PAI - NXP And NUW: 2 Higher Quality Muni Choices

2023-05-01 15:58:58 ET

Summary

- NXP and NUW are both municipal bond funds focused on higher quality portfolios.

- The overwhelming majority of their portfolios are invested in investment-grade municipal bonds.

- At the same time, they also operate with no or low leverage in their portfolios.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on April 17th, 2023.

The general idea about investing in municipal bonds is safety and tax-free income. When combining muni bonds with a closed-end fund, we often take the risk up due to adding generous portions of leverage. Additionally, the closed-end fund wrapper also subjects investors to discounts/premiums. The latter, the discounts/premiums mechanics, I believe are something to exploit.

The leverage being utilized is more of an investor choice. Muni bonds are often seen as incredibly safe, so adding leverage generally isn't too much of a problem until rates fly higher, as we saw in the last year.

With muni bonds, you often get long maturities, translating into long durations. Duration is a measure of interest rate sensitivity. It's reflected in the number of years, and the higher this number, the higher the sensitivity and the lower the number, the less interest rate sensitive an investment should be.

This is also something that investors can potentially exploit at this time. While interest rates were rising rapidly, and we saw many muni funds and really fixed-income funds across the board, we could now potentially play it to the upside. The upside would come when rates are cut, and while it isn't exactly predicted when that will happen precisely, it is expected to be a question of "when" and not "if."

What I'm ultimately getting at is this is another article on "choosing quality." We explored two funds previously when looking at Nuveen Quality Municipal Income Fund ( NAD ) and Western Asset Investment Grade Income Fund ( PAI ). NAD is another muni fund that employs leverage, and PAI is a fund focused on investment-grade debt but is not leveraged.

Today, I wanted to take a look at two more muni funds. In this case, neither muni fund utilizes elevated levels of leverage. Instead, they limit any potential leverage to 10% effective leverage through tender option bonds. That is a low amount; for some context, NAD is at nearly 40% leverage. The 10% is also listed as a limit. Both are even well below that amount at this time. The two funds are Nuveen Select Tax-Free Income Portfolio ( NXP ) and Nuveen AMT-Free Municipal Value Fund ( NUW ).

For some color on the performance of these funds relative to their leveraged cousin NAD, we can take a look at the charts below. This shows the total share price return in the top panel and the total NAV price returns in the bottom. These results are from the beginning of 2022 to April 14th, 2023.

YCharts

While rising interest rates had a negative impact on all three of these funds in the last 15 months, we can see that no/low-leveraged NXP and NUW saw significantly fewer losses, as expected. Additionally, 2023 hasn't been terrible for these funds due to yields dropping even while the Fed continues to hike and could have one or two more hikes. In this case, yields are dropping; it would seem, in anticipation of expected rate cuts in the future coming sooner than expected. The bank collapses kind of showed the Fed that things were starting to break, and they could work as a bit of an interest rate hike on their own to make financial conditions tighter.

Before discussing some of the basics for both of these funds, more specifically, it might be important to note that Nuveen is going through a bit of a reorganization phase. There were recently three other muni funds that completed mergers from this fund sponsor. That didn't include either of these two names, but both NXP and NUW have been funds that, in the past, have been impacted by reorganizations.

Nuveen Select Tax-Free Income Portfolio

- 1-Year Z-score: 1.61

- Premium: 0.21%

- Distribution Yield: 4%

- Expense Ratio: 0.25%

- Leverage: 0.00%

- Managed Assets: $669 million

- Structure: Perpetual

NXP's investment objective is "current income exempt from regular federal income tax, consistent with preservation of capital." In attempting to achieve this, the fund will:

Invest at least 80% of its managed assets in municipal securities rated investment grade at the time of investment, or, if they are unrated, are judged by the manager to be of comparable quality. The Fund may invest up to 20% of its managed assets in municipal securities rated below investment quality or judged by the manager to be of comparable quality, of which up to 10% of its managed assets may be rated below B-/B3 or of comparable quality. The Fund may invest in inverse floating rate municipal securities, also known as tender option bonds. The Fund's use of tender option bonds to more efficiently implement its investment strategy may create up to 10% effective leverage.

Before even touching on anything else on this fund, that 0.25% expense ratio is not an error. This is the lowest expense ratio I've ever seen in a CEF. This is probably because I hadn't spent a lot of time focusing on non-leveraged funds; in particular, I don't focus on muni funds. I've just now started paying more attention as they've plummeted due to rising interest rates. That data is straight from the fund's website.

{kind=link}

The last annual report actually reinforces this, too, as the expense at that time came to 0.29%, with most years reflecting an expense ratio of 0.26%. This very low expense ratio can be helpful when investing in something like munis that aren't necessarily the highest-yielding instruments. A lower expense ratio can leave more returns left over for the actual shareholders.

The 80% is the minimum or the "at least" level. In practice, the fund is invested 93.2% in BBB or higher-rated debt, with the largest portion being AA and A rated debt. That's some high-quality debt, and it can be beneficial when a potential recession is on the horizon.

NXP Credit Quality (Nuveen)

Of course, for the benefit of such high-quality muni debt, the issuers can extend out their maturities. In this case, NXP's effective maturity is 14.03 years. The average effective duration of the portfolio is 7.44 years. That means that for every 1% change in interest rates, NXP's underlying portfolio should move by 7.44%.

The largest issuer of bonds they are holding comes out of California. So while it is a national muni bond fund, Californians may benefit even further from this fund as they can also be eligible for tax-free state income.

NXP Top State Exposure (Nuveen)

The average bond price as a percentage of par came to $85.61. That means the fund's fairly shallow discount is on top of discounted muni bonds. This is worth pointing out; NXP isn't the most heavily discounted fund available, so in that case, that isn't one of its stronger selling points. Instead, the non-leveraged higher quality muni portfolio heading into a potential recession that could see interest rate cuts would be its strongest selling point.

Of course, knowing if NXP would ever realize that discount on its underlying portfolio is impossible. The fund is actively managed, so they are always selling and buying, but the general idea is that no matter what they switch to in terms of muni holdings, it should benefit from reduced rates. Even if rates stabilize, that can be good for NXP and NUW.

The fund's distribution rate comes out to 3.99%. One would have to calculate their own taxable equivalent yield based on their tax bracket. However, for an idea for those that are joint filers with a 24% federal tax rate, the equivalent taxable distribution yield would move up to 5.25%.

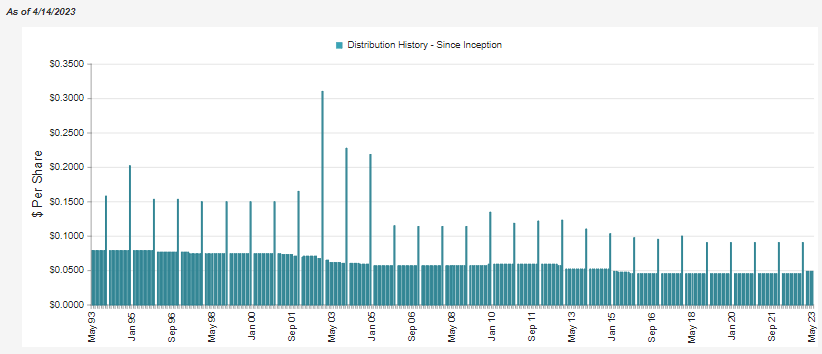

Many muni funds have been cutting their distributions since their borrowing costs are rising. That hasn't been the case with NXP. In fact, they just raised their distribution by a touch heading into 2023.

{kind=link}

Longer term, the trend has been lower, but that's expected as the last decade-plus has seen interest rates pegged at nearly 0% through this entire period. As bonds were being issued and maturing through the 90s and early 2000s, the yields they could invest in started decreasing.

As expected, the fund's distributions were largely classified as tax-exempt income in the prior two years.

{kind=link}

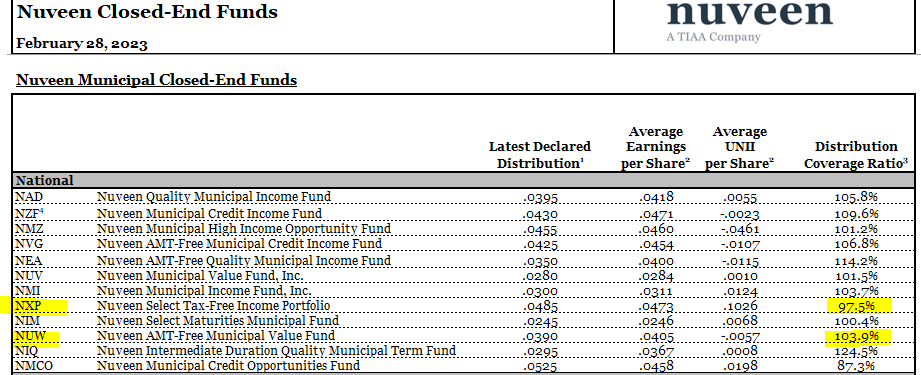

The latest UNII report for the period that ended February 8th, 2023, actually shows that NXP had a lack of distribution coverage. NUW was fully covering their distribution. For NXP, they still had quite a bit of UNII built up in their fund.

{kind=link}

As these reports usually do, the average earnings per share, in this case, is the fund's last three months of earnings averaged out. That gives us a bit of a snapshot of the fund's earnings, but it can still lead to some variability. Most muni funds and bonds generally pay their interest payments semi-annually. In the case of NXP and NUW, they even have some exposure to zero coupon bonds that pay no interest but are bought at a discount.

Nuveen AMT-Free Municipal Value Fund

- 1-Year Z-score: -0.92

- Discount: -8.71%

- Distribution Yield: 3.51%

- Expense Ratio: 0.62%

- Leverage: 0.74%

- Managed Assets: $269.862 million

- Structure: Perpetual

NUW's investment objective is "current income exempt from regular income taxes, and its secondary objective is to enhance portfolio value and total return." In an attempt to achieve this, the fund will invest in:

Municipal securities that are exempt from federal income taxes, including the alternative minimum tax ((AMT)). The Fund invests at least 80% of its managed assets in municipal securities rated investment grade at the time of investment, or, if they are unrated, are judged by the manager to be of comparable quality. The Fund may invest up to 20% of its managed assets in municipal securities rated below investment quality or judged by the manager to be of comparable quality, of which up to 10% of its managed assets may be rated below B-/B3 or of comparable quality. The Fund may invest in inverse floating rate municipal securities, also known as tender option bonds. The Fund's use of tender option bonds to more efficiently implement its investment strategy may create up to 10% effective leverage.

With NUW, we have significantly similar language in the makeup of the fund's investment policy. There are some subtle differences, with the most specific one coming in the form of looking for AMT-free income as well. NXP listed that around 10% of its portfolio was income subject to AMT. In the case of NUW, they list that 0.00% is subject to AMT.

Additionally, NUW has a higher expense ratio and has a touch of leverage at this time. It's a smaller fund than NXP, so that could be some of why they choose to have a higher management fee. The actual "other expenses" for running the fund are exactly the same as in the latest reporting.

{kind=link}

Despite having a sliver of effective leverage, they hadn't reported any leverage expenses in the annual expense ratio. However, it would be safe to assume that it could be another few basis points higher.

{kind=link}

The credit quality of NUW is largely similar to NXP's as well. They carry 90.2% of their portfolio listed as investment-grade quality. The AA and A rated debt are the largest contributors to the fund's composition.

NUW Credit Quality (Nuveen)

The top state once again belongs to California, but Texas also makes up a meaningful allocation, followed by Illinois and New Jersey. In this case, it would appear the NUW is a bit more diversified in being spread across more states, with less of a concentration in the top allocation.

NUW Top State Exposure (Nuveen)

One selling point for NUW over NXP is that the fund carries a deep discount, which can be another potential trigger for higher returns. In this case, the fund's average bond price as a percentage of par comes to $91.83. So it is less discounted than NXP's portfolio, but at the actual fund level, NUW is the clear winner. All else being equal, a discount contraction would be expected in NUW that could provide meaningfully higher upside moves over NXP.

NUW's portfolio is slightly longer in terms of its length of maturity at 15.74 years on average. That ticks the effective duration a touch higher as well to 7.87 years.

We saw above that NUW was covering its distribution, so perhaps unsurprisingly, they also raised their payout recently. Once again, we see the longer-term trend lower in distributions for the same reason as touched on above for NXP.

{kind=link}

The fund's distribution classification was primarily tax-exempt income, as expected once again in the prior two years. However, the fund also had achieved some sizeable long-term capital gains in the prior year that they distributed out as a year-end capital gain.

{kind=link}

This could be seen as a negative if investors held a large position and then received a large capital gains tax bill. The general idea of investing in muni bonds and funds is to minimize taxes, particularly for those in higher income tax brackets. Long-term capital gains are often tax-friendlier, but even at the lower relative rates to ordinary income could be a bit unexpected.

Conclusion

NXP and NUW have outperformed their leveraged cousins since interest rates were rising. If rates reverse, the reverse could become true where their leveraged cousins would become the better performers. Still, adding liberal amounts of leverage to muni funds takes some of their appeals away as being relatively less volatile. By focusing on non/low-leveraged funds such as NXP and NUW, you get left with being able to exploit the discounts/premiums on the funds and within their portfolios, taking away some of that volatility. At the same time, investors can collect fairly generous taxable equivalent distribution yields.

For further details see:

NXP And NUW: 2 Higher Quality Muni Choices