PYPL - Nuvei: 2022 Earnings And Valuation Update

2023-03-16 08:51:53 ET

Summary

- Nuvei Corporation reported solid earnings for 2022 despite tough comps and upbeat guidance for 2023 despite tough macro.

- It's possible to have misgivings about the unproven management, but the business fundamentals are strong and growing.

- The valuation has increased from bargain basement to undemanding.

- Nuvei now competes with other investment ideas, rather than being a clear favorite, but remains a good pick given appropriate sizing.

Introduction:

Nuvei Corporation ( NVEI ) recently reported earnings for 2022 , and since then the stock has risen dramatically, from around $33 USD per share to $40. When I first began covering Nuvei, it traded at around $25. It’s safe to say NVEI stock has seen a large run-up. Is it still a buy? Let’s find out.

Nuvei Earnings Update

Nuvei Corporation is a payment services provider, operating a top-tier modular payments platform for e-commerce merchants, and since a recent acquisition, also branching into business-to-business payments. The payments space is very competitive, with the likes of Stripe, Block ( SQ ) and Europe-based Adyen ( ADYEY ) competing for clients, but Nuvei being much smaller needs fewer customer wins, has top-quality software, and a niche in regulated online gaming. Being relatively unknown means Nuvei’s new direct sales marketing team (led by a former Mastercard Incorporated ( MA ) exec) could have an outsized impact in the future as well. Nuvei also has significant insider-ownership, with the CEO owning 20% of outstanding shares and employees having received $100,000 of equity when it IPO’d, the company has significant operating leverage, and management projects continued growth in margins and sales into the medium term:

Growth target for revenue decreased 10% since the last earnings report (Investor Presentation)

{kind=link}

Notably, the sales growth projections decreased from 30% down to 20% since last quarter’s guidance; the stock rose nonetheless, indicating how undervalued the stock was. While this drop in guidance is disappointing, I think this it is much more realistic. In my brief coverage of Nuvei, I’ve noticed that this is a trend with Nuvei, being slightly unrealistic. They tend to jazz up their results, highlighting the positives and burying the negatives. This isn’t uncommon for companies, except for exceptional ones like Constellation Software (CSU:CA) or Berkshire-Hathaway ( BRK.B ), but it does leave me wary.

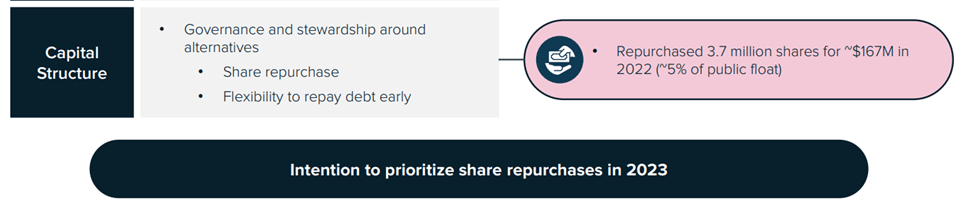

For example, the company highlights their share buybacks in the investor presentation here:

Highlighted in red is the stock buybacks (Investor Presentation)

{kind=link}

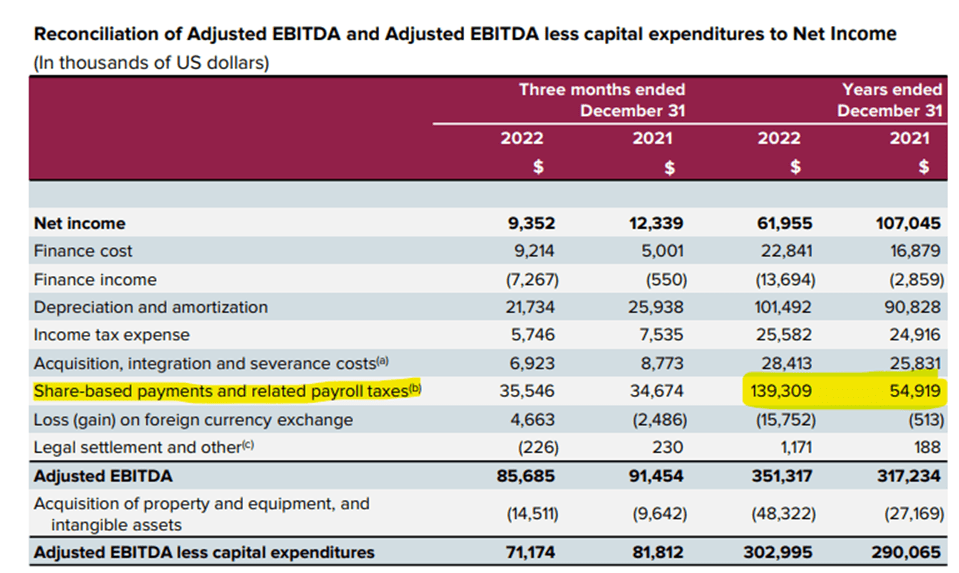

While neglecting to mention the massive increase in stock-based compensation ("SBC"):

In the appendix at the back is how much share-based compensation is used, offsetting the stock buyback (Investor Presentation)

{kind=link}

Buying back $167M in stock is great, especially because it was significantly undervalued, but if you issue $139M of undervalued options on those shares, then shareholders are not getting any benefit. Additionally, much of the compensation goes to those at the very top, who seem to be enhancing their lifestyles considerably. It also has the dual benefit (to management) of boosting cash flow and EBITDA numbers, since stock-based compensation is not counted as a cash expense. Were they to pay themselves and employees with cash rather than stock (as is the case with most companies), cash flow and EBITDA would be significantly lower. Nuvei’s reporting and compensation leaves something to be desired.

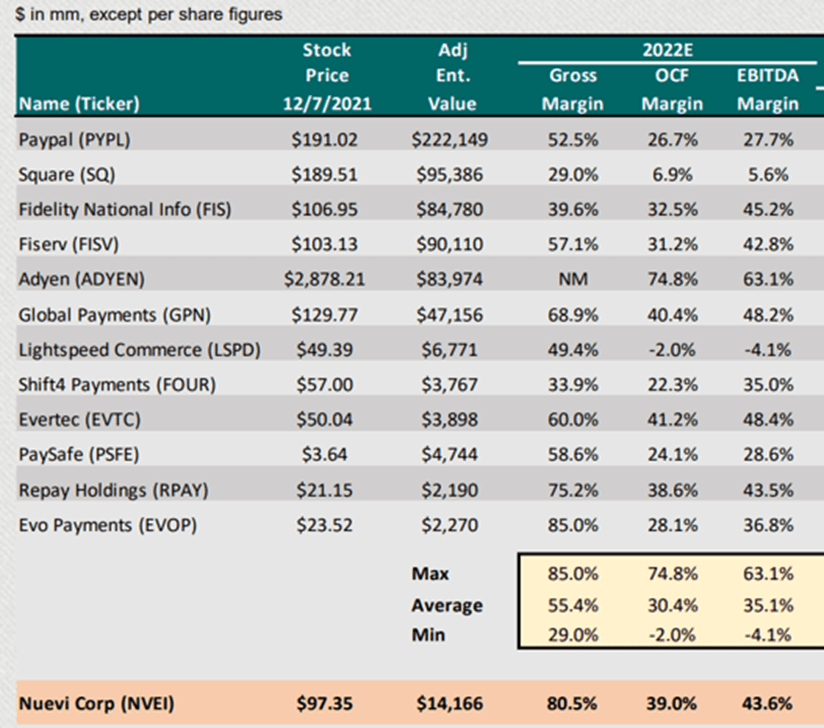

I’m not the only one who thinks this way. One of the reasons Nuvei toppled from its pandemic high was a scathing short report. The report was mostly an ad hominem attack on management’s reputation, which, to Nuvei’s credit, was refuted by the company and has not held water over time. Something that stuck out for me in that report though, was the questioning of Nuvei’s astronomical margins. They seem absurdly high, almost too-good-to-be-true high. In the short report was a very useful table comparing Nuvei to companies in its industry:

A useful chart regarding margins of payment companies (Short Report)

{kind=link}

A close look will reveal that Nuvei is about as profitable as a fintech can be and far above average. This could be concerning, but comfortingly for me, there are other companies that are similarly profitable, so Nuvei is not a clear outlier. Adyen, for example, its closest peer, has operating cash flow and EBITDA margins much higher. This chart is useful for industry comparisons as well, which I'll leave to the reader to peruse. In my opinion, the probability that Nuvei is cooking the books is low, though again, I am wary.

Guidance and Fundamentals

While I find Nuvei’s reporting slightly distasteful and its numbers so good they almost seem hard to believe, it doesn’t affect my core thesis on the company, that its niche, smaller size, top-quality software, and nascent direct sales team could propel growth in sales and margins for years to come. My lingering doubts about the unproven management team simply lead me to size the position smaller than I would if I encountered a company with fundamentals like Nuvei and a proven team leading it. It’s still worth a look because the fundamentals are incredible:

Nuvei grows everything, volume, sales, and margins. It's a hugely profitable growth stock. Ideal (Investor Presentation)

{kind=link}

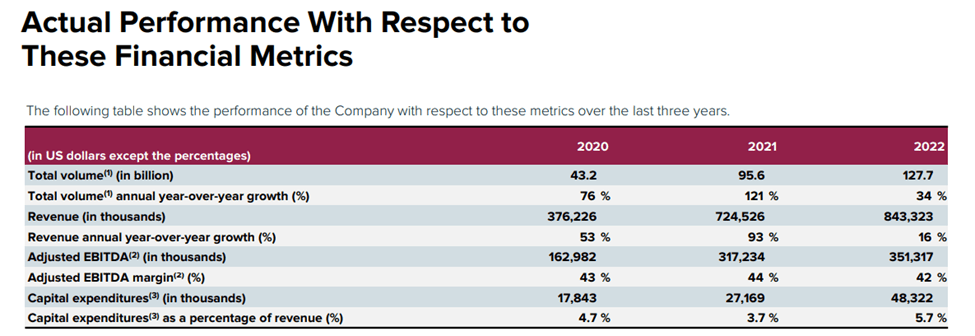

What stands out more for me is the fact Nuvei grew year over year in payment volume and revenue in 2022 despite very difficult comps. Nuvei’s had seemingly mediocre 16% sales growth in 2022 over 2021, but when we notice that sales almost doubled in the prior year we can see that the trend is up, and up quickly. The same is true with total payment volume (a measure of how much money is spent on their platform), which saw 34% growth year over year when in the prior year volume increased 121%. It’s an unbelievable feat, to grow your business by third after it more than doubled the prior year. More impressively, Nuvei did this without any net dilution, while keeping margins and capex steady. Skeptics may question management’s presentation of their company, but the fundamentals suggest the company is incredibly strong.

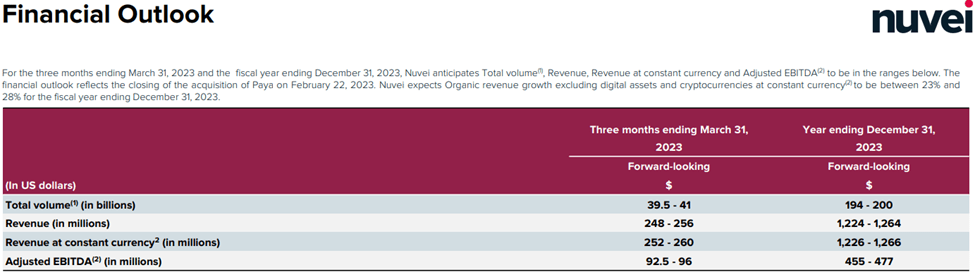

Management expects that strength to continue guiding the following into 2023:

The outlook takes into account the acquisition that closed in 2023, that's why in the fine print they mention the 28% organic growth, as they're trying to highlight that they are not an acquisition story (Investor Presentation)

{kind=link}

We need to compare this to the past to see if this represents growth and progress in the business. To better compare numbers, I put them into the following table:

Readers will note the sudden uptick in 2023 expectations. While some of this is due to the acquisition closing, much of it will be organic (Author's table)

And to help us visualize the growth, here are those numbers in graph form:

Up and to the right, this what we like to see. (Author's Graph)

It’s clear that Nuvei’s trajectory is up. I have some lingering doubts about management’s integrity, but there seems to be no question that they can grow a business. My doubts only affect position-sizing, not my view of the potential of the business and its stock.

NVEI Stock Valuation

Given the recent run-up in price, from a low of $25 USD to $40 per share, we need to see if the business is still worth buying at current prices. Below is a quick summary of Nuvei’s valuation:

Nothing demanding about the valuation of Nuvei, despite the recent run-up (Author's Calculations)

Nuvei continues to trade at very low multiples for a company growing margins and sales at the rate it is, at 15.2 times trailing free cash flow ("FCF") and 12.5 times 2023 free cash flow. These are ratios that value stocks trade at, not growth stocks. This is evident in the PEG ratio, where we divide the ratio by the growth rate; for example, a ratio of 20 for a company growing at 20% would be 1. A PEG ratio of 1 is considered fairly valued Notice that Nuvei has a PEG of 0.62 despite the recent run-up, suggesting it could have 40% farther to go on valuation alone. My discounted cash flow ("DCF") analysis (which included significant share-based compensation, Nuvei’s updated guidance, and multiple expansion to a PEG of 1), suggests something similar.

The recent run-up in the price of Nuvei’s stock appears to simply have brought it into being valued like its peers. PayPal Holdings, Inc. ( PYPL ) and Fiserv, Inc. ( FISV ), for example, trade at similar multiples of cash flow. These multiples continue to be low historically, especially for a company like Nuvei whose smaller-size, superior growth in margins and sales should demand a higher multiple.

One issue could be the stock-based compensation we discussed earlier, as some analysts will deduct it from cash, as if it were a wage, and proceed with the valuation from there, usually resulting in a lower valuation overall. Personally, I increased the annual rate in shares outstanding, as I feel that better captures the effect of stock options, because at the end of the day they don’t affect cash, they affect the outstanding shares.

We can disagree on this, though, and still find that Nuvei looks like good value, just not the total steal it was a few weeks and months ago.

Conclusion

Despite some misgivings about Nuvei Corporation management, their reporting, and their industry being very competitive, the fundamentals of the business are strong, with growing sales and margins, while the valuation has increased from bargain basement to just undemanding.

Nuvei continues to be a promising investment, but, with its increased valuation, it is now competitive with some other ideas available in the market.

I am not a buyer, as I already have a position of a size that I am comfortable with, and have some other ideas I’m pursuing. However, I would consider Nuvei Corporation at this price as it still represents good value in a growth stock.

For further details see:

Nuvei: 2022 Earnings And Valuation Update