ORLY - O'Reilly Automotive: The Winning Combination Of Buybacks And Market Share Growth

2023-12-14 14:59:18 ET

Summary

- O'Reilly possesses numerous favorable traits, including a large and growing Total Addressable Market, good management, and high and stable returns on capital.

- The auto parts industry exhibits predictability and healthy competition, with O'Reilly holding around 12% market share.

- O'Reilly's competitive advantages include customer service, an efficient distribution system, and the ability to pursue acquisitions for market expansion.

- It has a great culture and management with good incentive metrics.

- Valuation is reasonable, maybe even cheap.

My Thesis

If you've read some of my articles, you probably know that I admire businesses like O'Reilly Automotive ( ORLY ). That's because it possesses numerous favorable traits. O'Reilly has a large and growing Total Addressable Market ((TAM)). The industry is fragmented but consolidating. It boasts good management that has risen from the bottom of the chain.

Additionally, it maintains high and stable returns on capital with a conservative balance sheet. Operating for more than 60 years suggests resilience. Moreover, I believe it is at least trading at its fair price and might even be undervalued.

The Industry

O'Reilly operates in the auto parts industry, where the management believes it holds around 12% market share, placing it right behind AutoZone ( AZO )—a standout business in its own right. Other major players include Advanced Auto Parts ( AAP ) and NAPA, while the rest are regional entities.

The industry exhibits predictability, with a consensus among car companies to offer a seven-year warranty on vehicles. This predictability allows for the anticipation of future demand. The industry introduces the concept of the 'sweet spot,' referring to the period after the warranty has expired but before the vehicle is retired, typically falling within the 8-12-year range. However, with the aging of active cars in recent years, this 'sweet spot' has extended. A notable example was during the recovery from the 2008 recession when increased confidence in driving led to higher vehicle usage, more repairs, and subsequently, higher growth rates in the industry. Factors contributing to industry growth include increasing car sales, greater distances traveled by vehicles, and the aging of cars.

What I appreciate about this industry is that, while not recession-proof, it consists of essential products. Regardless of economic conditions, vehicles age and need repair and maintenance.

The industry exhibits healthy competition. The top players provide excellent services and generate high returns on capital. At least for now, it is not a price-war industry where profits are minimal.

What I Like About O'Reilly

The business is divided into what is called a dual market: the DIY segment, which is the more mature segment primarily serving car enthusiasts and those with the knowledge to 'do it themselves,' and the DIFM segment, which involves selling to local garages. The DIFM segment is the faster-growing one due to its more fragmented market. One of the reasons for the higher revenue growth by O'Reilly as opposed to AZO is that they are more dominant in the DIFM market, with 44% of their sales as opposed to around 30% at AZO.

The main competitive advantages O'Reilly has are their customer service, of which they take great pride. Their personnel are highly trained and adept at serving customers effectively. Furthermore, O'Reilly's distribution system is very efficient, and the management believes it is a key factor in bringing customers back .

More than 95% of our stores receive multiple same-day deliveries and deliveries on weekends of hard to find parts from our DCs and Hub stores. We believe this timely access to a broad range of products is a key competitive advantage in satisfying customer demand and generating repeat business.

Now, as a result of the fragmented market, O'Reilly can pursue acquisitions to enter new markets or enhance their already strong ones. Here is a brief history of their acquisitions, and they intend to continue doing so:

Our intention is to continue to selectively pursue strategic acquisitions that will strengthen our position as a leading automotive aftermarket parts supplier in existing markets and provide a springboard for expansion into new domestic and international markets.

Acquisition History (ORLY 10k)

Another important trait, in my view, is longevity. O'Reilly has been operating since the 1950s, giving it significant brand power and suggesting resilience over time.

Management

Another crucial factor in long-term success is the people and the culture behind the business, as well as their incentive to succeed. O'Reilly has an amazing culture that nurtures executives from the bottom of the chain to the top, ensuring a deep understanding of the business in all its aspects. Just take a look at the resume of the upcoming CEO, Brad Beckham:

Brad's O'Reilly career began as a Parts Specialist and progressed through the roles of Store Manager, District Manager, Region Manager, Divisional Vice President, Vice President of Eastern Store Operations and Sales, Senior Vice President of Central Store Operations and Sales, Executive Vice President of Store Operations and Sales, and Executive Vice President and Chief Operating Officer.

Now, moving on to incentives and compensation; O'Reilly does not have meaningful insider ownership, besides the two original O'Reillys, David and Larry, who together hold about 400k shares. Though it is not even 1% of shares outstanding, it does give the business a touch of Family-Owned Business (FOB), which tends to outperform over time.

While the executives might not have a significant number of shares in total, I would bet that most of their fortunes are linked to O'Reilly equity in stock or future bonuses, given that they have been with the company throughout their careers. This factor potentially gives them a shareholder's perspective in my view.

The compensation plan is solid, and what I particularly like is their metrics to measure performance. While many companies focus on the obvious metrics like EPS and revenue, O'Reilly's focus is on the Return on Invested Capital of the business, its free cash flow, and the same-store sales. Around 70% of the CEO's compensation is in equity, incentivizing for the long term. Directors also have about 50% of their compensation in equity, with minimal stock-based compensation affecting the operating cash flow.

The Important Numbers

So, the main quantitative factor that motivates me to own this business is its remarkable efficiency and profitability. Recent research by Michael Mauboussin suggests that a high and growing spread between a business's ROIC and its WACC is a common trait among successful companies. Not only are O'Reilly's returns consistently high, but they have also remained elevated for an extended period, indicating resilience and sustained profitable growth.

Those returns are a result of the high and resilient margins that O'Reilly possesses, which are particularly impressive for a retailer. In the recent quarter, it observed a 14% free cash flow margin. These margins are also experiencing modest growth, creating an operating leverage. High margins are crucial, especially in the case of inflation when costs are rising, and not every company has the pricing power to pass these increases onto consumers. In such instances, a substantial margin of safety is important, ensuring the company won't need to cut future investments or buybacks/dividends.

Now, a crucial aspect of my thesis and the valuation revolves around the buybacks O'Reilly is undertaking. These buybacks play a vital role in the long-term free cash flow per share growth rate. The company is consistently reducing its share count by 4-5% each year. This constitutes a tangible growth factor over the long term and is one of the key contributors to its outstanding returns over the last decade.

O'Reilly possesses a conservative balance sheet. It can cover its net debt with about two years of free cash flow. With an Altman Z score above 3 and an interest coverage ratio of 17, it exhibits financial strength. Most of the debt carries around 3-4% interest, making it reasonably priced, and more than half of the debt matures after 2027. While it may not be the best balance sheet I've ever seen, I don't perceive any meaningful risks at this point.

Growth and Valuation

To value the company, we will need to estimate its growth rates. In contrast to other companies, here the management is assisting us by providing a longer-term range of future growth:

I would like to highlight our updated four-year sales guidance. We have increased our four-year comparable store sales guidance to a range of 7%-8% from our previous range of 5%-7%.

So based on these factors, I assume a 7-8% compound growth, and on top of that, I'll assume a 2-3% store count growth per year, drawing from past expansions, whether through acquisitions or store expansions. This gives us a total of 9-11% sales growth. Additionally, I'll factor in a 4-5% reduction in share count per year. Without assuming margin growth or deterioration, we have a 13-16% free cash flow per share growth in the next couple of years. These are outstanding growth numbers for a mature company, and they make sense as O'Reilly's market share is still relatively small, and the market is consolidating. Of course, these are based on various assumptions, and while these growth rates may seem a bit optimistic, I don't believe they are overly so.

So, almost a 4% free cash flow yield and a forward 25 earnings multiple are not cheap, even for such high quality. However, I do think it is not overvalued by much. Paying a 25 multiple for a predictable company with above a 50% ROCE and double-digit free cash flow per share growth is reasonable, in my opinion. My philosophy is to buy high-quality businesses at a reasonable price for the long term, and I believe this is the case here.

I'm not particularly fond of DCF models because they often fall short, filled with assumptions. However, they can offer a different perspective on the business.

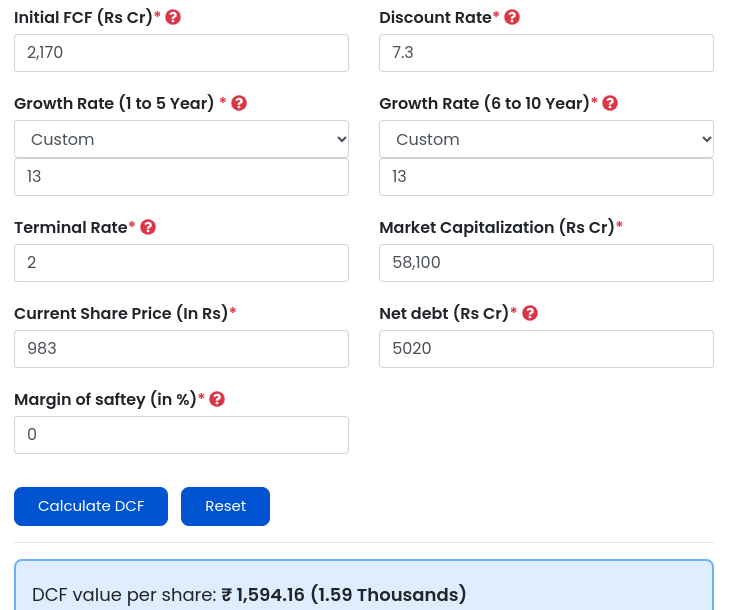

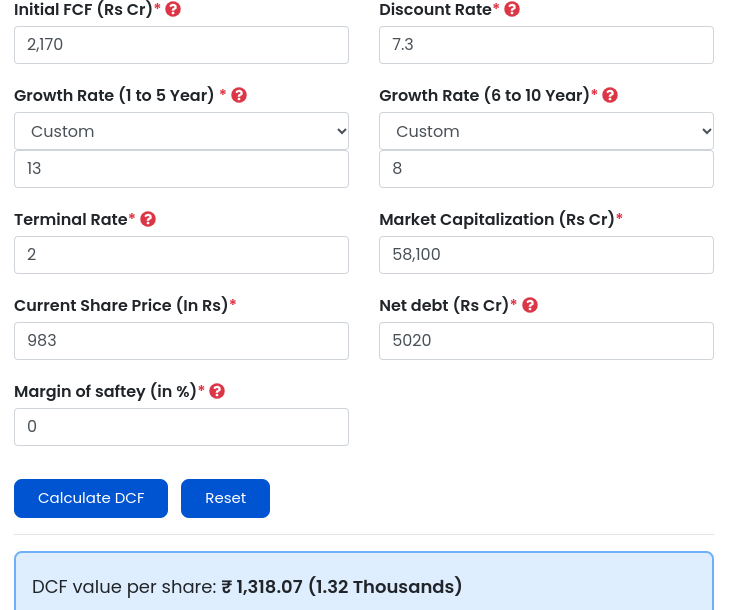

Using the average free cash flow margin over the last 10 years of 14%, assuming a 2% terminal growth, a WACC of 7.3%, and the lower 13% growth rate we assumed, we find a 38% undervalued business. Now, I don't anticipate the 13% growth rates to persist after 5 years as the industry consolidates and store count growth slows. Let's assume 3% comp sales growth and 1% store count growth, resulting in 8% free cash flow per share growth with buybacks. In such a scenario, the model suggests the business is still undervalued by 25%.

wacc (author) DCF (finology) DCF (finology)

{kind=link}

{kind=link}

Risk

Perhaps the most significant risk for ORLY's business is the transition to electric vehicles. EVs have fewer spare parts compared to internal combustion vehicles and generally require less maintenance and repair, directly impacting ORLY's business. As of October 12th, EVs accounted for 7.9% of the car industry sales, which, while still relatively low, is steadily growing. This marked a record high and a 50% growth over the past year.

However, I believe two factors may work in ORLY's favor. First, this risk has been evident for a while now, giving the management time to prepare and make necessary changes. Second, as EV innovation advances, more technologies and, consequently, more parts will be needed for these vehicles. In the future, as EVs capture a larger share of car sales, they may become even more complex than internal combustion vehicles.

Another risk is the CEO transition, which is always challenging, but since he grew up in the business, I do think it won't be a significant obstacle.

And, of course, there's competition. ORLY has great competitors, and although a pricing war is unlikely, it can erode margins.

Conclusions

Considering the price and the quality, I believe we have a future winner here. While there are risks, I don't perceive them as major hurdles. The combination of culture, brand, efficiency, and growth are massive value creators. Therefore, I rate O'Reilly as a Strong Buy.

What are your thoughts on the business?

For further details see:

O'Reilly Automotive: The Winning Combination Of Buybacks And Market Share Growth