary

- Nutanix saw its stock price rise 35.8% since September 2022, significantly outperforming the S&P 500.

- The company reported Q1 2023 revenue of $448.6 million, an 11.1% increase YoY, driven by a 12.7% increase in subscription revenue thanks to strong customer growth.

- Despite improvements in revenue, profits, and cash flows, Nutanix's high valuation and negative profits make it no better than a "hold" candidate.

Growth investing can be highly profitable when done right. But it can also be a very difficult way to make money in the market. A big part of the challenge of this investment philosophy is that you pay a premium for the stock in question and hope that future growth justifies that premium. Add on top of this the fact that company and industry conditions can change rather rapidly, and that you never know exactly how high a premium the market will come to accept, and it is an investment approach that I believe only works well for those with a high risk tolerance and who have significant experience. Even the most seasoned investors you can see their investment calls turn out wrong, whether that's in the short run or in the long run.

A great example that I can point to from my own experience is with Nutanix (NTNX), a company built around providing an enterprise cloud platform to its customers that consists of software solutions and various cloud services. Even though there are concerns about the cloud market slowing down right now, the overall trajectory for this space is positive. And even though shares of the business have been very pricey for a long while, continued revenue growth and some improvement on its bottom line, has helped to push the stock even higher. Given how pricey shares of the company are at this moment, I would most certainly tread carefully. But I would not go so far as to take a bearish stance.

A firm that has exceeded expectations

Back in early September of last year, I wrote my first article regarding Nutanix. In that article, I recognized that the company was continuing to grow at a nice clip. The firm was also making good progress toward generating consistently positive cash flows. Normally, these are factors that would warrant a great deal of optimism. But I felt that, on the whole, the company still had a long way to go before making for a solid prospect for most investors. I felt as though shares of the enterprise were expensive and that, absent continued significant improvements, the stock would make for nothing better than a 'hold' candidate. Since then, the market has strongly disagreed with me. Shares of the company are up 35.8% compared to the 5.6% seen by the S&P 500.

{kind=link}

A good portion of this upside came in a single day. That happened to be May 25th, when shares spiked 16.8%. This move higher was in response to earnings figures provided by management. Although the financial results of the company were somewhat mixed, they were more positive than negative. On top of this, management increased guidance for the 2023 fiscal year and announced the end of an internal investigation that was hanging over the firm's head.

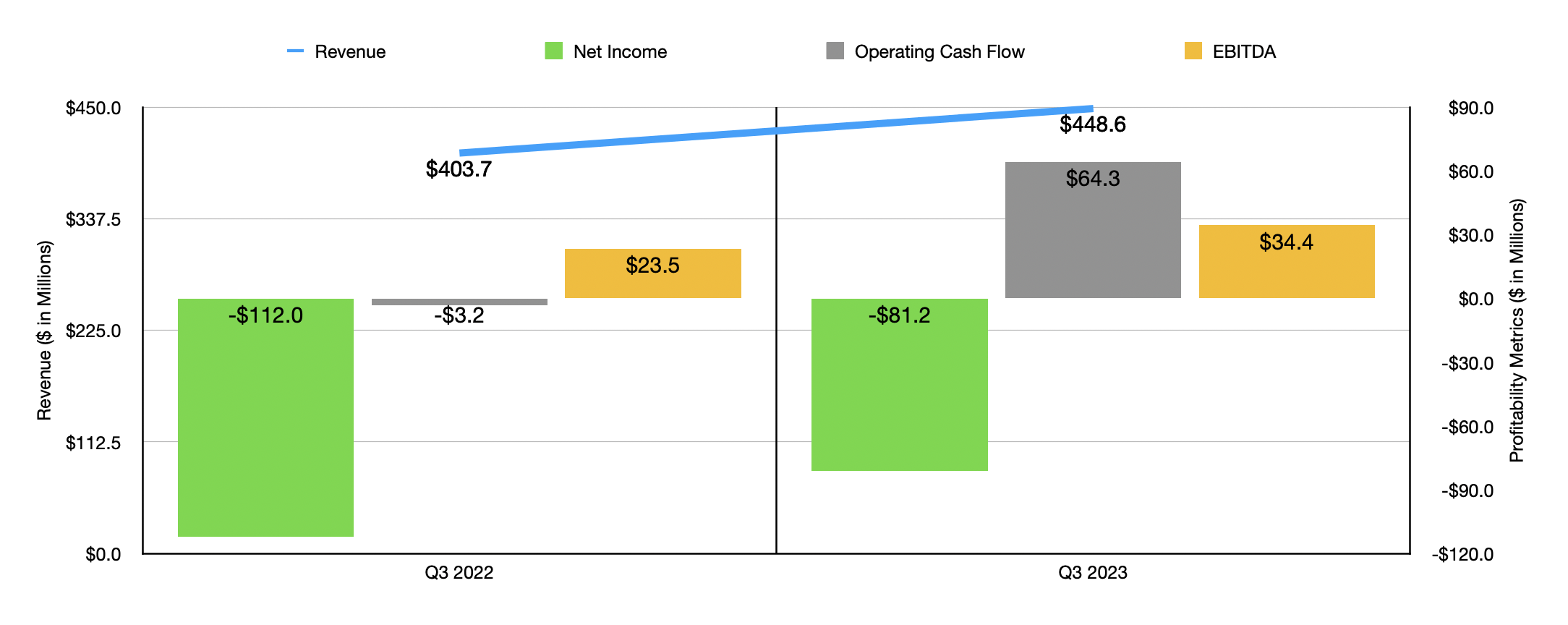

To start with, we should touch on financial results for the quarter. Based on the data provided, Nutanix reported revenue of $448.6 million for the first quarter of its 2023 fiscal year. That's 11.1% higher than the $403.7 million generated one year earlier. The sales figure reported by management actually came in about $15.2 million above what analysts anticipated . When you look under the hood, you actually find that, across almost every category, sales actually weakened year over year. The one exception was when it came to subscription revenue. This spiked 12.7%, rising from $370.5 million to $417.5 million. Revenue here includes performance obligations that have a defined term and that's generated from the sales of software entitlement and support subscriptions, subscription software licenses, cloud-based SaaS (Software-as-a-Service) offerings, and more.

{kind=link}

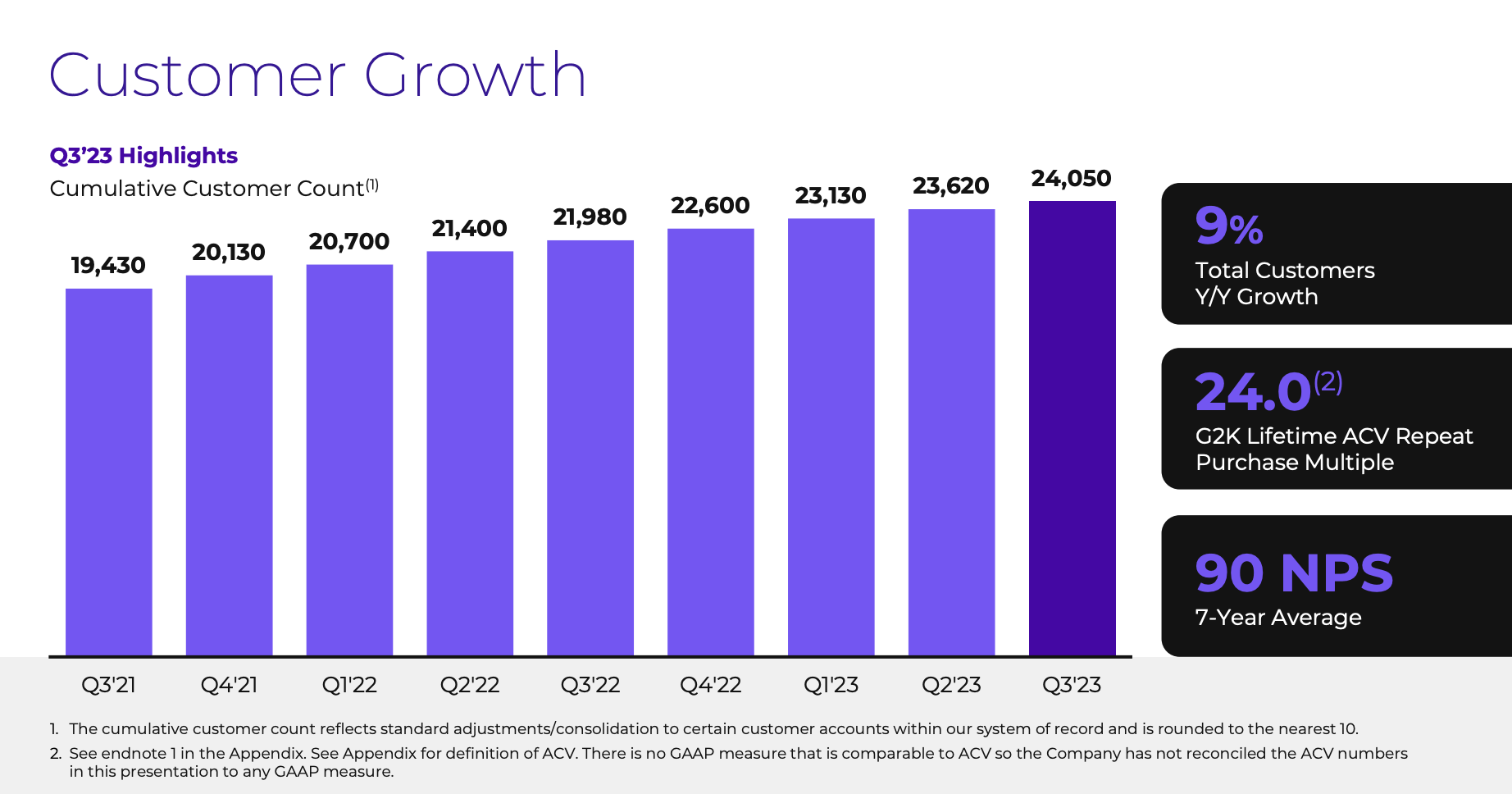

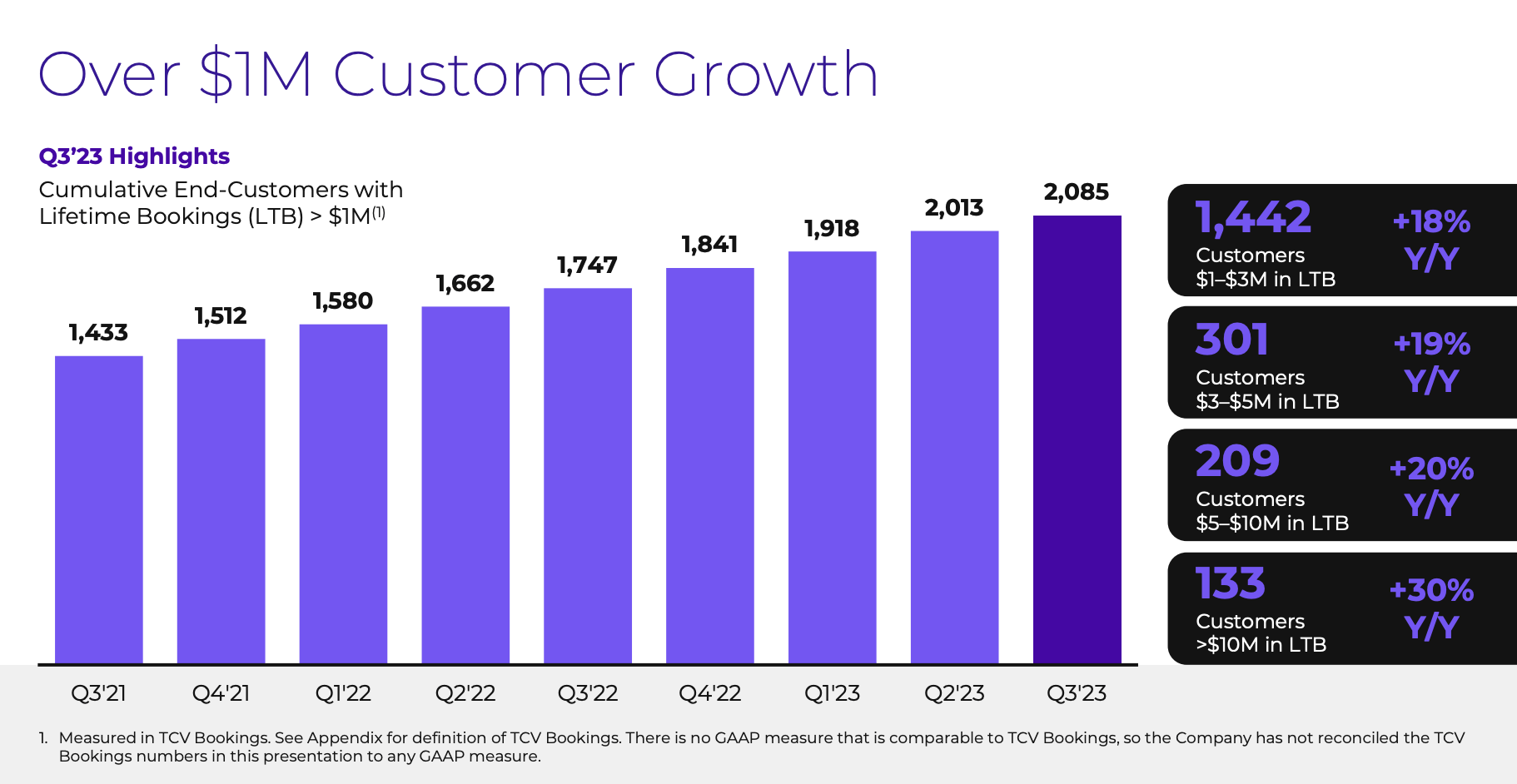

Subscription revenue growth was driven largely by an increase in the number of customers that the company services. At the end of the most recent quarter, it boasted 24,050 customers. That's up from the 23,620 that it had in the second quarter of the year and it is 9.4% above the 21,980 that the company had one year earlier. Customer growth was even more impressive when you look at customers that are responsible for $1 million or more in revenue per year. At the end of the most recent quarter, the company had 2,085 customers that fit this description. That compares to the 2,013 that it had only three months earlier and it is up 19.3% compared to the 1,747 customers that the company had the same time last year.

{kind=link}

On the bottom line, the picture was not as clear cut. For instance, the company reported a loss per share of $0.35. While this was better than the $0.50 per share loss the company reported one year earlier, the results did miss analysts' expectations by $0.01. But on an adjusted basis, the profit per share of $0.04 exceeded what analysts expected to the tune of $0.01 per share. But it translated to an overall loss for shareholders of $81.2 million. At least that was better than the $112 million loss generated the same time last year. This was not the only area that the company saw improvement on when it came to its bottom line. Operating cash flow, for instance, went from negative $3.2 million to positive $64.3 million. Meanwhile, EBITDA improved from $23.5 million to $34.4 million.

{kind=link}

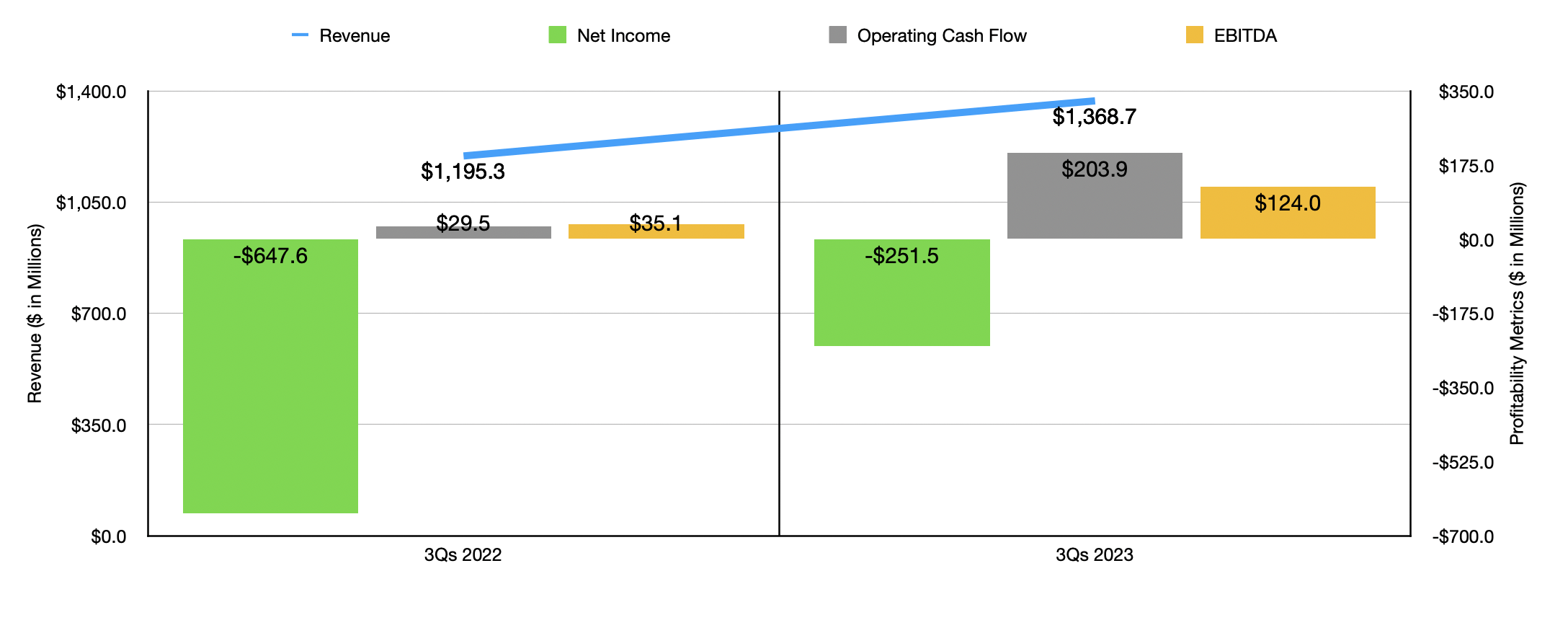

The improvements that the company saw in the third quarter relative to the same time last year were not a one-off thing. In fact, the business reported improvements across the board for all of its metrics for the first nine months of 2023 relative to the same nine months of 2022. In the chart above, you can see precisely what I mean, covering revenue, net profits, operating cash flow, and EBITDA. In addition to benefiting from increased revenue, the company saw some margin improvement during this time. During the first nine months of 2023, for instance, the gross profit margin of the company was 81.5%. That's up from the 79.8% seen one year earlier. Though this may not seem like a big disparity, when applied to the revenue generated during that time, it translated to $23.3 million in additional bottom line pre-tax profits. There were, of course, other areas of even greater improvement. Despite revenue coming in higher, the company saw a meaningful decline in its sales and marketing expenses. In the first nine months of this year, this figure came in at $697.4 million. The same time one year earlier it was $726.5 million.

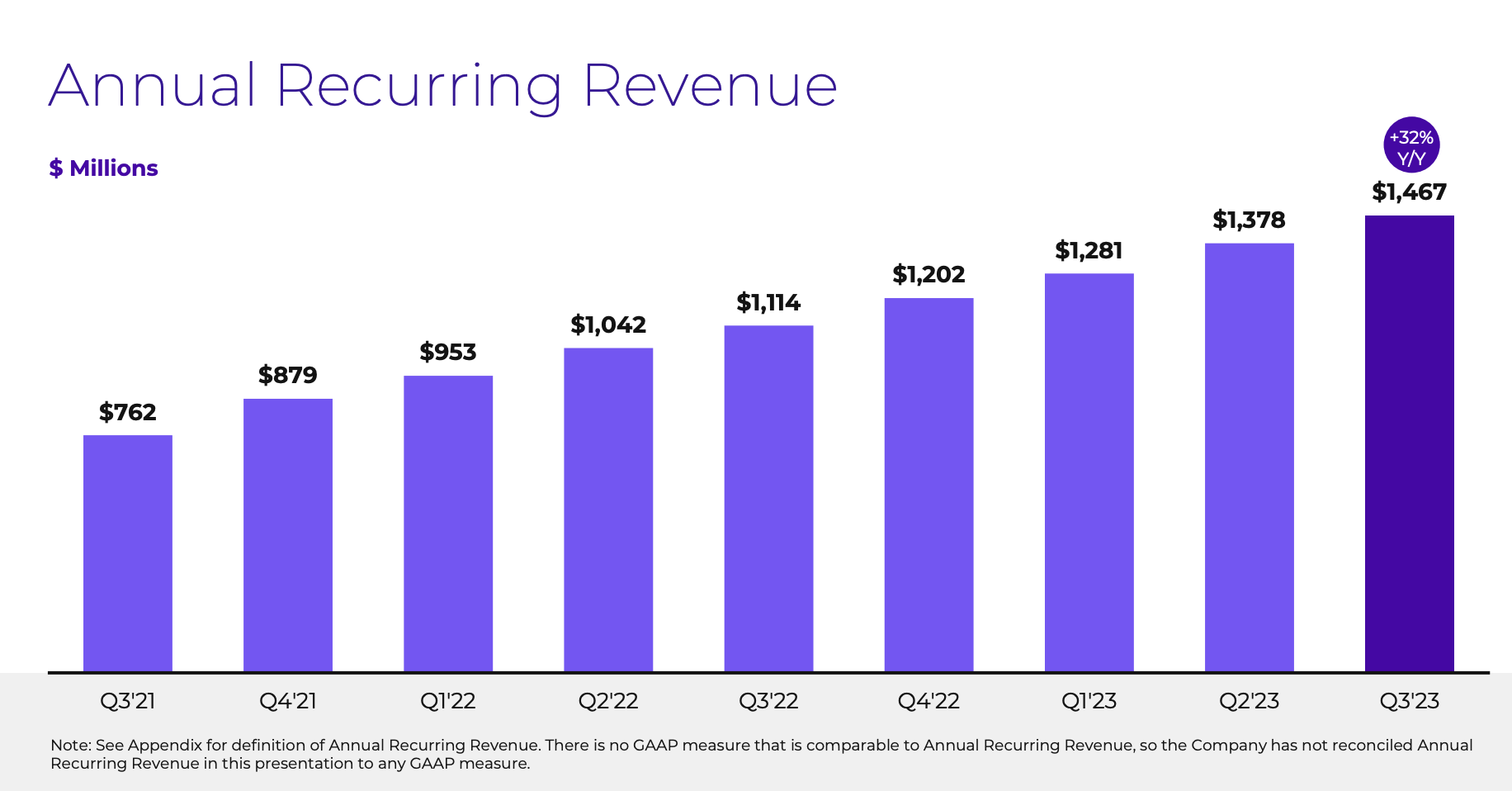

In addition to having generally positive financial results for the quarter, the company also managed to raise guidance for the year. The current expectation is for revenue of $1.84 billion to $1.85 billion. Prior expected guidance when the company announced financial results for the second quarter of 2023 was for revenue of between $1.80 billion and $1.81 billion. This increase in guidance was made possible by a surge in annual recurring revenue that the company has on its books. This number now totals $1.47 billion. That's 31.7% above the $1.11 billion that it reported one year earlier. ACV billings also were revised higher, to between $915 million and $925 million. By comparison, prior guidance called for this number to be between $905 million and $915 million.

{kind=link}

Unfortunately, the other guidance management provided was not adequate enough to give us a firm understanding of what cash flow might look like for the year as a whole. But if we assume that the fourth quarter of the year will see improvements like the first three quarters of the year did relative to the same time last year, then we would expect adjusted operating cash flow of $244.2 million. If we add back to this interest expense and taxes, we would expect adjusted EBITDA of around $283.6 million.

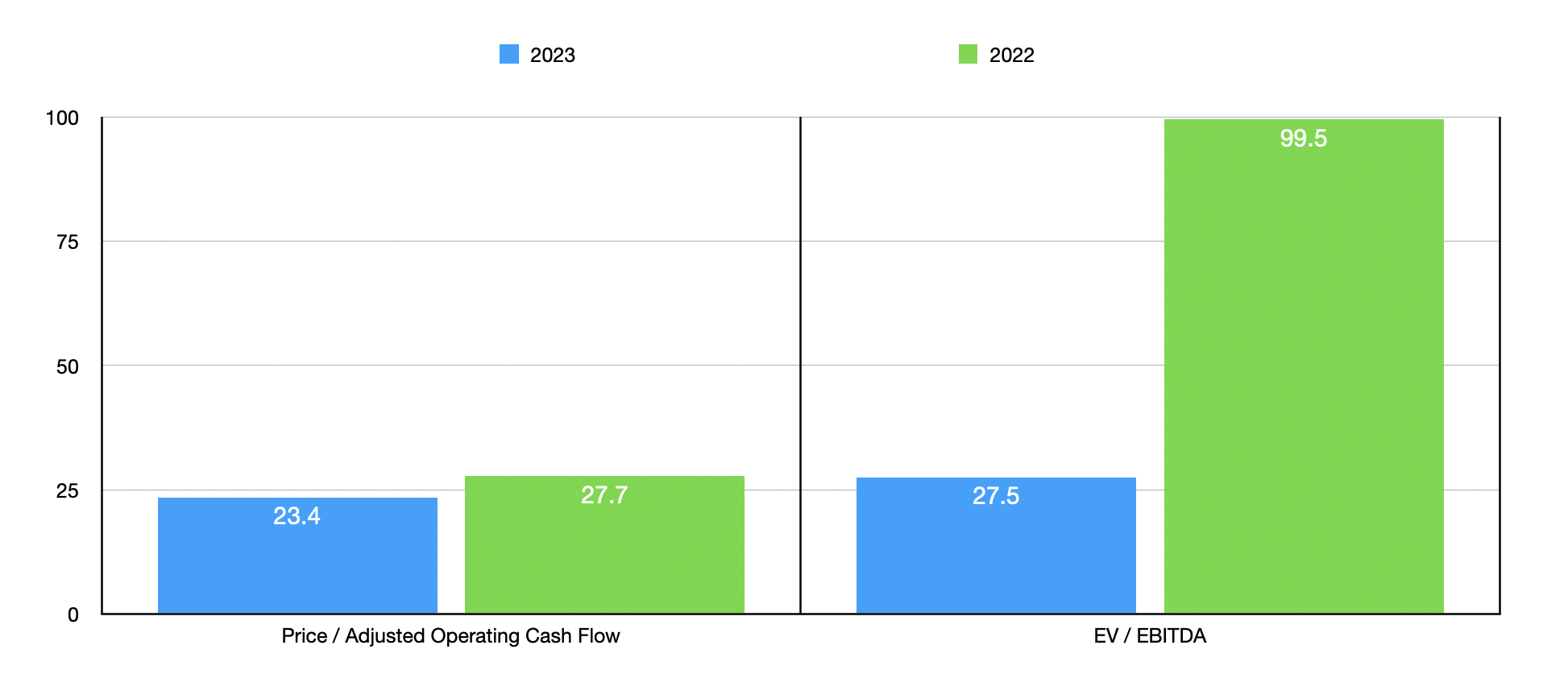

If these numbers come to fruition, shares of the company still look quite pricey. On a forward price to adjusted operating cash flow basis, shares are trading at a multiple of 27.5. However, that is substantially lower than the 99.5 reading that we would get using data from 2022. Fortunately, the EV to EBITDA multiple for the company, aided by a surplus of cash on the company's books, comes out a bit lower at 23.2. That compares to the 52.9 rating we would get using data from last year. Truthfully, I would not call any of these numbers that appealing. Though it is great to see such a significant improvement year over year.

{kind=link}

Outside of the valuation picture, there is one other thing that's worth mentioning. Earlier in the article, I brought up an internal investigation that the company was conducting. This investigation began around the time of the second quarter earnings release. The investigation itself was conducted by the company's Audit Committee and involved concerns about third party software usage. The committee ultimately determined that evaluation software from two software providers had been used in a non-compliant manner at the company over a multi-year period. Furthermore, the committee alleged that some employees had concealed the non-compliant use of the software, an act that was in violation of the company's code of business conduct and ethics, as well as other policies.

Fortunately for investors, this matter ended up being fairly small in the grand scheme of things. Although use of the software dated back to 2014 and ended only very recently, the overall impact to the company's financial statements in the form of costs came out to $11 million. Some additional costs, likely to total in the low single digit millions of dollars, will be realized moving forward as part of this. And the company also acknowledged that these issues constituted a material weakness over its internal control over financial reporting. Assuming there are no additional skeletons hiding in the closet, the impact to shareholders moving forward should be negligible.

Takeaway

Operationally, I would make the case that Nutanix is showing some nice improvements. Revenue continues to grow. Profits and cash flows are getting better. The aforementioned internal investigation is over and was not material in and of itself. And on the revenue side, management revised guidance higher. All things considered, I would consider this most recent quarterly release a win for the company. But I am still skeptical of a business that is trading at the multiples it is trading at. This is especially true when you consider that the firm's profits are still significantly negative. So even though my last call did not work out as I would have hoped, I do believe that a 'hold' rating is still appropriate at this time.

For further details see:

Nutanix Q1 Earnings: Shares Spike On Strong Guidance