NTNX - Nutanix: Underlying Secular Trends Despite Macro Uncertainties

2023-07-11 03:20:20 ET

Summary

- I recommend a buy rating, with expectations of valuation reverting to average and riding the secular trend in the hyper-converged infrastructure market.

- Despite slower growth due to COVID-19, NTNX has exceeded expectations in revenue, ACV billings, and free cash flow, and is expected to become profitable in the near future.

- The company's strong fundamentals, focus on cost efficiency, and positive demand outlook position it well for future growth.

Summary

My recommendation for Nutanix ( NTNX ) is a buy rating as I expect valuation to revert to average and NTNX to continue riding the secular trend that the industry is benefiting from.

Business

NTNX offers a business cloud platform across the globe, including in North America, Europe, the Asia-Pacific, the Middle East, Latin America, and Africa. The business provides a hyperconverged infrastructure software stack that bundles together server virtualization, data storage, and network connectivity.

Industry

By consolidating data center tasks onto commodity hardware and making them available to virtual machines running on any host in the cluster, hyperconverged architecture makes it possible to scale data centers on a massive scale. With this method, virtualized workloads may be deployed quickly, data center complexity can be decreased, and operational efficiency can be boosted. Therefore, I anticipate the industry's rapid expansion to continue. Markets & Markets predicts that the size of the worldwide Hyper-Converged Infrastructure Market will increase from $7.8 billion in 2020 to $27.1 billion in 2025, a CAGR of 28.1%.

Key competitors that NTNX competes against are: Dell, Cisco systems, NetApp, VMware, Microsoft, etc.

Investment highlights

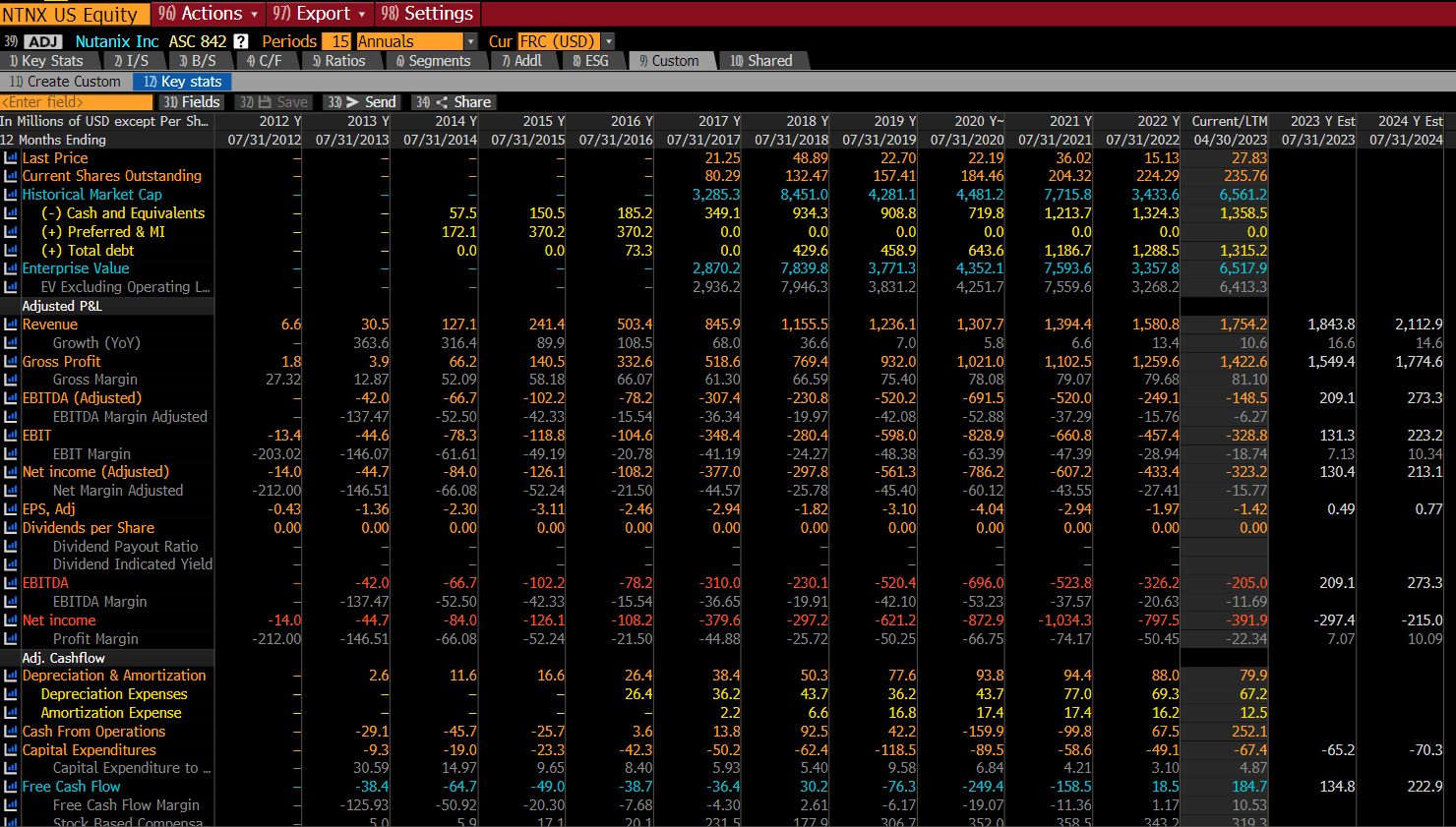

NTNX has had a successful start to the calendar year, reporting revenue, ACV billings, and free cash flow that all exceeded guidance. The company also had a remarkable FCF margin of 9.01%. NTNX's ability to achieve sustained high performance in the renewal portfolio was a major factor in supporting this expansion. This is significant because it implies that NTNX's retention rates remain high and that its base of consumers continues to see the company as the superior option. Even though management has said that new and expansion businesses have been slower than expected to start the year due to macro factors, this does not indicate demand destruction. Instead, I think this is just a pause in demand that will be made up for as the macro economy recovers.

Amidst these challenges, management remains upbeat about the demand outlook, increasing projections for FY23 in terms of revenue, ACV Billings, gross margin, and operating margin. I believe that the latter increase will eventually contribute to a higher structural FCF margin, and it is remarkable in and of itself because it demonstrates that management is keeping the ship tight by focusing on cost efficiency across the business.

At long last, NTNX declared that the audit committee probe into the shady usage of third-party evaluation software was closed. In general, I am relieved that this audit overhang has been lifted, since doing so will allow the stock price to more accurately represent the excellent fundamentals and solid FCF generation of the firm.

Financial highlights

{kind=link}

NTNX was a high flyer in this vast and developing business until it was hit by covid, which caused enterprises to postpone substantial IT implementation. This has resulted in substantially slower growth in the mid-single digits from FY19 to FY22. Given the macroeconomic uncertainty, I predict growth to remain lower than historical highs. However, I remain optimistic about the company's long-term prospects because the secular tailwind is substantial. As business confidence returns, NTNX should eventually recover to at least industry-like growth rates.

NTNX is not profitable currently, but I expect it to become highly lucrative at some point, and I believe the firm will begin being profitable in the near future (may very well be this year) as management focuses on cost savings and gross margin increases.

As NTNX is not profitable, I looked for any possible balance sheet risk. Based on the latest results, NTNX is in a net cash position with $1.35 billion in cash and $1.32 billion in debt. Hence, I believe there is certainly enough cash for NTNX to last until it breaks even.

Valuation

According to my model, NTNX is valued at $42 in FY24, representing a 54% increase. This target price is based on my growth forecast for the high teens over the next two years. The rationale for the lower-than-industry growth rate is that I believe the macro environment will remain this way in the short term, and the majority of expected growth will be backloaded when the economy improves.

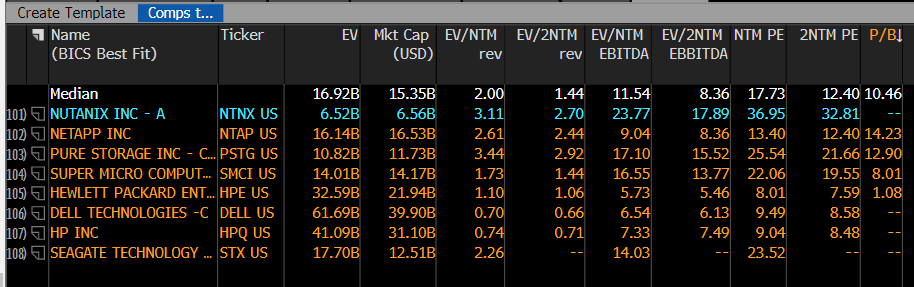

NTNX is now trading at 3x forward revenue, which I believe to rise over the next two years as the market anticipates a rebound. In FY24, I projected NTNX would trade at 3.8x forward revenue. I believe the value is appropriate because it compares favorably to peers, with NTNX selling at a premium to slower-growing peers and at a discount to faster-growing peers.

Author’s valuation model Bloomberg Bloomberg Finbox

{kind=link}

{kind=link}

{kind=link}

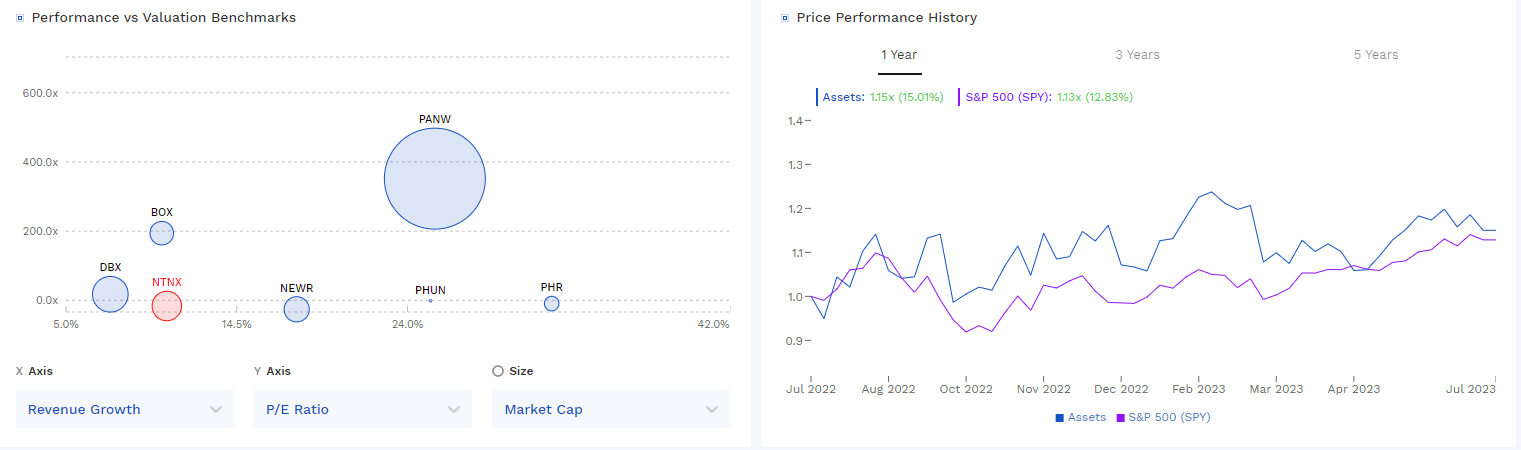

NTNX has outperformed the index by a minor margin over the past year, which I think speaks well of how the market views NTNX as an asset in the current investing climate. I believe NTNX attractive industry and growth profile will continue to support its valuation so long as growth recovers.

Risk

In order to sell its products in high-potential markets, Nutanix depends heavily on its partners to identify, vet, and cultivate relationships with distributors. The loss of these channel partner relationships will be detrimental to the business.

Competition in the software industry has typically been difficult to navigate due to the proliferation of similar features or tools offered by several providers. In order to give the industry time to standardize on a single design, customers may delay purchase decisions or postpone evaluations of new technologies. As such, NTNX always faces the risk of being left behind by technological advancement if it is not innovative enough.

Conclusion

In conclusion, NTNX is a leading provider of hyperconverged infrastructure software stack, operating globally across various regions. Despite the challenges posed by the COVID-19 pandemic, the company has shown resilience and exceeded expectations in terms of revenue, ACV billings, and free cash flow. With a positive demand outlook and increased projections for the future, NTNX is well-positioned to capitalize on the industry's rapid expansion. While macroeconomic uncertainty may temporarily impact growth, the company's strong fundamentals and focus on cost efficiency instill confidence in its long-term prospects. The recent resolution of an audit committee probe further alleviates concerns and allows the stock price to reflect the company's solid financial performance.

For further details see:

Nutanix: Underlying Secular Trends Despite Macro Uncertainties