NUW - NUW: Muni Exposure Low Leverage And Strong Distribution Coverage

2023-08-13 07:45:55 ET

Summary

- Nuveen AMT-Free Municipal Value Fund offers exposure to tax-free municipal bond distributions and has a large discount, making it a solid consideration for a portfolio.

- The fund has strong distribution coverage and has seen net investment income increase due to the higher yield environment.

- NUW's portfolio is diversified across various types of issuers and has a significant majority of investment-grade holdings.

- The fund has a policy of utilizing no more than 10% leverage, but has been running well below that and is currently at less than 1%.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Nuveen AMT-Free Municipal Value Fund ( NUW ) offers investors exposure to a basket of municipal bonds. The fund has strong distribution coverage and is benefiting from rising rates. The fund operates with no or very low leverage. As a muni fund, the fund naturally looks to target tax-free distribution for federal income tax, but in addition to that focus, the fund also targets distributions exempt from the alternative minimum tax ("AMT") as well.

The fund also sports a large discount that, combined with the overwhelmingly tax-free distributions, can make it a solid time to consider adding this fund to your portfolio. In particular, the higher the tax bracket of the investor, the higher the benefit.

We covered NUW earlier in the year , and since then, we have a new semi-annual report that shows net investment income is on the move higher, thanks to the higher yield environment.

The Basics

- 1-Year Z-score: -1.91

- Discount: -10.35%

- Distribution Yield: 3.57%

- Expense Ratio: 0.62%

- Leverage: 0.73%

- Managed Assets: $273.4 million

- Structure: Perpetual

NUW's investment objective is "current income exempt from regular income taxes, and its secondary objective is to enhance portfolio value and total return." In an attempt to achieve this, the fund will invest in:

Municipal securities that are exempt from federal income taxes, including the alternative minimum tax ((AMT)). The Fund invests at least 80% of its managed assets in municipal securities rated investment grade at the time of investment, or, if they are unrated, are judged by the manager to be of comparable quality. The Fund may invest up to 20% of its managed assets in municipal securities rated below investment quality or judged by the manager to be of comparable quality, of which up to 10% of its managed assets may be rated below B-/B3 or of comparable quality. The Fund may invest in inverse floating rate municipal securities, also known as tender option bonds. The Fund's use of tender option bonds to more efficiently implement its investment strategy may create up to 10% effective leverage.

The fund utilizes a very small amount of leverage and, in its policy, specifies that they only allow for up to 10% leverage. At this current time, they have tender option bond obligations of $2 million or what works out to 0.73%. Considering the annualized leverage cost has now come to 4.01% as of their latest month, it's clear why leverage in muni funds doesn't make a lot of sense these days.

It's not necessarily a complete negative to use leverage in a muni fund, but in that case, with rates where they are now, it is going to be for the expectation of capital appreciation. That would be instead of generating higher income than would otherwise be achievable as borrowing costs have now eclipsed muni yields unless you start getting into the high-yield muni space.

{kind=link}

Interest Rate Impact

Due to their safety, muni funds generally come with long maturities and lower relative yields. That creates a situation where the duration is long, and that means higher interest rate sensitivity. The effective maturity for NUW's portfolio comes to 16.57 years, and they have an average effective duration of 7.56 years. That means for every 1% change in interest rates, the fund's underlying portfolio should move about 7.56%.

Naturally, a rapidly rising interest rate environment caused an equally drastic move lower in terms of the fund's NAV due to bond values dropping.

Ycharts

However, the Fed is itself signaling that they are at or very near the end of this rate hiking cycle. That doesn't mean we don't stay "higher for longer" with rates between 4 and 6%, but most of the damage could or should be in at this point. In fact, should the Fed cut rates as anticipated in the next couple of years based on their own projections , that could see some relief and NAV for NUW could rise as a consequence.

FOMC Fund Rate Projections (FOMC (highlights from author))

Combining the fund's anticipation to at least level out at this point, the fund's discount also makes it a more tempting opportunity.

Ycharts

The fund has underperformed its peers quite considerably over the longer term history based on a total NAV return basis. This would primarily be because the last decade had rates mostly at levels where the yields would be enhanced due to cheap borrowing costs. Additionally, the fund, on a YTD basis, has also been delivering a lower return relative to its leveraged peers.

On the other hand, it's been one of the top performers in the last 1, 3 and 5-year periods. It's also interesting to note that over the last 6 months, so essentially excluding January's impact, the fund is also a relatively stronger performer.

NUW Total NAV Return Rank (CEFData (highlights from author))

{kind=link}

Strong Distribution Coverage

The fund's discount also helps because, similar to bonds themselves, the wider the discount, the higher the yield. Thus, as NAV dropped, the yield started rising to compensate for a higher rate environment. When the NAV started to drop, the fund's discount also started to widen out, causing a compounding impact on the fund.

That helps as long as a fund doesn't cut its distribution, which would obviously see the yield adjusted lower. Thanks to not having to deal with mounting leverage costs in the face of rising rates, this fund has been able to maintain strong coverage. In fact, coverage has been improving as net investment income has increased this year, as reflected in the semi-annual report .

NUW NII (Nuveen (highlights from author))

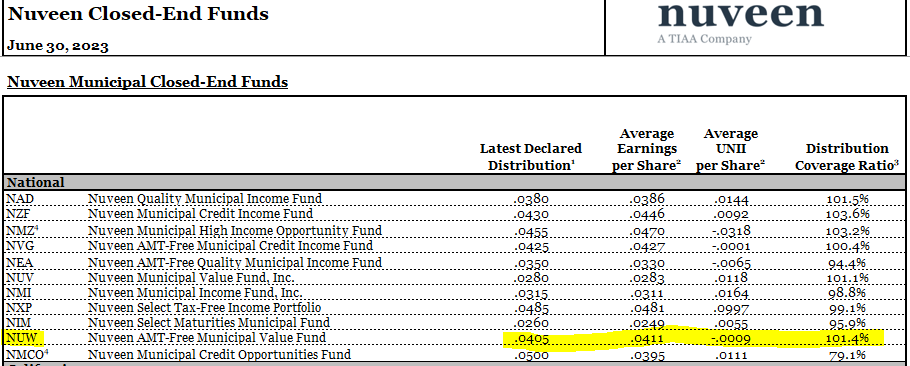

In a more recent UNII report, the fund shows that coverage of the distribution remains on track over the last three months for the period ending June 30th, 2023.

{kind=link}

Therefore, we not only have shareholders not received any cuts, but we are left in an even better relative position than other leveraged muni funds. They raised the distribution earlier this year from $0.039 to $0.0405 per month.

At a distribution rate of 3.57% and a NAV rate of 3.20%, it's not necessarily the most exciting fund to own in terms of high-yield plays. That isn't what it's for anyway; it's a relatively safer fund to invest in with very minimal leverage. Additionally, depending on your tax bracket, your taxable equivalent yield will be meaningfully higher. A 24% tax bracket would see the taxable equivalent yield come to 4.70%. Those in an even higher 37% bracket would see a taxable equivalent yield of 5.67%.

As a muni-focused fund, the fund will naturally generate lots of tax-free distribution classifications. However, it is important to note that as a closed-end fund, taxes can vary from year to year. In addition to the tax-exempt distributions, the fund has classified a small portion of the fund's distribution as ordinary income in the prior two years. In addition to that classification, 2022 tax classifications saw a fairly meaningful allocation characterized as long-term capital gains.

NUW Distribution Tax Classifications (Nuveen (highlights from author))

{kind=link}

NUW's Portfolio

The fund is largely invested in A or higher credit ratings, which suggests the portfolio is quite safe. When including BBB, as that's also an investment-grade classification, 90.32% of the portfolio is considered investment-grade.

NUW Credit Quality Breakdown (Nuveen)

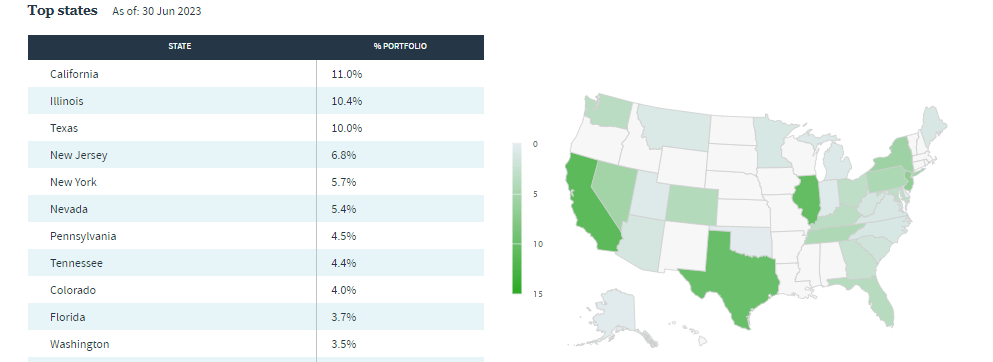

In terms of state exposure, the fund is fairly diversified. Some of the usual suspects populate near the top of the list, including California, Illinois, Texas, New Jersey and New York. Given the diverse allocation of the fund, it's very likely that for investors, at least some of the distribution will also be qualified as tax-exempt on the state level.

{kind=link}

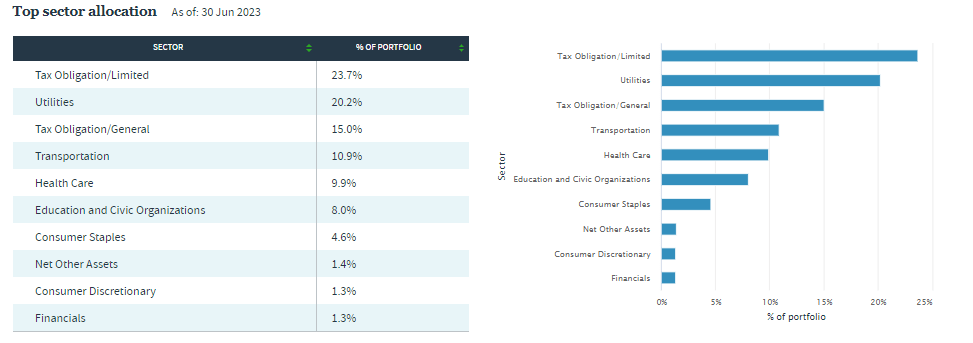

Instead of just being diversified within states, the actual sector allocation of the portfolio is also diversified. Thus, this portfolio is really going to give you a bit of exposure to a wide-ranging basket of various types of issuers.

{kind=link}

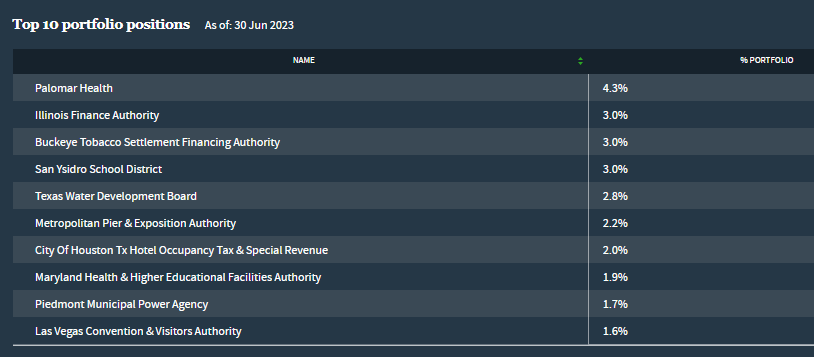

The fund is spread across 359 holdings as of the last update. However, several of the largest positions in the und do represent a fairly significant overall weighting at around 25.5%. The top five on their own represent just over 16% of the fund's exposure.

{kind=link}

Palomar Health is a relatively large position on its own. This is an AA-rated general obligation ("GO," meaning that a state or local government backs it) bond. It was issued with a 7% coupon. Given the higher yield but still high quality, this appears to be a rather attractive position.

{kind=link}

However, this is also reflected by the fact that the principal amount was $10.2 million as of their last semi-annual report, but the value is sitting at $11.85 million. That means depending on their cost of buying; they didn't necessarily buy it when it was at a 7% yield. Additionally, should the position be called or come to maturity, it will mean a loss from the current level. Fortunately, it doesn't become callable until 2029, and maturity would be in 2038.

Conclusion

NUW is the muni fund I've been accumulating due to its attractive discount and higher-quality portfolio. It's not the most exciting yield play. That said, being fully covered with the likelihood of the fund continuing to pay out the same rate due to strong coverage leads me to believe it's an interesting play in the tax-free space. If interest rates need to increase because inflation flares back up, we'd see NUW get hammered again. However, given what information we know now and the trajectory of inflation, it would appear that rates won't be going too much higher. In fact, if rates are cut as anticipated by the FOMC, then we could even see a bit of a boost in the value for NUW on a NAV basis.

For further details see:

NUW: Muni Exposure, Low Leverage, And Strong Distribution Coverage