LIN - NZS Capital Growth Equity Fund Q4 2022 Update

Summary

- NZS Capital is an investment company focused on adaptable, innovative businesses that work toward maximizing non-zero-sum (NZS, or win-win) outcomes for their investors, customers, employees, society, and the global environment.

- The narrowing of economic and rate expectations could be a positive backdrop for equities in 2023.

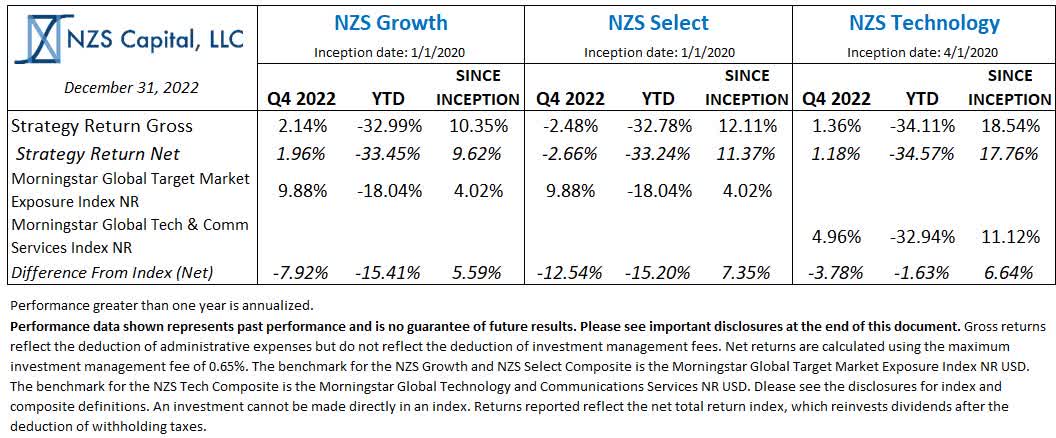

- The growth strategy was up during the period but meaningfully lagged its index.

- Bypopulating a portfolio with resilient, adaptable companies, able to weathereconomic storms and take advantage of turbulence to gain economic share, youcan insulate yourself from the inevitability of predictions gone awry.

Q4 2022 Update

{kind=link}

Market Overview

Interest rate policy stole the spotlight in 2022, and, while central government plans are far from settled, the range of outcomes may be coming into focus. Decades of free money may give way, for a time, to higher rates and sustained inflationary pressure. Industries, companies, and investments that benefited from cheap money and low rates must now demonstrate they can also generate cash in today’s environment. At the same time, businesses must evaluate the post-pandemic world to determine to what extent lockdown-influenced behaviors will persist.

This narrowing of economic and rate expectations could be a positive backdrop for equities in 2023. However, it may be a while before stock prices accurately reflect underlying fundamentals, and there may be some casualties along the way. Our view is that most digitalized industries are governed by power laws, where a handful of participants garner the lion’s share of profits. In 2023, we could see winning companies pull even farther ahead as cash-strapped businesses falter. We also believe supply chains will continue to de-globalize as companies and countries become more concerned about access and sovereignty rather than efficiency. Reshoring could provide a significant economic engine, along with inflationary pressure – at least until AI-driven automation and robotics sufficiently mature to provide a disinflationary counterweight.

We have crafted our portfolio to reflect our view that solid company fundamentals will be even more critical in times of heightened uncertainty and economic stress. Specifically, we have added adaptable companies likely to prove resilient in an environment where money is no longer free. Overall, however, our broad predictions regarding the overarching shift of the global economy from analog to digital remain unchanged. Our meaningful exposure to semiconductors and software in the portfolio reflects our view that these companies are mission critical components of every sector in the Information Age.

With digitalization comes transparency, and companies risk losing constituents if they attempt to extract exorbitant tariffs from consumers, suppliers, or the environment. As such, companies with the best value propositions will prove the most attractive over the long term. After the macro-driven 2022, we see a world in 2023 where these factors matter – as they should.

Performance Review

The market rallied during the fourth quarter, a positive end to what was a strongly negative year. Sectors not normally associated with growth stocks, such as materials, utilities, financials, and industrials, did well. Traditional growth areas, such as information technology and communication services, were positive but lagged other sectors. Healthcare, which spans growth and value, did well. Unsurprisingly, therefore, value indices outpaced growth indices globally. Overall, markets remain transfixed by the economic overhang of high inflation and higher rates. China’s reopening gave a boost to its local market as well as to many companies with exposure there.

The growth strategy was up during the period but meaningfully lagged its index. Sector exposure hurt relative performance, with information technology and communication services comprising the two largest concentrations in the portfolio and the worst performing sectors within the index. At the same time, relative performance suffered from the underweights in industrial and financials, two areas typically not large in this portfolio. Stock selection also hurt on a relative basis. Amazon ( AMZN ) fell sharply and hurt relative and absolute performance. Salesforce Inc. ( CRM ) was only modestly down but, as a large position, detracted from performance. Tesla ( TSLA ) also fell dramatically, impacting overall performance despite being a small position. The portfolio benefited from strong moves in Linde in the industrial sector and Intuitive Surgical ( ISRG ) in the health care sector.

We added a few companies with attractive fundamentals to the portfolio, including Progressive ( PGR ), NextEra Energy ( NEE ), and Autodesk ( ADSK ). We sold a few stocks that had been large positions, including Microsoft ( MSFT ) and Paramount ( PARA ). Some of the portfolio sells and trims, such as Paramount, reflect some deterioration in fundamentals and a reassessment of the business’ outlooks. We used the period of market disruption to focus the portfolio where we saw more attractive ranges of outcomes relative to valuations. As macro uncertainties persisted, we considered how to make the portfolio less sensitive to market fluctuations by widening the scope of investments. For example, Progressive, a leading insurance firm using data to offer better products to consumers, is an attractive holding with a much different exposure to interest rates than many technology companies.

How to be wrong

Raise your hand if five years ago you predicted a global pandemic, a return to high inflation and interest rates, a reversal of globalization, or Elon Musk buying Twitter. Anyone? Keep it raised if you predicted how these factors would intersect and drive behavior changes. Ok, put your hands down. We do not believe you.

A key characteristic that defines a complex adaptive system, like the world economy, is emergent behavior. When isolated or formerly unknown groups of agents interact, we frequently see entirely new behaviors emerge. These behaviors are impossible to predict. They do not result from the sum of the parts in the system but, rather, from the relationships within the system, a much more complicated algorithm.

We believe that, during these periods of pronounced emergence, focusing on adaptation to changing conditions is more important than trying to predict the future. Bold predictions intrigue investors and perhaps drive clicks, but they are not valuable. We know investing entails some degree of prediction; however, we start with the unconventional attitude that predictions are risks, not strengths, and we try to keep our predictions as few and as broad as possible, paying close attention to the potential range of outcomes that each prediction entails. While most managers focus on how right they can be, our goal is to equally prepare for how wrong we can be.

Our process, therefore, is to consider broad predictions. Sometimes these seem so straightforward they sound silly when said out loud.

- Electronics are likely to push deeper into the world

- Companies are likely to use more software to automate processes

- Innovation in the digital world will increasingly spill into the physical world

- The world wants to decarbonize

- Payments will continue to shift to digital

The benefit of broad predictions with staying power is that they clarify where we should spend our time.

Put simply, we only spend time where we believe the knowledge we accumulate can compound. Compounding knowledge is one of the most important aspects of being a good investor. We ask: Based on our broad predictions, is this an area of study that is likely to be even more relevant ten years from now? If so, we dig in and make sure we have portfolio exposure to well positioned companies poised to take advantage of an uncertain future.

For example, recently we have been spending more time on industrial gases. This area entails several of our broad predictions, such as electronics pushing deeper into the world, decarbonization, and innovation moving into the physical world. The companies leading the industry also pass our essentialness test: If the company disappeared, would it matter? After decades of consolidation, three industrial gas companies control 85% of the world’s industrial gas supplies: Linde ( LIN ), Air Liquide ( AIQUF ), and Air Products ( APD ). Rising geopolitical tensions are leading to more localization of production for goods ranging from semiconductors to solar panels. Perhaps most exciting over the long term is the possibility that the world significantly moves to hydrogen as a sustainable, non-carbon fuel source. It’s early days for the hydrogen economy, and viable methods for economic production of green hydrogen (e.g., with solar or wind) are still under investigation. However, we see tremendous optionality in hydrogen layered onto a resilient industrial supply business. Finally, industrial gas production is a major source of carbon emissions in the world today, so conversion to green energy could significantly move the needle for the global carbon footprint. .

Even if we are correct about the industrial gas industry, progress will not move in a straight line. Complex systems have positive and negative feedback loops. Positive feedback loops are the self reinforcing attributes where growth begets more growth, such as network effects, while negative feedback is the stubborn, real-world challenges that impair growth. Take electric vehicles, for example. While there is a steady growth in demand for EVs, the need to develop the infrastructure around charging and producing EVs and their batteries push back on EV adoption.

The interplay of positive and negative feedback is particularly relevant as we consider artificial intelligence, which is front of mind with the buzz around ChatGPT. AI appears to be a new engine for runaway growth, potentially outpacing even software, PCs, and the Internet. While AI has the potential to double the productivity of white-collar jobs, AI-driven automation and robotics are starting to impact the labor market. That disruption, however, is likely to experience much stronger negative feedback because it is harder to replace human physical labor than brain power. In general, the more digital the activity, the more likely that positive feedback loops will overwhelm, while the more analog, the more likely we see negative feedback loops win out.

Feedback loops mean that even the broadest predictions can take time to crystallize and can be quite fragile to small perturbations. Understanding how this dynamic interplay can lead to unpredictable outcomes with high frequency is critical to successful long-term investing, especially in a non-macro driven world. By populating a portfolio with resilient, adaptable companies, able to weather economic storms and take advantage of turbulence to gain economic share, you can insulate yourself from the inevitability of predictions gone awry.

Important DisclosuresThere is no guarantee that the information presented is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value. Net returns are calculated by subtracting the highest applicable management fee (.65% annually, or .1625% quarterly) from the gross return. Gross returns are inclusive of reinvestment of dividends or other earnings. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. The fees are available on request and may be found in Form ADV Part 2A. Index performance does not reflect the expenses of managing a portfolio as an index is unmanaged and not available for direct investment and include dividends after the deduction of withholding taxes. Any projections, market outlooks, or estimates in this presentation are forward-looking statements and are based upon certain assumptions. No forecasts can be guaranteed. Other events that were not taken into account may occur and may significantly affect the returns or performance. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events which will occur. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, and are subject to change at any time due to changes in market or economic conditions. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. An investor should not construe the contents of this newsletter as legal, tax, investment, or other advice. NZS Capital, LLC claims compliance with the Global Investment Performance Standards (GIPS®) GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. des NZS Growth Equity Composite includes all portfolios that invest primarily in equity and equity-related securities (including preference shares, warrants, participation notes and depositary receipts). The companies can be based anywhere in the world. The Portfolio Manager believes the companies and their shares will benefit significantly from innovation, particularly due to advances or improvements in technology, have attractive fundamentals, and offer good prospects for growth. The portfolios will typically hold 50-70 names. The NZS Select Composite includes all institutional portfolios that invest primarily in equity and equity-related securities (including preference shares, warrants, participation notes and depositary receipts). The companies can be based anywhere in the world. The Portfolio Manager believes the companies and their shares will benefit significantly from innovation, particularly due to advances or improvements in technology, have attractive fundamentals, and offer good prospects for growth. The portfolios typically will hold 20-30 names. The NZS Technology Composite includes all portfolios that invest primarily in equity and equity-related securities in the information technology and communication services sectors, (including preference shares, warrants, participation notes and depositary receipts). The companies can be based anywhere in the world. The Portfolio Manager believes the companies and their shares will benefit significantly from innovation, have attractive fundamentals; and offer good prospects for growth. It typically will hold 50-70 names. .GIPS® Composite Reports and a list of composite descriptions, pooled fund descriptions for limited distribution pooled funds are available upon request by emailing request to info@nzscapital.com. NZS Growth Equity, NZS Select and NZS Technology are reported in USD. The benchmark for the NZS Growth Equity Composite and NZS Select Composite is the Morningstar® Global Target Market Exposure Index NR USD . The index is designed to provide exposure to the top 85% market capitalization by free float in each of two economic segments, developed markets and emerging markets. The benchmark for the NZS Technology Index is the Morningstar Global Technology and Communications Services NR USD The Index measures the performance of companies engaged in the design, development, and support of computer operating systems and applications and computer technology consulting services. The Morningstar Global Growth Target Market Exposure measures the performance of large- and mid-cap growth stocks listed in developed and emerging countries around the world. These stocks represent the more growth-oriented half of the parent benchmark, the Morningstar Global TME Index, and are weighted by float-adjusted market capitalization. NZS strategies are not sponsored, endorsed, sold or promoted by Morningstar, Inc. or any of its affiliates (all such entities, collectively, “Morningstar Entities”). The Morningstar Entities make no representation or warranty, express or implied, to the owners who invest in the strategy or any member of the public regarding the advisability of investing in the strategy y or to any member of the public regarding the advisability of investing in equity securities generally or in the strategy in particular, or the ability of the strategy to track the Morningstar Global Target Market Exposure Index or the equity markets in general. THE MORNINGSTAR ENTITIES DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE STRATEGIES OR ANY DATA INCLUDED THEREIN AND MORNINGSTAR ENTITIES SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

NZS Capital Growth Equity Fund Q4 2022 Update