NTNX - Nutanix: Rare Sales Momentum In A Tough Environment

2023-05-25 22:23:32 ET

Summary

- Shares of Nutanix rallied more than 15% after the company posted very strong Q3 results.

- ARR grew more than 30% y/y while ACV billings grew nearly ~20% y/y, on top of landing hundreds of new customers.

- New initiatives like Project Beacon extend Nutanix's PaaS offerings to public cloud deployments.

- Expense controls have also helped Nutanix generate strong free cash flow.

Over the past two quarters, it's been rare to see a technology company - particularly one that sells a more capital investment-heavy product - report good results. In the current macro backdrop, companies are deprioritizing transformation projects in order to conserve cash and protect the bottom line, and as a result many IT investments are being delayed.

Even though Nutanix ( NTNX ) is no stranger to these conditions, the hybrid cloud company is managing to eke out much stronger than expected results. Up ~12% year to date, the company staged a ~15% rally after reporting strong fiscal Q3 results.

In my view, there's plenty of steam left in the Nutanix rally - especially considering earlier acquisition talks that highlight how attractive of a target Nutanix might be for a larger tech company, even if these discussions have not yet materialized into actions. I remain bullish on Nutanix and continue to ride out the stock in my portfolio.

As a reminder to investors who are newer to this name, here are the key reasons to be bullish on Nutanix:

-

Enabling the hybrid cloud: Not all workloads can be moved to the cloud. These days, IT and computing are all about the cloud. But while the market is chasing after all the hot cloud stocks, the reality is that most companies - especially those in complex or highly regulated industries, or those that simply want more direct control over their data - will never entirely move their systems into the cloud. Nutanix is a champion of the "hybrid cloud" strategy, in which some of a business's assets are in the cloud and others are in on-prem environments. For the on-prem assets, Nutanix's hyper-converged technology ensures that customers get the same performance and agility benefits that users receive in the cloud. Most companies today employ some sort of hybrid cloud strategy - meaning Nutanix products are widely applicable to all IT departments.

-

Thought leader in hyper-converged infrastructure. VMware (VMW) has been chasing Nutanix's tail ever since the company gained prominence. For multiple years in a row, the company has been recognized as the category leader by Gartner, the software industry's leading analyst and reviewer.

-

Software-first. Earlier on in Nutanix's lifespan, the company sold server devices as its primary business, with its proprietary software overlaid as a "package solution." Now, Nutanix sells only software. This has dramatically raised its margin profile while also making it more palatable for companies who only want to consume software to run on their own hardware.

-

Executing its new sales strategy. At the beginning of Nutanix's fiscal 2021, the company made the earth-shaking decision to incentivize its sales staff based on ACV and not TCV. In the past, Nutanix's account executives sold longer-term contracts and incentivized customers with bigger discounts because they were paid based on the value of the total deal. What's important for Nutanix and for investors, however, is how much Nutanix can rake in annually and for each customer's lifetime. So Nutanix shifted its sales compensation in line with this priority and began paying its sales teams based on ACV - and this has yielded very strong results in growing both ACV and ARR.

-

Prioritizing profitability. Nutanix made the decision to lay off 4% of its workforce, which is helping the company push above breakeven pro forma operating margins and deliver positive FCF.

Valuation wise, Nutanix also looks incredibly reasonable (note as well as a reminder that Nutanix used to be a part-hardware, part-software company. Even though the company's revenue is now pure software with an >80% pro forma gross margin, Nutanix's valuation multiples have not yet fully reflected its new reality). At current share prices near $29, Nutanix trades at a market cap of $6.75 billion. After we net off the $1.32 billion of cash and $1.30 billion of debt on Nutanix's most recent balance sheet, the company's resulting enterprise value is $6.73 billion.

Meanwhile, for FY24 (the fiscal year for Nutanix ending in October 2024), Wall Street analysts (data from Yahoo Finance ) are expecting the company to generate $2.06 billion in revenue, representing 15% y/y growth (note as well that consensus is calling for Nutanix to post a full-year positive pro forma EPS for the first time next year, though the company's bottom line will still be too nascent to support its valuation). This puts Nutanix's valuation at just 3.2x EV/FY24 revenue.

The bottom line here: there's a lot of untapped value in NTNX stock, especially as the company continues to execute on its software-driven sales strategy against a tough macro backdrop. Stay long here and ride the upward momentum.

Q3 download

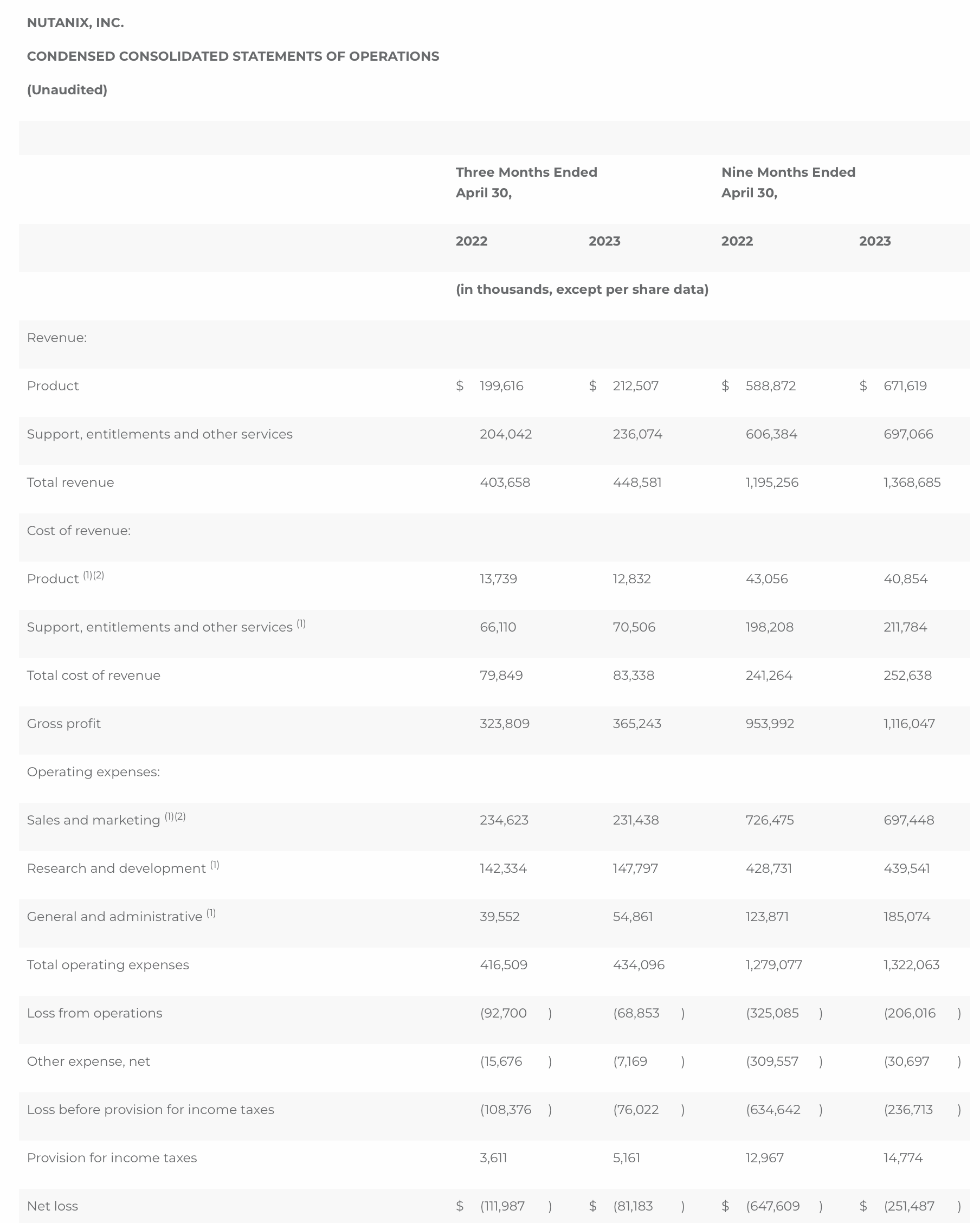

Let's now go through the company's latest quarterly results in greater detail. The fiscal Q3 (March quarter) earnings summary is shown below:

Nutanix Q3 results (Nutanix Q3 earnings release)

{kind=link}

Nutanix grew revenue at a 10% y/y clip to $448.6 million, beating Wall Street's expectations of $429.4 million (+11% y/y) by an impressive four-point clip. And in spite of sales headwinds across most of the industry, Nutanix landed 430 net-new customers in the quarter, growing its overall customer base by 9% y/y.

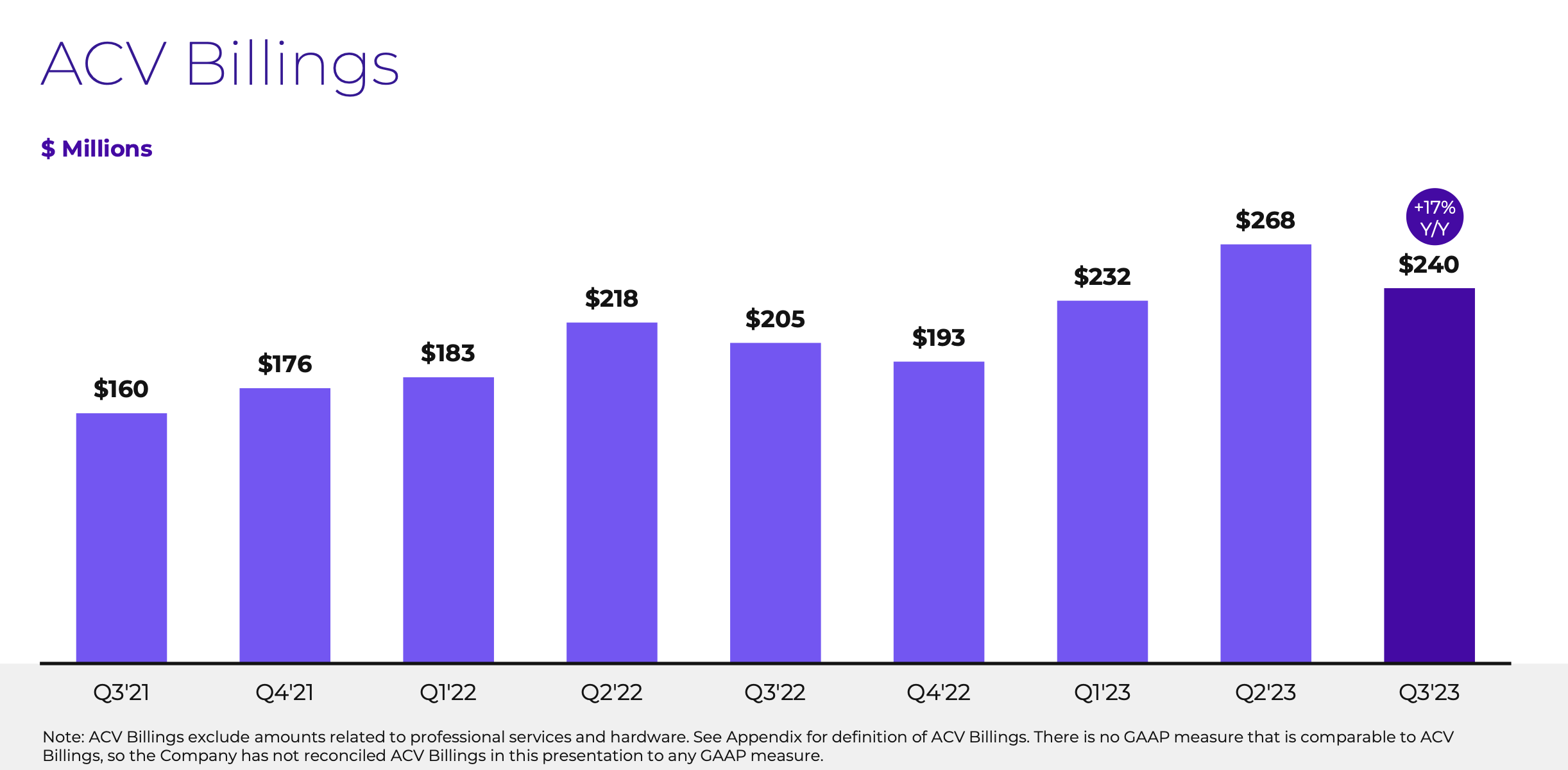

The company also continued a strong trend in ACV billings, up 17% y/y to $240 million:

Nutanix billings (Nutanix Q3 earnings release)

{kind=link}

Even better news still: the company's guidance for Q4 calls for ACV billings in a range of $240-$250 million, which implies growth accelerating to 27% y/y.

Management notes that in spite of a softer macro environment that has driven an elongation in deal cycles (which is similar commentary to what other software companies have reported), Nutanix has still been able to find and close sales opportunities. Per CFO Rukmini Sivaraman's remarks on the Q3 earnings call :

First, we are seeing continued new and expansion opportunities for our solutions despite the uncertain macro environment. However, as Rajiv mentioned, and similar to last quarter, we have seen a modest elongation of sales cycles likely due to increased deal inspection. Our fiscal year 2023 new and expansion ACV performance remains impacted by some of these macro dynamics and is performing slightly below our expectations entering the year and what we believe is longer term potential is. We have considered this dynamic in our updated guidance. The renewal business continues to perform well. However, it tends to be at a lower aggregate average contract duration compared to our new and expansion business. Our relative economics on renewals have also continued to improve over time as the renewals team has improved their execution."

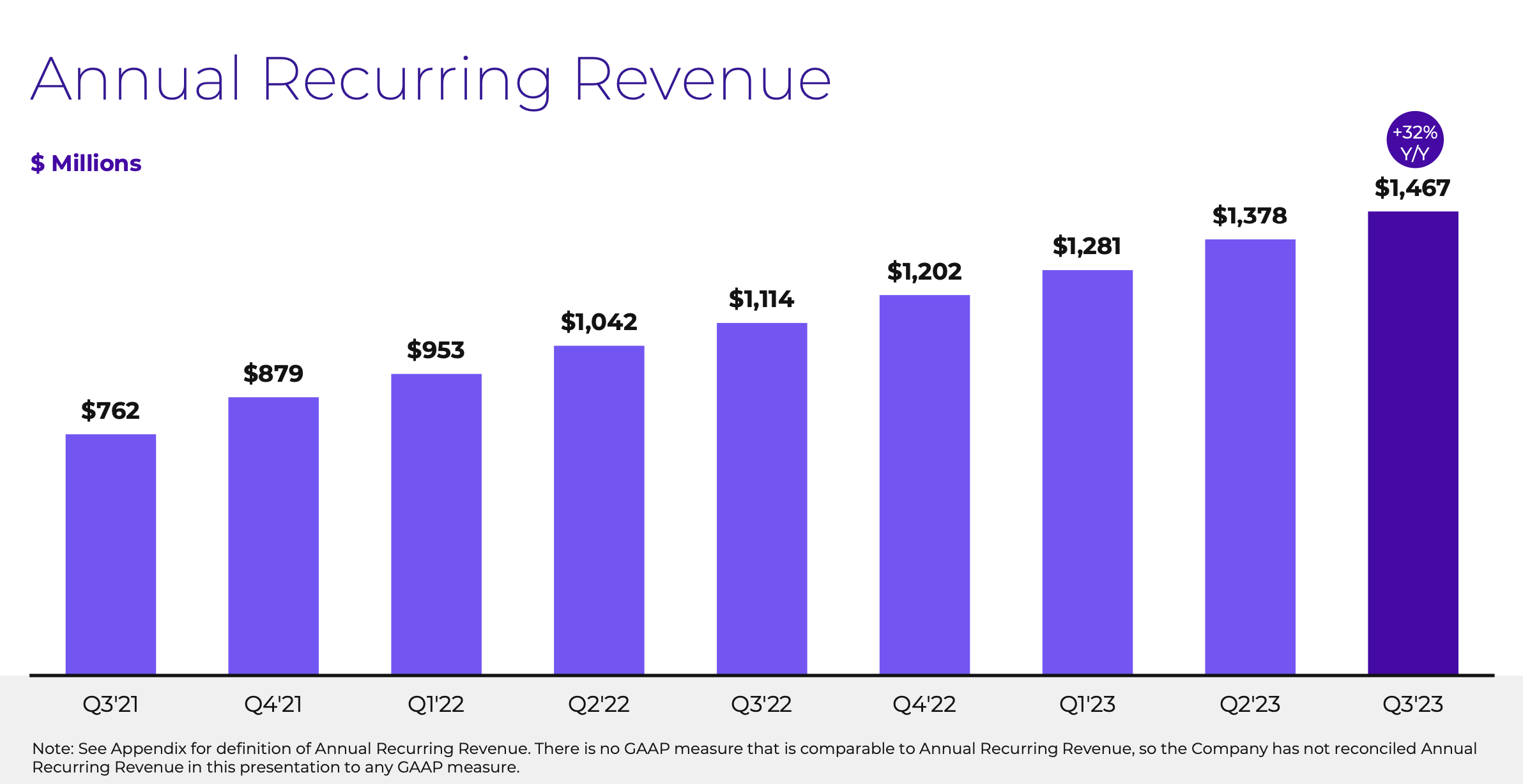

Nutanix has also continued to build up a healthy recurring revenue base: ARR grew 32% y/y to $1.47 billion in the quarter, a sequential add of $89 million:

Nutanix ARR (Nutanix Q3 earnings release)

{kind=link}

Nutanix also exceeded on profitability. Pro forma gross margins advanced 50bps y/y to 83.8% - which indexes high even against other software companies. Pro forma operating margins also nudged up 300bps y/y to 1.4%, versus -1.6% in the year-ago quarter, benefiting from the company's reductions in headcount. Free cash flow also jumped to $42.5 million, a substantial improvement versus cash burn of -$20.1 million in the year-ago quarter.

Key takeaways

There's a lot to like about Nutanix heading into the remainder of 2023: strong sales momentum in the face of a tough macro backdrop, improving margins, and a consistently growing recurring revenue base. Stay long here.

For further details see:

Nutanix: Rare Sales Momentum In A Tough Environment