NTNX - Nutanix: Rating Downgrade As Valuation Has Reached My Expectations

2023-09-04 13:30:08 ET

Summary

- I have downgraded my rating from buy to hold due to a less attractive risk/reward situation.

- The company had a strong quarter, exceeding consensus estimates with a 28% revenue growth and 86% PF gross margins.

- Partnerships with VMware and Cisco are expected to contribute to future growth, potentially exceeding guidance.

Overview

My recommendation for Nutanix ( NTNX ) is now a hold rating (downgrade from buy) as the risk/reward situation is no longer as attractive. The stock has moved in accordance with my expectations since I last wrote about it . That said, I am still positive about the business's ability to perform strongly. Note that I previously gave a buy rating to NTNX, as I expect valuation to revert back to average and NTNX to continue riding the secular trend that the industry is benefiting from.

Recent results & updates

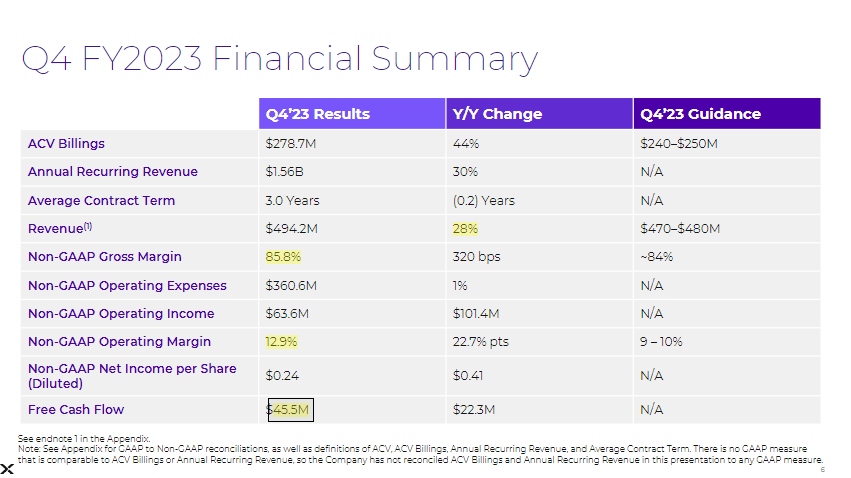

NTNX had another strong quarter, with strong performance seen across key metrics. Accelerating from 11% in the previous quarter, the 28% revenue growth exceeded consensus estimates by 400bps. The timing of hiring and other one-time cost reductions helped push pro forma gross margins up to 85.8%. The 12.9% pro forma operating margin exceeded expectations by 350bps due to the combination of a healthy top line and gross margin. Finally, free cash flow was $45.5 million, a margin of 9%.

{kind=link}

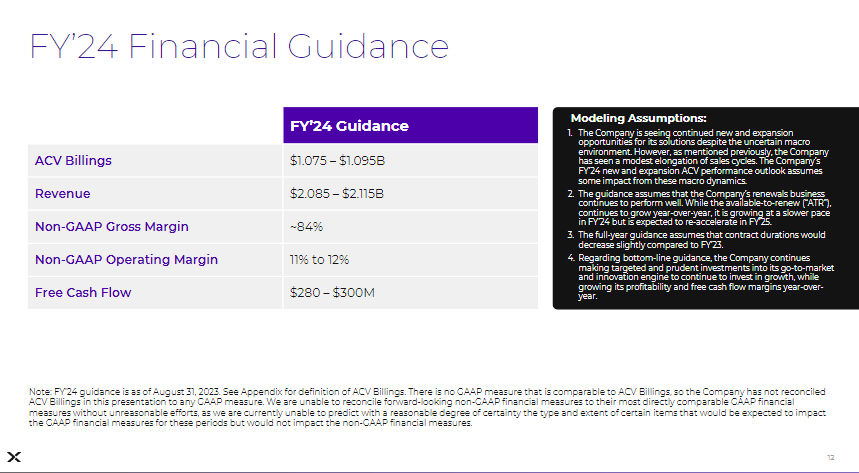

In light of management's FY24 guidance, it's clear that the impressive performance was not an anomaly. The company has projected a 13% increase in revenue and ACV billing for FY24.

{kind=link}

Note that the company anticipates a slowing in the available-to-renew ((ATR)) base in FY24, followed by a reacceleration in FY25, in terms of ACV billings, largely due to the timing of deals that may have been pulled into FY23. As a result, there could be some swings in between quarters, which I don't see as a major issue since it's just a matter of time before it's recorded. Management's projection of an 11-12% operating margin on a pro forma basis is an improvement on the 2Q23 results and a promising sign that the company's growth will be profitable.

“The guidance assumes that the Company’s renewals business continues to perform well. While the available-to-renew (“ATR”), continues to grow year-over-year, it is growing at a slower pace in FY’24 but is expected to re-accelerate in FY’25.” 3Q23 presentation slides

NTNX's growth momentum and ongoing partnerships have me confident that it will be able to hit its projections. NTNX's collaboration with VMware is bearing fruit in terms of partnership. NTNX, in particular, has recently closed a number of deals with businesses that are worried about VMware's impending acquisition and are considering switching to Nutanix as a result. In this context, it's important to note that this also includes a seven-figure agreement with a Fortune 100 firm. Since management only factored in a portion of the benefit from such deals when providing FY24 guidance, I believe NTNX may be able to exceed billing guidance. Management may be overly cautious and only factor in a minimal gain given the unpredictability of the timing of booking the deal.

We baked in any benefits from the VMware spending acquisition by Broadcom. And so, we continue to see significant engagement and opportunities related to potential concerns around that transaction. And in Q4, we did see a few of these opportunities close, including a 7-figure ACV deal with a Fortune 100 company. So, while it's difficult to predict the timing of these wins, as we've talked about before, just because of some of the dynamics in the market, we do expect some benefit from these deals influenced by this transaction and have factored that into our guidance. From 4Q2023 earnings call

NTNX's partnership with Cisco ( CSCO ) should also begin to bear fruit, in addition to VMware. Management has just revealed a worldwide strategic partnership with Cisco . As part of the agreement, Cisco will offer a unified service that combines the Nutanix Cloud Platform with its own UCS Compute, networking, and security. The Cisco salesforce will be responsible for making sales, according to management, and will receive the same compensation as they do when selling other Cisco products. I believe this partnership will help NTNX leverage Cisco's vast distribution channels. Since management is only baking in a modest amount for the second half of the year, and since they anticipate momentum to build, this is another area in which NTNX might outperform their own guidance.

Forward-looking impact on financials

Tying all the above points today, I expect to see the following impacts on NTNX financials:

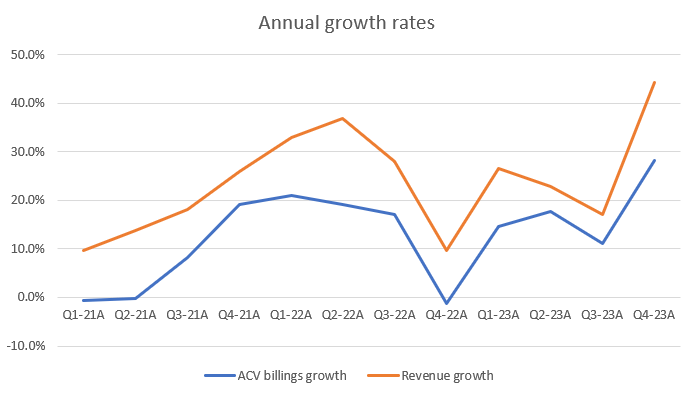

1) Revenue growth momentum should remain strong in the near-term as NTNX reported the highest annual ACV billings growth in 4Q23 (44.3%). I take this strength as indicative of the next few quarters growth, as revenue has traditionally trended in the same trajectory as ACV billings growth.

{kind=link}

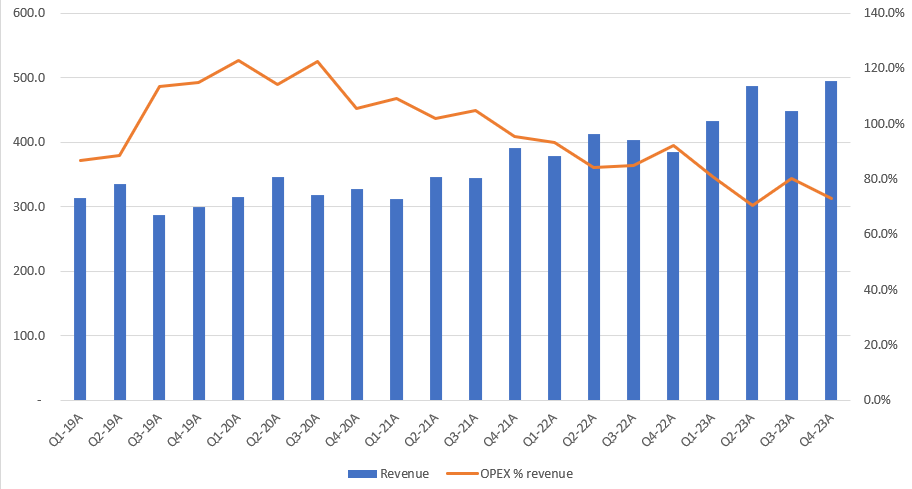

2) FCF margin should start to inflect further as NTNX starts to scale from its fixed cost base. NTNX historical performance over the past few years has clearly shown incremental margin kicking in as opex as a % of sales continue to trend down as revenue scales. With the Cisco partnership, I expect it to further reduce this percentage as the cost of distribution lowers significantly. Given the terms of the partnership, the customer acquisition cost ((CAC)) will be booked in CSCO financials, hence, lifting the financial burden on NTNX’s end. These “savings” should translate significantly to FCF margins.

{kind=link}

Valuation and risk

Author's valuation model

According to my model, NTNX is valued at $39 in FY24, a slight revision from my previous price target as I reduced my growth assumptions to reflect management guidance. Recall my previous update, where I made the forecast that NTNX is likely to see its valuation multiple grow over the next 2 years to 3.8x forward revenue, which is where the stock used to trade at on average over its trading history. This has happened just as I expected, and unlike the last time I wrote about NTNX, I do not see any strong catalyst that would particularly drive valuation upwards. In addition, the stock price has risen since I last wrote about it, further compressing the potential upside. My model now indicates a smaller upside of only 13% as the share price has increased from $27 to $35 today.

Summary

I'm revising my rating for NTNX from buy to hold as the stock has aligned with my expectations. While I maintain a positive outlook on NTNX's potential for strong performance, the risk/reward balance has become less favorable. NTNX exhibited impressive results, including a 28% revenue growth, surpassing consensus estimates. Notably, management's FY24 guidance indicates sustained growth, projecting a 13% revenue increase. The partnership with VMware and Cisco is promising, potentially exceeding guidance. However, my revised valuation of $39 for FY24, reflecting management guidance, offers a limited 13% upside, given the current share price of $35 and the stock trading at 3.8x forward revenue, as anticipated.

For further details see:

Nutanix: Rating Downgrade As Valuation Has Reached My Expectations