NVG - NVG: 3 Reasons To Be Cautious Despite Large Discount To NAV

2023-12-28 10:33:43 ET

Summary

- The Nuveen AMT-Free Municipal Credit Income Fund is a popular CEF with over $4 billion in managed assets.

- NVG trades at a significant discount to NAV, but there are several negative factors that make it unattractive compared to other similar products.

- Negatives include a high expense ratio, weak historical risk-adjusted returns, and a high cost of leverage relative to underlying asset yield.

- I am initiating NVG with a hold and would consider downgrading the fund to sell if the discount to NAV narrows from here.

The Nuveen AMT-Free Municipal Credit Income Fund ( NVG ) is a popular fund among investors.

NVG is an actively managed fund which seeks to provide income which is exempt from federal income tax, including the AMT. The fund uses leverage and may invest up to 55% of managed assets in securities rated BBB/Baa or below at the time of investment. Currently, none of income produced by the fund is subject to the AMT.

The fund launched in March 2002 and currently has more than $4 billion in total managed assets.

NVG enjoys strong ratings from the Seeking Alpha community and has not received a hold or sell rating since February 2019.

A big part of the bull thesis on NVG is centered upon the significant discount to NAV. Currently, NVG trades at a 14.4% discount to NAV, vs an average discount of 8.1% over the past 10 years. While this discount is indeed attractive, I believe there are three other negative factors which make NVG unattractive at current levels vs other comparable products:

1. High expense ratio

2. Weak historical relative risk adjusted returns

3. High cost of leverage relative to underlying asset yield

Thus, I am standing against the crowd and initiating NVG with a hold rating.

Seeking Alpha

1. High Expense Ratio

NVG charges a management fee of 1.02% and has other expense of 0.05%. Thus, the total expense ratio of the fund excluding interest expense is 1.07%. Comparably, investors have access to lower fee high quality active AMT-free municipal bond products such as the Franklin Dynamic Municipal Bond ETF ( FLMI ) which is actively managed and charges a net expense ratio of 0.30% or the Invesco National AMT-Free Municipal Bond ETF ( PZA ) which charges a net expense ratio of 0.28%.

NVG's fee is high compared to the average bond mutual fund fee of 0.37% and average actively managed municipal-bond fund fee of 0.65%. Moreover, NVG's total expense ratio is ~24% of its NAV distribution rate of 4.37%. I find NVG's fee particularly challenging to overcome, given the relative high quality nature of the underlying assets NVG invests in. NVG is focused primarily on investment grade rated municipal bonds. Historically, this asset class has experienced a default rate of 0.09% on average. For this reason, I believe it is difficult for active management to add value in this asset class, as avoiding defaults is not a major source of potential alpha.

2. Weak historical relative risk adjusted returns

While NVG has outperformed low fee AMT-Free Muni products as PZA, it has failed to do so on a risk adjusted basis. Over the past 10 years, NVG has delivered a total return of 61.5% compared to a total return of 42.3% delivered by PZA. During the same time period, NVG has experienced an average 30-day volatility of 9.7% while PZA has experienced an average 30-day volatility of just 4.3%.

In terms of share ratios, over the past 10 years NVG and PZA have realized average 3 year trailing sharpe ratios of 0.52 and 0.44 respectively. Thus, NVG has performed worse on a risk adjusted basis.

This historical data suggests that NVG investors have not been compensated enough for risks related to leverage and the CEF structure, which creates additional volatility related to the level of discount vs NAV.

3. High Cost of Leverage Relative to Underlying Asset Yield

As of November 30, 2023 NVG's annualized leverage cost was 4.49%. Comparably, the fund's NAV distribution rate is 4.37% and the fund's average coupon (excluding zero coupon bonds) is 4.88%. These numbers are striking and showcase the challenges related to using leverage to buy securities with very little credit spread.

NVG currently has an effective leverage ratio of 40.85%. Thus, even though the fund is highly levered, it is not result in higher distributions as the underlying asset yield is very close to the cost of leverage. NVG's fees also serve as a headwind which make it challenging for the fund to generate additional yield based on the small difference between the underlying asset yield and cost of leverage.

Comparably, FLMI, a unlevered low fee product with similar credit quality, has a distribution rate of 4.32%. PZA, a low fee unlevered product with better credit quality than NVG, is characterized by a portfolio with an average yield to maturity of 4.36%.

An inverted yield curve has made it difficult for CEF's in general to generate additional yield through the use of leverage in the current environment. This challenge is especially true for CEF's such as NVG that invest in underlying assets which carry relatively small credit spreads. Moreover, I also believe leverage is particularly challenging in the municipal space, as underlying yields tends to be lower than similarly rated corporate bonds due to the tax advantage.

The current leverage cost relative to underlying asset yield dynamic is extremely challenging. Based on this, I view the fund's current level of leverage as adding a lot of additional risk while not adding much in the way of additional income for fundholders.

Holdings Overview

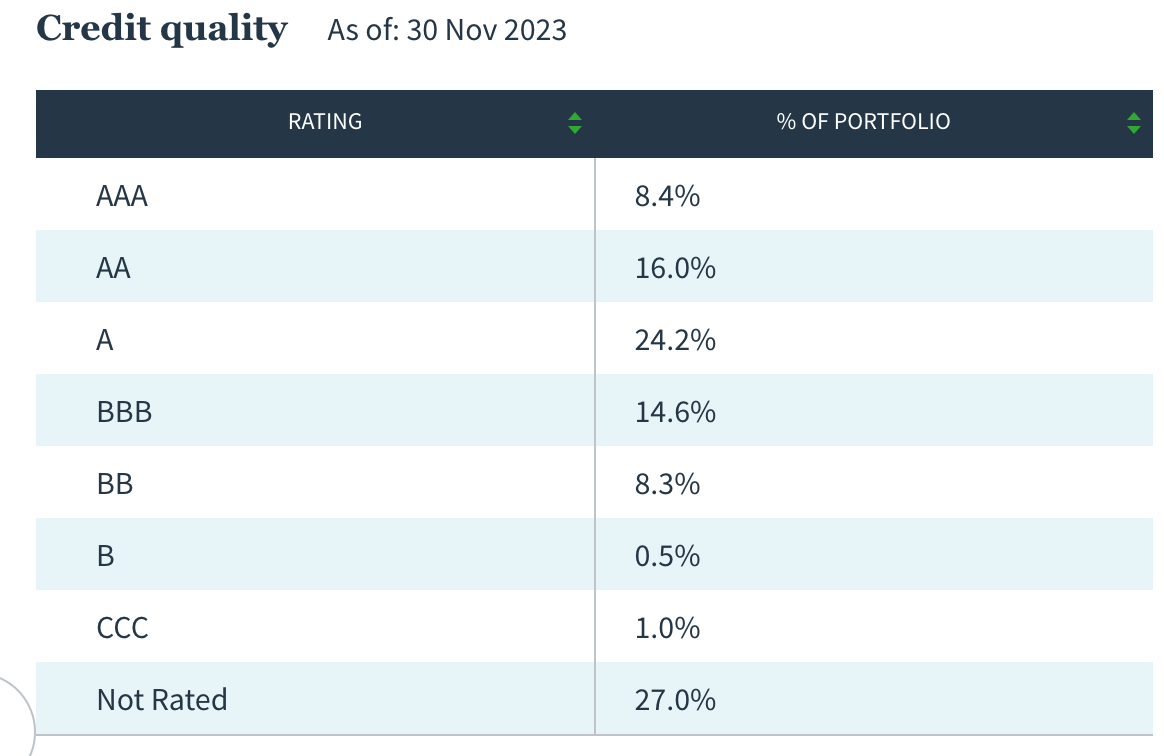

NVG's portfolio is fairly high quality in nature, with 48.6% of holdings rated A or better and 14.6% of holdings rated BBB. However, it should be noted that NVG's credit quality is worse than the aforementioned PZA. PZA has 82% of holdings rated A or better. Thus, while NVG's credit quality is strong, I view it as moderately more risky compared to index funds such as PZA.

NVG has a total leverage-adjusted effective duration of 15.3 years and thus is highly exposed to interest rate moves.

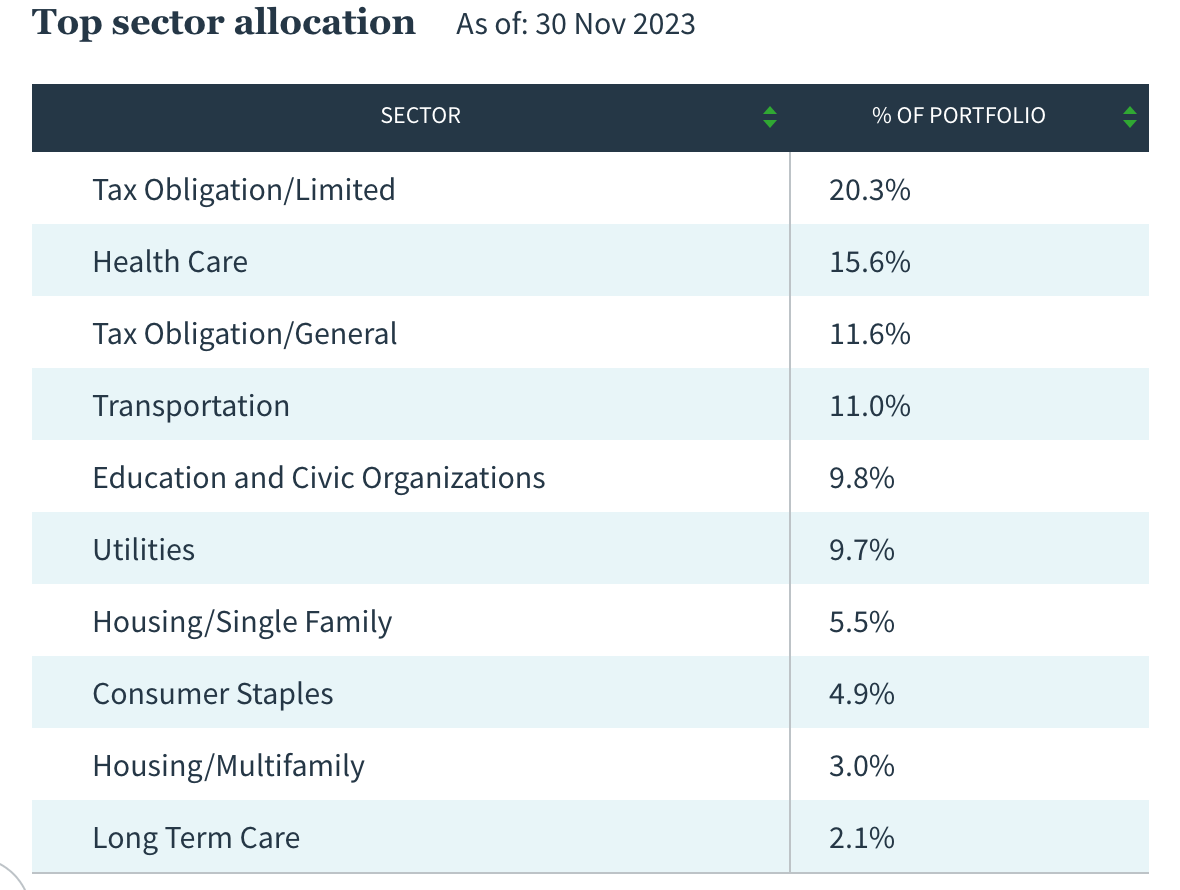

NVG is well diversified in regards to sector allocation, with no single sector accounting for more than 20.3% of total exposure.

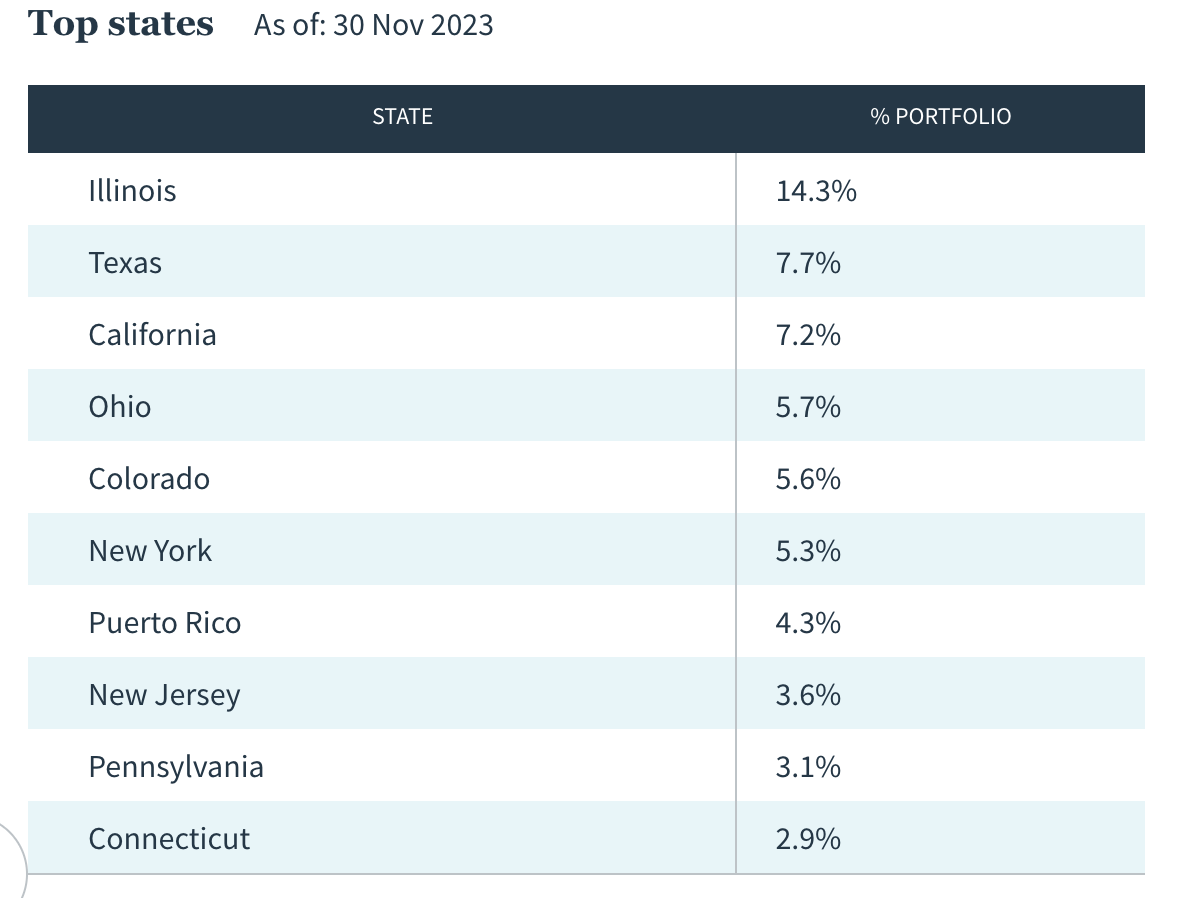

In regards to state exposure, NVG is less well diversified. The fund's 14.3% exposure to Illinois stands out relative to its weighting in passive index based products. For example, Illinois represents just 4.71% of PZA's portfolio. On the other hand, NVG is underweight New York, which accounts for 23% of PZA's holdings but represents just 5.3% of NVG's holdings.

Illinois has traditionally been one of the lowest rated states in terms of municipal finance. However, the state has been upgraded to "A" by all three ratings agencies after Fitch upgraded Illinois to A in November 2023. However, I believe Illinois remains a relatively risky municipal credit given historical challenges and high unfunded pension liabilities.

{kind=link}

{kind=link}

{kind=link}

What It Would Take For Me To Turn Bullish

One development which would lead me to become bullish on NVG over the short-term is if the discount to NAV were to substantially widen from here. As shown by the chart below, the widest discount to NAV that NVG has ever traded at was 35.2% during the 2008-2009 financial crisis. If the discount to NAV for NVG were to ever exceed 25% I believe the CEF would become attractive at least on a short-term basis.

In order for me to turn bullish on NVG for a long-term trade, I would need to see substantial improvement in terms of the difference between the fund's leverage cost and the underlying asset yield. Moreover, I would also like to see the fund reduce its expense ratio to be more inline with other actively managed municipal products.

What It Would Take For Me To Turn Bearish

If NVG's discount to NAV were too narrow modestly to less than 9%, I would consider downgrading the fund to a sell as I would view low fee products as clearly more attractive. Moreover, I would also turn bearish if the difference between the fund's cost of leverage and underlying asset yield were to materially worsen from current levels.

Another factor that would cause me to become more bearish on NVG is if the municipal credit picture in Illinois were to worsen substantially. Currently, Illinois represents NVG's largest exposure to a single state at 14.3% of the portfolio. While I do not anticipate this occurring in the near-term given recent positive fiscal actions included a balanced budget, municipal finance is often subject to political risk which can be difficult to predict.

Conclusion

NVG is currently trading at a substantial discount to NAV. While there is potential for this discount to narrow, other negative factors make this CEF less attractive.

NVG's high level of fees, weak relative historical risk adjusted returns, and low spread between cost of leverage and underlying assets are all substantial negatives.

I am initiating NVG with a hold rating, and would consider upgrading the fund if the discount to NAV were to widen considerably from here. I would also consider upgrading the fund if the spread between NVG's cost of leverage and the yield of its underlying investment portfolio were to widen substantially from current levels.

I would consider downgrading the fund to sell if the discount to NAV narrows moderately from current levels or Illinois begins to experience significant credit challenges.

For further details see:

NVG: 3 Reasons To Be Cautious Despite Large Discount To NAV