NVR - NVR: A Deep Dive Into This Phenomenal Homebuilder

2023-11-23 09:04:11 ET

Summary

- NVR is the largest homebuilder on the US East Coast and has consistently generated profit every year since 1993.

- The company has outperformed its peers with a compounded annual growth rate of over 30% and is built to thrive in downturns.

- Studying NVR will provide insights into market leaders in adjacent markets and help understand the opportunities and challenges in the homebuilding industry.

- NVR scores 12/20 in my Sleep Well Investment scorecard and is fairly valued, but in the case of a housing downturn, I won't hesitate to start a position.

I am excited to dive into NVR, Inc . ( NVR ) - the largest homebuilder on the US East Coast and the fourth largest nationally, with a $20B market cap.

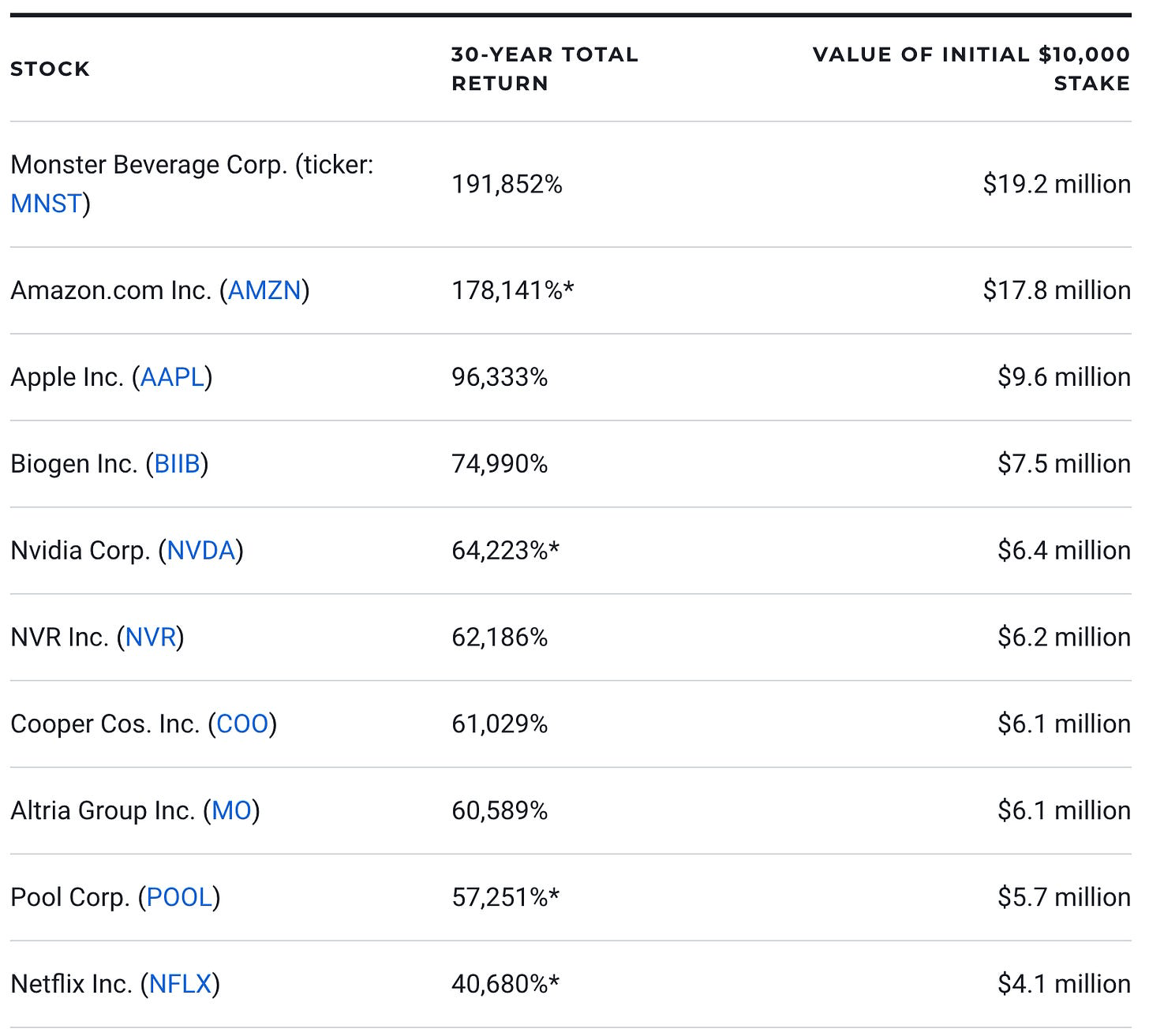

It fits the Sleep Well Investments mold with anti-fragile attributes that have generated profit every year since 1993 - no peers have managed this - and is built to thrive in downturns - no peers can say this . The market rewarded NVR stock with a compounded 30%+ CAGR return since - the best in the industry and the 6th best-performing stock in the US in the past 30 years.

{kind=link}

NVR is fairly valued; why study NVR now?

NVR is a phenomenal business. The write-up aims to equip you with a deep understanding and a tracking system - four leading indicators of the business and the capital allocation actions of the management - so that you recognize the opportunities when you see them. When you study the best, you get better at eliminating average ideas! Only a handful of companies are worth your time, let alone owning a piece .

Secondly, we will likely approach a challenging homebuilding period in the US. Affordability has been at its lowest for 20 years, and from peak to peak (2006-2022), housing starts have barely grown. NVR’s stock could be hit if sentiment gets worse.

Studying NVR will also help us understand market leaders in adjacent markets:

-

Ferguson ( FERG ) in plumbing,

-

SiteOne ( SITE ) in landscaping,

-

Watsco ( WSO ) in air-conditioning,

-

Sherwin-Williams ( SHW ) in paints,

-

Pool Corp. ( POOL ) in swimming pools,

-

Home Depot ( HD ) and Floor & Decor ( FND ) in home improvements,

-

SolarEdge ( SEDG ), First Solar ( FSLR ), and Enphase ( ENPH ) - solar energy platforms and components, and many more.

Corporate logo - Sleep Well Investments

NVR goes into my special jar. Robert G. Kirby , then a portfolio manager at Capital Group in 1984 , would put this business in his Coffee Can Portfolio , and Nobert Lou certainly did well with NVR in his Punch Card portfolio , buying in 1997 at $30 and selling in 2007 at $700/share. Had he held, even at the top, NVR would continue to 10x since then. That’s not to say the party is over; there are still at least a few decades of strong performance. We’ll see why!

First, a homebuilder’s life expectancy is about one cycle. NVR was atypical. Founded in 1980 with a traditional home-building model, it loaded up debts and bought lands as the market rose, but as the economy deteriorated in 1989, it struggled to pay off its debts while the land was losing value. Shortly, it filed for bankruptcy in 1992.

Because most homebuilders are land speculators and the business requires a lot of upfront capital , the story usually ends when the music stops (recession).

But believe it or not, since NVR’s emergence from its bankruptcy in 1993, it transformed the business, sworn off land speculation, and focused on profitability . Its story is rewritten.

It is the only homebuilder that has avoided losses in the last 30 years . Even during the 2007-12 subprime crisis, its return on invested capital was the same as that of some peers in the peak period (!). Moreover, peers have known NVR’s blueprints for three decades, yet no one has replicated it successfully.

NVR must be the black sheep like the one below!

Black Sheep - Sleep Well Investments (SA)

{kind=link}

Looking closer into NVR’s playbook, one finds a disciplined execution of a land-light, regional-focused, and profit-first strategy. On top of that, management’s capital allocation has been exemplary ; they bought back 60% of shares since the last peak in 2006 and compounded free cash flow ((FCF)) per share by 12% CAGR whilst housing starts barely improved and input costs (labor and construction materials) increased for everyone.

I can’t find a better business that will benefit in a downturn, given that most homebuilders still operate the traditional business model - capital-intensive and leveraged - which makes it even more worthwhile to study NVR. When (not IF) the next housing crisis hits, NVR will stand as the primary beneficiary again.

You can expect a thorough analysis into:

-

Why is NVR a sleep-well business?

-

Disciplined asset-light business building the American Dream

-

Maximise market share at the regional level

-

Irreplicable invisible moat

-

Value creation

-

-

Breaking down future growth and tracking system.

-

Demand: affordability, millennials, population growth from WWII

-

Supply: housing stock shortage, vacancy rate, new build

-

Average house price movements

-

What to track to get ahead

-

Growth opportunities

-

-

Operation risks

-

What’s a good entry price?

-

Base case

-

Bear case

-

-

Sleep Well Investments scorecard

-

Thesis Tracking

-

Leading indicators

-

Buying signals

-

Why is NVR a sleep-well business?

This section will show the ingredients contributing to NVR’s longevity, overcoming a hyper-competitive and speculative market.

Sleep Well Investments

NVR is a simple business in a land full of speculators

First, what are the typical homebuilders ( the white sheep) who make the same mistake?

They buy raw land outright - or undeveloped lands (in the UK - we call it greenfield lands) that require building new infrastructure from scratch, such as zoning, hazard removals, and utility hookups - and then finally build and sell homes on those lots. The process can take years and a lot of initial capital, from land acquisition to the sale of the completed product/homes.

Thus, the cash conversion cycle (‘CCC’) from day 1 to completion of a house sale can be anywhere between 300-950 days (Toll Brothers’s CCC was at 419 days in 2022 and peaked at 963 days between 2008-2012; D.R. Horton was at 303 days in 2022 and peaked at 401 days in 2010), primarily from holding inventory in the balance sheet.

Homebuilders’ CCC and Inventories FY2022 (Sleep Well Investments)

That’s the norm and is part of the problem of why they struggle in a downturn.

The biggest problem is they bought and developed these lands from borrowed money. That makes most homebuilders land speculators .

That works great in good times. The underlying land increases in value during this multiyear process, and the homebuilders generate abnormal profits when the homes are sold. When fuelled by leverage, the profits and rate of return can be too good to refuse, as Norbert Lou noted in his early work on NVR.

“They just couldn’t help themselves.”

However, when the homebuilding cycle inevitably turned down, the demand for homes dried up, land prices fell, and all leveraged builders were caught with heavy debt-service obligations on value-depreciating lands; their profits and inventory on their balance sheets evaporated. In short, the land speculation element of the homebuilding industry was the cause of serial bankruptcies.

And that was precisely what happened to NVR in the early 1990s. When the housing market collapsed, NVR and others saw revenue plummeting 50% for several years, losses incurred on lands that were sitting idle, and debts that were rising in cost. Eventually, they went bust and had to start over again.

In 1993, NVR reemerged from Chapter 11 protection just three years earlier. By 1997, investors were aware of this pattern of boom and bust, and it had accorded the industry, NVR included, a low multiple, between five to nine times earnings.

However, the market failed to recognize that NVR had changed.

Dwight Schar (founder and CEO from 1980 until 2005) had a different playbook this time.

NVR exited the speculative land development businesses, exited unprofitable regions, and eliminated inefficient manufacturing processes . Dwight Schar turned NVR into an asset-light business focused only on the East Coast.

It had turned NVR into the most profitable homebuilder with the best balance sheet to capitalize on when a recession comes. NVR’s two-pronged business model is an open secret that, till now, no peers have been able to replicate.

a. Land-light business

How did Dwight Schar do it?

NVR uses option agreements to acquire land and outsource most of the construction work to contractors. Let me explain.

First on land acquisition.

NVR doesn’t buy undeveloped lands. It typically acquires finished building lots from various third-party land developers under fixed-price finished lot purchase agreements (LPAs) that require a deposit ranging up to 10% of the aggregate purchase price of the finished lots.

NVR’s lot acquisition strategy allows them to:

-

upfronting just 10% of the land cost

-

minimize the risk associated with direct land ownership and land development.

So, the initial cost is just 10% of other homebuilders, freeing up capital in the balance sheet. More importantly, they only lose this 10% if they cannot develop or sell the homes at an acceptable profit margin and sales pace. Effectively, they do not have any financial guarantees, completion obligations, or any specific performance basis under these LPAs, and the maximum loss is the 10% deposit.

In the good times, they pay a premium on lands compared to other builders, but in bad times, they carry minimal inventory and don’t incur maintenance expenses and losses when they sit unsold and depreciate. As they don’t carry substantial debts like others (they don't need to when they don’t need as much capital to acquire land), they don’t need to sell the land at a steep discount to service their debt.

The second part of making NVR asset-light is the building and sales process.

NVR operates as a general contractor. It outsources most of its building work to independent subcontractors under fixed-price contracts. This allows NVR to hold limited ‘work-in-progress’ and building material inventories.

To sell, NVR builds model homes to showcase the finished version, and the garages of these homes are converted into temporary sales centers with sales staff mainly compensated on commission. These model homes are also rented out or sold not to keep any capital on the balance sheet longer than needed.

In summary, NVR has streamlined its homebuilding process from Day 1. It’s a carefully thought-out process to minimize capital requirements and risks of ownership and development . This results in the shortest cash conversion cycle at 80 days vs. 300+ average, lowest inventory holding, and best-capitalized cash balance sheet. This is still true today.

Sleep Well Investments

NVR has an incredible patient approach during upcycles and has another gear to be aggressive and adaptable during downcycles. The disciplined execution minimized risks and refrained from land speculation activities, enabling NVR to lead the US East Coast market while maintaining high returns on invested capital and profitability across a cycle.

a. Top market share in the US East Coast

Let’s review NVR’s product, market, and land bank before we go into NVR’s market position.

Products

NVR offers single-family detached homes, townhomes, and condominium buildings under three brands: Ryan Homes, NVHomes, and Heartland Homes. These homes generally include two to four bedrooms and range from approximately 1,000 to 10,000 finished square feet. In 2022, the prices of settled homes ranged from approximately $160,000 to $2.6 million, averaging $454,300.

NVR

It also offers mortgage and title services under NVRM. NVRM originates mortgage loans almost exclusively for its homebuyers from numerous underwriters, including Fannie Mae and Freddie Mac, and thus bears little concentration risk. NVRM generates revenues primarily from origination fees, gains on sales of loans, and title fees. True to its asset-light philosophy, NVRM sells all mortgage loans into the secondary markets within 30 days after closing.

Sleep Well Investments NVR 10-K

Markets

NVR’s four reportable homebuilding segments operate in the following geographic regions:

-

Mid-Atlantic: Maryland, Virginia, West Virginia, Delaware, and Washington, D.C.

-

North East: New Jersey and Eastern Pennsylvania

-

Mid-East: New York, Ohio, Western Pennsylvania, Indiana and Illinois

-

South East: North Carolina, South Carolina, Tennessee, Florida and Georgia

NVR 10-K

Mid-Atlantic and South East are the largest and most profitable segments.

NVR 10-K NVR 10-K

Developed and underdeveloped lots

NVR aims to maintain control over a supply of lots to meet its five-year business plan.

In 2022, NVR controlled approximately 131,900 lots , of which 125,100 were under LPAs with third parties through deposits totaling approximately $550M ($57M is recorded as impairment reserve). NVR also controls 5,300 lots totaling approx. $27.2M through five Joint Venture Limited Liability Corporations.

NVR 10-K NVR 10-K

In addition, NVR also controls 19,300 lots of undeveloped lands that require rezoning or other approvals to achieve the expected yield. These properties are controlled with cash deposits totaling approximately $10.1M, of which approximately $2.5M is refundable if NVR does not perform under the contract.

Competition

NVR competes with thousands of homebuilders as well as the home resale market.

Since homes are commodities, homebuilders often find it tough to differentiate themselves. Thus, they compete primarily on price and location and partially on design, quality, service, and reputation.

The home building industry in the US remains fragmented, but like many industries in the country, it has slowly concentrated, with a handful of large companies achieving economies of scale. As they become more efficient, have more resources to acquire, and drive smaller builders out of the market. In the 1990s, the top 10 builders only commanded 5-10% of the market in completions. Today, the top 10 commands 27% of the market, as seen in the chart below.

Sleep Well Investments

D.R. Horton ( DHI ) and Lennar ( LEN ) are the clear leaders in scale, with 13% and 11% of the total market, respectively, and NVR is in the fourth spot with 3.5%.

Builder magazine

NVR is the top in Washington-Arlington-Alexandria with a 27% market share. The top 5 control 57% of the market.

Builder Magazine

D.R. Horton is top with 19.5% in Dallas-Fort Worth-Arlington. The top 5 controls 42% of the market.

Builder magazine

It’s a similar picture in other markets . Below is the market share of the top 10 builders in different regions. They own 90% of the market share in Las Vegas, with Lennar at the top with 17% .

Builder magazine

However, it’s important to note that scale within local markets is more important to NVR and is reflected in a more simplified and regional building process.

First, NVR has fewer house models , resulting in fewer moving parts, making it easy to standardize production, keep track, maintain quality, and has shorter build time.

Second, NVR has eight pre-fab manufacturing facilities in Maryland, Pennsylvania, New York, New Jersey, North Carolina, Ohio, Virginia, and Tennessee. They reduce waste and improve efficiency because structural building components, such as external walls, internal walls, panels, stairs, etc., are produced to exacting standards in a controlled environment before being delivered to the job site. It also eliminates delays when the weather isn’t favorable. Peers also have pre-fab production facilities, but as their houses allow for higher customizations, the process isn’t as streamlined.

Moreover, NVR’s manufacturing sites are located within 90% of their communities . The proximity to land developers, their workers, and subcontractors helps NVR maintain a close relationship across cycles, in addition to higher productivity and efficiencies.

The focus on one region, the proximity of NVR’s operation to its community, and the pre-fabrication construction process provide major scale/cost competitive advantages , reflected clearly in the 20% operating margin, 4% above industry standard, 80-day cash conversion days vs 300+ for the industry, despite having an industry average gross margin.

High barriers to entry

A new entrant must secure at least five years’ supply of land inventory in the best areas to compete with the top builders, creating a scarcity barrier to scaling immediately. The poor initial economics combined with the long investment cycle is a significant deterrent to entering new metros that are already saturated. It’s not impossible, but it’s challenging to do well.

NVR uniqueness - an invisible moat

The secrets are written on the wall. After 30 years of running a land-light business model that resulted in 30 years of recording no losses and the highest return on investment over the cycle, no competitor has managed to copy it successfully and durably.

I can only say that NVR’s moat must be invisible ! Or it is mostly hidden in intangibles - stuff we can’t see.

Let me go to another capital-intensive and cyclical industry to explain what I mean.

Take the low-cost airline segment—the airline's success results from filling up the planes and cutting costs. But there is only so much you can do to do this. For example, standardize aircraft models to cut training and maintenance costs, enforce single-class seating to cut boarding time, simplify in-flight meals to minimize cleanup time, and target uncongested air-ports to reduce take-off and landing time. The cost savings reinforce airlines’ ability to reduce ticket prices and, hence, more customers to airports, which also allows cheaper landing fees and secures lower prices on aircraft and other items bought in bulk.

Ryan Air has done all these and enjoyed nearly 20% operating margins since 2000 until COVID-19! That’s unheard of in many industries, let alone in the airline industry. Like NVR, Ryan Air’s playbook is open, yet no other budget airlines come close. Even the larger ones tried and failed. So, Ryan Air and NVR must have more than planes and land lots on the balance sheet. I can only attribute it to the discipline and patient approach in executing the activities that contribute to adding value.

Why don't other home-builders use options? - you ask?

I’d guess home-builders, at the core, are land speculators. Thus, their existence is tied in with the adrenaline rush and the excitement of owning land and selling it at a huge profit in upcycled.

Ensemble Capital put out a note on NVR back in 2022, saying,

[…] Despite NVR's land-light strategy success, the industry's use of land options remains lower than it was during the housing boom in 2004-2006.

[…] They're not moving toward NVR's land-light asset-light business model. The industry is sticking to the asset-heavy own the land and pray model.

NVR doesn't care about getting rich quickly or land grabbing to maximize market share nationally. Their success stemmed firstly from the determination to avoid another bankruptcy. They are patient and satisfied with getting rich slowly in upcycles and then using downcycles to enter new markets when most struggle to survive.

In the global financial crisis, they entered six new markets and bought back 35% of their share outstanding at the lowest prices between 2009-2012—impeccable timing and conviction.

Its return on invested capital never dipped below 12% in the worst of the global financial crisis. That's nearly the same as the industry average today.

Phenomenal value creation and skillful capital allocation

Many businesses claim to be differentiated and that competitors can’t replicate their business model. But the truth lies in the fundamentals.

NVR’s top-class metrics vs peers (Sleep Well Investments)

{kind=link}

NVR’s fundamentals shine uniqueness .

NVR requires the lowest Capex / Operating Cash Flow at 1% vs. 4% on average and the lowest inventory requirements at 20% of sales vs. 65% of sales, yet it generates the highest operating margin. That spells efficiency and asset-light.

Sleep Well Investments

While the industry average return on invested capital ((ROIC)) of the last ten years was 16%, NVR’s was 60%. It was the only one that grew FCF per share by 30% CAGR, while others burned cash in some years (hence, no CAGR value in the table below).

Sleep Well Investments

The trade-off is that NVR grows revenue slower than the top guys in an upcycle, at just 15% vs 20% for D.R Horton or 21% for Toll Brothers. However, it was still in line with the industry growth rate of 15%.

NVR’s ROIC, margin, low inventory, and CAPEAX requirements are in a class of their own. Let’s not forget that NVR buys back stocks, too, allowing it to grow earnings and free cash flow per share higher than peers.

Sleep Well Investments Sleep Well Investments

{kind=link}

{kind=link}

Unsurprisingly, the stock has returned 30% CAGR since IPO and 20% in the last ten years, the best in the industry.

Lastly, unlike its major homebuilding peers, NVR’s asset-light, cash-rich balance sheet is a distinct advantage during downcycles in the housing market. This was displayed following the 2008 housing crisis when NVR expanded into new markets like Florida and Ohio. I expect NVR to make similarly opportunistic investments in a prolonged weak housing market.

Homebuilding market and NVR’s future revenue

-

Demand: affordability, millennials, population growth from WWII

-

Supply: housing stock shortage, vacancy rate, new build [Part 2]

-

Average house price movements

-

What to track to get ahead

-

Growth opportunities

NVR’s business is driven by the demand and supply of newly built homes in the US . These two factors determine the average price.

We are not trying to predict the housing market, but we will look into a few leading indicators so we can track and understand the future outlook better.

1. Demand

Demand is driven by affordability, the general growth in population, and the growth of millennials who are at the age of buying their first home.

a. Affordability

Affordability is driven by income, interest rate, and house price changes (more on this later). It’s most affordable when income is high, interest rate is low, and house price is decreasing. In the previous housing crisis, affordability was not bad because the falling house prices and interest rates (2008-2016) outweighed the drop in income and employment.

Sleep Well Investments

However, affordability has fallen since 2016 and is currently at its lowest point in 20 years, driven primarily by rising mortgage interest rates and high house prices.

Sleep Well Investments

Across the US, affordability is as low as in the pre-housing bubble in 2006/7. Zooming in on the DC area, where NVR is a market leader, affordability is also deteriorating fast.

Sleep Well Investments

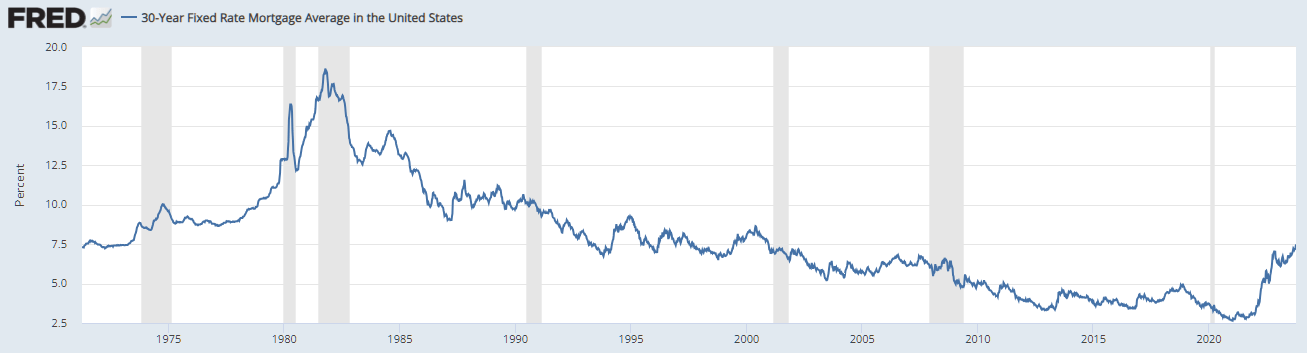

Looking back to the 1960s, interest rate change has been the largest driver of affordability. We have had an incredibly low interest rate environment between 2008 and 2021; the 30-year fixed-rate mortgage averaged around 3%.

{kind=link}

Today, the current 30-year fixed rate in the US is equivalent to the 1990s at 7%. The high-interest rate will be quite sticky as employment is still strong. Meanwhile, the Fed base interest rate is on par with the peak of 2006-2008.

Sleep Well Investments

So, my approach is always to be prudent. Hence, I assume we are entering a prolonged period of high mortgage rates. The average homeowners’ mortgage payments will likely be 2-4x that of the last decade; affordability will remain low and negatively impact housing demand in the next 2-3 years unless their income increases or house prices decrease significantly.

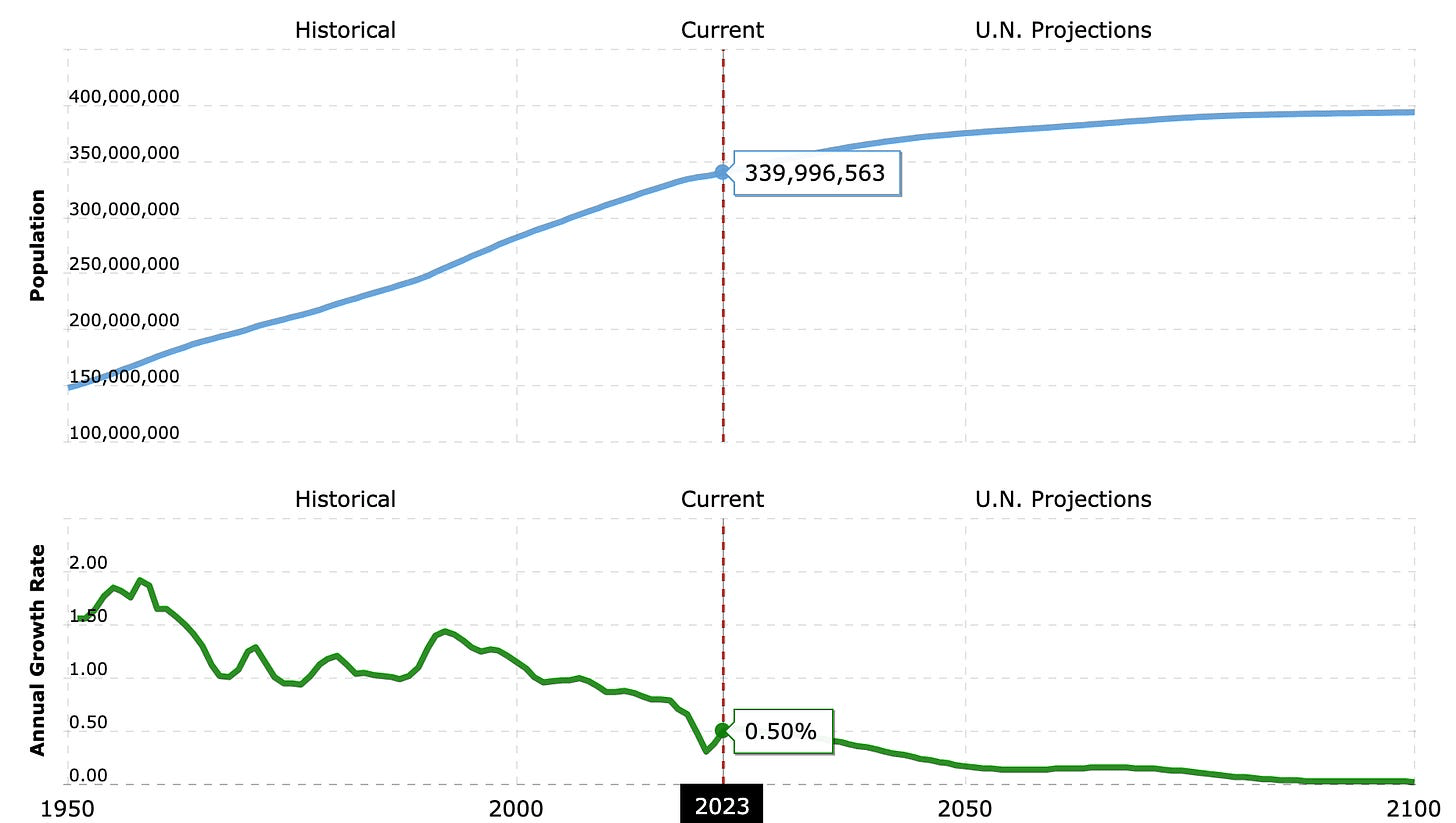

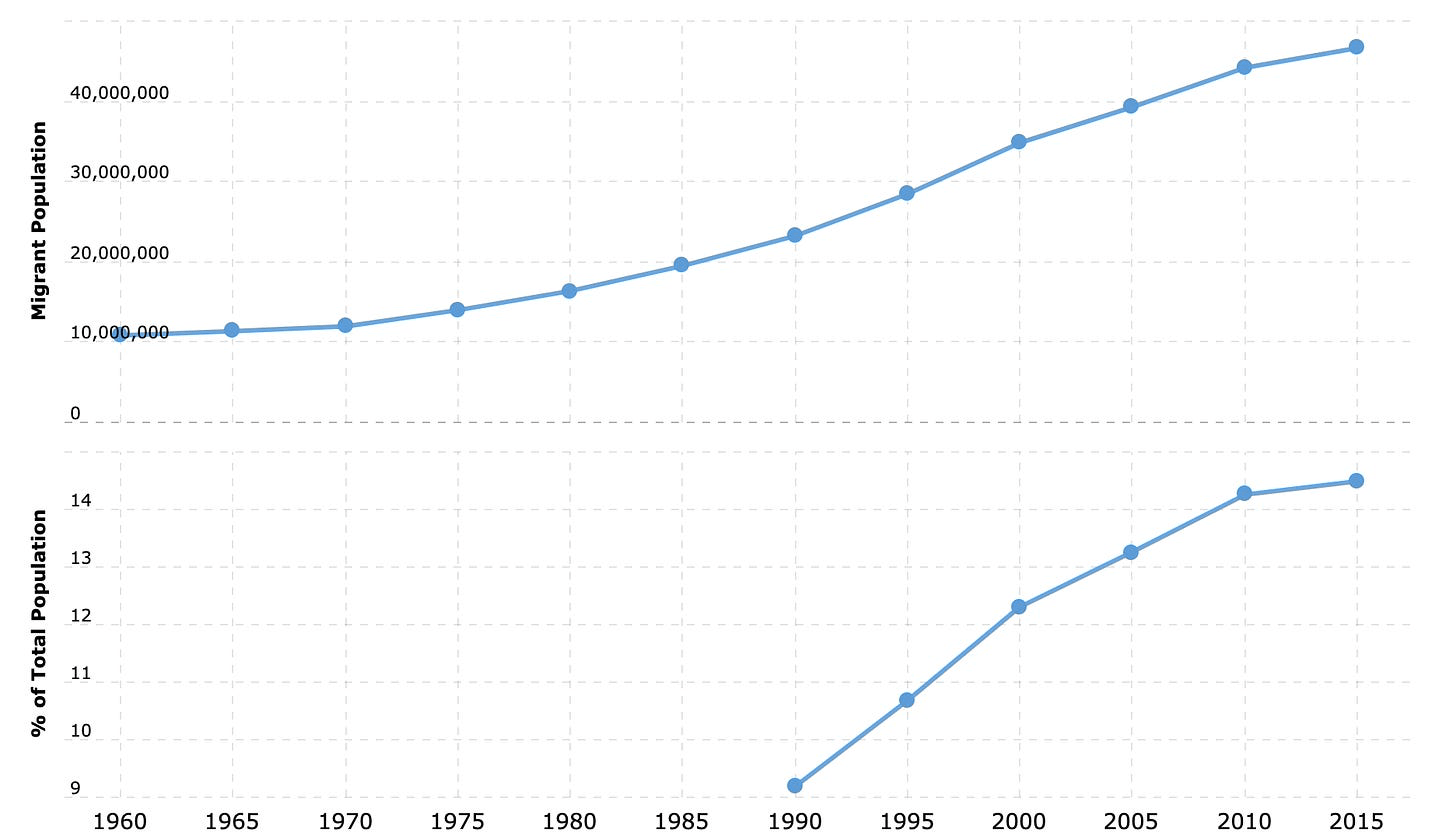

b. Population growth (1950-2100)

The second factor that impacts housing demand is the growth of the US population. More people = more demand for housing.

Population growth is a function of natural increases (births - deaths) and net immigration.

Since WWII to 1990, the US has had strong population growth (1-1.5% per annum) thanks to baby boomers and a jump in life expectancy.

{kind=link}

But from 1990 to today, population growth has meaningfully decreased to about 0.5% pa, mostly attributed to sustained net migration flow as birth rates declined.

{kind=link}

Net migration accounts for nearly 15% of the total population today and over 50% of the population growth rate (vs. 20-30% between 1950 and 1980).

Sleep Well Investments

Going back to the first chart, the United Nations projects the US population to grow at just 0.25% per annum over the next 80 years, decelerating from 0.5% per annum in the next few decades, buckling the trend in Europe, and could move to negative growth at some point.

That means for the next 10-20 years, a 0.5% increase in population equates to an additional 1.7M newborns and migrants each year, which will drive the number of households (2 adults+) higher, as it did in the past, adding around 1M+ new households each year.

Global Data

The number of households around the East Coast, where NVR operates, has grown by 10%+ per annum in the last decade.

Pew Research Center

With the US growing population (1.7M each year) and rising number of households (1M+ each year), the demand for more housing will only increase.

c. Demographic change

The third driver of housing demand is the millennials, aged between 28-43. They will play a key role as they are the largest age cohort in the U.S., with 72 million people, and they are entering their prime home-buying years.

Sleep Well Investments

Let’s try some napkin maths. Assume most millennials buy a new home with their partner. In the US, 50% of the population is married, so out of 72 million millennials, we assume 18 million married millennial couples (72 x 50% = 36 M married individuals or 18 M couples) will need a larger home in the next 5-10 years.

65% of millennials aspire to own a home, but 50% already own one (according to the US homeownership rate, 2022); so, roughly 2.7 million millennial couples are looking to own a home in the next 5-10 years (15% x 18 million) .

So, while affordability has been at its lowest point for decades, when you combine an influx of 1.7M in net migrants and newborns and 1M+ of new households each year, with 2.7M millennials entering their prime home purchasing years, supply better keeps up!

However, the US is incredibly short of homes.

2. Supply

According to the most recent estimates from Freddie Mac , the country is short about 3.8 million housing units for rent and sale, increasing from 2.5 million in 2018. CNN and other sources estimate the shortage is up to 6.5M .

US Census

The table above shows that while the number of households increased over the years, the number of housing units available (vacancy) decreased, creating a gap of 3.8 million homes.

The main reasons are:

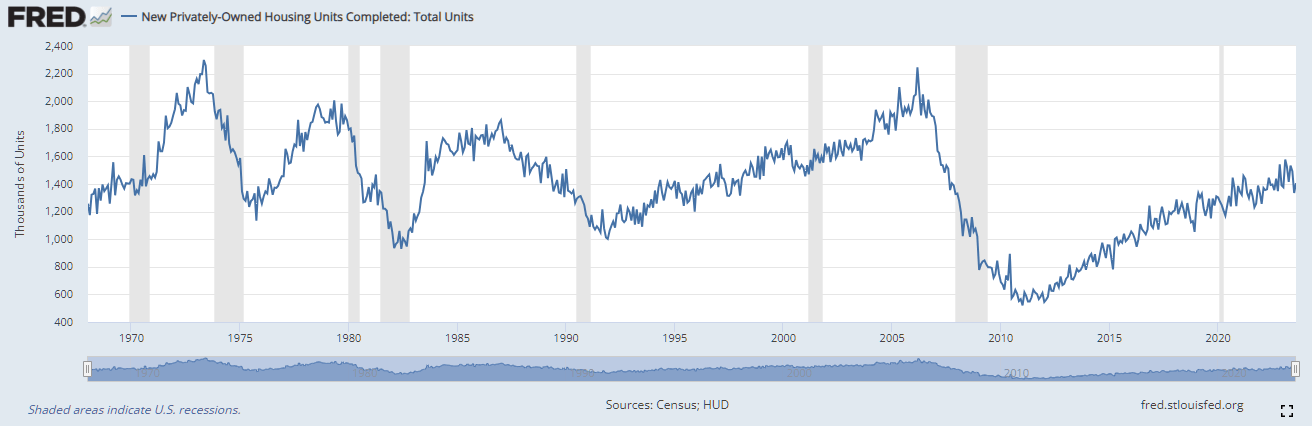

- Homebuilding activity cratered after the Great Recession and never recovered (see chart below).

{kind=link}

- US home builders build more homes in the good times and almost stop when it’s bad. The differential is huge. In 2006, they built 2.2M single and multifamily units and dropped 70% capacity to below 0.6M units in 2011. They built more homes since then, but until now, new builds have not recovered to the previous peak, hovering at 1.4M units.

US Census

-

The annualized housing starts per 1,000 households tells an even worse story. The US is building half what it used to be, at 12 new houses for 1000 households, compared to the 1960-1990, at 22 new houses per 1000 households.

But, their hands are tied.

-

There is a lack of available labor to build homes and lengthy regulations over land use and zoning limit construction. For example, in some jurisdictions, the maximum number of dwelling units allowed in the highest residential zone (8 units per acre) rose from 15.5% in 1994 to 16.0% in 2003 and 22.4% in 2019, based on National Longitudinal Land Use Survey data. The gradual increase in restrictive zoning has limited new housing construction and raised prices. Additionally,

-

Fewer adults are living together. In the past 140 years, we have seen a gradual fall in marriage and a rise in divorce , which results in fewer adults/household.

US Census

There are only 2.51 adults/household today vs. 3.33 seventy years ago. There is more competition for vacant homes today than ever.

US Census

Altogether, there is a major structural problem. In numbers, there are

-

1.7M newborns and net migrants each year

-

1M+ new households form each year

-

2.7M millennials looking for their first home, while we have

-

3.8M to 6.5M homes short

Homebuilders must build more than the current 1.4M homes/year to close this gap. Assuming it could build 1.7M homes each year, closing the current gap would take 13 years . In the unlikely scenario that they build 2M homes each year, it would still take more than six years to close the gap , all else constant. All point to a prolonged undersupplied housing stock, and prices increase when too many buyers chase too few supplies.

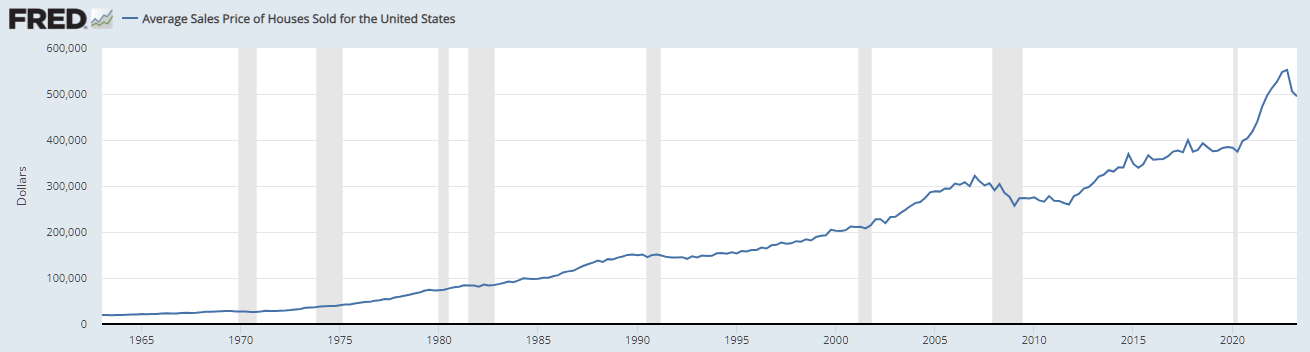

Average house price

With the imbalanced demand and supply above, it’s no surprise we see a chart like the one below.

{kind=link}

The average house price has risen from $300K at the peak of the last bubble in 2006 to $500K today, roughly 5% CAGR, surpassing the US GDP growth of 2% CAGR.

However, the good news is prices can only rise if there are enough buyers - which we have in abundance- but with a 2-4x jump in mortgage costs compared to last year, demand cannot be sustained for long.

Additionally, when affordability is at its lows (usually at recessions), the adults/household ratio starts to go up again. Young people live at home longer, and more people opt to share their space. That can also hurt demand for new industry completions, even with a housing deficit.

Overall, I am more on the side of a weak near future demand due to record low affordability , but I acknowledge that due to a structural shortage in housing supply for the next 5-10 years, house prices are unlikely to decline like the last recession .

So, assuming we have soft price increases or decreases, NVR’s revenue and other builders’ future rely on the number of house starts in the coming years.

Next, I lay out the metric to track this indicator, so I’ll be ready to own a piece when an opportunity comes.

What to track?

I believe there are a few leading indicators investors can track to get ahead of the game.

-

New build permits (industry)

-

Housing starts (industry) - new orders (company)

-

The average price of the new orders (company)

-

Cancellation rates (company)

Let’s go through each.

Between June and Oct 2022, we saw a significant drop in permits (light blue) and starts (navy blue), which coincided with NVR and the homebuilders’ stock prices’ 30% drop.

US Census

This chart of single-house building permits goes back to 2014, magnifying the dramatic drop in permits during the first half of 2022.

US Census

Second, below are the number of contracts the top 5 builders signed. These are orders agreed to be delivered between 1-3 years, depending on the builder. Paired with the average house price of new orders, less the cancellation rates, we can work out the future revenue.

Sleep Well Investments

Following is the new contract average price. Toll Brothers is an outlier here as they focus on building luxury homes in urban areas with prices 2-3 times more expensive than the other top 4 builders.

Sleep Well Investments

The final aspect to track is the cancellation rates at the company level.

These are home orders that buyers are walking away from, likely because of the change in affordability. For now, the cancellation rates are not out of the ordinary compared to the last five years. High cancellation rates will be a good indicator of a deeper affordability problem.

Interestingly, NVR has the lowest cancellation rate out of the top 4 (except Toll Brothers), indicating a good product and further shines on the unique building setups explained earlier.

Sleep Well Investments

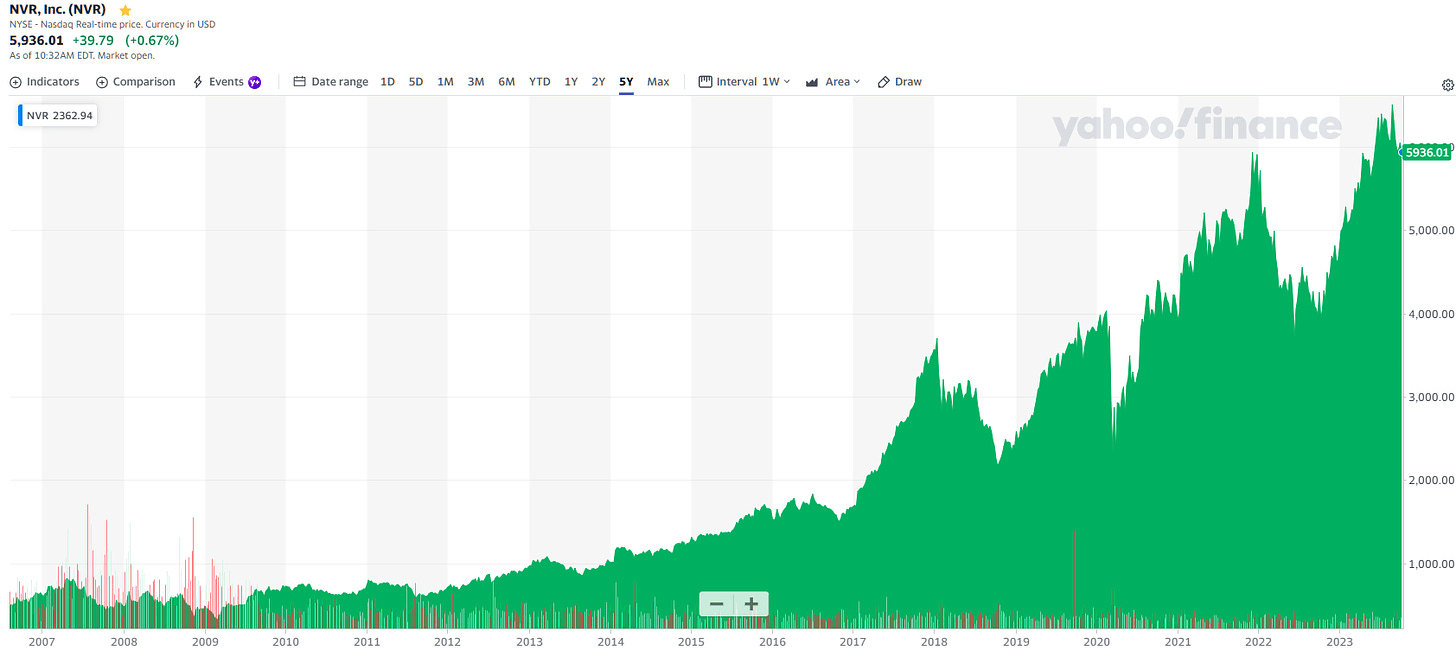

After tracking the four metrics above, I’d also track management’s share repurchasing activities. They have been impeccable in their timing (2010, 2011, 2013, and 2021), and I’d be tempted to follow their lead if the four indicators above also flash red.

Sleep Well Investments Yahoo Finance

{kind=link}

So, what’s left is -

At what price does NVR’s stock become attractive? We will consider a few scenarios in the valuation section.

Before that, can NVR grow from here, and what are the risks?

NVR’s future growth

Housing is a trillion-dollar per annum market . Just residential fixed investment, building new homes every year is about 4%-5% of the U.S. 22 trillion GDP. It’s a major driver of the U.S. economy and the American dream. Compared to NVR’s $10B FY2022 revenue, it’s a drop in the bucket.

NVR has a long growth runway when it decides to leave the East Coast. I suspect that will happen when a crisis hits and other builders struggle.

Besides moving out of the East Coast, NVR will grow organically with the rising prices of new homes (5% CAGR in the past 18 years).

Risks

Macroeconomic conditions

The supply condition is a long-term tailwind to NVR, but it’s not guaranteed that whatever it builds will be sold.

Demand for new homes is sensitive to economic changes driven by employment levels, job growth, consumer confidence, inflation, and interest rates. As we have seen, affordability plays a key role in determining demand.

What drives affordability is the level of interest rates, increasing the cost of borrowed funds to homebuilders and reducing the availability of suitable mortgage financing for the NVR mortgage department, thus limiting its ability to deliver the backlog.

Inventory management

NVR carries some inventory on its balance sheet, although it’s ten times less than top competitors; this inventory of land and buildings would still lose value in a downturn.

Sleep Well Investments

NVR also must continuously acquire lots for expansion into new markets and replacement and expansion within the current markets to maintain a healthy level of backlogs when the market turns.

Material and labor shortages

The homebuilding business has occasionally experienced building material and labor shortages, including fluctuating lumber prices and supply. In addition, strong construction market conditions, like in the past few years, have restricted the labor force available to NVR’s subcontractors. Significant increases in costs resulting from these shortages, or delays in the construction of homes, could adversely affect sales, profitability, and future cash flows.

Extreme weather

Significant snowfalls, hurricanes, tornadoes, earthquakes, forest fires, floods, terrorist attacks, or war are also real risks. Adverse weather can increase costs or delay the construction of homes. Having said that, NVR’s facility proximity and standardized process should shield the business from extreme weather better than peers.

NVR valuation

How much money can I make if things go well? (affordability improves, 30-yr mortgage rate falls quickly)

What will happen if events don’t go as planned? (a recession and collapse in permits, housing starts, and rise in cancellations)

How much could I lose if things get ugly? (70% fall in completion, permits and housing starts like 2009-2012)

These are some of Howard Marks's favorite questions when valuing an investment. I’ll provide two scenarios.

-

Bear case: A housing crash like 2008-2012

-

Base case: A minor housing downturn

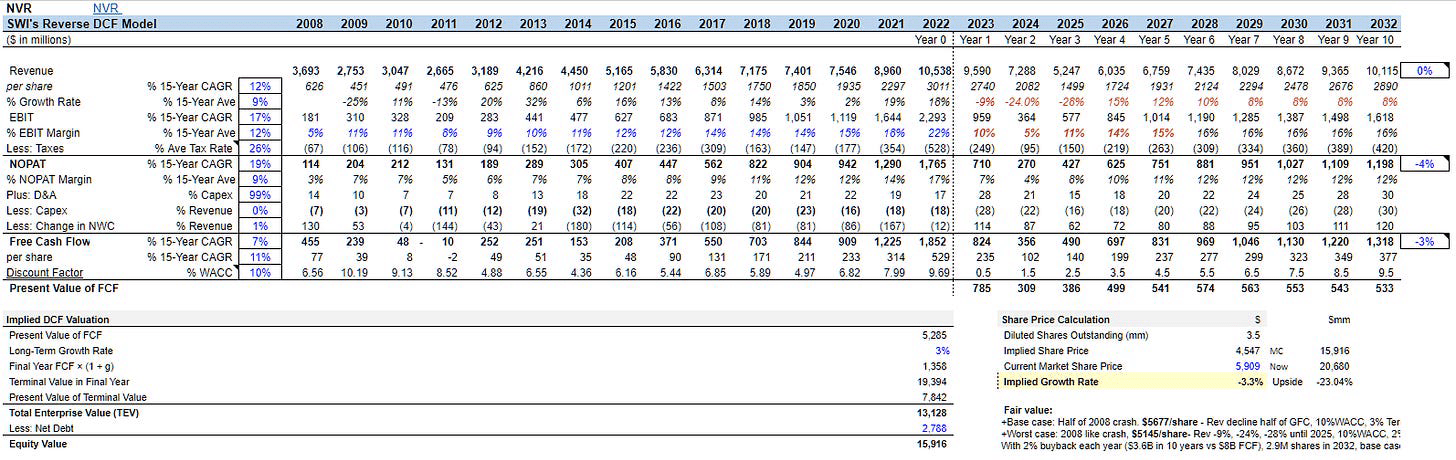

In a bear case , the fair price is $4547/share, a 23% downside from today’s price . I assume we are heading into a deep and prolonged US housing recession. Thus, the assumptions below reflect the 2008 crash with no buyback activity (it’s quite extreme).

-

Revenue declines: -9%, -24%, -28% in 2023-2025, and it takes ten years to recover to 2022 levels.

-

EBIT and FCF profiles are similar to 2008 levels, too.

-

10% WACC, 2% Terminal Growth

With a buyback of 2% a year (50% of FCF), which is also conservative (80% of FCF in the past ten years), we have a fair value of $5488/share, a 7% downside.

Here are the full workings:

{kind=link}

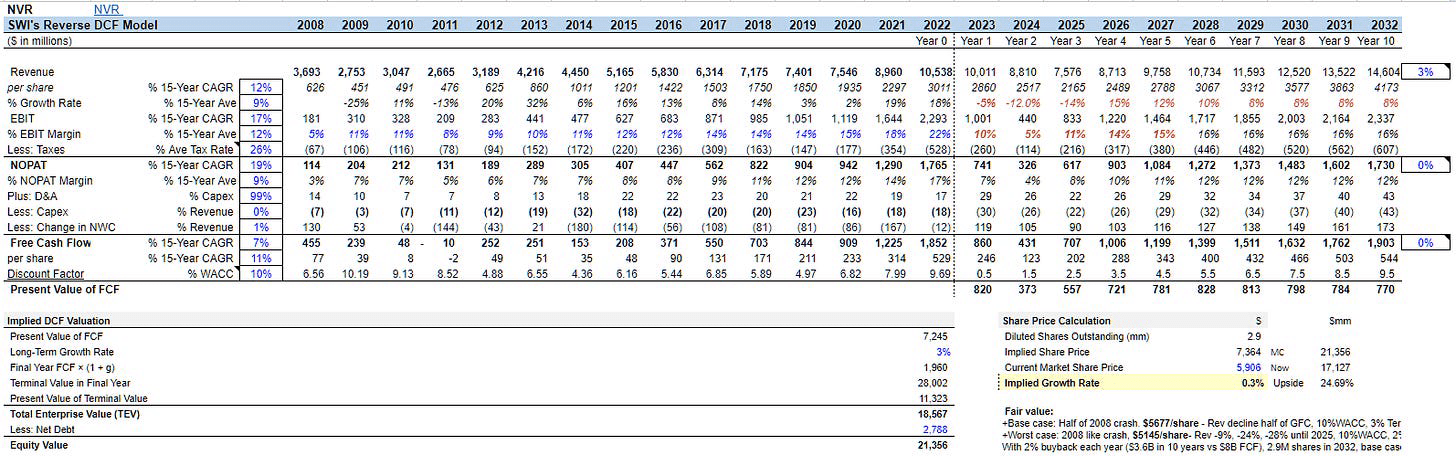

In the base case , we have a fair value of $6102/share or 3% upside. We enter a mild housing crash, so I assume the sale decline is half the 2008-2012 period, while I also assume no buyback.

With a buyback of 2% CAGR until 2032, we have a fair value of $7364/share, a 24% upside. Below is the full workings:

{kind=link}

Whichever camp you take, get comfortable with NVR’s business strategy and track the leading indicators and management capital allocation to ensure an informed buying decision.

After researching NVR deeply, I feel confident that this business is phenomenal. However, I only want to invest if it offers a healthy margin of safety, even accounting for a potentially deep and prolonged downturn in the US housing market. Thus, there is no sunk-cost bias here; I am comfortable staying on the sideline today and will be the first to buy a piece if the stock falls to $4900/share (20% margin of safety) . If I don’t get it, I still have other opportunities to wait for.

Sleep Well Investments scorecard

Wall Street seems to be pricing a mild decline in the next few years, targeting revenue at $9B in 2026.

SA SA

I don’t think that’s conservative. So, let’s return to earth and see how NVR performs under my Sleep Well Investment checklist.

The scorecard is my last layer of defense (from my own emotionally driven decisions) and helps me quantify the quality of market leaders.

NVR - In the last column, it scores 12 points out of the possible 20 .

Sleep Well Investments

+1: Product relevance

NVR scores full points for product relevance. Homes epitomize the American Dream, and even 65% of the new generations - Millennials and Gen Z - aspire to own one. There is little risk of NVR’s business going obsolete here, limiting the risk of permanent capital loss.

+3: Business model

NVR's business model is one of its kind in the industry. It’s land-light, adaptable in different macro conditions, and scalable. Although the final product has little differentiation, NVR’s cancellation rate is one of the lowest, indicating quality. There is some dependency on suppliers and subcontractors, but that has never hindered the business. So it gets a full point.

+6: Financial strength

NVR’s financial metrics are outstanding: 15%+ CAGR growth in revenue and 30% in free cash flow per share, the only builder with a net cash position, consistent gross margin, strongest net margin, and proven ability to survive and thrive in downturns, emerging stronger and poised to take market share. It deserves a full point.

+2: Management

Dwight Schar created NVR’s business model and led the business until 2005. Paul Saville became CEO from then till recently as he moved to Executive Chairman of the Board in 2022. Currently, Eugene Bredow is the CEO, having been at NVR since 2004. The new management has stayed the course and preserved the company’s strategy, culture, and current course of asset allocation. The track record speaks for itself.

Collectively, Paul Saville, the current Chairman, Eugene Bredow, CEO, and other directors own 8.6% of NVR. That’s substantial skin in the game.

10-K

They are also awarded stock options if they achieve a capital return within the industry's top three. Needless to say, the management is well incentivized.

10-K

+1: Antifragile

Since 1993, NVR has thrived after recessions; this is a rare breed of a company in a highly cyclical and competitive industry.

-2: Competition is strong

NVR is the top dog within the East Coast, but moving out of this region, NVR has plenty of competition. It will find it tough to expand unless we have another recession. This is a risk, so 2 points are taken off the overall score.

+3: Moats & barriers to entry

NVR has points for scale/cost and intangibles moats (invisible), which are widening. However, there is little advantage over branding, and the industry barrier to entry is moderate, depending on the size of the new entrant.

-2: Moderate to strong risks

In addition to a highly cyclical industry, there are strong operation risks in land acquisition and managing subcontractors in a full employment environment.

Moreover, single-family home building permits have plummeted since 2022. Cost inflation or volatility regarding materials such as lumber have wreaked havoc on margins for less savvy operators. And the trajectory of inflation in building materials and labor remains unpredictable.

-0: Fairly priced

That makes 12/20 points. A point away to qualify as an investment.

I’m comfortable with the business strategy, moats, and opportunity to reinvest in growth when a recession comes, but what’s missing is a point from valuation to make it investible today.

How to track NVR - Thesis Tracking

-

For supply: I’ll track single and multifamily home building permits and housing starts. I’ll also track NVR’s new orders and the average price of new orders.

-

For demand: I’ll track affordability - interest rates and mortgage application. And I’ll also track the cancellation rates.

-

For a signal to start buying, I’ll track management buybacks, given supply and demand indicators above are flashing red.

Closing thoughts

NVR is an outstanding homebuilder with a unique business model that offers investors a high return on invested capital and significantly lower financial risk than its competitors. The company's subtle barriers to entry and strong market position should enable it to continue its success.

NVR's exceptional attributes in the home building industry make it a must-have addition to my Sleep Well Portfolio. However, I am aware that housing market downturns can be lengthy and brutal. Although NVR remained profitable during the housing crisis, sales dropped more than 50%, taking over a decade to reach new highs. Therefore, I will only invest in the company if it offers a healthy margin of safety, even accounting for a potentially deep and prolonged downturn in the US housing market in the years ahead. I will closely monitor NVR's investment case and consider it further if the share price approaches the $4,900 level.

Stay tuned for my investment thesis updates!

Thank you for reading!

For further details see:

NVR: A Deep Dive Into This Phenomenal Homebuilder