AZO - O'Reilly Automotive: Reiterating Our Bullish View On This Share Buyback Machine

Summary

- Since we initiated coverage on O'Reilly Automotive back in April 2022, the stock has outperformed the S&P 500 by a considerable margin.

- In an uncertain macro environment, ORLY's constant cash flow profile, fair multiple and below-target leverage ratio should continue to provide support well into 2023.

- Annual comps of +5%, a 2% increase from new store openings, 1% from operational leverage and 6-8% in share repurchases are expected to yield annual shareholder returns of 15-19%.

- With tighter monetary policy, persistent inflation and elevated consumer debt levels, history is about to repeat itself. Be prepared for lower-beta cash flow compounders to outperform the market. "BUY".

Summary

O'Reilly Automotive (ORLY) reported Q2 earnings on July 27. Since then, shares have risen 1.3% versus a -0.7% return for the S&P-500. On August 23, ORLY reinstated its annual investor day to discuss industry trends and the company's long-term financial track record.

Since we initiated coverage on ORLY back in April 2022 , the stock has outperformed the S&P-500 by a considerable margin. In light of the recent news flow, we believe this relative strength will persist for the remainder of the year as well as into 2023.

Investment Thesis Recap

Our long-term buy recommendation was built on four key pillars:

- Annual comparable sales growth to be in a range of 4% to 6%. Higher same-SKU inflation should compensate for short-term volatility in ticket count, primarily on the DYI side of the business.

- Net new store openings expected to add 2% to sales growth.

- Once the pro pricing initiatives have been fully digested by gross margin, operational leverage should contribute 1% to annual EBIT growth.

- And last but not least, share repurchases should enhance annual EPS growth by 7% or even 9%+, if the company decides to opportunistically accelerate its share buyback authorization. At the end of Q2 '22, ORLY's debt ratio stood at 1.96 times EBITDAR, below the targeted 2.5x figure.

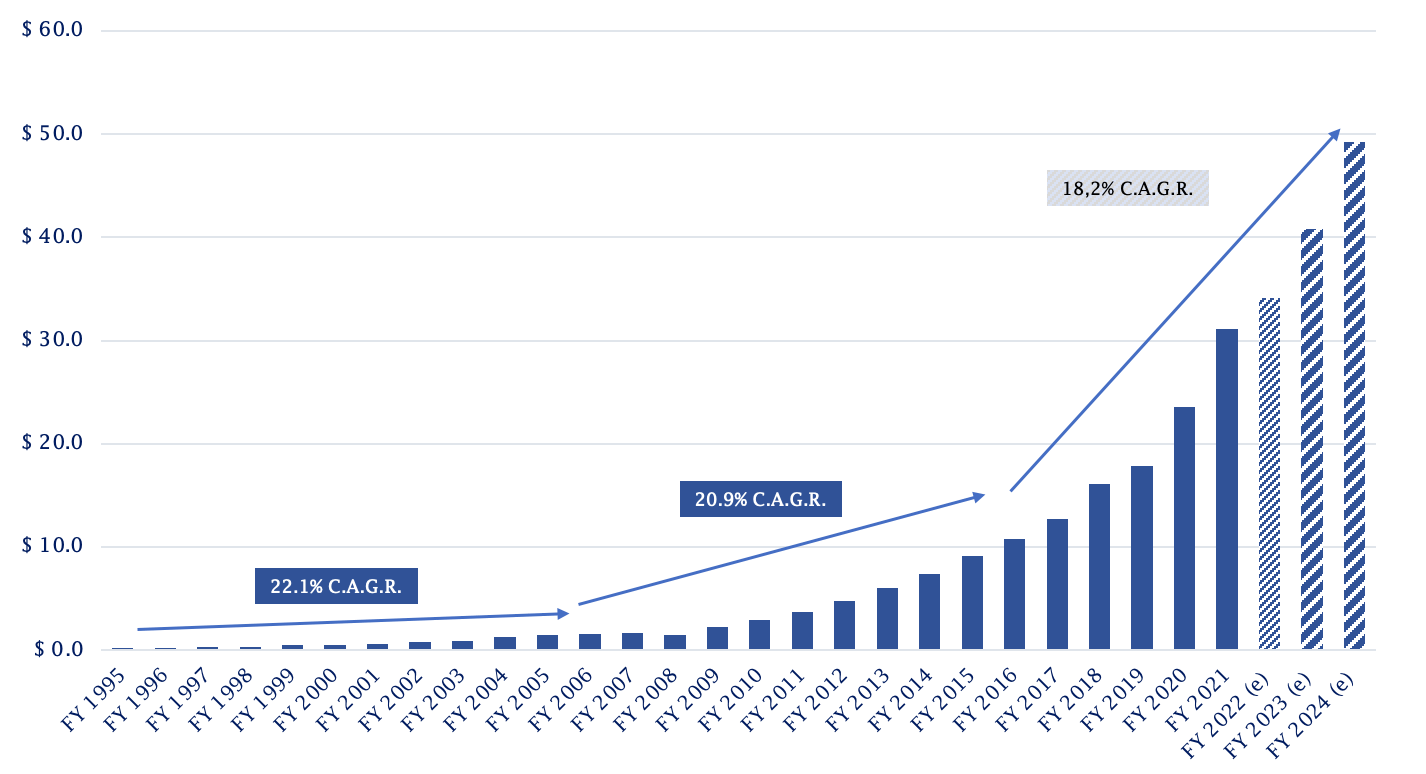

ORLY: EPS Track Record and Projections

{kind=link}

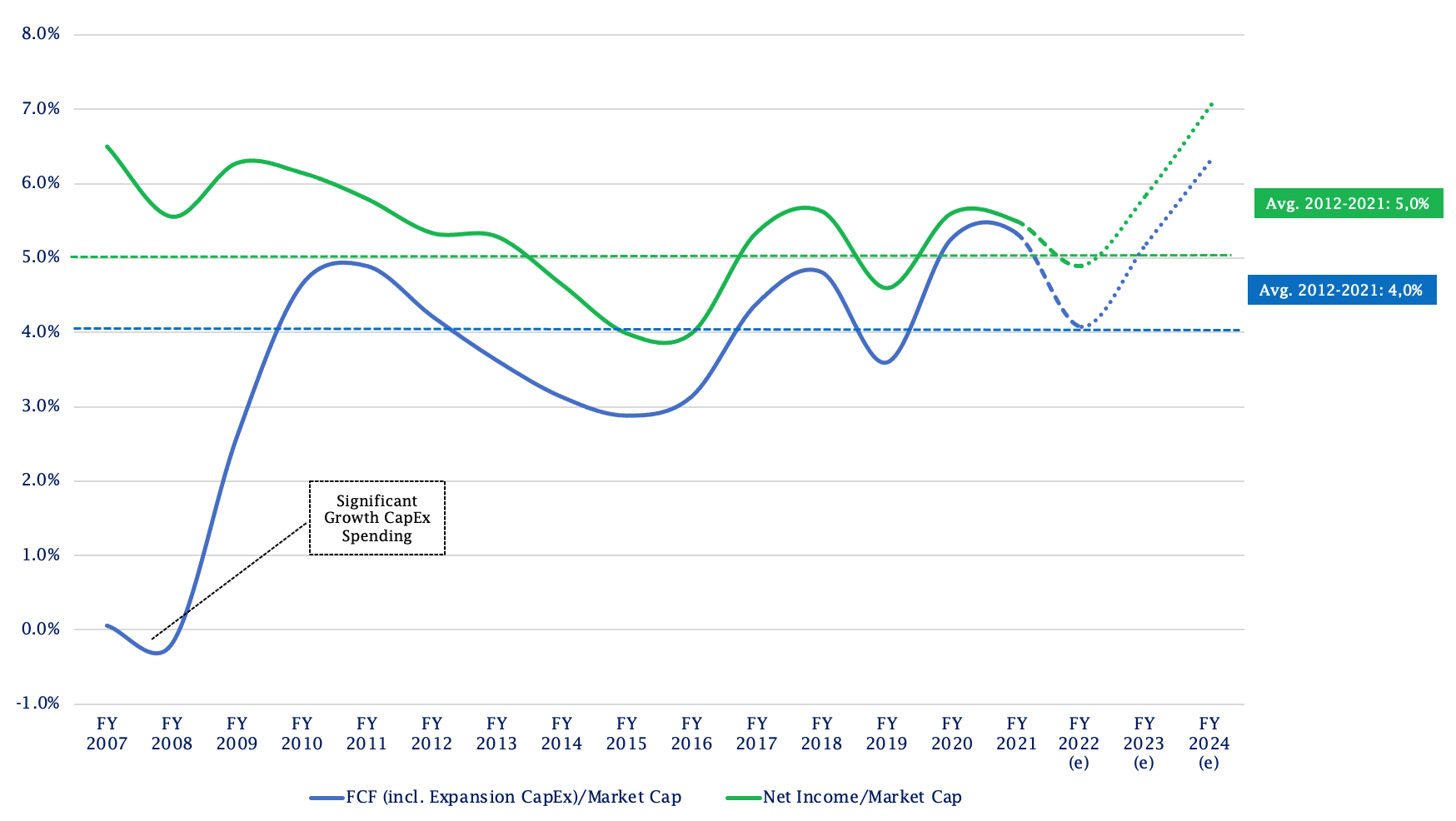

The above elements should translate into expected annual returns of 15% to 19% over the next 3-4 years, entirely driven by growing cash flows with no assumed multiple expansion or contraction.

ORLY: Historical and Future Earnings Yield

{kind=link}

We continue to view the stock as an attractive long-term compounder in a very fragmented market. As such, we reiterate our "Buy" recommendation. Furthermore, as per Investor's Business Daily , ORLY's beta was 0.64. Based on the current macro environment and monetary tightening cycle, lower-beta stocks are expected to strongly outperform the broader market.

Q2 Earnings Release And Revised FY22 Guidance

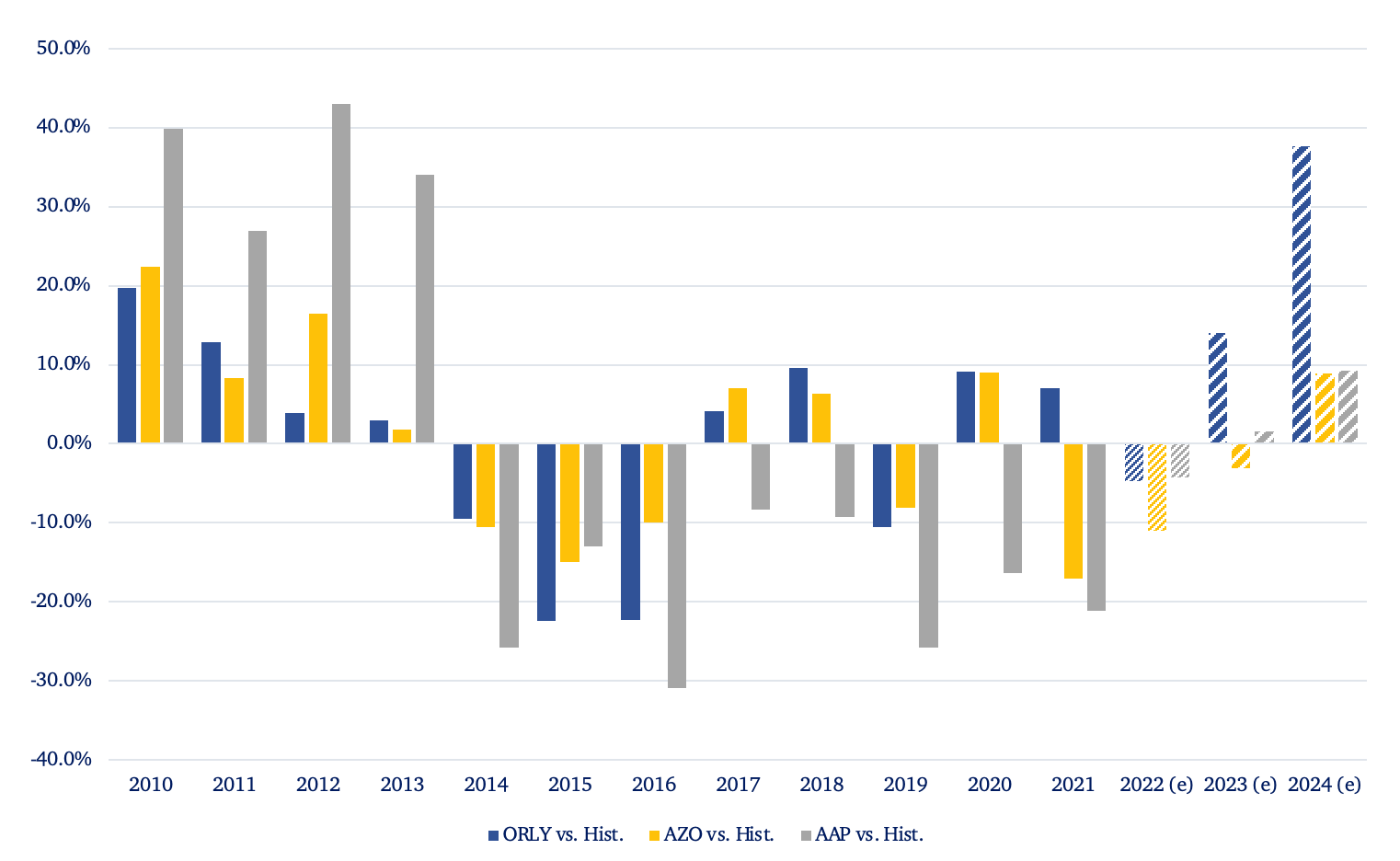

ORLY's Q2 earnings came in slightly below expectations, as its DYI segment was pressured in average ticket count. Despite having lowered the bar for FY22 on the back of its first half results, ORLY's growth outlook is more consistent than that of its closest peers, namely Autozone (NYSE: AZO ) and Advance Auto Parts (NYSE: AAP ). FY22 comps are now expected to grow by 3-5% versus the previously guided 5-7% in February and April 2022.

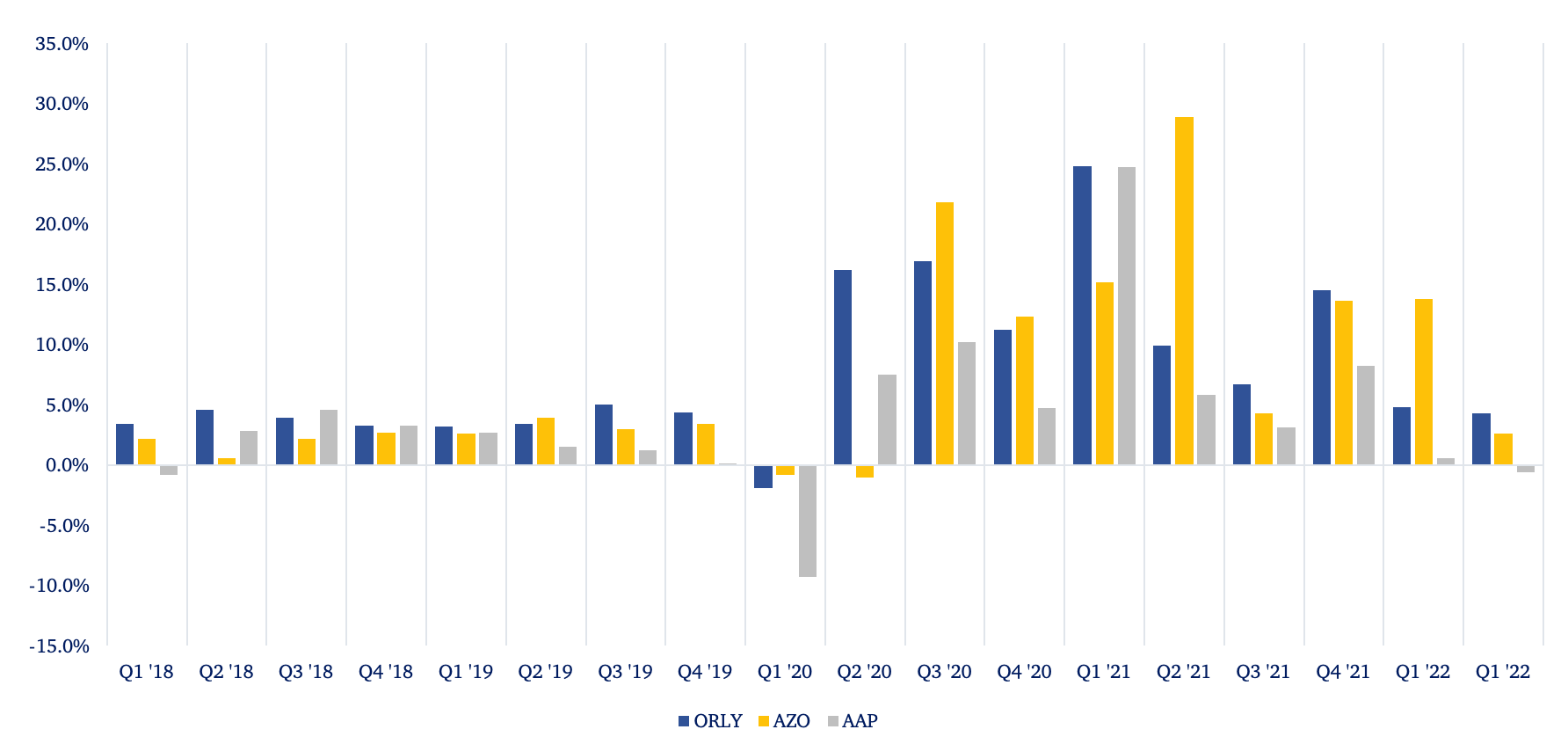

We highlighted their comparable sales growth in the below graph. Please note that AZO's quarter differs 2.5 months from ORLY's, while AAP's deviates 1 month from normal quarter reporting. Still, the picture remains quite clear: ORLY has a smoother core top line growth trend compared to its direct peers.

ORLY vs. Peers: Quarterly Comps

{kind=link}

Management sounded very conservative in its prepared remarks on comp growth, pointing to decelerating same-SKU inflation in the back half of 2022 versus 2021 (when inflation already started to tick higher). However, despite its conservative LIFO accounting method, the gross margin benefit from decelerating acquisition cost inflation was not incorporated in the revised guidance. As Michael Baker, D.A. Davidson analyst, noted :

You said you certainly expect to hold on to price. So does that imply that if inflation does start to moderate, you should see a little bit of a gross margin benefit in the back half? That potential gross margin benefit doesn’t seem to be in your back half guidance. Correct me if I’m wrong on that. – conference call transcript Q2 ’22

We haven’t forecasted a deflation in pricing in how we’ve thought about where we’ll go for the rest of the year.” conference call transcript Q2 ’22 – CFO Jeremy Fletcher

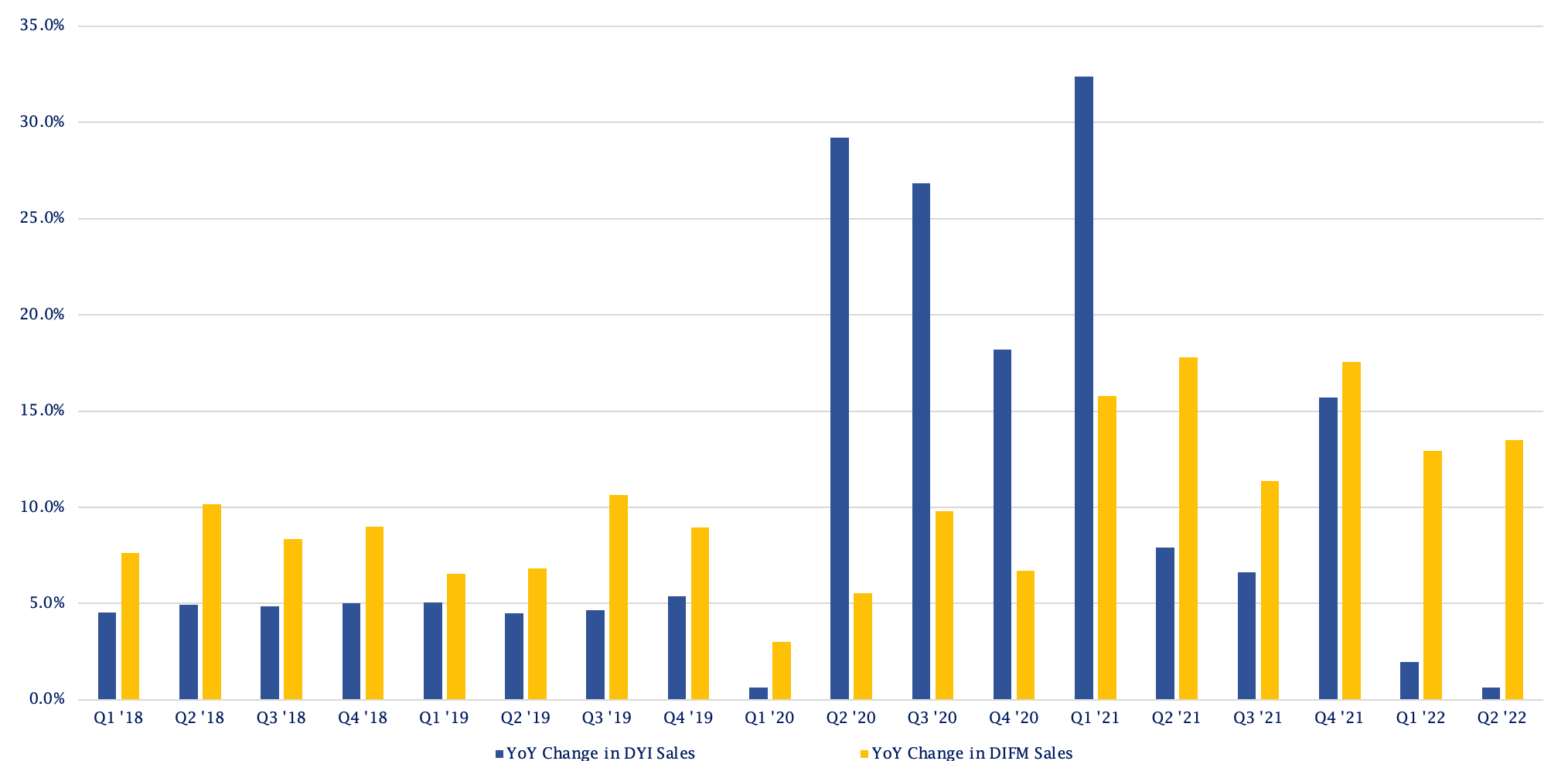

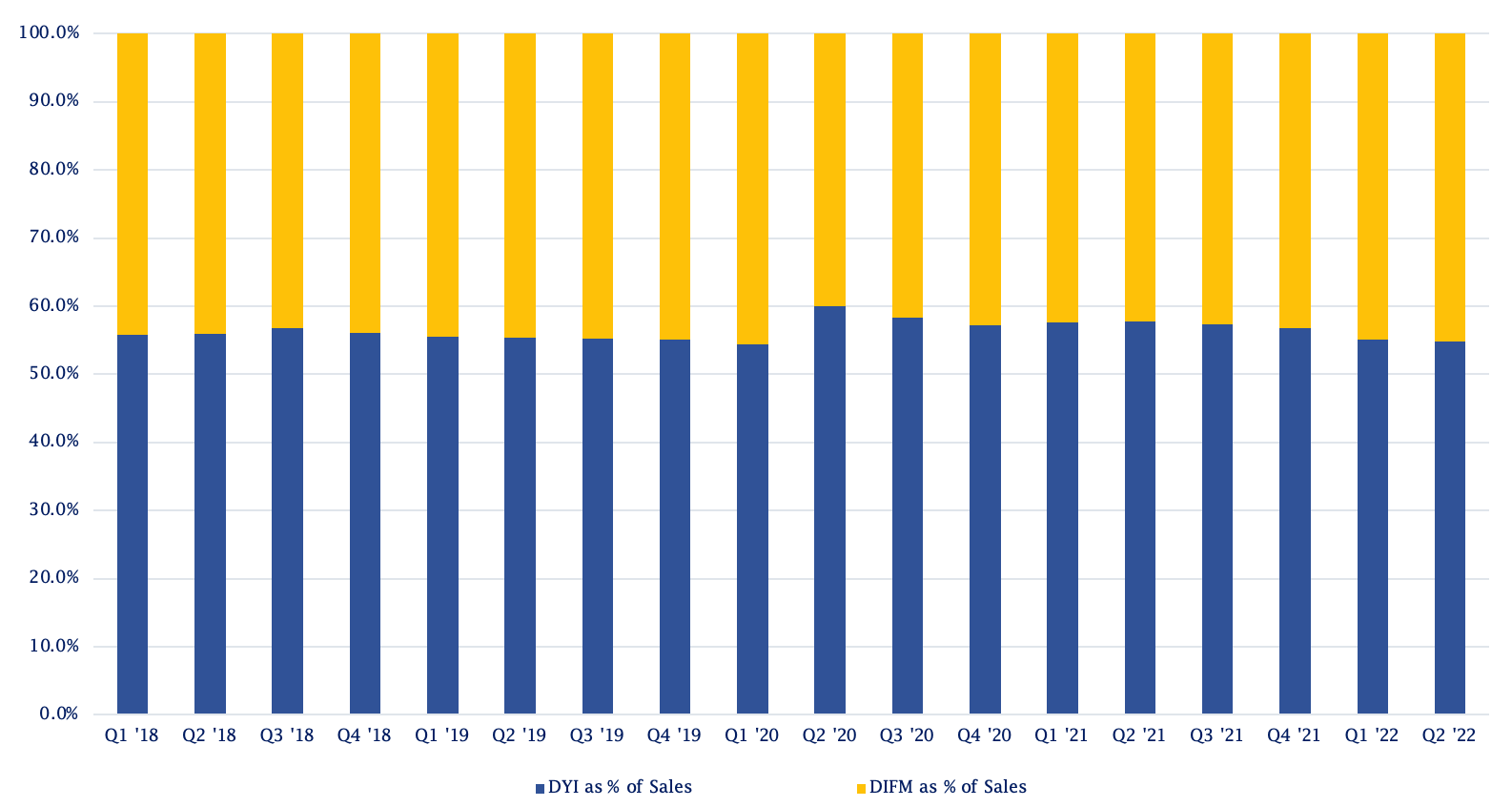

Fellow ORLY shareholders should be little surprised to see the management team make cautious comments about the short-term outlook. One might call it "under-promising and over-delivering". Considering that DIFM represents a multi-year growth opportunity for the company, as that side of the business is less prone to inflationary pressures and remains very fragmented, ORLY is very bullish on the longer-term business prospects. In Q2 2022, DIFM year-over-year growth actually accelerated to 13.5%, aided by both average ticket and ticket count growth. This performance should be stacked against a record-breaking +17.8% in Q2 of last year.

ORLY: Quarterly Growth in DYI and DIFM

{kind=link}

For reference, only 27% of AZO's business is being derived from commercial customers, despite growing twice as fast as ORLY in Q1 '22.

ORLY: Quarterly Breakdown Between DYI and DIFM

{kind=link}

Constant Free Cash Flow Equals Share Repurchases

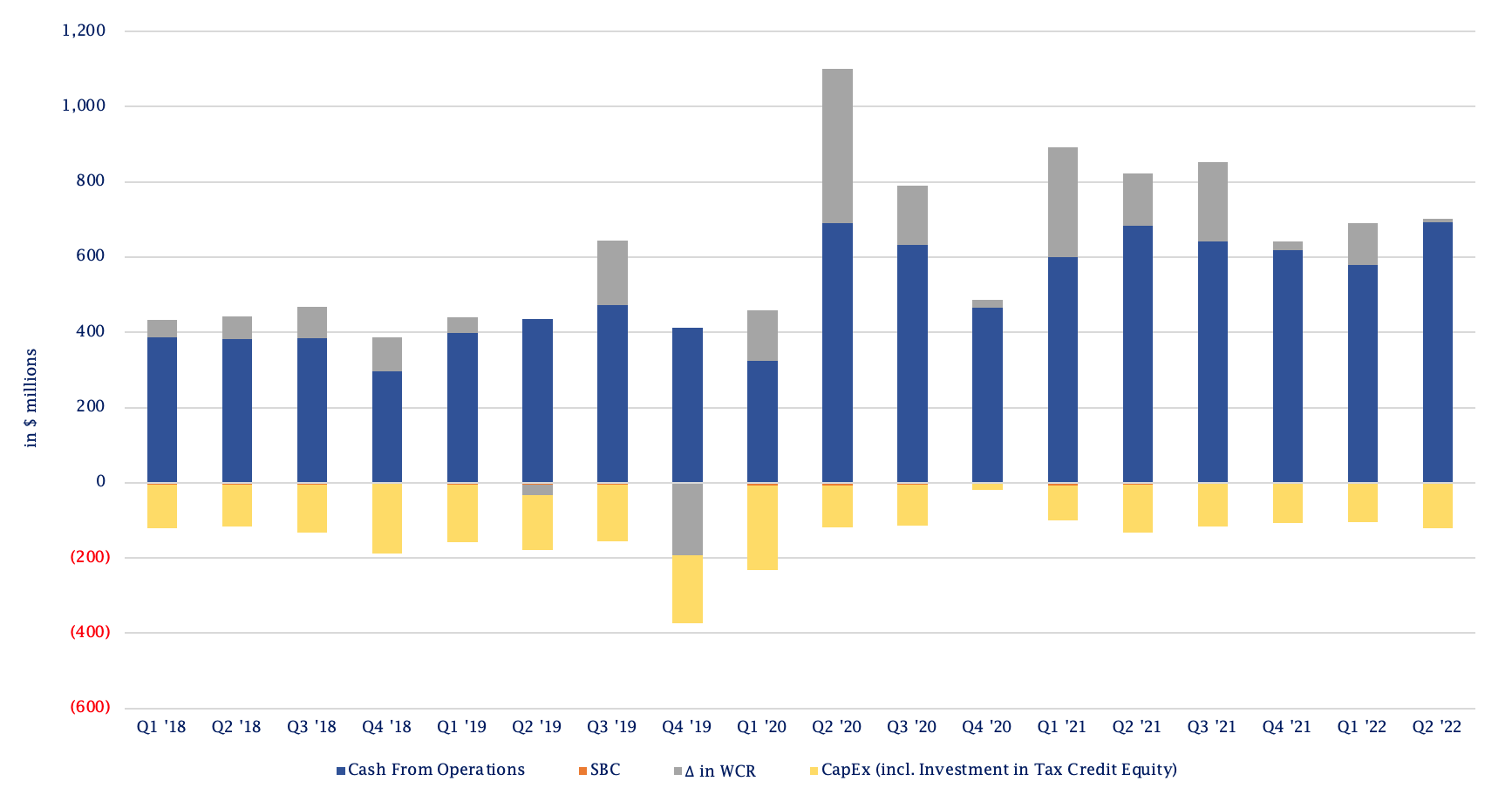

What we really like about ORLY's business is the constant free cash flow generation with absent seasonality in working capital requirements. Additionally, its Return On Invested Capital has been trending upwards since the GFC both on a working capital-neutral as well as reported basis. In Q2 '22, ORLY generated $576M in free cash flow, compared to $689M over the same period last year due to reduced working capital cash inflows.

ORLY: Quarterly Cash Flow Breakdown

{kind=link}

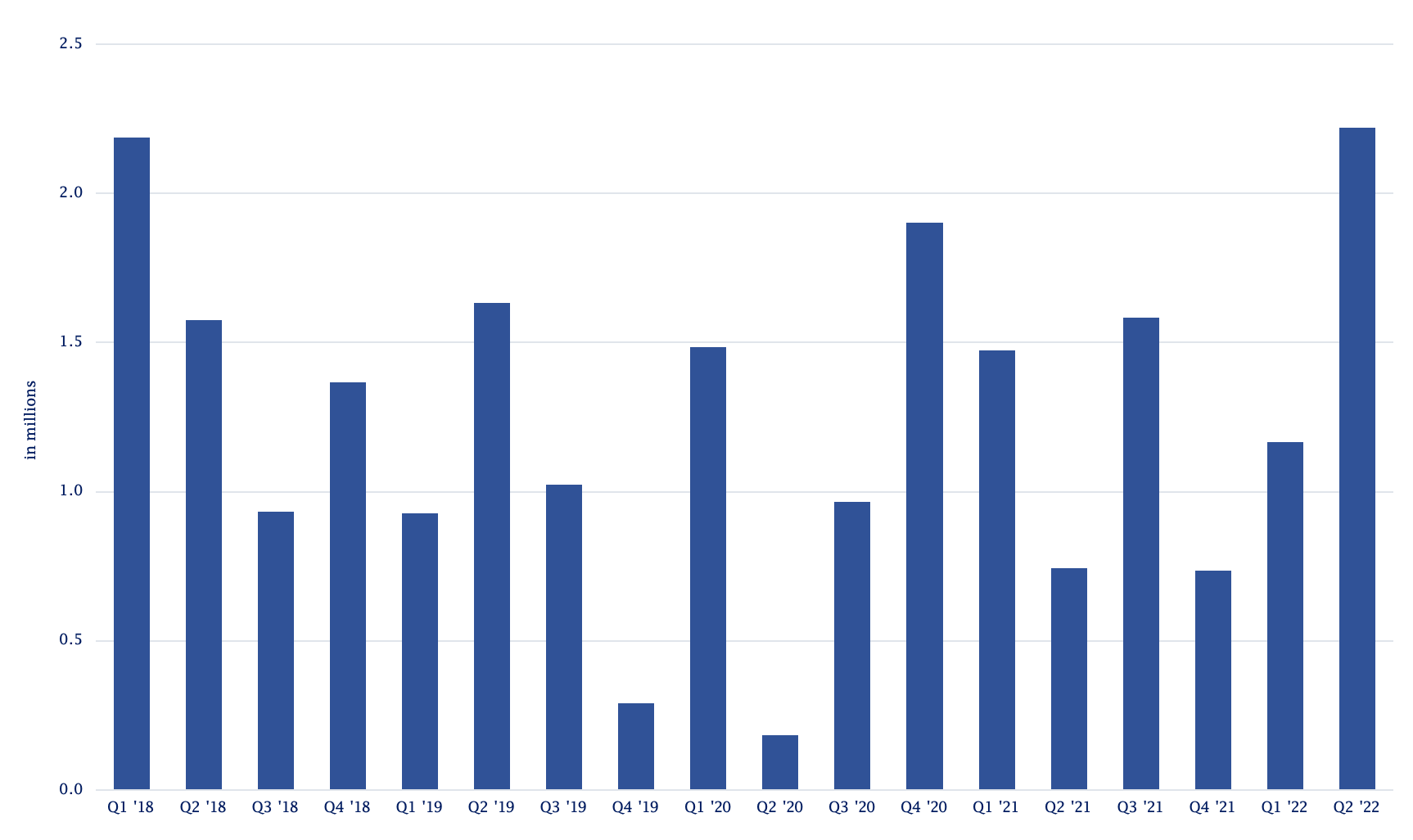

Given the market volatility and considerable correction after its Q1 results, ORLY repurchased 2.219M shares for a total investment of $1.38B. This number marked the busiest buyback activity on record.

ORLY: Quarterly Share Repurchases

{kind=link}

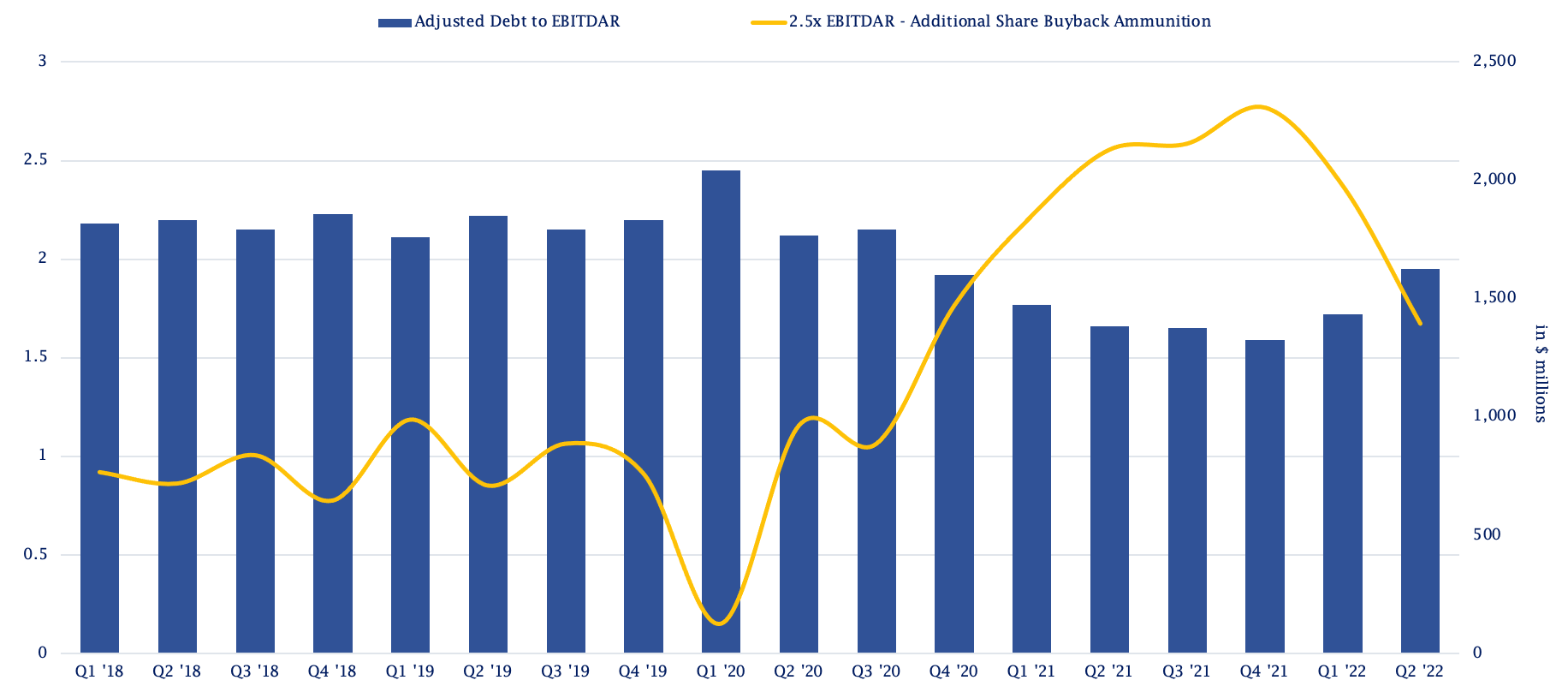

Still, the leverage ratio remains well below management's targeted 2.5 times EBITDAR. If ORLY were to move closer to this figure, buyback firepower equaled $1.39B at the end of June 2022, ignoring all future free cash flow for the remainder of 2022. As CFO Jeremy Fletcher stated during the conference call:

From a repurchase perspective, we continue to feel like we utilize our repurchase program as an effective means of returning capital to our shareholders. And I think for us, over the course of time, it has been successful really because it’s been driven by our ability to be both consistent and drive repurchases really month in, month out because of the consistent nature of our cash flows. But then also when we have opportunities to be opportunistic at times. And I think you probably saw some of that in the first half of the year. That philosophy hasn’t changed. We’ll prioritize our capital for reinvestment in our business because we like those returns to the best. But when we have an opportunity, we’ll execute our buyback program with that same philosophy.

ORLY: Quarterly Leverage Ratio

{kind=link}

Assuming ORLY continues to execute its prudent buyback activity beyond FY22, the total outstanding share count could decrease by roughly 8% per annum.

ORLY: Expected Annual Share Repurchases

{kind=link}

Attractively Valued Despite Short-Term Sales Growth Volatility

Trading at an expected earnings yield of 4.9% for 2022 and 7.1% for 2024, ORLY shares are currently attractively priced. In fact, over the past 12 years, the stock has typically traded at a 1-year forward earnings return of 5.1%. Compared to AZO and AAP, adverse re-valuation risks are moderate for ORLY shareholders. Based on softer-than-anticipated DYI performance, possibly heading into FY23 as well, ORLY's greater tilt toward DIFM justifies a premium. The below graph, though, indicates ORLY shares are now trading at a rare discount.

ORLY vs. Peers: Valuation

{kind=link}

The last time ORLY traded at a forward multiple this low was in 2010, after which it started to substantially outperform both AZO and AAP for several years in a row.

ORLY vs. Peers: Valuation Discount/(Premium)

{kind=link}

Risks to Our Case

Risks to our investment thesis haven't changed materially since our April article. One could rightfully argue that the DYI performance has come in worse than expected, which is much more relevant for AZO and AAP. In that regard, ORLY's more balanced DYI/DIFM split, lower leverage ratio, better ROC and historical undervaluation should mitigate downside risks.

Based on the operational returns ORLY's business currently produces, we believe management's execution in rolling out an omni-channel strategy has been a highly effective one. Although price is an important determinant for its customers, technical expertise and parts availability are the driving factors behind its past and current financial performance.

As the switch towards electric vehicles takes hold, one might question how solid ORLY's long-term prospects are. If we're talking about the short to medium-term outlook for EVs, persisting supply chain constraints and lower demand for automobiles is expected to result in a longer lifetime of existing vehicles and thus more maintenance and repair requirements. In addition to that, steadily rising miles driven as a result of fewer COVID-19 restrictions and a lack of mass transit infrastructure support the long-term outlook for the automotive aftermarket retailers.

Nationwide box stores cannot reach into ORLY's smaller markets, whilst online competitors are not capable of offering a nearby physical location run by experienced employees. The exact same reasons also apply to big-box retailers and online retailers such as Amazon ( AMZN ). As O'Reilly is planning to invest heavily in its inventory base, its moat will undoubtedly widen further.

Furthermore, ORLY's market-leading return on capital makes it a reliable cash-minting business, which helps ward off competition from pure online automotive aftermarket retailers. It is unviable for a company to perpetually generate a negative Return On Invested Capital as it then permanently destroys shareholder value. Hence investors will have to put up more capital to avoid ceasing business activities.

One of ORLY's smaller competitors (with about $650M in annual sales) is CarParts.com ( PRTS ) which positions itself as a disruptor and intrigued many growth investors at the beginning of the pandemic. At-the-market equity offerings have so far managed to keep the company afloat, while the underlying business continues to destroy shareholder value as the gap between return on capital and the weighted average cost of capital remains 25+%. Not the kind of business one wants to be invested in under today's circumstances.

Wrapping Up

Given the solid business prospects, capital-light business model, permanently negative working capital, investment-grade credit rating and below-target leverage ratio, ORLY remains a very appealing long-term cash flow compounder. Our base case scenario yield an IRR of 16.5% when targeting a long-term fixed leverage ratio of 2.0 times EBITDAR, well below management's guidance of 2.5 times. We rate ORLY shares "BUY" for long-term conservative high-quality investors and expect its relative outperformance to continue beyond 2022, given its below-average beta of 0.64.

For further details see:

O'Reilly Automotive: Reiterating Our Bullish View On This Share Buyback Machine