AZO - O'Reilly Automotive: A Great Company But A 'Hold' At Current Valuation

2023-12-03 07:35:50 ET

Summary

- O'Reilly Automotive is a prominent retailer of automotive parts and accessories with over 6,000 stores in the US and expanding in Mexico.

- This sector typically exhibits anti-cyclical behavior because during times of recession or economic uncertainty, people tend to prioritize repairing their existing vehicles over purchasing new ones.

- O'Reilly's entry into the Mexican market presents significant growth potential due to the country's high average age of vehicles and limited access to new cars.

- Although the quality of the business is undoubted, I believe that current valuation does not offer an attractive upside.

Investment Thesis

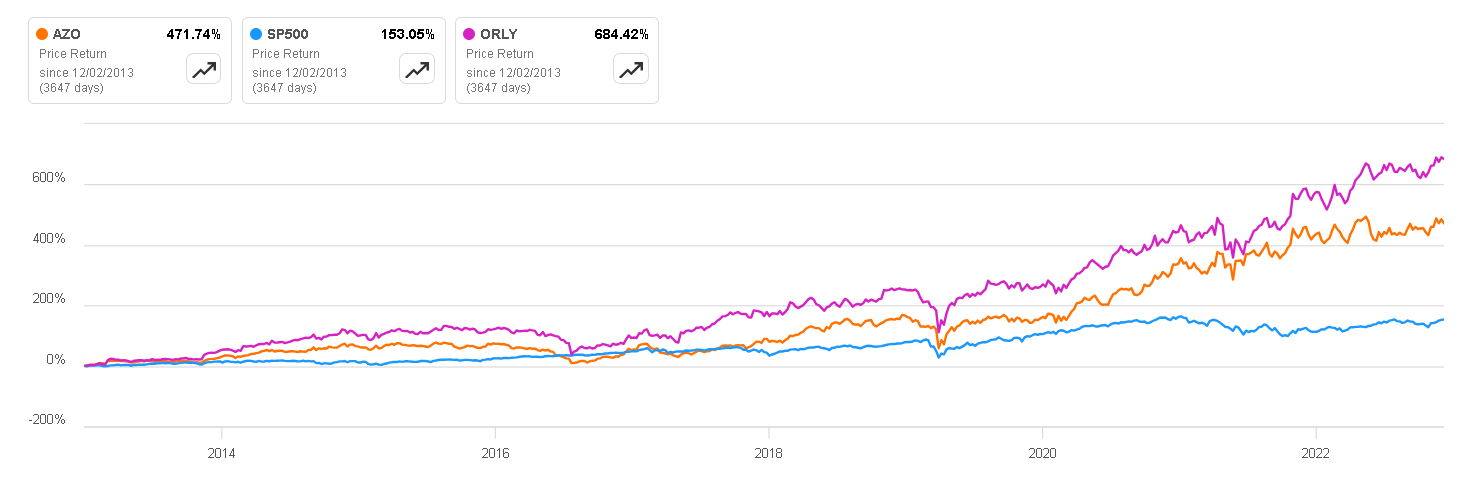

O'Reilly (ORLY), alongside AutoZone (AZO), has delivered exceptional performance over the past decade. Thanks to the quality of their businesses and effective management, both companies have consistently generated value , surpassing the S&P500 by a considerable margin.

In this article, I aim to discuss both companies, with a particular focus on O'Reilly. Over the last 15 years, it appears that O'Reilly has taken strategic measures to compete with the longstanding leadership that AutoZone has maintained. Presently, there are indications that O'Reilly is poised for greater growth in the coming years.

Additionally, I'll address the risks associated with the transition to electric vehicles and conduct a valuation to provide insights into the potential returns one could expect from the current share price.

{kind=link}

Business Overview

O'Reilly Automotive is a retailer of automotive parts and accessories. The company is one of the largest in its industry, operating more than 6,000 stores across the United States and nearly 50 in Mexico, where it has been recently expanding. O'Reilly Automotive provides a wide range of automotive products, including replacement parts, tools, equipment, and accessories for both professional mechanics and do-it-yourself automotive enthusiasts.

The company was founded in 1957 and has grown to become a prominent player in the automotive aftermarket, along with AutoZone. This is a sector that typically exhibits anti-cyclical behavior because during times of recession or economic uncertainty, people tend to prioritize repairing their existing vehicles over purchasing new ones. However, even in periods of economic prosperity, the need for replacement parts remains constant, making this sector a reliable defensive one in any economic condition.

As demonstrated in the following image, auto parts sales were not significantly impacted during the 12 months following the last two severe recessions in the United States (in 2001 and 2008). In fact, they even experienced growth ranging from 2% to 4% during those periods.

Performance during Recession (Hedges Company)

Average Age of Vehicles: A Growth Driver

One of the primary drivers of growth in the auto parts market is the average age of vehicles. An uptick in this factor corresponds to an increased demand for regular vehicle maintenance and the replacement of various automotive parts, including tires, lubricating oil, and other components.

In the United States, this variable has experienced a significant increase, with the median age currently at 13 years, slightly surpassing the previous median of 12.5 years . As previously mentioned, the recent surge in prices due to inflation and concerns about a recession is prompting consumers to approach significant purchases such as new cars with caution. Consequently, they are opting to maintain their existing vehicles rather than making investments in new ones.

S&P Global Mobility

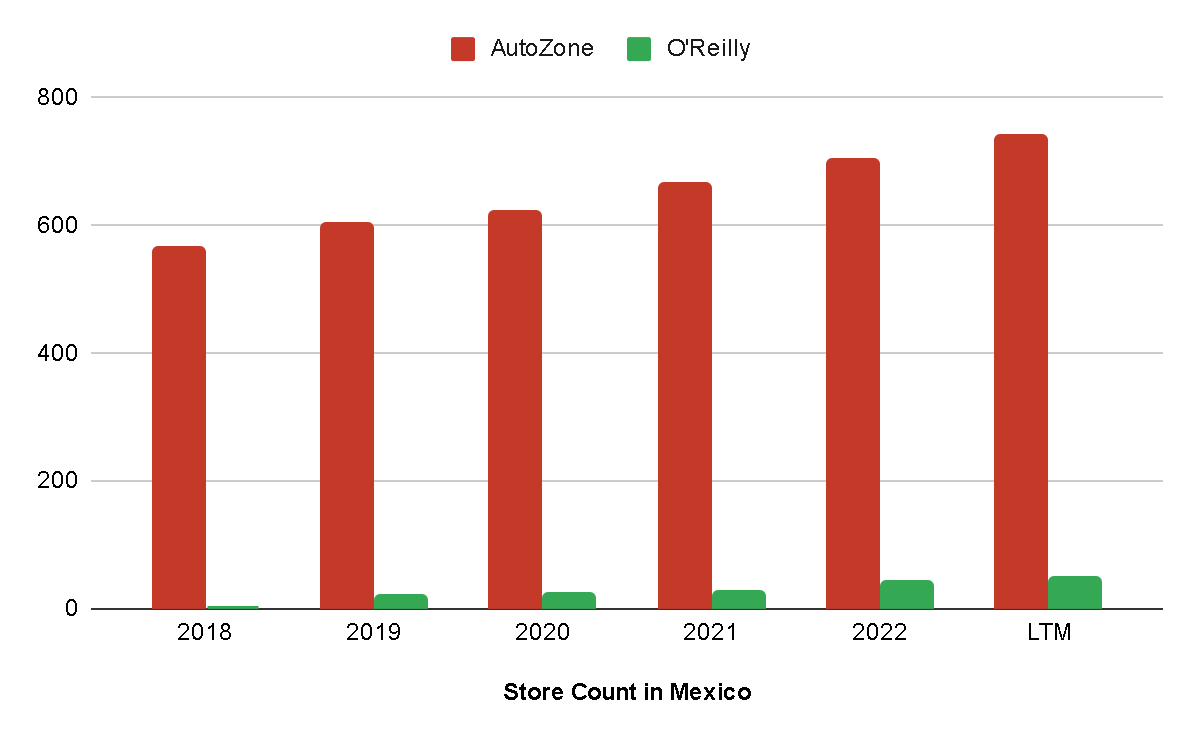

A particularly attractive market for these companies is the Latin American market, to which O'Reilly has exposure through expansion in Mexico that began in 2019. Returning to the study carried out by S&P Global Mobility in 2022, the average age of vehicles in Mexico was around 16 years old. In other words, the country has an abundance of extremely old vehicles that will necessarily require greater maintenance and replacement of parts.

This is why the growth potential for O'Reilly in Mexico is particularly intriguing—a market with a substantial demand for auto parts. With its current 48 stores, the company could potentially expand this number by 15 times just to reach the store count that AutoZone has in the country . There is significant growth ahead, which seems to be caused by structural characteristics of the country, which will hardly change in the coming years.

Firstly, the price of a 2023 Nissan Sentra in Mexico is approximately $400,000 Mexican pesos, while the minimum wage is $207 pesos per day. This means a Mexican would have to work almost 1,900 days at the minimum wage to afford a new Nissan. In contrast, in the United States, the same Nissan costs around $20,000 USD, and the minimum wage is $17 an hour, equivalent to $136 a day. An American would have to work 147 days to buy a new Sentra.

Moreover, credit does not seem like a feasible option either. While interest rates in the United States are at 5%, in Mexico, they exceed 11%. Once again, the option of a new vehicle seems unviable, providing an explanation for the high average age of vehicles in Mexico .

{kind=link}

Transition to Electric Vehicles

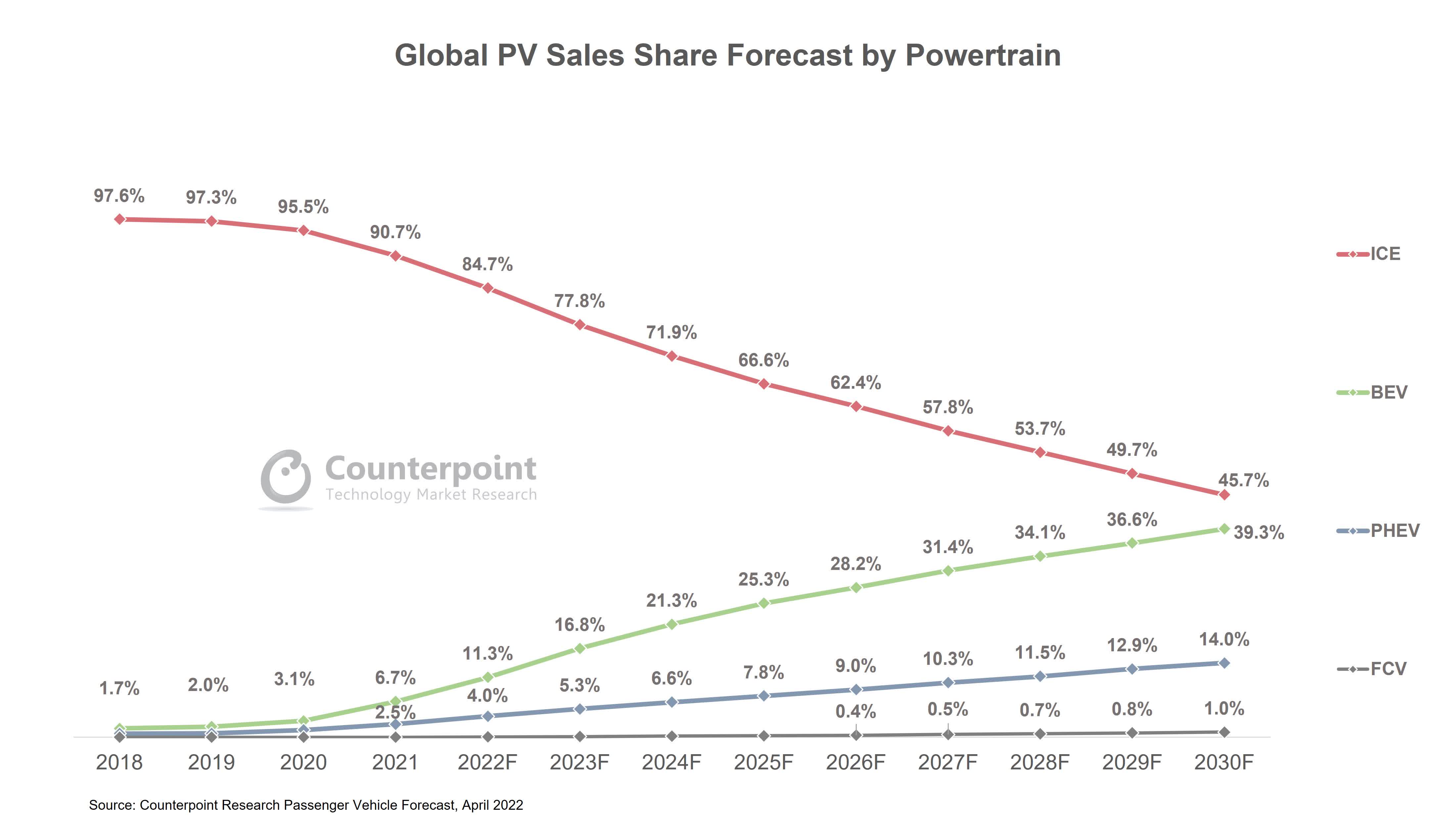

One of the primary concerns for sellers of automotive parts is the rise of electric vehicles (EVs), given their significantly lower number of moving parts compared to internal combustion engine vehicles (ICEVs). Estimates suggest that EVs have approximately 20 moving parts, a stark contrast to the roughly 2,000 found in ICEVs. This reduced reliance on parts maintenance directly impacts these sellers.

However, it's not anticipated that electric vehicle sales will surpass those of internal combustion vehicles in market share within the next decade. Even if they were to do so, it wouldn't automatically lead to the disappearance of maintenance needs for ICEVs. Additionally, less developed countries may take a longer time to transition to electric vehicles.

{kind=link}

Once again, O'Reilly's recent entry into the Mexican market seems to alleviate this concern. In these countries, electric vehicle purchases currently represent less than 1% , a notable contrast to the nearly 6% observed in the United States. O'Reilly's establishment in this market has the potential to enhance its long-term growth. When coupled with the growth factors mentioned earlier, this presence could pave the way for another decade of sustainable expansion.

Key Ratios

We have already discussed why the growth rate opportunity for O'Reilly seems more attractive to me compared to AutoZone. Now, I would like to highlight relevant quantitative aspects of each.

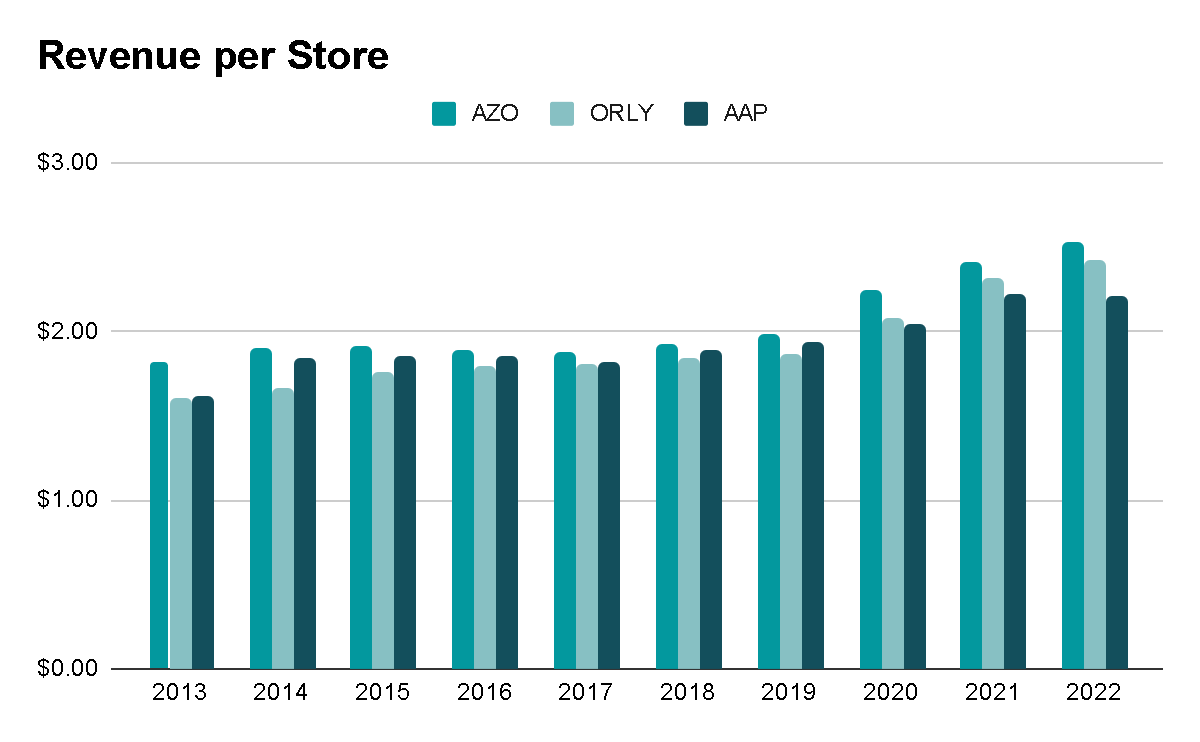

Firstly, ORLY has grown its revenue at an annual rate of almost 9% over the last decade. This is considerably higher than the 7% for AZO and 6% for AAP. Furthermore, it is even more noteworthy considering that 4.7% of ORLY's growth originated from increased revenue per store . This indicates an improvement in the efficiency and productivity of individual stores, surpassing the 3.3% increase in revenue per store for AZO and the 2.6% for AAP in the last decade.

{kind=link}

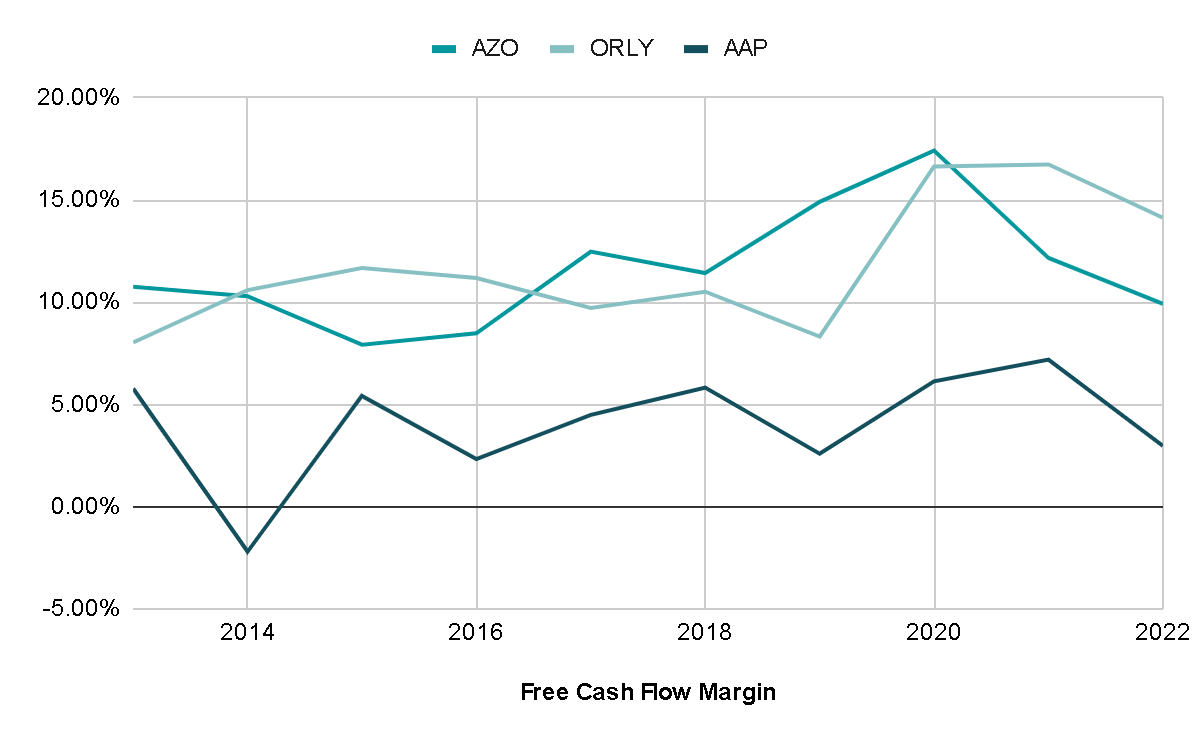

While revenue per store is an important metric, it's crucial to consider profitability alongside it. Therefore, it seems relevant to highlight the Free Cash Flow margins that each company generates. At this point, we can observe that both ORLY and AZO have quite similar margins, and even ORLY had higher margins in 2022 and the last twelve months. This indicates that not only has ORLY grown more, but it has also done so while maintaining profitability.

{kind=link}

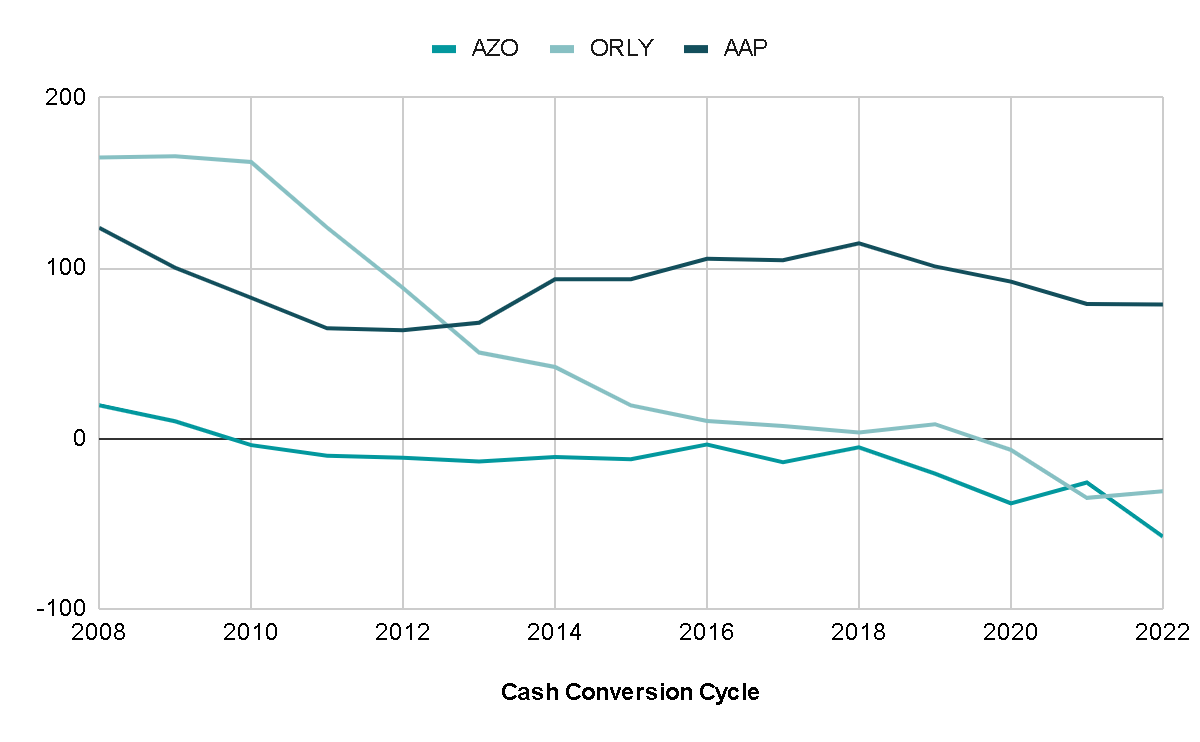

One of the key metrics that allows us to understand why these companies have such wide profit margins is their cash conversion cycle , which tells us the number of days it takes them to convert their inventory into cash.

Currently, AutoZone's conversion cycle is minus 57 days, and O'Reilly's is minus 30 days. In other words, ORLY collects cash for its inventory 30 days before having to pay its suppliers. This achievement is possible through having a good reputation and a large scale that allows them to negotiate favorable conditions with their respective suppliers. Although AutoZone had a better cycle more than a decade ago, there was a significant gap between the two. Therefore, it is noteworthy that even during 2021, O'Reilly has had a better cycle than AutoZone, demonstrating a significant improvement in its scale and closing the gap between both companies.

{kind=link}

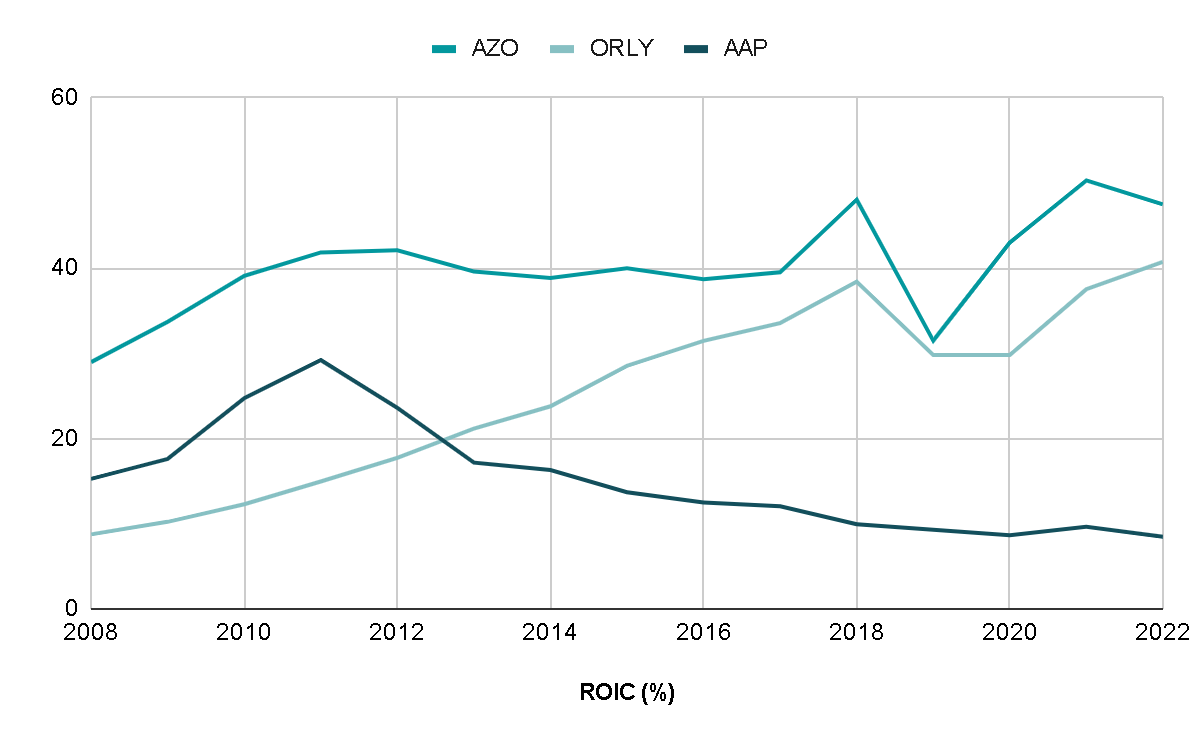

Having higher free cash flow generation margins is crucial because these companies boast very high return ratios on invested capital —47% in the case of AutoZone and 41% in O'Reilly. Considering that the majority of cash is used to open and enhance new stores, as well as distribution centers that accelerate delivery times and improve the supply chain, it provides insight into the profitability of these businesses.

Therefore, having a broad margin allows for the reinvestment of the maximum amount of cash possible at these high rates. This, in turn, enables the companies to derive significant benefits from investments, translating into increased cash flow that can be further reinvested, creating a ' virtuous circle '.

{kind=link}

Management Incentives

A part that is sometimes not talked about much but is a pillar of the success of both companies is how well managed they are . This has not been a coincidence but is the product of a compensation plan structured so that managers have skin in the game in the company and with targets based on generating long-term value .

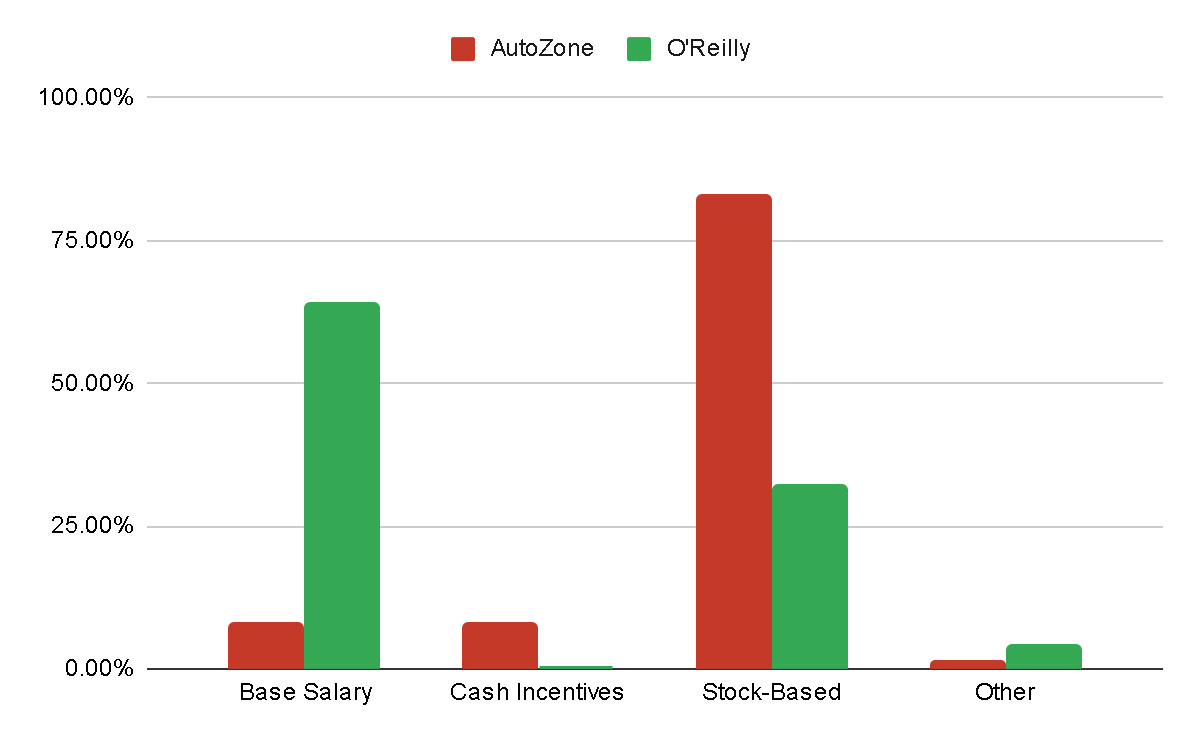

If we look at the CEO's compensation structure during the last fiscal year, we can notice how an important part of his compensation is in stock-based compensation with objectives which we will talk about a little later. In this regard, AutoZone seems to me to have a better structure, since during the previous year, 83% of the CEO compensation came from this, while at O'Reilly 64% came from the annual base salary.

{kind=link}

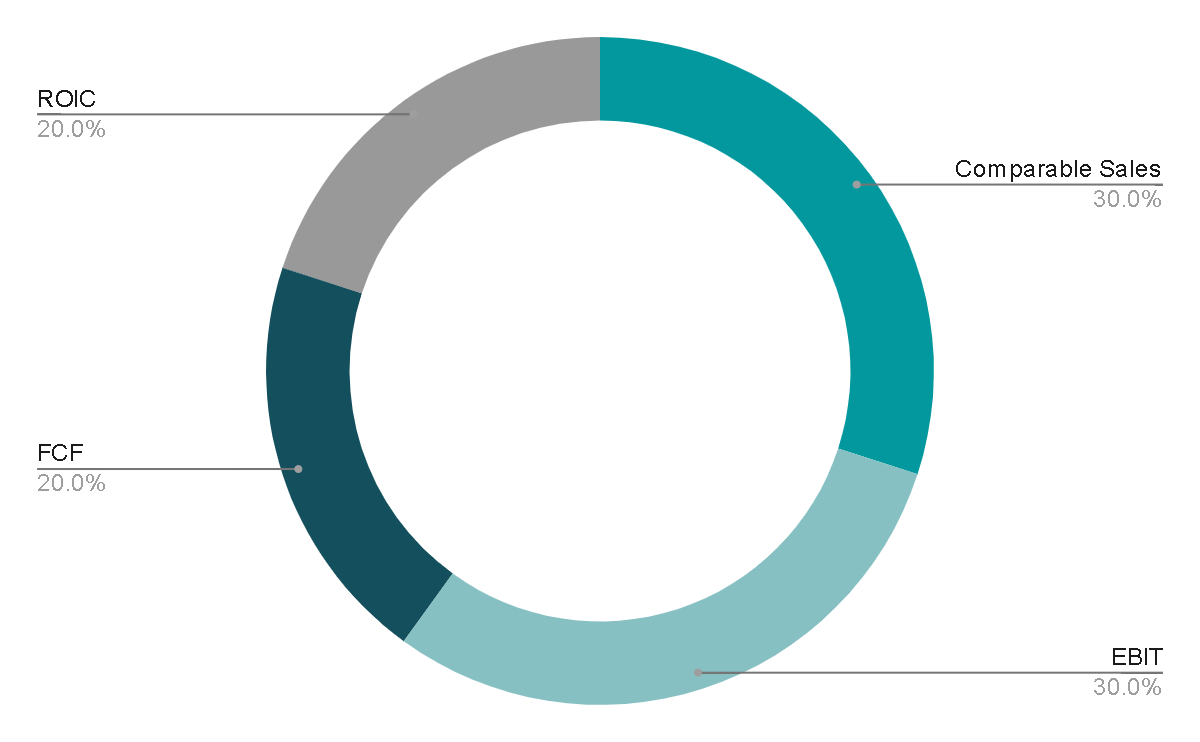

The incentives to earn compensation in shares vary in each one, but they have something in common: Seek operational improvement (increase EBIT) accompanied by value creation ((ROIC)).

In the case of ORLY, 30% of the compensation depends on the CEO achieving an increase in revenue per store between 4.5 and 6%, 30% on improving operating income, 20% on increasing free cash flow and 20% on that the ROIC is around 60%. On the other hand, although AutoZone does not break down exactly the percentage of each metric to earn stock-based compensation, they do share that these objectives are based on increasing the operating margin and maintaining an ROIC of around 55%.

In this way, we have managers who are constantly seeking to invest in organic, sustainable and profitable growth , avoiding disasters like what happened with Advance Auto Parts, and which has led it to have a worse performance compared to its peers.

{kind=link}

Valuation

While we've examined two high-quality companies, it's crucial to remember that a good company may not necessarily translate into a good investment if it's not acquired at the right price. Hence, I'll conduct a valuation using key performance indicators (KPIs) to provide an insight into the intrinsic value of the company and the potential return from the current price.

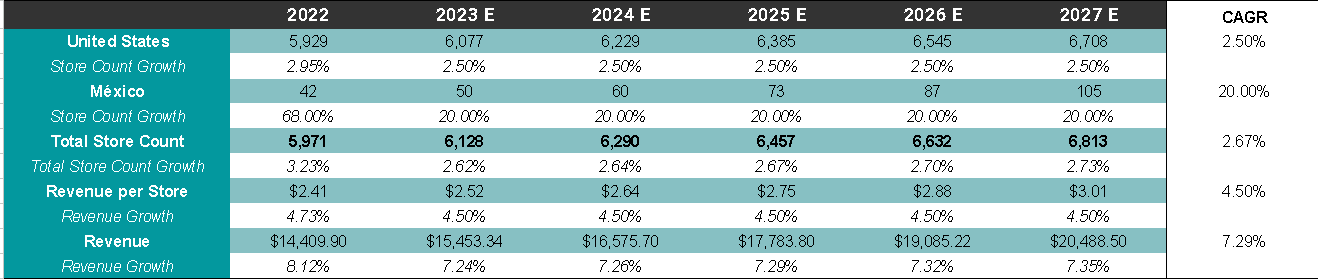

I anticipate that O'Reilly can sustain an annual store growth rate of 2.5%, a figure that might be considered conservative, projecting a total of 6,700 stores within five years. This estimate is even lower than AutoZone's current count of 6,900. Additionally, the growth potential in Mexico could be notably more dynamic due to the small comparable base and the significant untapped market, especially considering that, apart from AutoZone, there is no other national competitor in Mexico with strong brand power.

{kind=link}

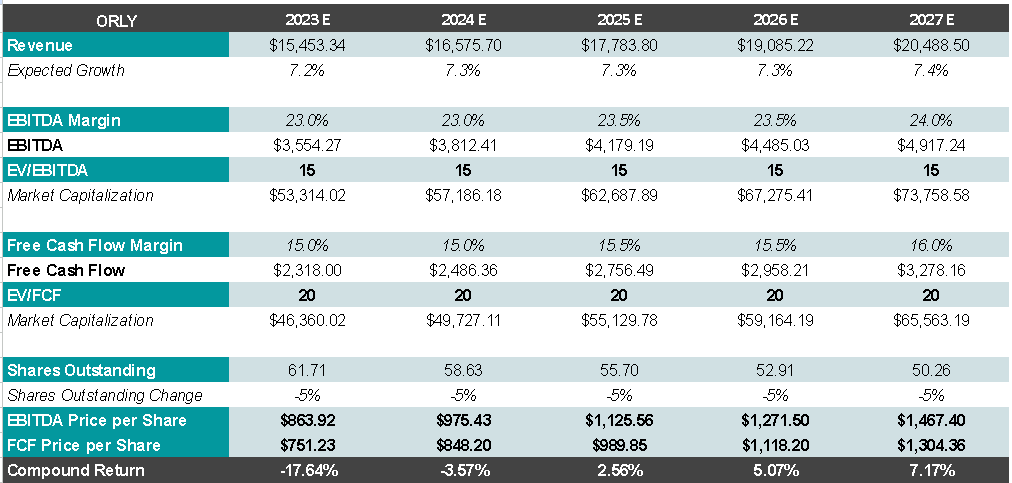

As for revenue per store, a growth rate of 4.5% annually, in line with historical trends, appears reasonable to me. This would result in a compounded annual growth rate of 7% for the top line. Assuming a slight expansion of margins, aggressive buybacks similar to previous years, and exit multiples of 15x EBITDA and 20x FCF, we could anticipate an annual return of 7% five years from now. This rate seems rather modest for a company of such high quality.

{kind=link}

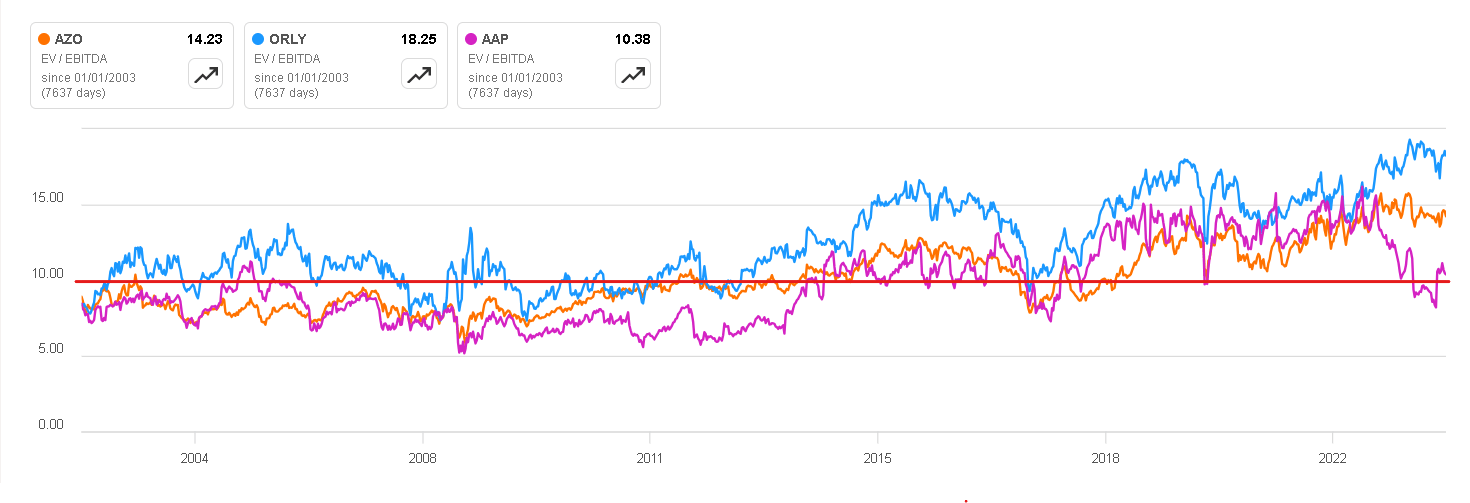

In addition to these considerations is the risk of facing a de-rating , indicating a potential decrease in the valuation multiple. Currently, both companies are trading significantly above the historical multiples that the market has traditionally assigned them, typically around 10-12x EBITDA. Consequently, this diminishes the margin of safety even further if one were to acquire these companies at their present valuations.

{kind=link}

Final Thoughts

In summary, O'Reilly has had an exceptional decade , positioning itself as the second-best company in the sector, surpassed only by AutoZone. Presently, it has laid a strong foundation, suggesting the potential to compete for industry leadership, evident in its key ratios and the quality of its management.

While the risk of disruption from electric vehicles appears distant, there are strategic levers, such as entry into the Mexican market, to potentially mitigate this risk. Consequently, I believe the company has at least another decade of growth and strong performance ahead. However, the current valuation appears to more than account for these prospects, making it less attractive as an investment opportunity. In my view, the company would need to experience a decline of at least 20% to become intriguing. Although predicting such a decline is uncertain, I believe it is prudent to exercise caution for now, leading me to assign a ' hold ' rating, with the hope of more favorable prices in the future.

For further details see:

O'Reilly Automotive: A Great Company, But A 'Hold' At Current Valuation