MYE - O-I Glass: Boring Can Be Profitable

Summary

- O-I Glass continues to generate positive returns in this current environment, though some of its numbers have been mixed.

- Fortunately, investors are paying attention to the good facets of the business and rewarding shareholders accordingly.

- While the easiest money has likely been made, the firm does offer additional upside from here.

Over the past several months, things have been rather difficult for investors for the most part. While there have been some bright spots in the market, overwhelmingly there has been more pain than upside. But there have been some companies, in some segments of the market, that have performed exceptionally well. One great example of this can be seen by looking at O-I Glass ( OI ), an enterprise focused on producing glass containers for its customers for beverages, food items, soft drinks, pharmaceutical offerings, and more. Driven by robust performance on both its top line and bottom line, the company has seen its share price rise nicely. Even with this being the case, shares of the company still look cheap enough, in my opinion, to warrant a solid ‘buy’ rating at this time.

Great returns from a ‘boring’ business

Most people might not view the packaging industry as being exceptionally interesting or exciting. But to me, the more boring the company the better. And what could be more boring than a glass bottle manufacturer? The last time I wrote an article about O-I Glass was back in the middle of October of this year. In that article, I talked about how the company had completed its operational transformation and was now in the process of growing nicely. Fundamental performance was also attractive and shares were trading cheap enough to deserve plenty of attention from investors. At that time though, because of how much shares had already risen, I decided to rate the enterprise a ‘buy’, down from the ‘strong buy’ I had rated it previously. So far, the company has lived up to this expectation. While the S&P 500 is up 5.5%, shares of O-I Glass have generated upside of 9.8%. Since I first rated the company a ‘strong buy’ back in December of 2021, shares have generated total upside for investors of 48.3% at a time when the S&P 500 has fallen 18.5%.

{kind=link}

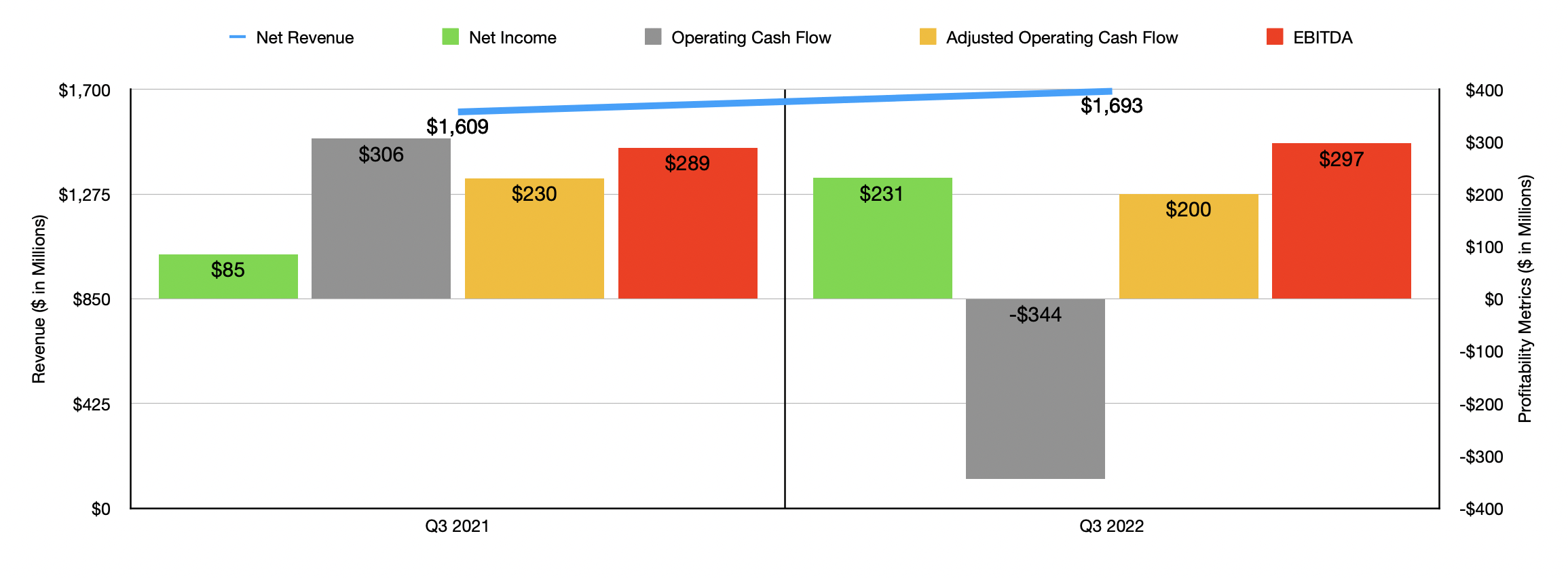

In my last article, we were only able to cover data going through the second quarter of the company's 2022 fiscal year. Today, we now have data covering through the third quarter as well. In that quarter, the company generated revenue of $1.69 billion. That's 5.2% higher than the $1.61 billion generated the same time last year. That sales increase, totaling $84 million in all, was primarily driven by higher pricing as the company offset inflationary pressures and unfavorable foreign currency fluctuations by passing those costs on to its customers. It also had to combat the downside associated with the sale of its glass tableware business that was completed in early March of 2022.

With sales rising, profits have followed suit. Net income of $231 million dwarfed the $85 million reported the same time of 2021. It is true that operating cash flow for the company tanked, plunging from $306 million to negative $344 million. But if we adjust for changes in working capital, it would have fallen more modestly from $230 million to $200 million. Much of that adjustment is associated with a $618 million cash outflow associated with a trust settlement that the company paid. That truly is a one-time event for the firm. Meanwhile, EBITDA for the company managed to rise from $289 million to $297 million.

{kind=link}

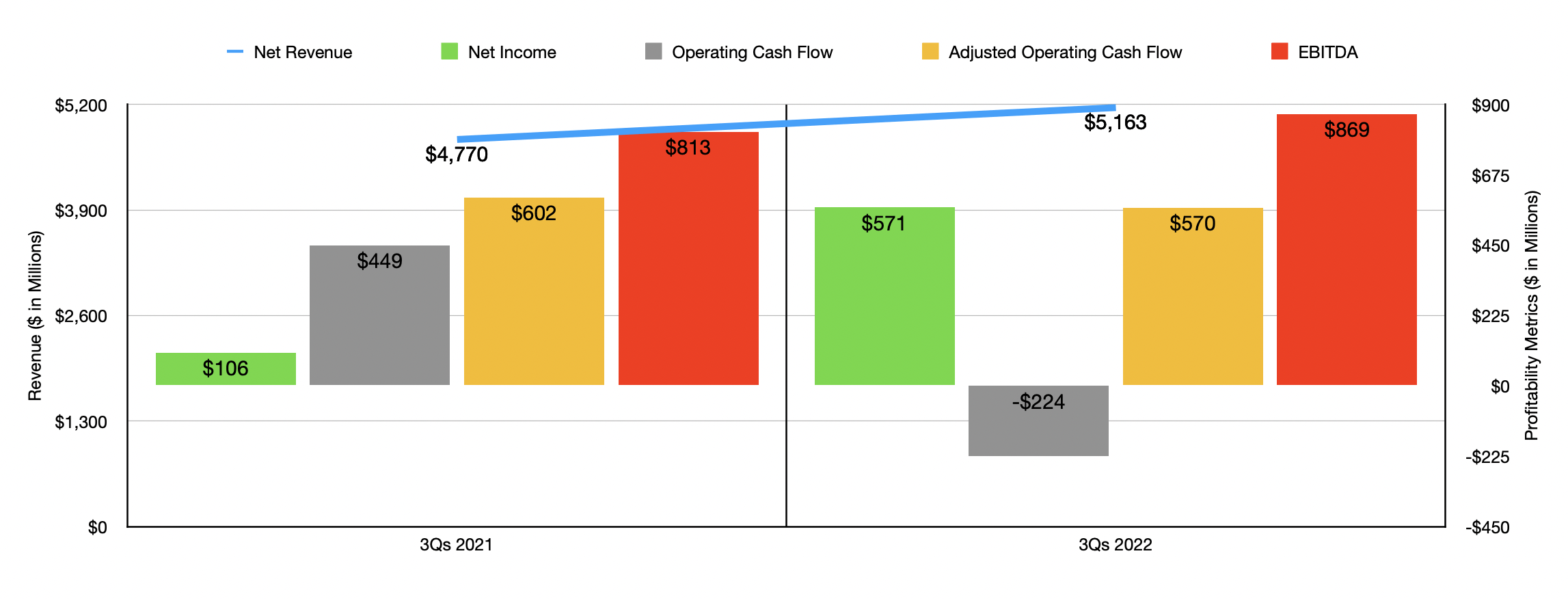

The results experienced in the third quarter alone were very similar to what the company achieved in the entirety of the first nine months of its 2022 fiscal year. Sales of $5.16 billion came in far higher than the $4.77 billion reported in the first nine months of 2021. Net income jumped from $106 million to $571 million. Once again, operating cash flow was down, having fallen from $449 million to negative $224 million. But if we adjust for changes in working capital, the drop would have been more modest from $602 million to $570 million. And over that same window of time, EBITDA for the business increased from $813 million to $869 million.

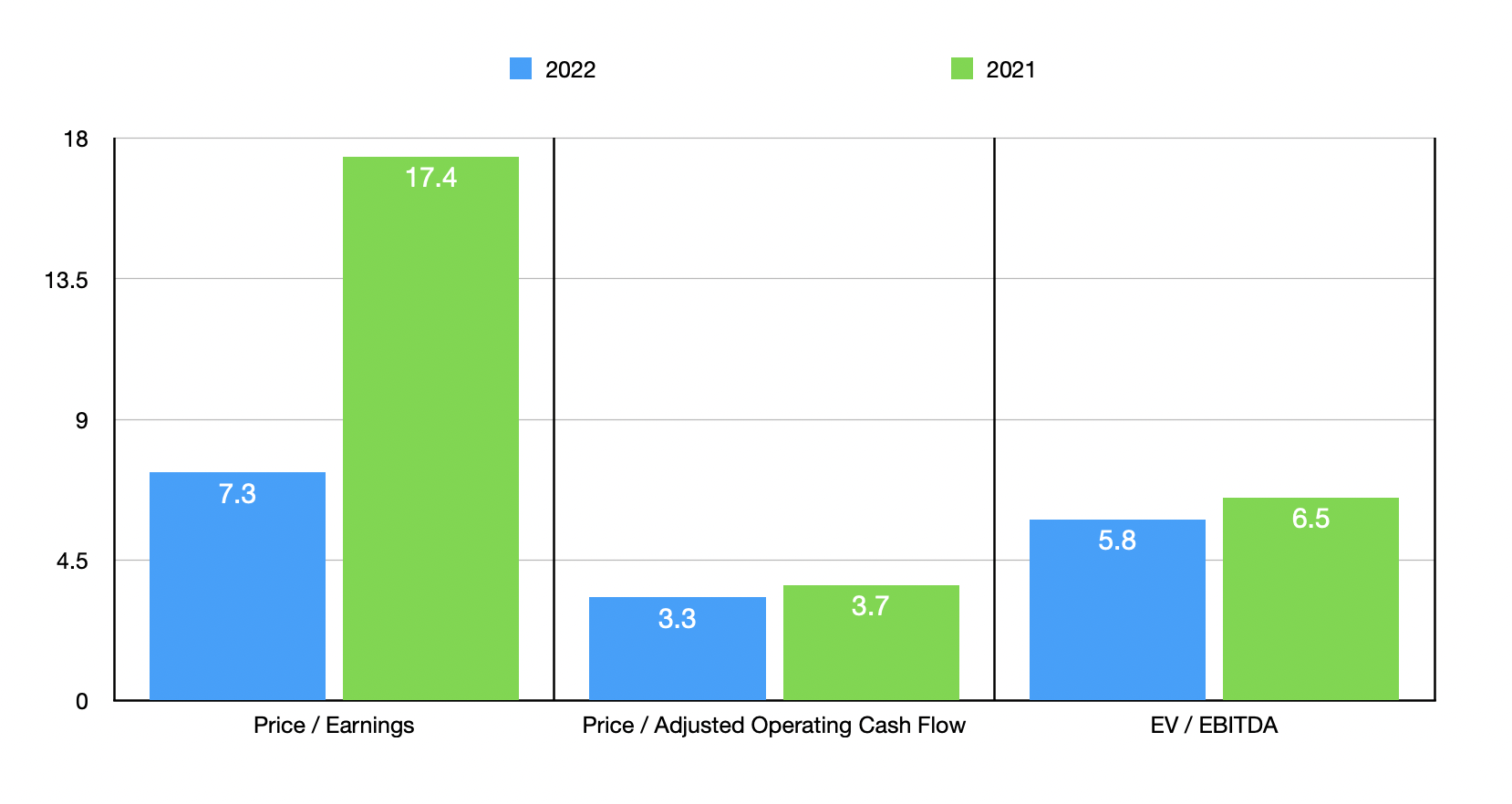

For the 2022 fiscal year in its entirety, management has only provided guidance when it comes to earnings per share and operating cash flow. Earnings per share should be between $2.20 and $2.25. That would imply net income, at the midpoint, of $353.6 million. On an adjusted basis, operating cash flow should come in at around $775 million. No guidance was given when it came to EBITDA, but if we assume that it will increase at the same rate that adjusted operating cash flow should, then we should anticipate a reading of $1.14 billion.

{kind=link}

Using these figures, it becomes pretty easy to value the company. On a price-to-earnings basis, the company is trading at a multiple of 7.3. That's down from the 17.4 reading that we get using data from 2021. The price to adjusted operating cash flow multiple should come in at 3.3 compared to the 3.7 that we would get using data from the year prior. Meanwhile, the EV to EBITDA multiple should be around 5.8. That compares favorably to the 6.5 reading that we get using data from the year before. As part of my analysis, I also decided to compare the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 10.4 to a high of 19.6. Using the price to operating cash flow approach, the range was from 5.1 to 13. And when it comes to the EV to EBITDA approach, the range should be from 7.2 to 10.3. In all three cases, our prospect was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| O-I Glass |

| 7.3 |

| 3.3 |

| 5.8 |

| Greif ( GEF ) |

| 10.7 |

| 6.1 |

| 7.2 |

| TriMas ( TRS ) |

| 19.6 |

| 11.5 |

| 10.3 |

| Myers Industries ( MYE ) |

| 15.1 |

| 9.9 |

| 9.1 |

| Silgan Holdings ( SLGN ) |

| 14.4 |

| 13.0 |

| 10.3 |

| Berry Global Group ( BERY ) |

| 10.4 |

| 5.1 |

| 7.5 |

Takeaway

With all the data that I see in front of me, I must say that I am not terribly surprised by how well O-I Glass has performed over the past year or so. Shares were drastically underpriced and fundamental performance has been quite robust. Yes, the company has dealt with some one-time events. But on the whole, it seems healthy and is likely to continue performing well in the long run. I definitely think the easy money has been made at this point. But given how cheap shares are, both on an absolute basis and relative to similar businesses, I would make the case that shares warrant further upside to the point of deserving a solid ‘buy’ rating still.

For further details see:

O-I Glass: Boring Can Be Profitable