NVR - NVR: A Unique Home Builder That's Reasonably Priced

Summary

- Over the last decade, NVR has established an impressive track record for growth, profitability, debt management, and share repurchases.

- There has been much speculation about the risks of an upcoming recession that would negatively affect NVR.

- NVR is priced well enough to begin building a position in your portfolio.

Business Model and History

NVR Inc. (NVR) is a company that operates in the construction and homebuilding industry. The company designs, builds, and sells homes through its various brands, including Ryan Homes, NVHomes, and Heartland Homes. NVR's business model is based on acquiring land and obtaining construction permits, building homes on the land, and selling the homes to customers.

NVR typically acquires land through a combination of purchasing land directly from sellers and entering into agreements to develop land owned by others. The company then obtains the necessary permits and approvals to build homes on the land and constructs the homes according to its own designs or the designs of the customers. Once the homes are complete, NVR sells them to customers through its own sales teams or through independent real estate agents.

In addition to its homebuilding operations, NVR also provides mortgage financing and title insurance services to its customers through its NVR Mortgage and NVR Title subsidiaries. These businesses are integrated with the company's homebuilding operations and allow NVR to offer a full range of services to its customers.

NVR was founded in 1980 by Dwight C. Schar. The company was originally known as NVHomes, and its focus was on the construction and sale of luxury homes in the Washington D.C. metropolitan area. In the early 1990s, NVR expanded its operations to include the construction and sale of homes in other parts of the United States.

Over the years, NVR has grown through a combination of acquisitions and organic growth. In 1986, the company acquired Ryan Homes, a homebuilding company based in Pittsburgh, Pennsylvania, which expanded NVR's presence in the eastern United States. In 2012, the company acquired Heartland Homes, a homebuilder based in Indianapolis, Indiana, which expanded NVR's presence in the Midwest.

Today, NVR operates through its various brands in more than 25 markets across the United States. The company is headquartered in Reston, Virginia and is publicly traded on the New York Stock Exchange.

Track Record

Recently, NVR's leadership has experienced significant changes. In May 2022, Paul C Saville stepped down as Chief Executive Officer and became the company's Executive Chairman. Saville is well respected within the industry; he's been employed with NVR since 1981 and served as the company's CEO since 2005. Saville will continue to continue to provide his leadership and help define the company's strategic direction as Executive Chairman.

Stepping in for Saville is NVR's new President and Chief Executive Officer Eugen J. Bredow. The future should be bright under Bredow's leadership as he has had an impressive career up to this point. Bredow started with NVR in 2004 and has held several leadership positions prior to becoming CEO including being the President of NVR Mortgage, Senior Vice President and Chief Administrative Officer, Vice President and Controller, and Chief Accounting Officer.

Under Saville and Bredow's leadership, NVR has established an impressive track record of growth. Over the past decade the company has grown it's revenue by 137% with not a single year of revenue declines.

NVR Data by Stock Analysis

NVR's impressive track record for growth extends to its free cash flow growth as well. The company has increased its free cash flow every year since 2014 and over the past decade free cash flow has grown a staggering 415%.

NVR Data by Stock Analysis

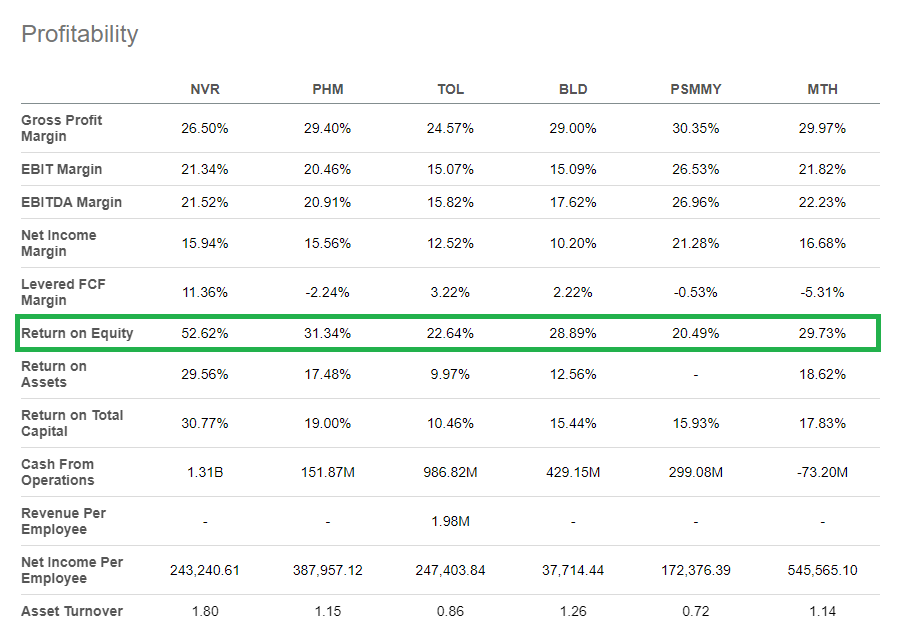

Beyond growth, the company has also established a strong track record for profitability. NVR has averaged a return on equity of 35.9% over the last decade without a year under 15%. In addition, the company has reported its highest ROE in the previous 12 months at 54.40%. Yet what's most impressive is how NVR compares with its peers because it's reported one of the highest ROEs in the industry.

{kind=link}

In addition, NVR has done an excellent job managing its debt. The highest debt-to-equity ratio the company has had over the last decade has been 0.53, seen in 2021 and 2014. The company also sports an interest coverage ratio of 46.93 while tripling its book value over the past ten years. Therefore, the company's balance sheet is rock solid.

One last note on NVR's track record is the company doesn't pay a dividend but is known to repurchase shares. Over the past ten years, NVR has repurchased 31% of its outstanding shares.

Land Light Business Strategy

One reason for NVR's superior track record in growth and profitability is its land light business strategy . The company primarily acquires finished building lots from third-party land developers through fixed-price agreements (LPAs) that require deposits which may be forfeited if the company fails to fulfill the agreements. The deposits are typically around 10% of the aggregate purchase price of the finished lots.

This gives NVR the option to choose not to fulfill the agreements, and the only legal and economic loss in this case would be the deposit. They do not have any financial guarantees or completion obligations and generally do not guarantee lot purchases on a specific performance basis under these LPAs. Creditors of the development entities do not have recourse to the company's credit.

Ultimately, NVR believes that this strategy avoids the risks and financial requirements associated with direct land ownership and development while also helping them maintain control over a supply of suitable lots to meet their five-year business plan.

Risk Factors

There are significant risk factors regarding NVR that investors need to consider before investing in the business. Chiefly among them is the risk of an economic downturn. If there is a decline in economic conditions, the demand for new homes is sensitive to those economic changes. For example, suppose there is a downturn in the housing industry. In that case, the company's sales may decline, negatively impacting its profitability, stock performance, ability to pay debts, and future cash flows.

In addition, high-interest rates and high inflation can negatively impact the business. High inflation rates can harm the homebuilding industry because they can lead to higher interest rates, which can increase the cost of borrowing funds and make housing less affordable for potential buyers. NVR is also subject to fluctuations in the price of commodities used in its homebuilding business, including lumber, concrete, and steel. As the price of these critical commodities increases, so does the cost to build homes, which negatively affects demand for the houses NVR builds.

Economic downturns, high-interest rates, and high inflation negatively affect most businesses to some degree, but they are particularly impactful to the home building industry. For most people, a house is the most significant purchase they'll ever make, and in times of economic hardship, purchasing a house is just not possible for many people.

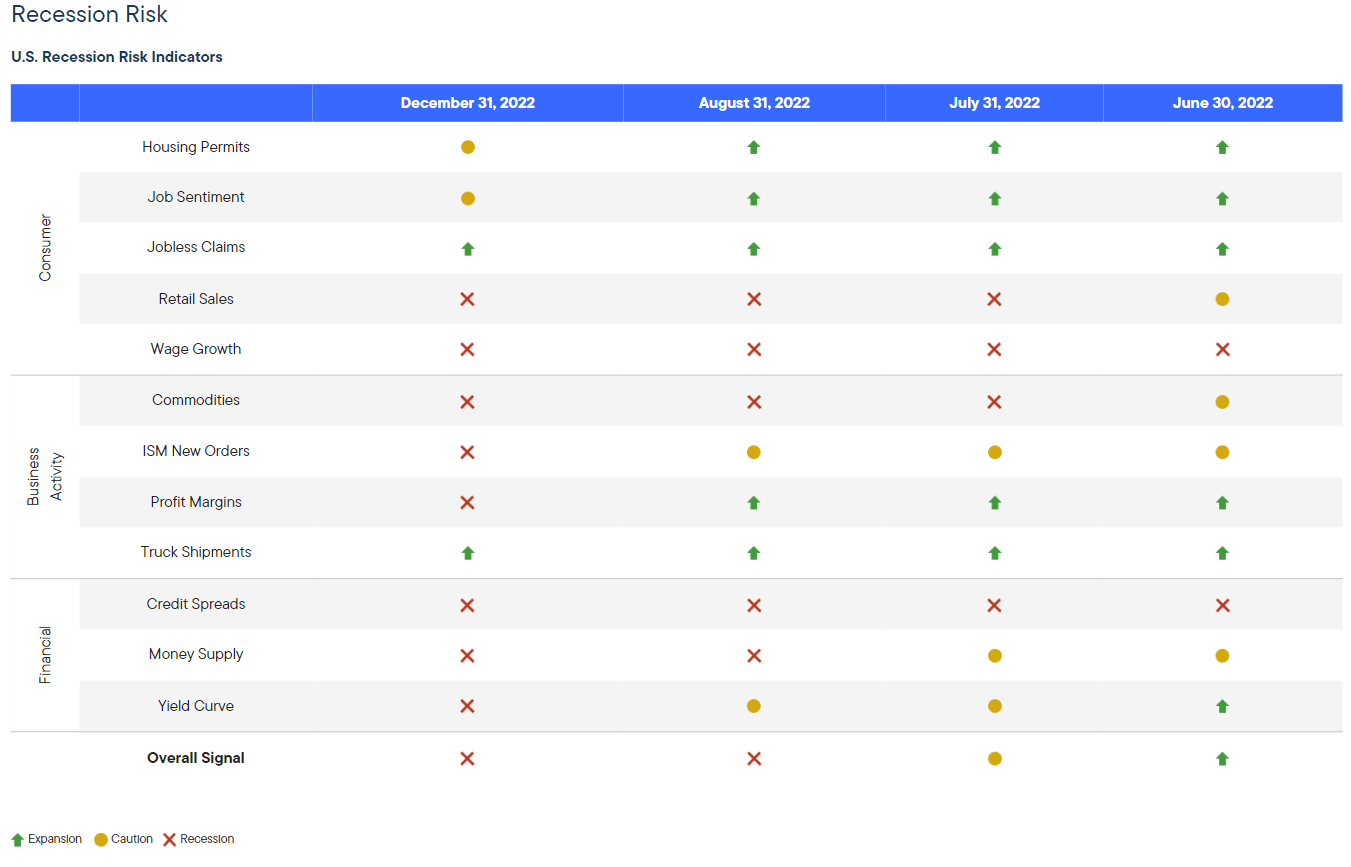

I cannot speculate on the state of the US economy. There are just too many factors to predict what will happen reliably. Nevertheless, there has been much speculation about the risks of an upcoming recession. Franklin Templeton puts together an excellent "Anatomy of a Recession" program that delivers a monthly snapshot of the state of the US economy. Recently, the results have not been encouraging.

{kind=link}

Valuation

To estimate NVR's intrinsic value, we will run comparative and discounted cash flow ("DCF") analyses. To begin, we'll start with the comparative analysis and look at the highest, lowest, and median price-to-earnings ratios the market has paid for NVR over the past five years. We'll also look at the sector median P/E, which is 13.57 . Finally, we'll multiply these ratios by NVR's consensus 2023 EPS estimate of $ 337.36 per share.

| Scenario |

| P/E |

| trailing 12-month EPS |

| Intrinsic Value Estimate |

| % Change from Current price |

| Bear Case |

| 8.811 - Oct 14, 2022 |

| $337.36 |

| $2972.47 |

| -40.23% |

| Base Case |

| 16.91 - 5 -year Median |

| $337.36 |

| $5704.75 |

| 14.69% |

| Bull Case |

| 29.09 - Jan 19, 2018 |

| $337.36 |

| $9813.80 |

| 97.32% |

| Sector Median Valuation |

| 13.53 |

| $337.36 |

| $4564.48 |

| -8.22% |

On a comparative analysis, NVR has a wide range of scenarios that can play out. Investors could realize an excellent 97.32% return if the market were bullish and applied the 29.09 multiple, seen in 2018, to next year's average analyst earnings estimate, should those estimates materialize. On the downside, investors could realize a -40.23% loss if the market were to value NVR at the P/E ratio seen just a few months ago in October 2022. Keep in mind that NVR's consensus 2023 EPS estimate is -24.60% lower than its trailing 12-month EPS.

Turning to the discounted cash flow analysis, we will begin by taking the average of the last five years of free cash flows, which is $996 million. Please note that this figure is 23.14% lower than the free cash flow that NVR has accumulated over the trailing 12-months, which I believe is a good starting point due to the current fears of a recession in the US economy.

Then we will apply a 7% growth rate for the next ten years based on rule 72, which states a 7% growth rate will double the original value in 10 years. We will follow rule 72 for this DCF because it's challenging to accurately forecast free cash flow growth rates multiple years into the future. Still, I am confident that NVR will be able to double its free cash flow over the next decade regardless of the near-term concerns regarding the state of the US economy.

Following the 10th year, we will use a 2.5% growth rate into perpetuity to determine the terminal value. We will then use a discount rate of 10%. I use this discount rate because it's my personal required rate of return. With these inputs, the DCF analysis gives us an intrinsic value of $6304.22, representing an upside of 26.54% from NVR's current share price.

{kind=link}

If you believe a 7% growth rate over the next 10 years is too aggressive, consider that NVR would only need to grow a little more than 3.5% per year over the next decade for its current share price to match the estimated intrinsic value from this DCF. However, as it stands now, NVR looks like a decent deal.

Take Away

Over the last decade, NVR has established an impressive track record for growth, profitability, debt management, and share repurchases. This performance can be attributed to its excellent leadership team and unique business model. Though there are fears of an impending recession that would negatively impact NVR's business, the company's stock is trading at a reasonable price based on a discounted cash flow analysis.

This investment opportunity comes with risks in the short term, but if you can stomach some risk for short-term losses, this business can be a winner in the long term. NVR is priced well enough to begin building a position in your portfolio, but if you disagree, please let me know in the comments section below.

Thank you for reading!

For further details see:

NVR: A Unique Home Builder That's Reasonably Priced