PAGP - NXG: This CEF Can Help You Play The Energy Transition And Get A High Yield

2023-03-15 19:02:41 ET

Summary

- It is difficult to get exposure to renewable or clean energy companies and still get a high yield.

- NXG NextGen Infrastructure Income Fund invests in a portfolio of both traditional and renewable energy companies in an attempt to provide its investors with an incredibly high yield.

- The NXB closed-end fund's portfolio has changed a lot over the past several months as it has shifted a great deal toward traditional energy companies.

- The 8.64% distribution appears to be sustainable based on the fund's current investment performance.

- The fund is trading at an incredibly attractive discount to the net asset value.

We spend a great deal of time discussing traditional energy companies such as midstream companies and high-yielding upstream companies here at Energy Profits in Dividends. The biggest reason for that is that these companies represent some of the few opportunities available today to earn the 7% yields that we like. However, numerous politicians, activists, and many others keep discussing how fossil fuels will be going the way of the dinosaur in the near future. Although that is highly unlikely for reasons that we have discussed numerous times, it still makes sense to include exposure to transitional energy firms and renewable companies in your portfolio.

There are, unfortunately, few opportunities to accomplish this now that former opportunities such as Brookfield Renewable Partners ( BEP ) or NextEra Energy Partners ( NEP ) do not offer the high yields that they once did. As of the time of writing, each of these partnerships is yielding less than 5.20%, which is not enough of a premium over a money market fund to properly reward investors for the additional risk. Thus, we are left somewhat wanting opportunities to earn a high yield from renewable energy companies.

Fortunately, there are some ways to invest in the energy transition and still earn a yield in excess of 7%. One of the best ways to do this is to invest in a closed-end fund, or CEF, that specializes in the clean energy sector. These funds are often overlooked, which is unfortunate as they enjoy the benefits that come with a professional management team and can, in many cases, deliver a much higher yield than the underlying assets actually possess.

In this article, we will discuss the NXG NextGen Infrastructure Income Fund ( NXG ), which is one fund that falls into this category. As of the time of writing, this fund yields an impressive 8.64%, which is much closer to the yields that we like to see on the investments that we discuss here. I have discussed this fund before, but that was nine months ago so obviously, a great many things have changed. This article will therefore focus specifically on these changes and, of course, provide an updated analysis of the fund’s financial report. Let us proceed and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage , the NXG NextGen Infrastructure Income Fund has the objective of providing its investors with a high level of total return. This is hardly surprising for an equity fund, which this one certainly qualifies as since 92.08% of its assets are invested in common equity:

CEF Connect

The reason why a focus on total return is not surprising is that common stock is by its very nature a total return vehicle. After all, we generally purchase common equity with the desire to earn income through dividends as well as getting capital gains as the issuing company grows and prospers. With that said, this fund does specify that it aims to deliver that total return primarily through current income. That would imply that it mostly purchases high-yielding assets, but as was already mentioned, there are scant few of these in the renewable energy sector. Despite the name though, this fund does not specifically invest in renewable energy and related companies. Rather, the fund states that it invests in four types of things:

- Energy Infrastructure Companies

- Industrial Infrastructure Companies

- Sustainable Infrastructure Companies

- Technology and Communications Infrastructure Companies.

This certainly looks like a far cry from a renewable energy fund. In fact, this description would include things such as midstream companies, railroads, and telecommunications companies, along with renewable energy yieldcos like NextEra Energy Partners. However, the fund does state that less than 25% of its assets will be invested in master limited partnerships, so its exposure to yieldcos is likely to be rather limited. This is unfortunate because master limited partnerships typically have much higher yields than corporations, so the fact that the fund limits its investments in these firms means that its income will be lower than it could otherwise be.

Despite that restriction, we do see a number of master limited partnerships among the fund’s largest positions:

Cushing/NXG

MPLX ( MPLX ), NuStar Energy ( NS ), Energy Transfer ( ET ), Plains GP Holdings ( PAGP ), and Crestwood Equity Partners ( CEQP ) are all master limited partnerships. These five partnerships alone are 28.05% of the fund, which exceeds the 25% limit that the fund states on its own webpage. This is not really a problem as all five of those companies are quite solid investments today, although NuStar Energy and Plains GP Holdings do not have particularly strong forward growth potential. These companies have very high yields, and this will help to offset the low yields from New Fortress Energy ( NFE ) and similar companies that account for the remainder of the portfolio.

It is also interesting to see Crestwood Equity Partners here, as that is not a company that we usually see among the largest positions in the fund. Indeed, as some people on Seeking Alpha have commented, that company almost seems to be the forgotten gem of the industry. The fact that it has strong exposure to natural gas likely explains its presence here since natural gas demand is actually climbing as renewable energy becomes more popular due to the need to have something reliable and clean to supplement the intermittent nature of wind and solar energy.

There have been surprisingly few changes here since the last time that we looked at the fund. In fact, the only significant change is that NextEra Energy Partners was replaced with New Fortress Energy in the fund’s largest positions. The remainder of the changes were simply weighting changes, which can easily be explained by one asset delivering better market performance than another.

The fact that there have been so few changes since June 2022 could lead one to believe that this fund has a very low annual turnover. That is certainly not the case though, as the NXG NextGen Infrastructure Income Fund had an annual turnover of 124.56% last year. That is, without a doubt, one of the highest turnovers that I have ever seen a closed-end fund possess. The reason why this is important is that it costs money to trade stocks or other equities, and these costs are billed directly to the shareholders of the fund.

This creates a drag on the fund’s performance that makes management’s job more difficult. After all, the fund’s managers have to generate sufficient returns to cover these additional costs and have enough left over to provide the shareholders with an acceptable return. This is a difficult task that very few management teams manage to accomplish consistently, which results in actively-managed funds typically underperforming index funds. There is not really a good index to use for a point of comparison when it comes to this point, but its long-term performance does leave a lot to be desired:

Cushing/NXG

The biggest thing that I notice here is that the fund had a negative total return over the past twelve years. This is quite different from the Cushing MLP & Infrastructure Total Return Fund ( SRV ) that we discussed this morning as that fund managed to deliver a very strong positive total return over the period. This is probably because the other fund is more heavily focused on traditional energy and less so on renewables. The renewable energy sector benefitted a lot from all the free money and excess liquidity sloshing through the economy in 2021 but as that dried up, the sector collapsed, but fossil fuel companies did quite well.

We can see here that sustainable infrastructure companies account for 27.67% of this fund:

Cushing/NXG

I will admit that the allocation to traditional energy companies is higher than I expected to find. It is not particularly surprising though, given that high annual turnover. After all, during 2022, it was a very profitable play to sell renewable energy companies with inflated valuations and buy fossil fuel producers and midstream companies. The fund could very well be doing that, especially since the allocation to traditional energy is a lot higher than it was at the end of March 2022.

This could be a good place to be since much of the traditional energy sector still appears significantly undervalued. I pointed this out in a recent blog post . The fund’s management appears to agree and has positioned itself to take advantage of this. Investors should appreciate this, particularly considering the recent Goldman Sachs (GS) prediction that there will be a crude oil shortage in 2024 that will have a very positive effect on prices.

Leverage

In the introduction to this article, I stated that closed-end funds like the NXG NextGen Infrastructure Income Fund have the ability to employ certain strategies that boost their yields beyond that possessed by the underlying assets. One of the strategies that are employed by this fund to accomplish this is the use of leverage. In short, the fund borrows money and uses that borrowed money to purchase various energy and infrastructure assets. As long as the purchased assets have a higher return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective return of the portfolio. The fund is able to borrow money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This is something that could have proved problematic for the fund last year as previously high-flying renewable energy stocks collapsed. As such, it is important that we ensure that the fund is not employing too much leverage since that will expose us to too much risk. I typically do not like to see a fund’s leverage exceed a third of its assets for this reason. Fortunately, this fund is fulfilling that requirement. As of the time of writing, its levered assets comprise 25.13% of the portfolio. Thus, it appears that this fund is currently striking a reasonable balance between risk and reward.

Distribution Analysis

One of the biggest advantages that many midstream and traditional energy investments have today is that they boast remarkably high yields. This also applies to companies like Atlantica Sustainable Infrastructure plc ( AY ), which is the largest position in the fund and yields a respectable 6.40% today. This fund invests in a portfolio of such companies and then applies a layer of leverage to boost the effective yield. As such, we can guess that the NXG NextGen Infrastructure Income Fund will have a similarly high yield.

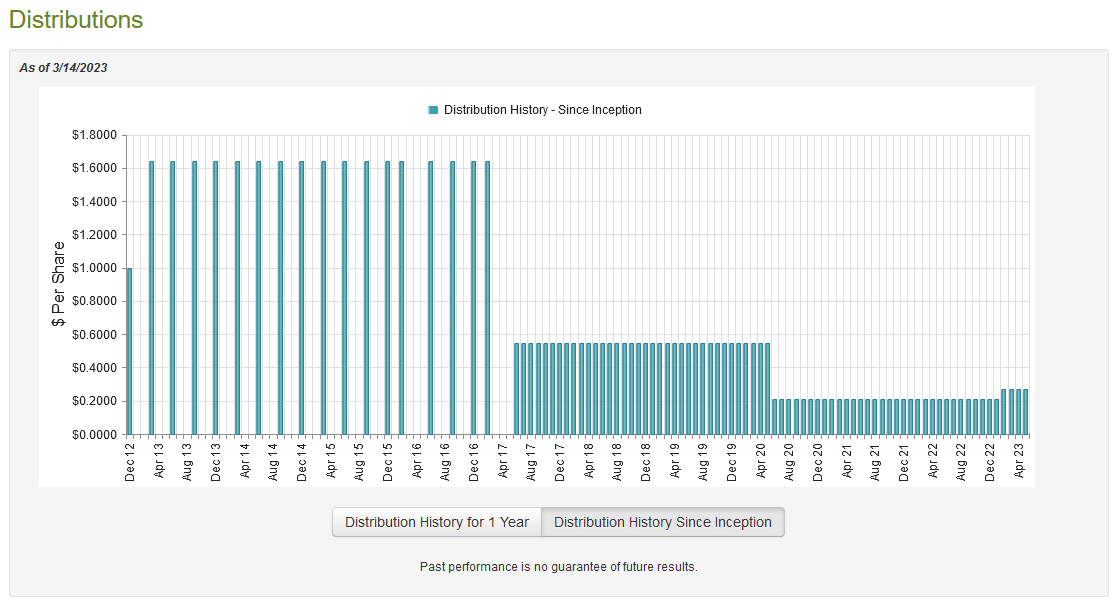

This is certainly the case as the fund pays out a monthly distribution of $0.27 per share ($3.24 per share annually), which gives it an 8.64% yield at the current price. Unfortunately, the fund’s past distribution does not engender a great deal of confidence as it has varied quite a bit over the years:

{kind=link}

The fact that NXG NextGen Infrastructure Income Fund was forced to cut its distribution in 2020 is not particularly surprising. As many readers likely recall, that was a time of great turbulence for the traditional energy sector. In April 2020, crude oil prices went negative but other than that we saw the pandemic-related lockdowns cripple the demand for crude oil, which resulted in low prices. Natural gas prices also fell, but not as severely. The industry generally found itself cut off from raising capital in the markets, so it was forced to reduce shareholder distributions and rely entirely on internal funding.

Although things have improved somewhat, the industry still faces difficulty raising capital traditionally due to environmental, social, and governance policies at many asset managers and pension funds so it has still not returned shareholder returns to the levels that it once had. The fund naturally had to react to this by cutting its own distributions since it is never sustainable to pay out money that the fund did not actually earn.

The fund’s past is not really that important to anyone buying today, though. This is because a buyer today will receive the current distribution and the current yield. Thus, the most important thing is how well the fund can cover its current distribution. Fortunately, we have a very recent document that we can consult for this purpose. The fund’s most recent financial report corresponds to the full-year period that ended on November 30, 2022.

This is obviously a much more recent report than we had available the last time that we looked at the fund, which is nice because 2022 was an interesting year for both the traditional and renewable energy industries and this report should give us a good idea of how it negotiated that environment. During the full-year period, the NXG NextGen Infrastructure Income Fund received total dividends and distributions of $8,843,371 along with $1,046,561 in interest from the assets in its portfolio.

However, a large proportion of this was distribution payments from master limited partnerships, so it does not count as taxable income. The fund actually reported a total investment income of $3,767,962 during the period. It paid its expenses out of this amount, which left it with a net investment loss of $160,138 during the period.

In other words, the fund’s net investment income was insufficient to cover its expenses. The fund still paid out $6,656,226 in distributions, however. At first glance, this could be concerning as the fund’s net investment income was nowhere close to enough to cover the payout.

However, the fund received $6,122,984 in distributions from master limited partnerships during the period. That was enough to completely cover the net investment loss and most of the distributions, which certainly helps a lot. The fund also managed to achieve capital gains during the period as it reported net realized gains of $11,907,876 over the year. While that was offset by $1,194,557 net unrealized losses, the fund still saw its assets increase by $3,896,955 after paying the distribution. Clearly, it did manage to cover the distribution with money left over. Overall, things do look just fine here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund, the usual way to value it is by looking at the net asset value. The net asset value of a fund is the total value of the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. As is the case with most energy infrastructure funds, this one is currently selling for substantially less than it is worth.

As of March 14, 2023 (the most recent date for which data is available as of the time of writing), the NXG NextGen Infrastructure Income Fund had a net asset value of $50.73 per share but the shares actually trade for $36.10 per share. This gives the fund’s shares a discount of 28.84% at the current price, which is an incredibly large discount, to say the least. This discount is much better than the 20.56% discount that the shares have averaged over the past month, so the price certainly looks attractive today.

Conclusion

In conclusion, the NXG NextGen Infrastructure Income Fund offers an attractive way to invest in the energy transition and renewable sectors while still earning a very high yield. Although the fund is currently weighted towards traditional energy sources, it does still have a sizable exposure to renewables and frankly, traditional energy sources are a better investment right now anyway. The fund’s 8.64% appears to be sustainable based on its performance and the price cannot really be beaten. Overall, NXG NextGen Infrastructure Income Fund might be worth considering for a portfolio today.

For further details see:

NXG: This CEF Can Help You Play The Energy Transition And Get A High Yield