NVR - NVR: Controlled Risk With Potential Upside

2023-10-03 07:28:08 ET

Summary

- NVR's unique business model benefits from the upside in an inflationary environment while protecting the downside in a recession.

- The company is enjoying some tailwinds from a shortage in the housing market in the U.S.

- Through the whole cycle, NVR's average return on capital employed is at 24% and is improving.

Investment thesis

I don't usually like to own cyclical businesses and try to look for those who perform well in as many economic environments as possible. I am making the exception with NVR, Inc. ( NVR ) because of its high returns on capital, increasing margins, and impressive business model.

As I will show in this article, NVR is not a classical house builder with a leveraged balance and high risks related to land and housing inventory.

NVR's unique business model allows the company to benefit from the upside of an inflationary environment while it gets protection on a downturn, as we saw in the 2007-2009 financial crisis when it had the best performance compared to its peers.

The company is enjoying some tailwinds from a shortage in the housing market in the U.S., and it operates in some of the best states of the country.

The housing business is not likely to be disrupted by any new technology or artificial intelligence, which provides an extra margin of safety over the long term.

Company background

NVR is one of the largest U.S. homebuilders (mainly single-family detached homes) and complements its business with a mortgage banking division to fully serve its customers.

The company was formed in 1980 in Virginia, it currently operates in fifteen states in the eastern part of the U.S. and Washington DC, and operates under three business names, Ryan Homes, which is marketed primarily to first-time buyers at more affordable prices, NVHomes, and Heartland Homes, its more expensive and luxury segments.

The company has evolved its business model and it is not the typical homebuilder. In 1992, NVR filed for bankruptcy because of decreasing demand for new housing in an over-built market and bad risk management, since it had an overloaded balance of inventory ($600MM at the beginning of 1990 for $30MM net income in 1989).

The company learned its lesson, and as we will see in the next sections, it has allowed it to reduce risk, perform better than its competitors, and deploy its capital in a more efficient way.

In the upcoming years, the company concentrated its business on fewer states and made some small acquisitions to enter surrounding markets and improve efficiency. In 1997, it acquired Fox Ridge Homes for $20MM, entering the Nashville market, in 2005 it bought Marc Homebuilders , which operated in the Columbia South Carolina market, and in 2012 it acquired Heartland Homes for $17MM, the second-largest homebuilder in Pittsburgh.

Business model

What makes NVR's business model particular is that instead of purchasing the land directly, they control it through options, which typically range up to 10% of the purchase price of finished lots. To get control over the land, they sign land purchase agreements ((LPA)) with land developers and give a deposit in the form of cash or letters of credit (usually cash), which allows the company to avoid the financial requirements and limits its risk in a market downturn since they can walk away and not exercise the option.

Using this purchase model, NVR gets protection on the downside, while profiting in an inflationary environment with rising land prices.

Once they have arranged with the final home buyers the delivery of the houses and got the initial deposits, they exercise the LPA and start the construction, which is usually delivered in less than 90 days to its customers.

NVR leases seven production facilities where they stock some of the building materials and pre-assemble them before delivering them to the building site to reduce delivery times and increase inventory rotation.

The company offers a limited number of house models that can be customized, which requires less material inventory and design costs. As mentioned earlier, NVR operates on the East Coast with a higher geographical concentration when compared to its competitors, which allows the company to be more efficient and develop strong relations with land developers.

On top of the construction segment, which represents over 97% of total revenues and 92% of net income ( 2Q 2023 ), NVR also has a mortgage banking division that provides mortgages to 86% of its home buyers. To avoid carrying the liquidity risk, the company sells all its mortgages to investors in the secondary markets, usually within 30 days from the loan closing.

The company employs approximately 6,550 full-time employees, of whom 5,500 are working in the homebuilding segment and 1,050 in the mortgage banking operations. Reviews from employees are in line with its competitors ( 3.7 out of 5 at Glassdoor ).

Since the company operates on the East Coast, I believe NVR has fewer risks in a market downturn compared to its competitors, since those are states with a higher percentage of public employees , like Washington D.C., Delaware, Virginia, New Jersey, or Maryland.

Regarding seasonality, NVR generally has higher new orders in the first half of the year and higher home settlements and net income in the second half.

This conservative business model in a cyclical industry paid off during the 2007-2009 great financial crisis when NVR's stock fell by 65% from its peak at the end of 2005 to its bottom in March 2009, while other homebuilders like Lennar Corporation ( LEN ) fell 95%, PulteGroup, Inc. ( PHM ) 93%, and D.R. Horton, Inc. ( DHI ) 91%.

Financials

One of the aspects that caught my attention about NVR's business model is its impressive financials since I don't usually own stocks that operate in cyclical industries.

I believe it is important to evaluate NVR's performance through the whole cycle, and not just a few years where the company performed better than average like it has done in the most recent years due to a shortage of housing, as we will see later, and a low-interest environment.

Since NVR doesn't own the land until it starts building, it has a light balance, where almost half of the assets are cash. In the 2Q 2023, the company had $2.6B in cash for a total asset balance of $6.2B. It had $1.8B of lots and housing units covered under sales agreements with customers and $438MM in mortgages held for sale. Building materials are just $22.41MM (2Q 2023), which reduces the risk on a downside but also limits the upside in an inflationary environment since they can't benefit from the increasing cost of building materials held in stock.

On the equity and liability side, $4.1B is equity and $900MM are its Senior Notes due 2030 at a 3.00% interest rate.

This asset-light balance with high inventory turnover allows NVR to achieve superior returns on capital, which can be reinvested in the business and returned to shareholders through share buybacks.

Author (Data from NVR's Annual Reports)

When reviewing NVR's return on capital employed through the whole cycle, from the heights of the housing market in 2006 to 2022, the average ROCE is at 24%.

It wouldn't be fair to judge NVR's performance with the most recent results, since the company had gross margins of 26.7% in 2022 and 23.6% in 2021, way above its average gross margins of 19% (2006-2022) because of increasing inflation, low-interest rates and the pandemic effect were many families were looking for moving into bigger houses, and I expect margins to reduce in the upcoming years.

The data that I believe is representative, apart from the increasing ROCE, is that the company has been able to increase its net income margins thanks to its operating leverage and the reduction of its selling and administrative expenses compared to revenues.

In 2006, with a 22.1% gross profit margin, NVR's net income margins were at 9.6%, while in 2019 and 2020, with gross profit margins at 20.2% and 20.8% respectively, net income margins were at 11.8% and 11.9%.

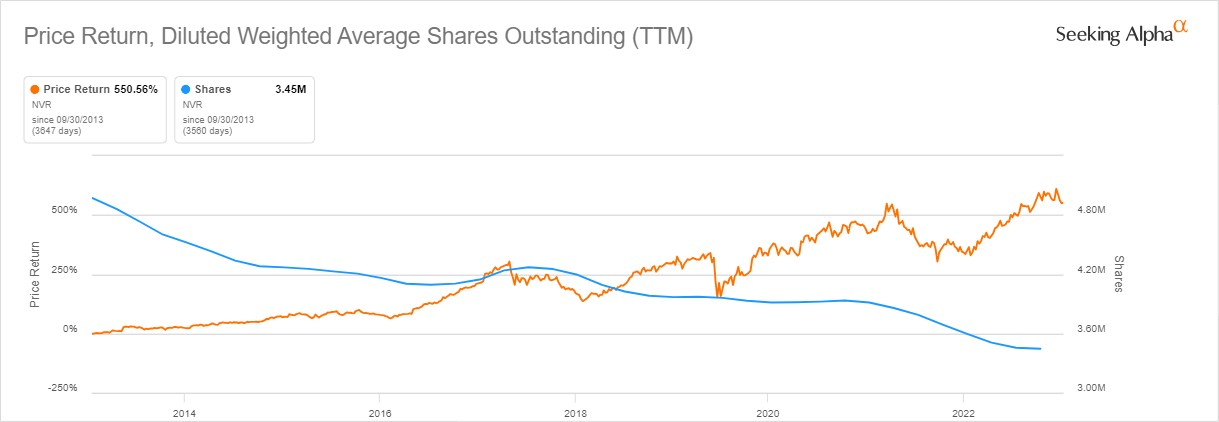

NVR has low Capex since it leases its offices and production facilities and it has limited ability to reinvest its free cash flow into the business. During the last 10 years, it has reinvested an average of 22.4% of its cash from operations into the business and has spent $7.3B on share repurchases (101% of its cash from operations). The total diluted shares outstanding have reduced from 4.86MM in 2013 to the current 3.46MM in the 2Q of 2023, eliminating almost 29% of its outstanding shares, which has boosted its share price.

{kind=link}

In my opinion, this is a top capital allocation, where management deploys the capital into the business without forcing too much geographical expansion to maintain its competitive advantage and leading market position while returning the remaining free cash flow through share buybacks, a more efficient way compared to dividends when seeking to compound.

Housing market shortage

To analyze the current state of the housing market in the U.S., we need to take a look at the rate of household formation and the supply of new homes.

In the U.S., there are currently 130.2MM households ( August 2023, Yardeni Research, Inc. ) growing at an average rate of 1.3% annually, which would correspond to 1.69MM new households per year.

This data is similar to the 1.62MM new units needed per year calculated on a Freddie Mac study about the housing supply, which includes 1.1MM for new household formation, 0.3MM to replace depreciated existing homes, 0.1MM for second homes, and 0.1MM for vacancy.

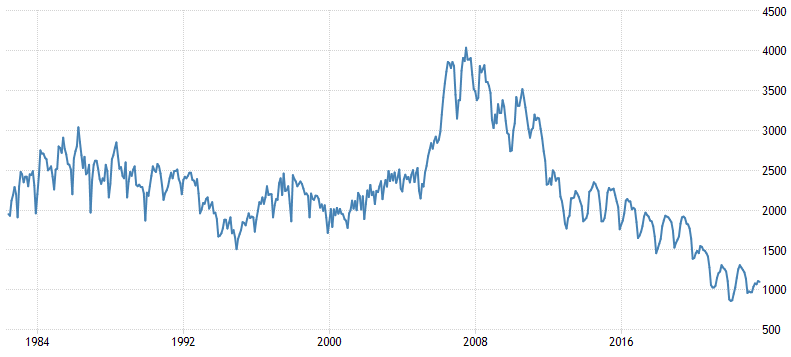

If we take a look from a longer time-frame perspective, since 1959 until the great financial crisis, there have been only two years of housing starts below 1MM units , and since then there have been six. The market has been balancing the over-supply during the 1998-2007 upcycle, but the main question to answer would be, is there a shortage in the U.S. housing market?

During the 1998-2007 period, the number of household formations totaled 14.99MM , while the supply of new houses was 17.18MM , giving us an over-supply of 2.19MM homes.

From 2008 to 2022, the number of new homes averaged 1.06MM homes delivered per year, way below the average of 1.6MM of new homes needed, with a deficit of 0.44MM homes per year. The over-supply of 2.16MM homes had been already covered in the next 5 years, and from 2014 until 2022, we accumulated an under-supply that totaled approximately 3.5MM homes and the housing inventory has fallen to an unprecedented low level.

Tradingeconomics.com (Data from the National Association of Realtors)

{kind=link}

In the most recent report from the U.S. Department of Housing and Urban Development for August 2023 building permits were at 1.54MM, meeting the current long-term average demand for new housing.

The current situation would require home builders to deliver a higher number of new homes per year to cover the under-supply, otherwise, home prices would increase significantly, as we have recently seen.

From 2001 until 2Q of 2023, home prices have been increasing at an average of 2.8% CAGR, but prices increased significantly faster from 2019 at a 6.8% rate. Even if inflationary pressures played their role, I believe the current state of the housing market could benefit homebuilders over the upcoming years.

From a short-term perspective, higher interest rates would intuitively be seen as negative for homebuilders because of lower demand from new buyers, but this also limits current homeowners from selling their homes that were bought at lower interest rates.

If we take into account that current homeowners are not incentivized to sell their homes, and new families are formed every year, the most likely outcome would be higher prices, even in a recession.

As soon as interest rates go down, new home supply should increase to meet the under-supply accumulated during the last years. Current expectations from the Federal Reserve are that rates will stay at current levels for some time, declining to 4% in 2025 and 2.9% in 2026, but this can change quickly based on the economy's performance, which for now seems to be strong.

Expected growth

I don't expect new homes delivered to grow fast in the short term since 30-year fixed loans are currently at over 7% , but I also expect the prices to keep at current levels or grow for the next years.

This is the trend we have seen the last quarter , with settlements decreasing by 13% when compared to the 2Q of 2022, but prices at the same levels. The good news is new orders increased by 27% and the cancelation rate was 11%, compared to 14% a year ago.

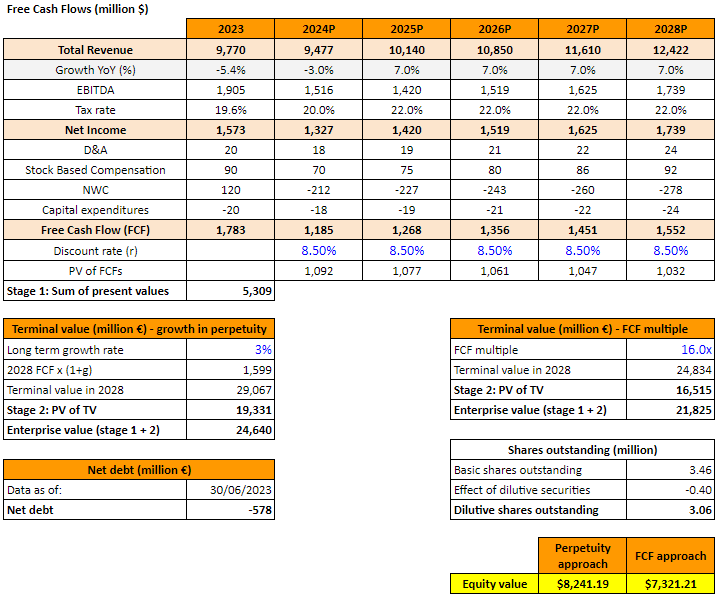

Since the second half of the year used to have higher revenues and new orders are increasing, I agree with current estimates of revenue at $9.7B for 2023, a 5.4% decrease from 2022. For 2024, I expect revenues to decrease by 3% at $9.4B, which is more pessimistic compared to analyst expectations of $10.37B. I expect operating margins to decrease from 19.5% in 2023 to 14% margin from 2025 onwards and net income margins at 13% because of lower administrative expenses as the company becomes larger, continuing with last decade's trend.

From 2025, I expect revenues to grow at 7%, above its historic average based on the current under-supply that needs to be covered. I used an 8.5% discount rate, given its 3% cost of debt, a 10% cost of equity, a 22% tax rate, and 20-80 weight for debt and equity. The long-term growth rate I expect is at 3%, lower than the average historical inflation rate and assuming there isn't new household formation, which I believe is a really conservative scenario.

In my base case scenario, I already included all exercisable shares from management and I assume the company is reducing the 4% annually, which already includes the dilutive effect from management stock options.

{kind=link}

From a terminal value perspective, my fair price would be $8,241, while from an FCF multiple perspective at 16x LTM FCF, it would be $7,321. The average fair price is $7,781, presenting a 30% upside from current prices.

When applying the same model but with a 10% net income margin, which I believe would be the low end of a recessive cycle, the fair value would be at $5,715, limiting the downside at current prices and just overpaying by 5%. In that scenario, net income would be at $0.95B in 2024 and $1.01B in 2025.

Valuation

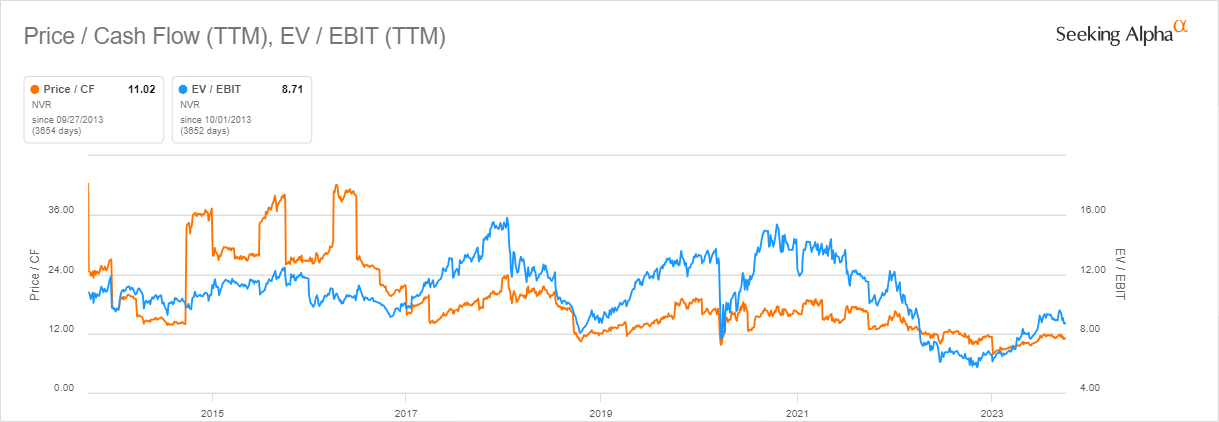

NVR is currently trading at 11x LTM FCF/EV and 8.7x EBIT/EV, but I believe this is not representative since 2022 was an abnormal year from a margin and FCF perspective.

{kind=link}

In my opinion, it would be more accurate to assess the current valuation with the next twelve months free cash flow, and it would be currently trading at about 12x-15x, depending on using my estimates presented on the model or consensus estimates, which I believe are a little optimistic. NVR is trading below its next twelve months FCF/EV average of 16.8x for the last 10 years.

Risks

The main risk I see from NVR would be a strong economic crisis with a fast increase in unemployment while interest rates do not come down because of high inflation.

This scenario could be caused by energy price increases or a shortage of goods that limits NVR's ability to deliver new homes.

This would also leave NVR with some mortgages pending for sale that could decrease in price, the company currently owns $438MM in mortgages for sale. These mortgages could cause losses if interest rates continue to increase since the company could not be able to match the interest rates committed with its customers at origination with interest rates paid by third parties that buy those loans from NVR.

If interest rates come down during a recession, some of the pain from higher unemployment could be compensated by increasing new orders coming from the under-supply accumulated during the last years.

Conclusion

Even though there are some risks if a hard landing is to come, and NVR is operating on a cyclical business, I believe the quality of the company, its controlled risk structure, and the current discount more than compensate for these short-term risks.

I see a risk-reward asymmetry given the current shortage in the housing market in the U.S. and I believe current prices are already taking into account a decrease in revenues and margins.

In a base case scenario, my fair price is currently at $7,781, representing a 30% upside and that is why I rate NVR stock as a buy.

For further details see:

NVR: Controlled Risk With Potential Upside