ORLY - O'Reilly: This Fantastic Stock Is Too Expensive

2023-03-22 02:31:00 ET

Summary

- O'Reilly Automotive operates as an automotive aftermarket retailer and supplier in the United States.

- Rising fuel prices, greater competition from e-commerce, and the EV transition have the opportunity to slow demand in the coming months.

- These headwinds are counterbalanced by an inflated secondary car market and current economic conditions.

- O'Reilly's financials are incredibly attractive, with impressive profitability and unwavering growth. The business has rewarded investors through mammoth buybacks.

- Our valuation, alongside SA's quant, considers this business overvalued. With headwinds in the near term, we rate ORLY stock a hold.

O'Reilly's profile:

O'Reilly Automotive, Inc. ( ORLY ) operates as an automotive aftermarket retailer and supplier in the United States. The company offers a wide range of automotive parts, tools, and accessories, including new and remanufactured hard parts, maintenance items, automotive body paint and related materials, automotive tools, and professional service provider equipment. The company serves both do-it-yourself and professional service provider customers.

The share price of ORLY has experienced a remarkable decade, with only a brief period of poor performance surrounded by consistent and substantial gains. This has been due to sustainable continuing growth and this translates into shareholder value.

Investment thesis:

ORLY is a strong and consistent performance, characterized by its resilience. This makes it an attractive option for long-term investors, as there are no unexpected negative surprises, allowing them to hold the stock for a prolonged period without worry. Chuck Akre, a long-time supporter of the company, views ORLY as a compounder, aligning with his three-legged stool. However, his fund has recently reduced its position ( Source: Tikr Terminal ), and the stock has hit an all-time high amidst a weakening economy. This analysis aims to evaluate the underlying business fundamentals and examine the potential outlook for 2023, with the view to assessing if we are in a period of consolidation.

Fuel prices are reducing miles driven:

One of the supply-side disruptions we reference above is the sharp uptick in energy prices, driven by the economic response to the War in Ukraine.

This has resulted in a substantial rise in gasoline prices globally. This has had the effect of compounding consumers' cost of living woes, leading to many seeking alternative transportation options. With fewer miles being driven, maintenance spending will naturally decline. Further, one of these alternative transportation methods could be EVs, which generally have lower maintenance requirements.

Our view is that this is a short-term threat that will soften demand rather than fundamentally change the economics of the industry.

EVs pose the threat of obsolescence

The rise of EVs is having a negative impact on the automotive parts industry, particularly for traditional gasoline engine parts. With the shift towards EVs, demand for traditional parts such as spark plugs, fuel injectors, and fuel pumps has decreased, while demand for EV-specific parts such as batteries, electric motors, and power electronics has increased.

EVs have fewer parts overall than gasoline vehicles, which further reduces demand for traditional automotive parts. As the EV market continues to grow, it is expected that the impact on the automotive parts industry will only become more pronounced.

There is a real risk that the business loses prominence in the coming decades, however, it is far too early to be certain of this. Much will rest on how Management looks to transition the business, as there is scope for development through such things as agreements with OEM suppliers.

E-commerce is creating greater competition

The growth of e-commerce retail has been a major trend in the last 2 decades, accelerating in recent years. The automotive aftermarket industry is no exception to this. Online sales of automotive parts and accessories have been growing for ORLY, especially with individuals increasingly seeking to do work themselves. Further, traditional retailers, such as Walmart, have been expanding their offerings in the automotive aftermarket space.

ORLY has done well to expand into the e-commerce retail space, given its large store presence, and it is one of the reasons they have been able to maintain growth. ORLY allows its customers to purchase goods online and either have them delivered to their home or to a local store, thus ensuring consumers get a heightened level of convenience from going to them v. say Amazon.

This is one of the biggest risks the industry has faced in the last decade. We have yet to see it cause a material shift in demand, however, which suggests ORLY is holding its own.

Economic considerations will soften growth

We are seemingly at an economic crossroads with demand having materially cooled and inflation inching down. The question is whether it will decline fast enough for economies to avoid a recession, and all for the kickstarting of expansionary policy.

Inflationary pressures have impacted both retail businesses and consumers, with higher prices and costs. The economic response has been to raise interest rates, with the object to cool demand. As the below graph illustrates, this has been successful but is clearly not incredibly effective. It is slow in action.

Looking ahead to the coming 12 months, our outlook is further uncertainty. Demand will likely continue to decline as interest rates remain in excess of 4%, contributing to declining consumer sentiment and businesses becoming fiscally protective. Inflation will likely return to a sustainable level in Q4-23/Q1'24.

This may result in a slowdown of growth for ORLY, as people may choose to put off making large purchases. However, we do not anticipate a decline in revenue as most individuals / businesses depend on their vehicles for income and are unlikely to risk further expenses by not conducting maintenance. Additionally, during tough economic times, people are more likely to maintain or purchase older vehicles rather than buy new ones, leading to increased spending on maintenance.

ORLY has responded to the DIY movement

The do-it-yourself (DIY) market has been growing as more people take on car maintenance and repairs themselves. This trend is driven by the rising cost of labor, which makes DIY a more cost-effective option for many consumers. Current economic conditions have only accelerated this trend. ORLY has leaned into this market, by providing consumers with advice to assist in the DIY process.

O'Reilly Website (O'Reilly) O'Reilly Website (2) (O'Reilly)

{kind=link}

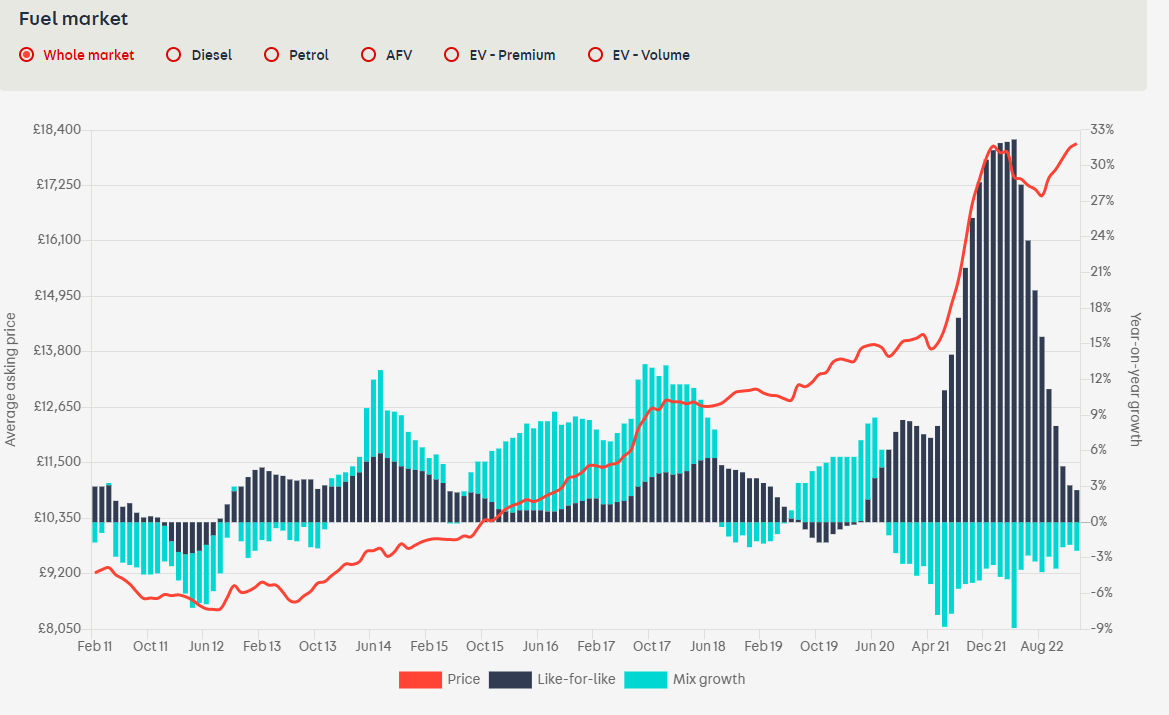

The second-hand market is getting expensive

The second-hand vehicle market has seen an unusual trend in recent years, with prices increasing quite noticeably. The following is a graph of UK average asking prices on Autotrader, the largest online marketplace. A similar trend is observed across most western nations.

Average Asking Price (Autotrader)

{kind=link}

The primary reason for this is automakers struggling to produce vehicles to meet demand. The well-publicized chip shortage is the specific supply-side issue that has delayed production. Given this reality, consumers and businesses have been forced to purchase older and cheaper vehicles, accelerating the average vehicle age. Our view is that this will inevitably lead to greater demand for parts in the coming years.

ORLY's financial performance has been incredible

P&L (CapIQ)

Over the past 7 years, ORLY has experienced a growth rate of 9% in its revenue, due to both the consistent growth of its like-for-like sales and the addition of new locations. In the last quarter, comparable sales increased by a remarkable 9.0%. Further, despite the impact of the pandemic, the business still managed to grow. This showcases the strength of ORLY as a sustainable compounder and highlights the capabilities of its management and the resilience of the US automotive industry.

ORLY boasts an extremely appealing profitability profile, with a low-to-mid teen net income margin and a similar unlevered free cash flow yield. This is due to their strong pricing power in the industry and their ability to achieve economies of scale. Although margins have declined in recent times due to supply-side challenges causing higher costs, they are still higher compared to the pre-pandemic period.

Balance sheet (CapIQ)

ORLY's balance sheet is equally as strong. The business is continuing to make operational improvements, with its inventory turnover and CCC improving Y/Y.

Further, the business has utilized its FCF and debt-bearing capacity to return value to shareholders through buybacks.

Overall, it is clear that ORLY is an elite business that is effectively printing money Y/Y. Management has remained relentless in achieving incremental improvements, which should be highly beneficial in the short term. Our view is that demand will soften due to temporary headwinds, which likely means the growth in the coming years will be closer to 3-5%.

ORLY is slightly overvalued:

Given the impressive profile of the business, it is not surprising to see that it is trading at a premium to the automotive parts industry as a whole. Seeking Alpha's quant rating is currently a hold, primarily driven by what it perceives to be an elevated valuation and poor growth.

Quant Valuation (Seeking Alpha)

To verify this view, we performed a discounted cash flow valuation of ORLY. The key assumptions made in the valuation are:

- EBITDA growth of 5%, half that of the prior 6 years. This reflects the weakening conditions forecast.

- FCF conversion improves marginally, as further operational efficiencies are made.

- An exit multiple of 15x, which is above ORLY's historical average of 12x but below its current 18x.

- Perpetual growth rate of 2.75% and a discount rate of 8%.

Based on these criteria, we derive a downside of 5%. With the margin for error in mind, this suggests ORLY is trading at its fair value.

If we were to increase the exit multiple to 18x, we would only have an upside of 6%. Further, if we increased the initial growth rate of 5% to 7.5%, the upside would again only increase to 6%.

Final thoughts:

ORLY is an exceptional company that is growing in a sustainable manner across all aspects of the business. Although there may be short-term challenges ahead that could decrease demand, these will not change the overall upward trajectory of the company long-term. The electric vehicle transition could be a factor, but it is too early to determine its impact.

With limited upside potential as determined by our valuation, we consider this stock to be a hold. However, if growth slows, it may lead to a re-rating of the stock.

For further details see:

O'Reilly: This Fantastic Stock Is Too Expensive