NUVL - Nuvalent Stock Gains On Lung Cancer Data But I'd Only Buy On Dip

2023-10-05 11:00:43 ET

Summary

- Nuvalent, Inc. stock gained 36% and reached an all-time high of $58 per share yesterday, with a market cap valuation of $3.3bn.

- The biotech company is focused on developing targeted therapies for cancer patients, with its lead drug candidates showing promising results in treating lung cancer.

- Data released yesterday from candidate NVL-655 in NSCLC, showing a 65% ORR in patients with ALK+NSCLC, impressed the market.

- The market opportunity for Nuvalent's drugs in ALK/ROS1 NSCLC is significant, with a potential patient pool of ~50k and a market opportunity potentially worth up to ~$3bn.

- These are crowded markets with several approved therapies - where Pharma giants Pfizer and Roche are entrenched competitors. Nevertheless, Nuvalent's data suggests the biotech has genuien approval shots in play.

Investment Overview

The shares of Cambridge, Massachusetts biotech Nuvalent, Inc. ( NUVL ) made a 36% gain in trading yesterday, reaching an all-time high value of $58 per share, for a market cap valuation of $3.3bn.

Since its IPO was completed in July 2021, raising ~$166m via the issuance of 9.75m shares priced at $17 per share, Nuvalent stock has performed exceptionally well for investors - despite a dip to <$10 per share in mid-2022, at the height of the biotech bear market, a number of notable catalysts have helped shares to increase in value by >200%.

Nuvalent is focused on discovering "precisely targeted therapies for patients with cancer," and the design and development of "innovative small molecules that are designed with the aim to overcome the limitations of existing therapies for “clinically proven” kinase targets," according to the company's Q2 2023 10Q submission (quarterly report).

Kinase inhibition is not exactly a new approach to treating cancer - apparently , there are ~72 protein kinase inhibitors approved by the FDA, the vast majority of which are orally administered, and >60 of which are approved to treat solid tumor and hematological cancers. In a paper titled KinaseMD: kinase mutations and drug response database, shared on PubMed , the authors write:

Protein kinases ("PKs") represent one of the largest recognized protein groups that are involved in multiple biological processes. More than 30% of all human proteins can be modified by PK activities. In addition, PKs are the enzymes for the process of phosphorylation, which play critical roles in the regulation of almost all biological processes and pathways in eukaryotes. Therefore, dysfunction of PKs and their downstream substrates has been involved in various human diseases, especially in cancer.

Nuvalent Builds Momentum Through Promise Of First Lead Drug Targeting NSCLC

Nuvalent's first lead product candidate, NVL-520 is described by Nuvalent as:

a novel ROS1-selective inhibitor designed with the aim to address the clinical challenges of emergent treatment resistance, central nervous system (CNS)-related adverse events, and brain metastases that may limit the use of currently available ROS1 tyrosine kinase inhibitors (TKIs)

In October last year, Nuvalent stock spiked from ~$20, to ~$35 on positive data from a Phase 1 study of NVL-520 in patients with advanced ROS1-positive Non Small Cell Lung Cancer ("NSCLC") and other solid tumors, showing partial responses to the therapy from 10 out of 21 evaluable patients. In patients with ROS1 G2032R mutations, the objective response rate ("ORR") was 78%, and in patients with a history of CNS metastases the ORR was 73%.

Importantly, there were no dose reductions or treatment discontinuations in the study, providing encouragement for management's thesis that its drug may be more selective, with less off-target toxicity, yet just as effective as presently approved drugs with a similar mechanism of action ("MoA").

A 100mg dose has been selected for the Phase 2 portion of the study, which includes cohorts management says "have been designed to support potential registration in kinase inhibitor naïve or previously treated ROS1-positive NSCLC patients." In other words, management is hopeful the expansion cohorts could deliver data strong enough to support a push for FDA approval.

Nuvalent Stock Spikes, Then Spikes Again On Promise Of ALK Targeting NSCLC Target

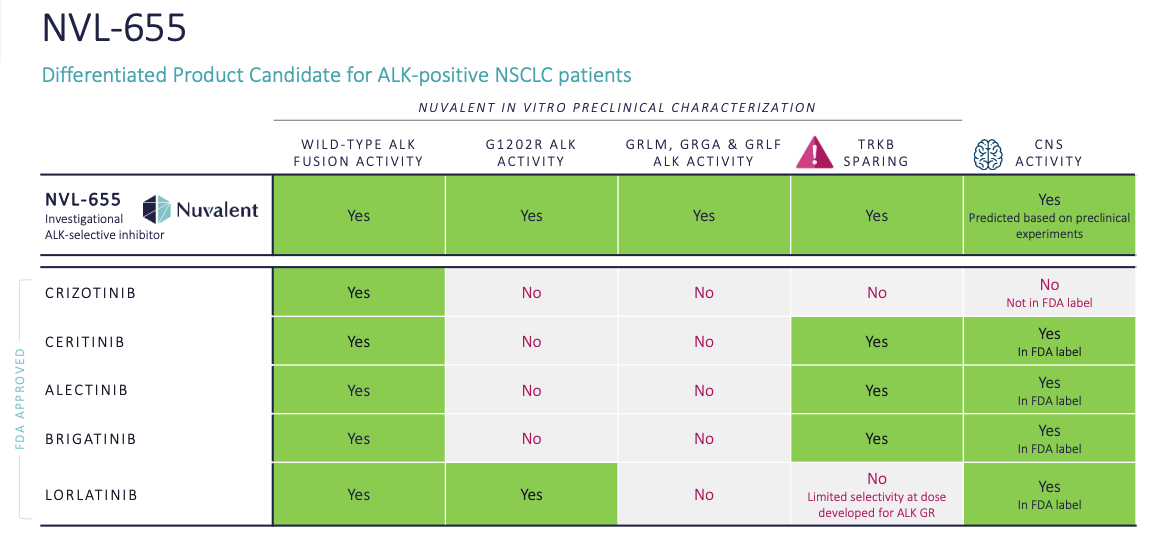

Nuvalent's second lead product candidate is NVL-655, and this drug is chiefly responsible for the company's recent share price gains, including yesterday's spike. Where NVL-520 targets the tyrosine kinase ROS1, often found mutated in cases of lung cancer or other solid tumor cancers, NVL-655 targets the ALK receptor tyrosine kinase, associated with the proliferation of cells.

Nuvalent stock, which had drifted from ~$35 to ~$25 since the positive NVL-520 data, began to pick up again after the company shared news about preclinical testing of its second candidate. In a press release from mid-April, Nuvalent discussed results from a collaboration with the Yonsei University College of Medicine, quoting Professor Byoung Chul Cho, M.D., Ph.D, of Yonsei as follows:

The potent preclinical efficacy of NVL-655 in a challenging patient-derived model of treatment-resistant intracranial ALK NSCLC was consistent with its design as a brain-penetrant ALK-selective TKI with activity against the G1202R mutation, and supportive of a differentiated preclinical profile for NVL-655 compared with approved and other investigational ALK TKIs

Like NVL-520, NVL-655 is brain penetrant, which is important given management believes that 30-40% of patients with ALK positive NSCLC present with brain metastases. This is a crowded indication, however, with 5 TKI's approved already, led by Roche’s (OTCQX: RHHBY ) Alecensa, with Pharma giant Pfizer's ( PFE ) Lorbrena (alectinib), and Xalkori (crizotinib), Japanese Pharma Takeda's Alunbrig (Brigatinib), and Novartis' ( NVS ) Zykadia (certinib) all competing for market share in the first-line treatment space.

NVL-655 versus competition in NSCLC (Nuvalent presentation)

{kind=link}

As we can see above, however, Nuvalent believes its candidate has the edge over all of these FDA approved therapies based on its superior selectivity, and wider targeting of ALK. Many biotechs make similar claims about their drugs safety and efficacy when they are still preclinical, however, but few go on to establish proof of concept and validate the preclinical data when conducting in-human studies.

Yesterday, arguably, Nuvalent did just that - albeit with an early stage data set - when revealing preliminary dose escalation data from a Phase 1 study of NVL-655 in patients with advanced ALK-positive non-small cell lung cancer (NSCLC) and other solid tumors. The data was taken from 57 evaluable patients, 54 of whom had NSCLC, with the population described as follows in a Nuvalent press release:

The patient population was heavily pre-treated and included:

- patients with baseline CNS metastases (51%);

- patients with ALK resistance mutations (47%), including compound ALK mutations (32%);

- patients who had received ?3 prior ALK TKIs (53%); and,

- patients who had received ?1 2 nd generation ALK TKI (alectinib, brigatinib, ceritinib) and the 3 rd generation ALK TKI lorlatinib (77%).

Activity observed in patients after receiving NVL-655 was broken down as follows:

Partial responses were observed in 45% (15/33; 8 pending confirmation) of response-evaluable patients with ALK-positive NSCLC who received NVL-655 at doses ranging from 15-150 mg once daily.

An ORR of 65% (11/17) was observed in patients with baseline ALK resistance mutations, and an ORR of 41% (12/29) was observed in patients post-lorlatinib, including cases with compound resistance mutations. Early indicators of CNS activity were also observed.

From a safety perspective:

NVL-655 was well-tolerated and treatment-related adverse events (TRAEs) were generally mild. The most frequent TRAEs were nausea (12%), transaminase elevation (12%), fatigue (9%), and constipation (7%). Grade ?3 TRAEs were transaminase elevation (n=2), CPK elevation (n=1), and fatigue (n=1). An MTD was not identified and Phase 1 was ongoing to determine the RP2D.

Market Opportunity In ALK / ROSL Non Small Cell Lung Cancer

The market was clearly impressed with Nuvalent's data, shared yesterday, with the stock price climbing >35% and reaching a new all-time high - but does the market opportunity in play justify the $3.3bn market cap that Nuvalent now enjoys?

According to the National Cancer Institute, Roche's Alecensa was approved for ALK-positive NSCLC was based on:

two small single-arm clinical trials of patients with ALK -positive NSCLC who were previously treated with crizotinib. In the first trial, tumor reductions were observed in 38 percent of patients, with median survival of 7.5 months. In the second trial, tumor reductions were observed in 44 percent of patients, with median survival of 11.2 months.

With its ORR of 65% in patients with baseline ALK resistance mutations, NVL-655 looks competitive, although Pfizer's Lorbrena has since upped the bar, apparently cutting the risk of tumor progression or death by 72% over Xalkori in a pivotal study, when Alecensa could only do so by ~50%, which is similar to the other approved candidates.

Crucially, however, Alecensa remains favored over Lorbrena by many physicians, earning ~$1.5bn of revenues in 2022, versus ~$450m earned by Pfizer's drug - due to its superior toxicity profile, rather than its superior efficacy profile - safety is an issue for Lorbrena, as is targeting brain metastases effectively. As such, there is potentially an opportunity for NVL-655 to establish a best-in-class safety / efficacy profile, provided later stage studies support early data, which is not always the case.

It should be noted that ALK pathology is only present in ~3-5% of all cases of NSCLC, significantly restricting the market opportunity, although with ~1.8m people globally diagnosed with lung cancer annually, that still represents a patient pool of ~72k. If approved in a first line setting in the US, if we assume a patient pool of ~30k, and a list price for an annual course of therapy of ~$100k, we could have a $3bn opportunity in play. If approved in second line only, its hard to forecast peak revenues >$500m per annum.

Turning to candidate NVL-520, ROSL-positive NSCLC is a subset of ~1-2% of all NSCLC patients, implying this drugs market opportunity is less than 50% of NVL-655, with peak sales likely to be in the region of ~$250m - $750m. Erring on the lower side of estimates, my "guesstimate" would be that peak sales from both drugs, if approved in NSCLC, would be <$750m per annum.

Assessing NUVL Stock's Valuation & Upside Possibilities

As mentioned in my intro, Nuvalent is currently a rare thing in biotech, in that it is a company trading comfortably ahead of its IPO price even after the damaging and prolonged bear market of 2022.

A market cap of >$3bn is also an unusually high valuation for a company that has scarcely entered the Phase 2 clinical study stage, and is relying on earlier stage data to establish PoC, although the NVL-655 study involved >50 patients - large enough to eliminate concerns over the data set being too limited - and Nuvalent believes that data collected in the Phase 2 portion of its NVL-520 study could be sufficient to support an approval push.

Part of what may be making Nuvalent's valuation grow, besides its success in subsets of NSCLC, is the proof of concept ("PoC") the company is establishing, which is encouraging the market to think beyond the 2 NSCLC drugs and speculate about what other markets the company could target.

Nuvalent is already working on a third candidate, NVL-330, a brain-penetrant human epidermal growth factor receptor 2 (HER2)-selective inhibitor that could target breast cancer, which, like lung, is sadly one of the largest markets in oncology. The company is also developing a next-generation ALK+ NSCLC candidate.

Nuvalent reported >$430m in cash and equivalents as of Q2 2023, reporting a net loss of $(29m) for the quarter, so there is a lengthy funding runway in place, and no significant debt to speak of.

Although Nuvalent pitches itself on the "bleeding edge" of new cancer drug development, you could argue the company made quite conservative choices with its first 2 development candidates, targeting known oncogenes like ROSL and ALK, in the knowledge that drugs with the same MoA had already secured approvals in these indications (Xalkori and Roche's Rozlytrek are approved in ROSL+ NSCLC).

Essentially the investment thesis in relation to Nuvalent at present is whether the company can bring 2 kinase inhibitors to market in NSCLC and improve upon the current standard of care in this drug class, which is currently Alecensa, Xalkori, Lorbrena and Rozyltrek.

That is going to be a tough challenge for Nuvalent, as the Big Pharma industry has far greater resources and an entrenched position in target markets that will be extremely difficult to erode, even with a best-in-class drug. In its annual report, Nuvalent additionally notes that Bristol-Myers Squibb ( BMY ), another pharma giant, has "two ROSL TKI programs in clinical trials."

Concluding Thoughts - An Intriguing Opportunity - But No Rush To Buy Following Yesterday's Gains

To summarize all of the above, Nuvalent is a company that has arguably been flying slightly under the radar since its IPO, but whose valuation is now surging after its pipeline has delivered 2 candidates with potentially best-in-class credentials in ket cancer markets, within the overall market worth as much as ~$5bn per annum.

Does that justify a surge in valuation to >$3bn? Arguably, both assets remain too early stage to support genuine hope of approval in 1-2 years' time, but balanced against that is the fairly large data set used in the NVL-655 study, and management's contention that that Phase 2 NVL-520 data could be used as part of a New Drug Application ("NDA") - perhaps even as part of a push for accelerated approval from the FDA.

As such, I think the market is right to be excited about Nuvalent - a company that relies on playing the percentages in drug development as much as it does on bold innovation, in my view. Some analysts have quoted target share prices for Nuvalent stock of ~$65, but if the company were to secure 2 approvals within the next 3 years, and make meaningful progress with its breast cancer candidate, I could see the valuation creeping >$5bn, based on a 5x peak sales valuation of $3.5bn, plus the value implied by expansion opportunities for the lead candidates, plus the promise of a breast cancer drug and a next generation ALK candidate.

I would caution investors however that with no obvious data catalysts now in play - the next data readout will be in relation to the Phase 1/2 study of NVL-520 and will arrive in 2024 - I would expect Nuvalent's share price to drift downward as the hype dies down and the buying frenzy eases. This is certainly a company biotech investors will want to keep a close eye on, however, and if the share price does drift back into a $35-$45 range - I would be tempted to open a position.

For further details see:

Nuvalent Stock Gains On Lung Cancer Data, But I'd Only Buy On Dip