MYE - O-I Glass: This Ride Still Has Room To Go

2023-05-31 08:17:58 ET

Summary

- O-I Glass shares continue to look fundamentally cheap despite significant gains, warranting a 'buy' rating.

- The company has performed well, transferring higher costs onto customers and generating higher profits.

- Even with a potential recession in the second half of 2023, OI stock remains attractively priced compared to similar firms.

One of the biggest challenges I have had as an investor is knowing when to sell. This is true both when things are going right for me and when they are going wrong. There is no perfect answer to the question of when you should sell. This is especially true when shares of a company still look fundamentally attractive. Those who have followed my thoughts over the past few months on O-I Glass ( OI ), a company that's dedicated on the production of glass containers that are used for beverages, food items, pharmaceutical offerings, and more, likely have been asking whether now is the time to exit their positions. Although there is nothing wrong with taking money off the table, especially after a company has seen significant upside, it is also painful to do so when the shares of the business in question continue to look cheap. In the case of this firm in particular, I would argue that some additional upside probably still does exist. So while the easy money has been made, I do think that the company still warrants a ‘buy’ rating at this time.

Great performance… for now

O-I Glass has, over the past couple of years now, been one of the best investment calls I have made but did not actually buy stock in. From my original ‘strong buy’ article on the company back in the middle of July of 2021 through today, shares of the business have spiked 32.4%. Over the same window of time, the S&P 500 has seen downside of 3.5%. As recently as early January of this year, I still remained bullish on the company, rating it a ‘buy’. And since then, shares have seen upside of 31.1% compared to the 9.1% drop the broader market experienced.

{kind=link}

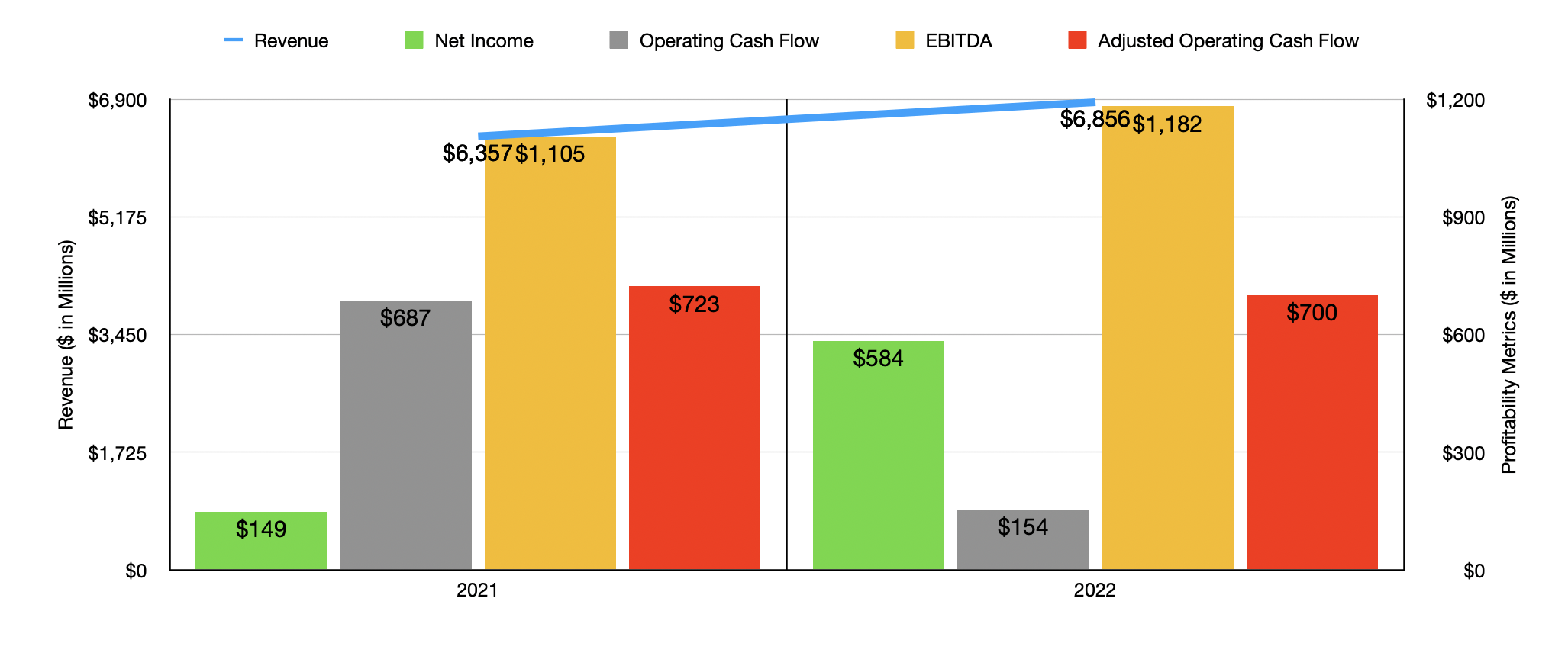

You would think that, after seeing such a nice move higher, I would become more neutral on the company. This is especially true when you consider recent guidance provided by management. Overall revenue for this year, for instance, is slated to fall in the low single digit to mid single digit rate. This comes after a very strong 2022 when revenue totaled $6.86 billion. That's 7.8% above the $6.36 billion the company generated in 2021. On the bottom line, management believes that earnings per share will be between $3.05 and $3.25 for 2023. At the midpoint, this would represent profits of $501 million. Although this is far better than the $149 million generated in 2021, it would represent a decline from the $584 million reported last year. Although both of these are slated to be worse than last year, operating cash flow has been guided higher. Management currently expects this to be about $875 million. While this is significantly greater than the $154 million reported for 2022, it's also comfortably above the $700 million reported for that same year if we adjust for changes in working capital.

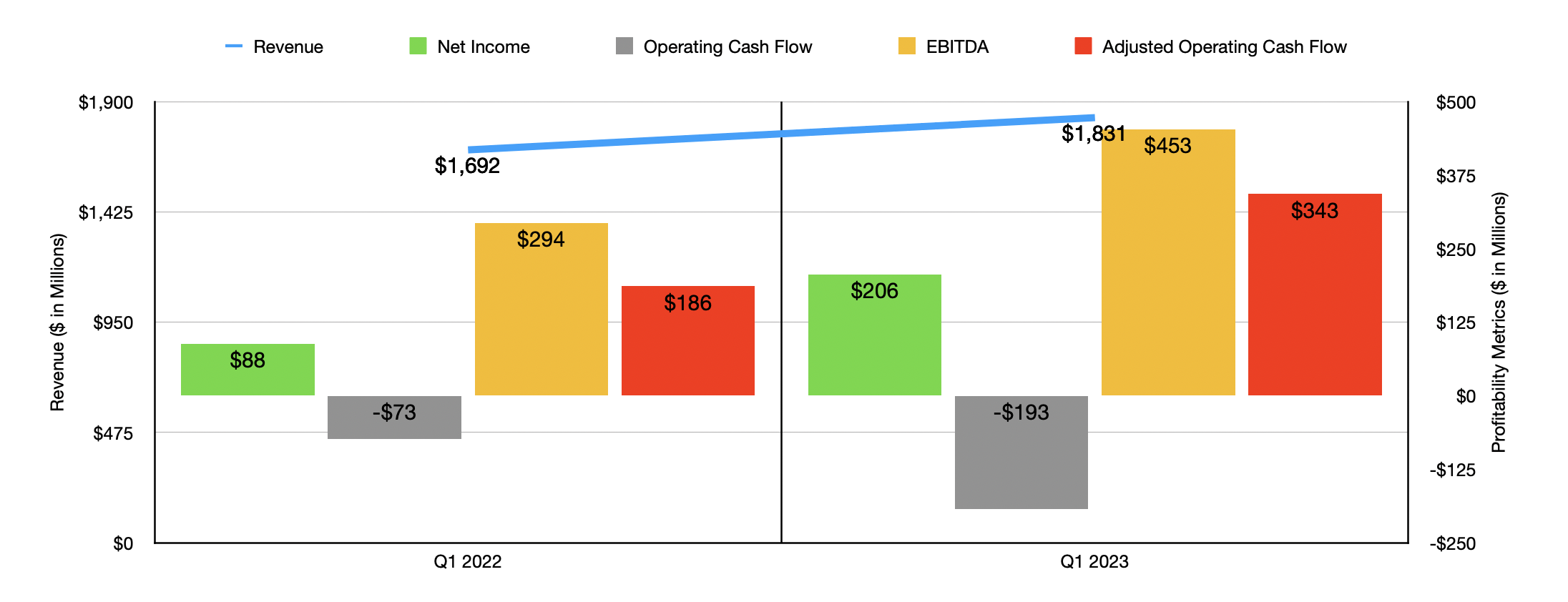

To some extent, it may be difficult to believe the current guidance offered up by management. Consider how the company performed during the first quarter of its 2023 fiscal year. Overall revenue for that time came in at $1.83 billion. That represents an increase of 8.2% over the $1.69 billion reported for the same quarter of the 2022 fiscal year. This increase in revenue was across the board. But the largest chunk came from a 9.2% rise in revenue associated with the packaging for alcoholic beverages like beer, wine, and spirits. Revenue there grew from $1.11 billion to $1.21 billion. Shockingly, this increase came even at a time when glass container shipments for the company as a whole dropped by 8% year over year. This impacted revenue negatively to the tune of $123 million when combined with changes in product mix. Foreign currency fluctuations hit sales to the tune of $19 million, while divestitures impacted the company negatively by $8 million. These were all offset, however, by $301 million worth of contribution associated with price increases as management aimed to push higher costs onto its customers.

{kind=link}

In truth, O-I Glass succeeded in transferring far more than its higher costs onto its customers. I say this because, during the first quarter of 2023, the enterprise generated profits of $206 million. That's significantly higher than the $88 million reported one year earlier. Those who are bearish about the company will point out that operating cash flow worsened from negative $73 million to negative $193 million. But if we adjust for changes in working capital, the increase would have been from $186 million to $343 million. Meanwhile, EBITDA for the company also increased, growing from $294 million to $453 million.

According to management, results should remain strong for the first half of the 2023 fiscal year. But in the second half of the year, they are forecasting rather conservative results because of their view that the probability of a recession is rising. Even if this does come to fruition, I would argue that shares of the company look attractively priced. We already know what to expect when it comes to net profits and adjusted operating cash flow. If we assume that the decrease in net profits will match the decrease in EBITDA, then we would expect a reading for that of $1.01 billion for the year.

{kind=link}

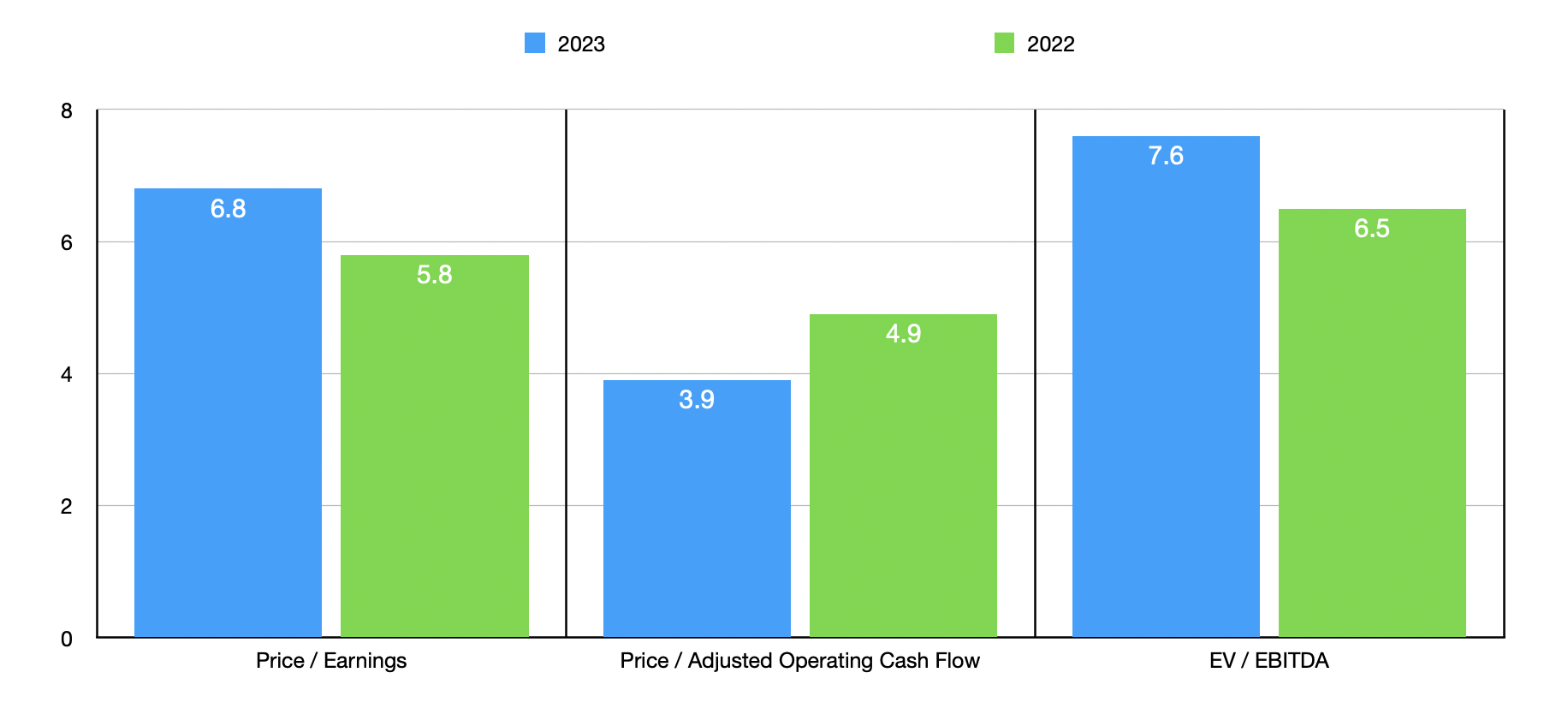

Taking these figures, we can see that the company is trading at a forward price to earnings multiple of 6.8. The forward price to adjusted operating cash flow multiple is considerably lower at 3.9, while the forward EV to EBITDA multiples should be 7.6. As you can see in the chart above, two of these three metrics look worse for the 2023 fiscal year than they do if we were to use data from 2022. In the table below, meanwhile, I compared the company to five similar firms. On both a price to earnings basis and a price to operating cash flow basis, O-I Glass ended up being the cheapest of the group. Meanwhile, using the EV to EBITDA approach, only one of the five companies was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| O-I Glass |

| 6.8 |

| 3.9 |

| 7.6 |

| Greif ( GEF ) |

| 8.0 |

| 5.4 |

| 6.4 |

| TriMas Corp. ( TRS ) |

| 18.8 |

| 14.1 |

| 9.8 |

| Myers Industries ( MYE ) |

| 12.9 |

| 7.8 |

| 7.7 |

| Silgan Holdings ( SLGN ) |

| 15.8 |

| 13.4 |

| 10.3 |

| Berry Global Group ( BERY ) |

| 10.4 |

| 4.3 |

| 8.0 |

Takeaway

On both an absolute basis and relative to similar firms, shares of O-I Glass look fundamentally cheap. The company also looks healthy, even if we assume that management is right about the impact that a recession would have heading into the second half of the 2023 fiscal year. And in the event that no recession comes about, then the end result should be even far better for shareholders than what is being forecasted. Due to all of these factors, I would still believe that some additional upside exists for shareholders. As such, I've elected to keep the ‘buy’ rating that I had on the firm previously.

For further details see:

O-I Glass: This Ride Still Has Room To Go