BXSL - Oaktree Or New Mountain For Solid 11% Yield?

2023-07-19 15:17:08 ET

Summary

- This article discusses dividend coverage for two BDCs currently yielding around 11% including supplemental dividends.

- We suggest one of these companies with a list of positives that investors should consider.

- One of the largest mistakes that BDC investors make is focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality.

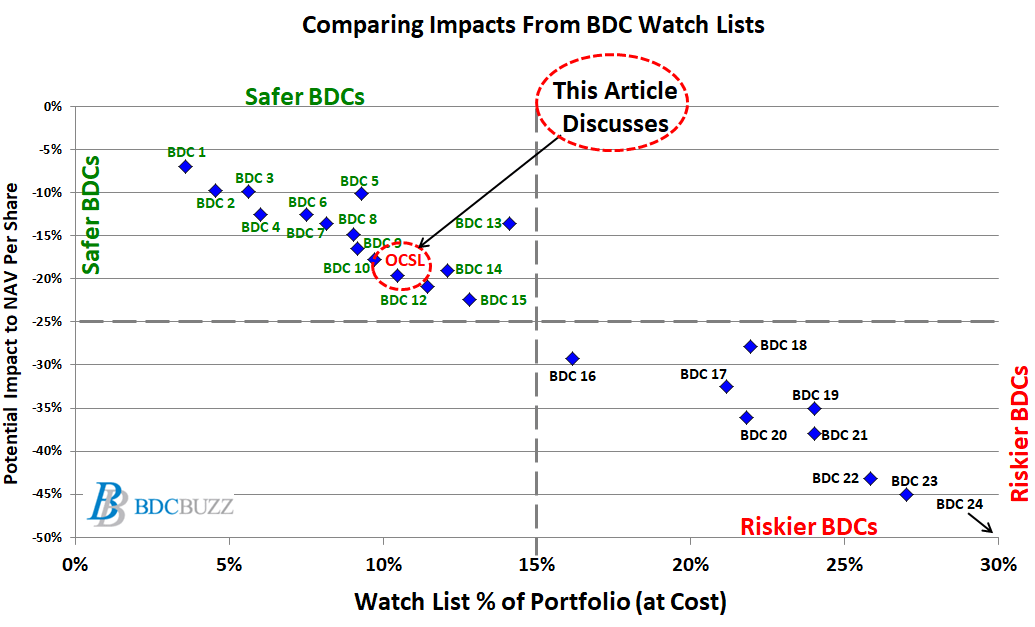

- Please see the chart at the end of this article comparing the potential impact on NAV per share, assuming that 100% of watch list investments (including non-accruals) defaulted with 0% recovery.

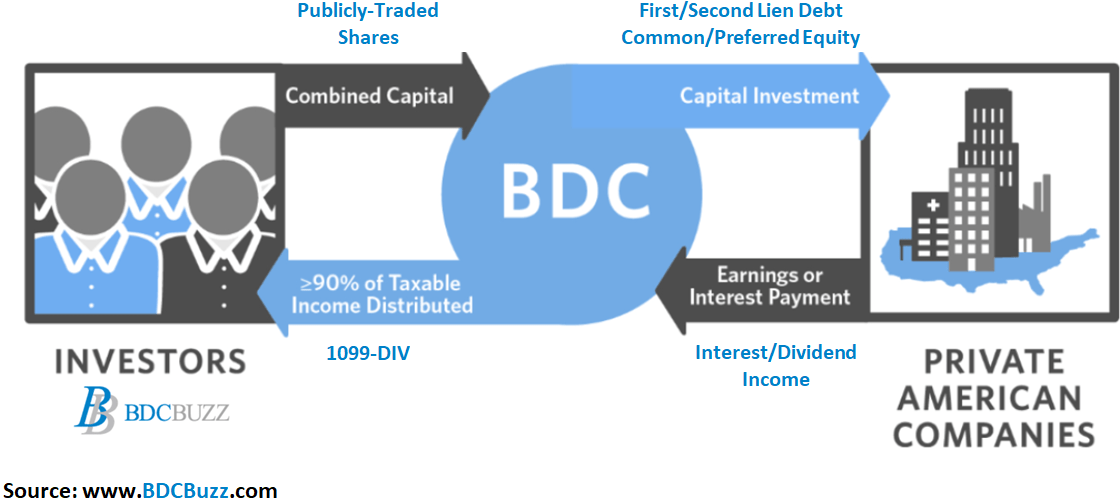

Quick Introduction To Business Development Companies

Business development companies ("BDCs") invest shareholder capital in privately-owned, small- and medium-sized U.S. companies generating income from secured loans and capital gains from equity positions, much like venture capital or private equity funds. Anyone can invest in BDCs as they're public companies traded on major stock exchanges.

{kind=link}

The three biggest mistakes that new BDC investors make are:

- Focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality.

- Not taking the time to dig into portfolio credit quality and assess which investments could potentially have a negative impact on earnings and NAV per share.

- Not understanding why BDCs trade at different prices and thinking that price-to-NAV is the only measure to find a "good deal." Please see the end of this article for a quick discussion of how BDCs are valued.

This article discusses dividend coverage for Oaktree Specialty Lending ( OCSL ) and New Mountain Finance ( NMFC ) which currently have dividend yields of around 11% including supplemental dividends (discussed below). At the end of the article, I pick one of these BDCs and compare the potential impact on net asset value ("NAV") per share assuming that 100% of its watch list investments (including non-accruals) defaulted with 0% recovery.

{kind=link}

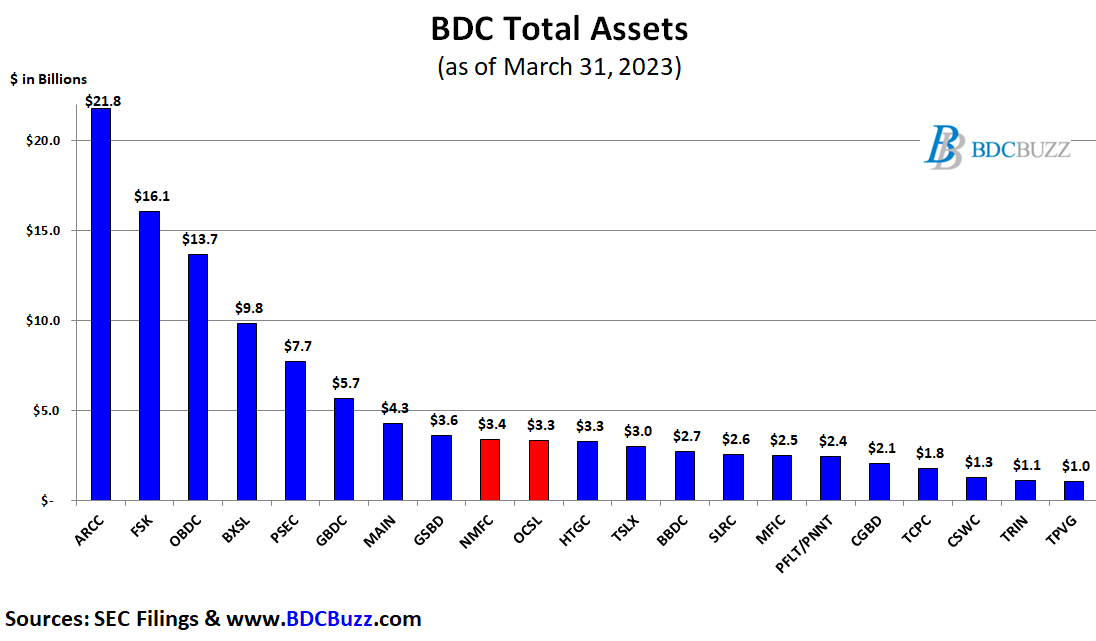

Please note that the BDCs in the chart above account for around 90% of the total assets and market capitalization for the sector. Over the last six weeks, we discussed the portfolio credit quality and/or dividend coverage for many of them including Ares Capital ( ARCC ), FS KKR Capital ( FSK ), Prospect Capital ( PSEC ), Goldman Sachs BDC ( GSBD ), Hercules Capital ( HTGC ), PennantPark Floating Rate Capital ( PFLT ), PennantPark Investment ( PNNT ), TriplePoint Venture Growth ( TPVG ), Monroe Capital ( MRCC ), and BlackRock TCP Capital ( TCPC ) in the following articles:

- Ares Capital 10% Yield: Need To Check Credit Quality

- Better High-Yield Buy: FSK or PSEC?

- PennantPark: Big Win From Dominion/Fox Settlement

- Venture Debt Opportunity Yielding 13% To 14%: HTGC or TPVG?

- BlackRock Or PennantPark For Solid 12% Yield?

- Safer 12% Yield: Goldman Sachs BDC or Monroe Capital

BDC Buzz & SEC Filings

Later this week, we will discuss dividend coverage for ARCC which is reporting Q2 2023 results next week:

BDC Buzz & SEC Filings

Comparing Dividend Coverage

As mentioned earlier, one of the largest mistakes that BDC investors make is focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality. Each quarter I update the financial projections for each BDC with base, best, and worst-case scenarios to test the sustainability and/or changes to the current dividends. Below I discuss many of the drivers used for projecting dividend coverage.

NMFC

NMFC's dividend yield has been consistently covered, with a defensively positioned portfolio and management that exhibits higher quality indicators including waived management fees and a look-back feature for the capital gains portion of the incentive fee. However, NMFC does not have a best-of-breed fee structure due to income incentive fees not taking into account realized or unrealized losses.

Previously, the company reduced its quarterly dividend from $0.34 to $0.30 starting in Q2 2020, which was predicted in previous reports. At the time, the company had spillover or undistributed taxable income (“UTI”) which is typically used for temporary dividend coverage issues . Please do not rely on UTI as an indicator of a "safe" dividend.

In November 2022, NMFC increased its regular quarterly dividend to $0.32 per share and management has “committed to paying quarterly dividends of at least $0.32” through Dec. 31, 2023 , with additional fee waivers. There's a good chance that management would extend the fee waivers, but will likely not be needed:

The investment adviser has committed to a management fee of 1.25% for the 2023 calendar year. We have also pledged to reduce our incentive fee if and as needed during this period to fully support the $0.32 per share quarterly dividend. Based on our forward view of the earnings power of the business, we do not expect to use this pledge. It is important to note that the investment adviser cannot recoup fees previously waived.

NMFC has adopted a formula-based quarterly supplemental dividend program in an amount to be determined each quarter calculated at 50% of earnings in excess of the regular dividend.

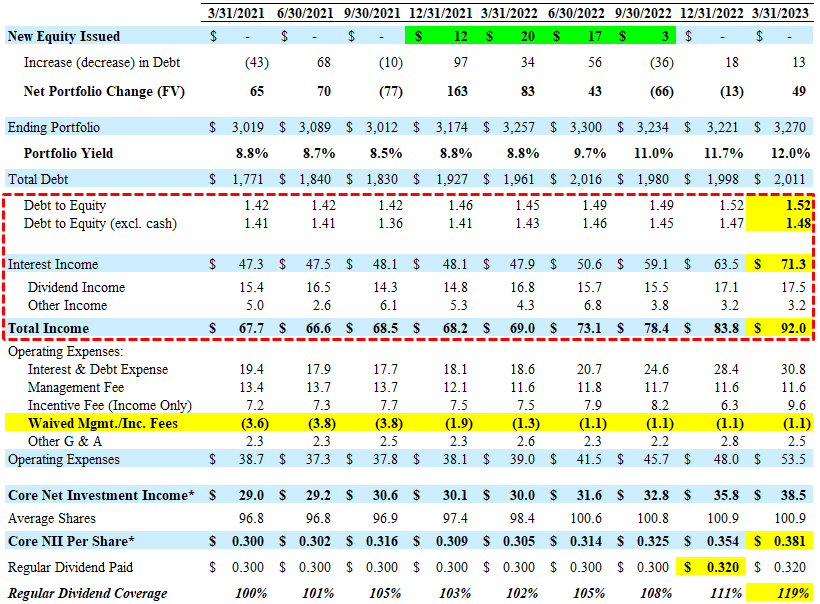

For Q1 2023, NMFC reported between my base and best-case projections due to higher-than-expected dividend income while maintaining higher leverage partially offset by continued lower other income, covering its dividend by 119%. In May 2023, the company reaffirmed its regular quarterly dividend of $0.32 per share plus a supplemental dividend of $0.03 per share paid in Q2 2023.

{kind=link}

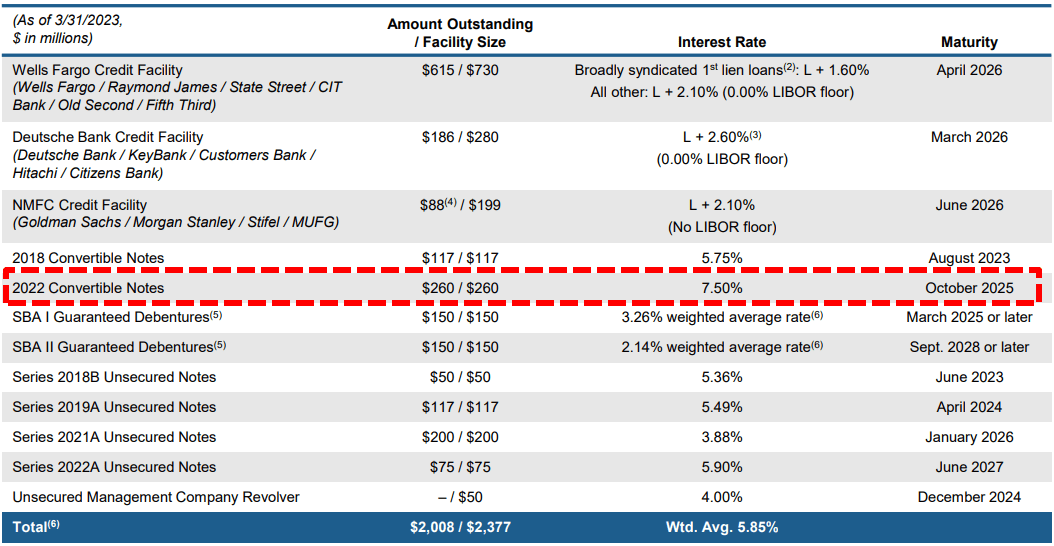

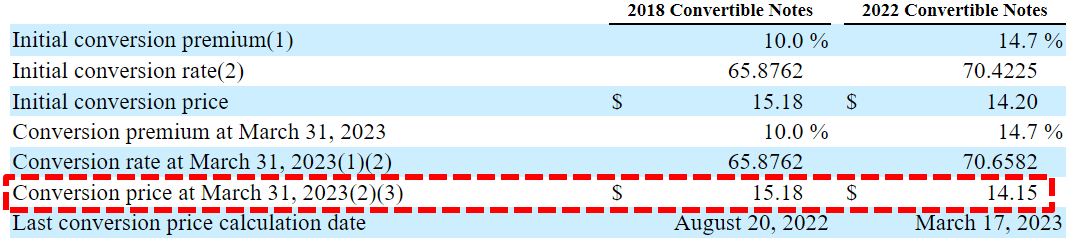

In November 2022, NMFC issued $200 million of its 7.50% convertible notes due Oct. 15, 2025, and used the proceeds to launch a tender offer for its existing 5.75% Convertible Notes. On March 14, 2023, the company issued an additional $60 million of convertible notes to repay the 2018 unsecured notes which have been taken into account with the updated projections.

{kind=link}

These 2022 notes are currently convertible at $14.15 per share which is only around 7.7% above the current NAV and could be an overhang on NMFC’s stock price . Also, as shown in a previous chart/table, “a 10% change in the FMV or our equity positions impacts book value by $0.30 per share” implying that additional appreciation of these investments could drive NAV closer to the conversion price.

{kind=link}

During Q4 2022, its $46 million first-lien position in Haven Midstream was repaid and there will likely be another $10 million or $0.10 per share of realized gains in Q2 2023 due to a recent equity distribution:

Q. “Did you say you received a $10 million distribution from one of your equity investments, did get that correctly? And then, if so, what investment was that from and how should we expect that to be accounted for in the second quarter?”

A. “Yeah, you did hear that correctly. So this was from our Haven position, which was an equity distribution, in addition to the payments that we have already received through Q1. This was one that we received on this past Friday for an additional $10 million and so that will show up as an equity distribution in Q2. It will be a realized gain .”

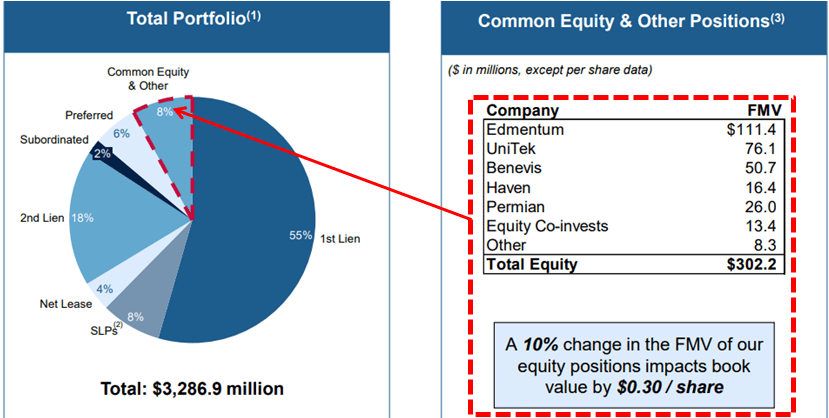

NMFC previously had around $36 million or $0.35 per share of net realized gains mostly related to net lease investments, as management was in the process of "reducing overall exposure with the goal of reinvesting sales proceeds into core strategy of a floating rate defensive growth-oriented private credit." However, over the last 10 years, NMFC has experienced net realized losses of around $31 million or $0.31 per share (using the current share count). NMFC’s net asset value (NAV or book value) has declined by only $0.92 per share since 2012 due to offsetting unrealized gains and over-earning the dividend. Also, there's a good chance that many of its equity positions will appreciate over the coming quarters and could drive upcoming realizations to be reinvested into income-producing assets:

We have significant control over the monetization of UniTek, Benevis, Permian . It meant it’s worth noting we are a minority and we are in with others. And I would say that, while it’s not a perfect M&A environment, I think, sponsors do want to -- and other buyers, frankly, are getting eager to buy good, well-performing assets. I think we mentioned that UniTek and Permian were two on this list that are growing nicely and have some really compelling structurally advantageous tailwinds and so we are -- we think that among this list, there could be another name on this list that over the medium term we could seek to exit .”

{kind=link}

Management discussed its investment in Edmentum on the recent call as it continues to be marked higher and now accounts for almost 4% of the portfolio fair value (as shown below).

Edmentum is very well positioned to benefit from the trends in artificial intelligence. Edmentum is a digitally native provider of curriculum and assessment primarily for the K-12 market. And because they are digitally native, they have been - they are software first and they have been thinking about AI for a long time and their most recent product incorporated non-generative AI in a material way, and in the recent months, the company has been really front footed on incorporating a generative AI into the product set. We sell to districts. So the districts, they don’t move as quickly as a 14-year-old kid in terms of embracing ChatGPT for assessment and curriculum. But they will get there. And so it’s funny, right now, what they are requesting from Edmentum is to accept the requesting anything and most aren’t, but they are requesting help on the plagiarism side and where they would able to provide that. But as we look out two years or three years, we do believe that the biggest driver is going to be the ability to evolve assessment beyond recitation effects and writing papers. And we believe there are ways to use our software to allow districts to provide an effective answer to that, as well as using our software to provide personalized tutors to children. So longwinded answer, but we are pretty excited about the ability of generative AI to be a tailwind for Edmentum going forward.”

BDC Buzz & SEC Filings

There's a chance for another dividend increase back to the previous level but also could be used for continued supplemental dividends. The dividend yield of 11% shown earlier assumes that the company maintains the regular dividend plus $0.10 per share of supplemental dividends paid annually.

We expect to continue to significantly out earn our $0.32 per share base dividend at current interest rates, if all other factors hold constant. Given our earnings of $0.38 per share this quarter, we will make our first variable supplemental dividend in the amount of $0.03 per share. This is equal to half of the Q1 quarterly earnings in excess of our base dividend of $0.32. This additional $0.03 dividend will raise the total dividend to $0.35 per share all in for this quarter, which is at the high end of the range. Our supplemental dividend program pays out at least 50% of any earnings in excess of the regular dividend. Since our Q1 earnings exceeded the regular dividend by $0.06 per share, we are paying a supplemental dividend of $0.03 per share alongside the Q2 regular dividend.”

Based on Q2 2023 earnings expectations, the Q3 supplemental dividend will likely be $0.03 to $0.04 per share:

{kind=link}

{kind=link}

One of my primary concerns is the need for higher amounts of leverage (debt-to-equity) to cover its regular dividend as well as previously realized losses. Also, NMFC has higher amounts of non-cash payment-in-kind (“PIK”) interest income that has historically been around 10% to 12% of total interest income but increased to almost 13% for Q1 2023 , and needs to be watched.

OCSL

OCSL has increased its regular quarterly dividend 11 times, from $0.285 (Q2 2020) to the current 0.550 per share:

Given the strong overall earnings, our Board maintained our quarterly dividend at $0.55 per share. As a reminder, this is nearly double our pre pandemic quarterly run rate of $0.285. We've been very conservative in our approach to the dividend. This quarter, the adjusted investment income was $0.62, the dividend was $0.55. So I think there's a lot of conservatism in that. But just owing to uncertainty and volatility in the market without prudent just to - let's just kind of keep it at $0.55 for this quarter. We have increased it really almost double the pre pandemic. But at this point, the dividend yield on NAV is north of 11% . Our ROE for the quarter was north of 12.5%. So we feel very good about the dividend coverage, very good about the earnings and the ROE, but just kind of given all the uncertainty out there it seem to make sense to just keep at $0.55. So that's really kind of how we thought about the dividend for this quarter.”

{kind=link}

Similar to other BDCs, during 2022, management decided to payout a good portion of its excess earnings/gains to avoid excise tax and "return the capital to the shareholders." I'm expecting the company to pay another special dividend in Q4 2023 that will likely be announced later this year.

From previous call: “Our Board also declared a special distribution of $0.14 per share (or $0.42 per share split-adjusted), primarily as a result of increased taxable income. It's the first time we've paid this dividend. But at end of the day, the decision was, let's return the capital to the shareholders . Let's not pay the excise tax . There is an excise tax like 4%. So, in essence, let's return all the capital to the shareholders, let them redeploy it as they see fit rather than kind of using it to build that or fund internally and pay the tax. I know some of our peers do different things. But for us, it was - let's avoid the excise tax, let's pay the distribution to the shareholders. We looked at what our taxable income was for the year, what we would need to pay out to try to minimize or outright avoid that excise tax, and that's where we shook out.”

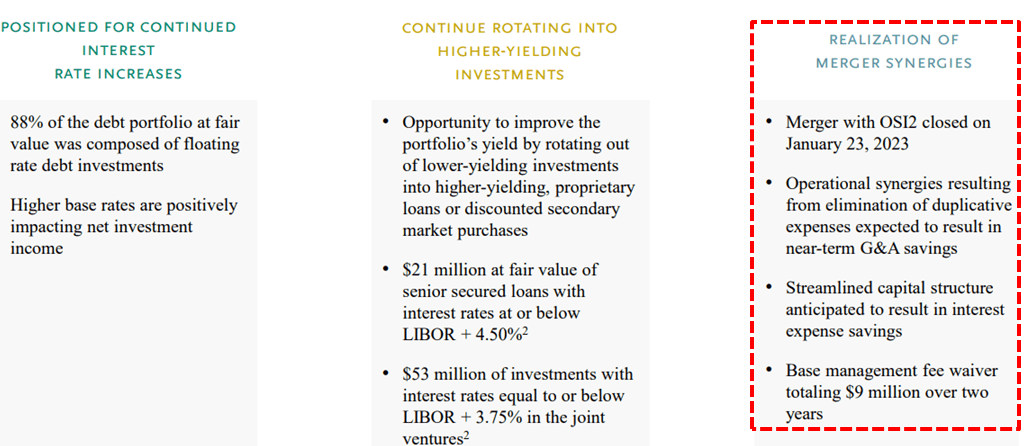

In January 2023, the company completed the merger with OSI2 which is mostly positive for OCSL shareholders, including $572 million of new investments at fair value and the $9 million of fee waivers starting in Q1 2023, just as the previous waivers from the OCSI end.

We successfully closed our merger with OSI2 in January and we believe the combination will result in significant benefits for the combined company and substantial long term value for our shareholders. With more than $3.3 billion of assets, the combined company has more financial flexibility and greater scale, while adhering to our value driven investment strategy. We also anticipate realizing operational synergies as well as interest expense savings from streamlining our capital structure. In addition, we are benefiting from reduced management fees for the next two years at Oaktree, our manager has agreed to waive $9 million of base management fees in total, $6 million in the first year and $3 million in the second year.”

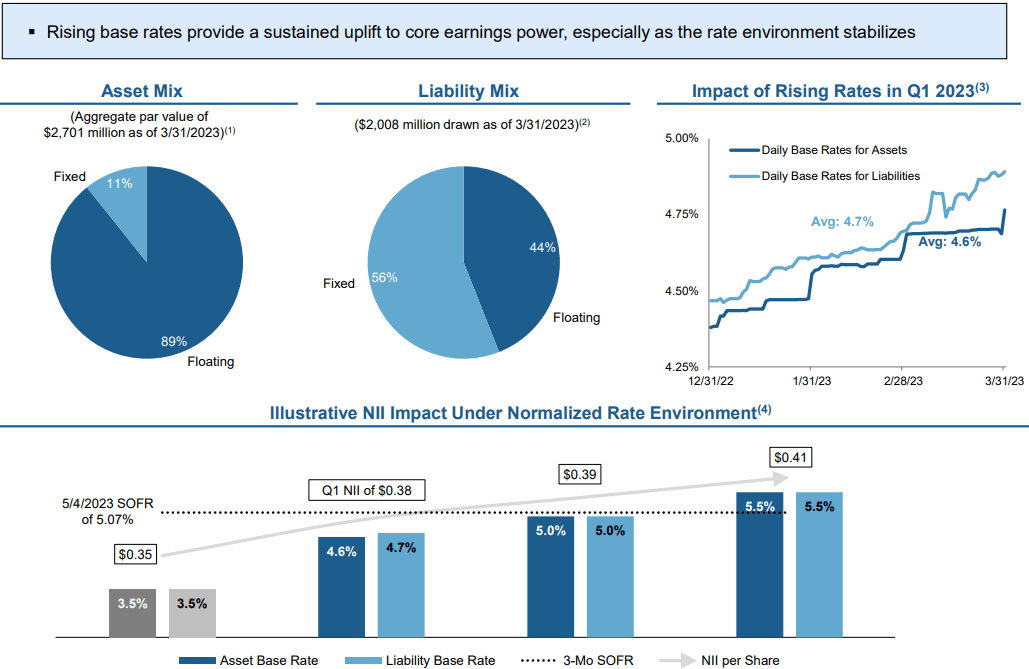

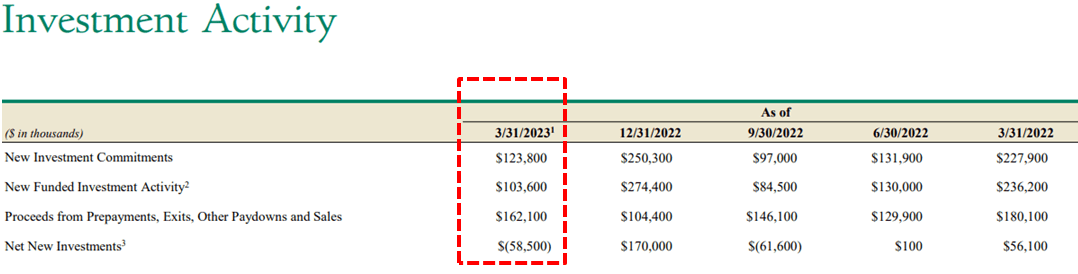

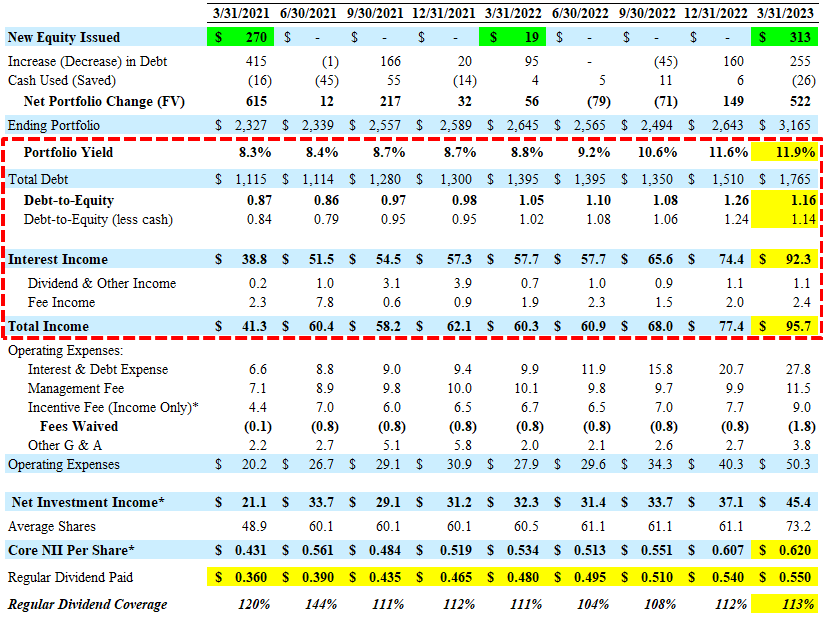

For calendar Q1 2023, OCSL reported between its base and best case projections covering its dividend by 113% with another increase in portfolio yield from 11.6% to 11.9% partially offset by lower portfolio investment activity resulting in lower leverage (debt-to-equity) that is now firmly within its revised targeted ratio of 0.90 to 1.25, currently at 1.14 (net of cash), down from 1.24 (prior to the merger).

{kind=link}

There was a meaningful reduction in the amount of payment-in-kind (“PIK”) income, from 7.9% to 4.3% of total income. OCSL has an excellent history of credit quality and continues to invest in larger companies that would likely outperform in a recessionary environment, so a higher amount of PIK is acceptable, but I will continue to watch over the coming quarters.

{kind=link}

Dividend coverage should continue to improve due to higher portfolio yield, maintaining higher leverage, continued rotation into higher yield investments, increased returns from its Kemper and Glick joint ventures, and the recent merger with additional fee waivers.

Armen Panossian , CEO and CIO: “OCSL achieved strong results in the second fiscal quarter, driven by solid adjusted net investment income generated from wider spreads on new originations and the impact of higher base rates on our predominantly floating rate loan portfolio. We also continued our strategy of rotating out of public debt investments and redeploying capital into our robust pipeline of compelling and higher-yielding private credit opportunities. Moreover, we were delighted to successfully close our merger with OSI2 on January 23, 2023, which marked another significant highlight of the quarter. We are excited to leverage the benefits of the combined company, which we believe will generate substantial long-term value for our shareholders. These positive results underscore our commitment to delivering strong risk-adjusted returns, and we believe we are positioned to sustain this momentum in the future.”

{kind=link}

BDCs are expected to benefit from tightened lending policies and potentially increased banking regulations, which will likely include stronger capital and liquidity standards for certain banks. BDCs have a distinct advantage over banks in that they have “permanent equity capital” and are not subject to “runs on the bank,” which could lead to the forced liquidation of undervalued assets. The recent instability in the banking sector is likely to have a considerable effect on BDCs, resulting in continued improvement in yields on new investments and a wider range of investment opportunities. As a result, BDCs can continue to be very selective in their new investment choices. Earlier this month, OCSL management mentioned the more lender-friendly environment with better terms, including stronger covenants (safer investments) and higher overall yields taken into account with the best-case projections:

The recent failures of Silicon Valley Bank, Signature Bank and First Republic along with the emergency sale of Credit Suisse in Europe could further tighten financial conditions, even if the Fed seizes interest rate hikes. In fact, according to Fed data, banks have already tightened their lending standards since the failures. While we are not predicting a severe recession or a material failure of the banking system, we think the events of the past quarter suggest that market volatility will continue and thus prudent credit investors with available capital will be well positioned. This creates potential growth catalyst for OCSL, we believe private credit funds may have significant and possibly long lasting opportunities to fill the lending gaps resulting from the bank's inability to meet demand. Ultimately, we believe the fallout from all of this will likely benefit those private lenders such as Oaktree that have sufficient scale to provide debt financing for large scale transactions. The opportunity sets widened as a result of that type of stress or distress. And then at the large banks, one should expect the regulatory oversight of what they do and how they use their balance sheets to earn syndication fees will take a toll. I think given that unsteady equilibrium that appears to be the case in the broadly syndicated loan market, we're finding the best opportunities in supporting large sponsors in doing new deals. That's probably the best risk adjusted return that we're seeing in the private credit market currently. First lien deals with very large sponsors running a 60% equity check and paying us 12% in a company that has $75 million to $700 million of EBITDA. The number of deals has declined in that zip code versus a year or two ago, but the quality of those deals is meaningfully better today than it was a year or two ago. So we're pretty excited about that opportunity.”

{kind=link}

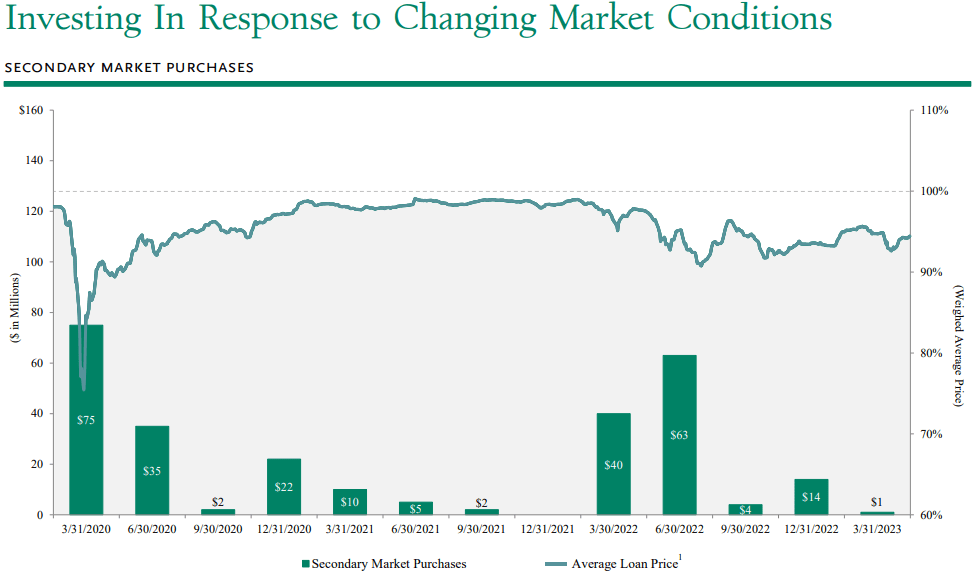

During calendar Q1 2023, OCSL exited another $40 million of lower-yielding assets that will likely be reinvested through its new private direct lending fund:

We have, obviously, a very active publicly traded book at Oaktree across our platform and evaluate relative value in public versus private every day frankly. So we saw some good opportunities in private. We took those opportunities rather than leaning into public, given the strength in the market there. We also further advanced our strategy of rotating out of public debt investments and redeploying capital into attractive and higher yielding private credit opportunities. During the quarter after the OSI2 merger, we also had some low yielding assets both in OCSL and from OSI2 that we sold throughout the quarter given the strength in the public markets. So we're able to sell upwards of $40 million in the publics to make room for future privates as well, all in the high 90s.”

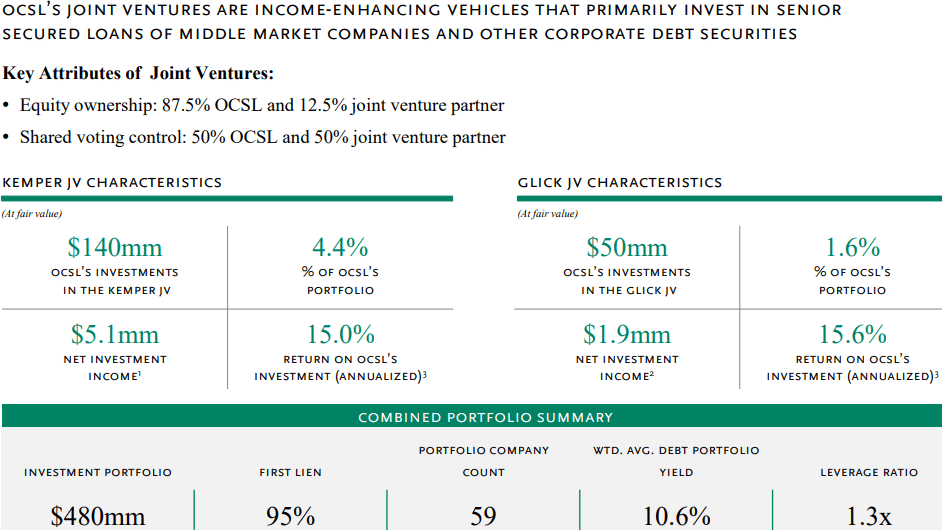

Also, there will likely be higher (or at least maintained) earnings from its joint ventures:

The Kemper JV had $393 million of assets invested in senior secured loans to 56 companies, down from $409 million last quarter, primarily driven by exits from two investments. The JV generated $3.2 million of cash interest income for OCSL in the quarter, up from $2.6 million in the fourth quarter as a result of the portfolios continue strong performance and the impact of rising interest rates on floating rate investments. We also received a $1.1 million dividend consistent with the first quarter dividend. Leverage at the JV was 1.4 times at quarter end, unchanged from the prior quarter. The Glick JV had $131 million of assets as of March 31, down from $138 million at Dec. 31. These consisted of senior secured loans to 39 companies. Leverage at the JV was 1.2 times at quarter end and we received $1.5 million worth of principal and interest payments on OCSL subordinated note in the Glick JV during the quarter.”

{kind=link}

BDC Valuations

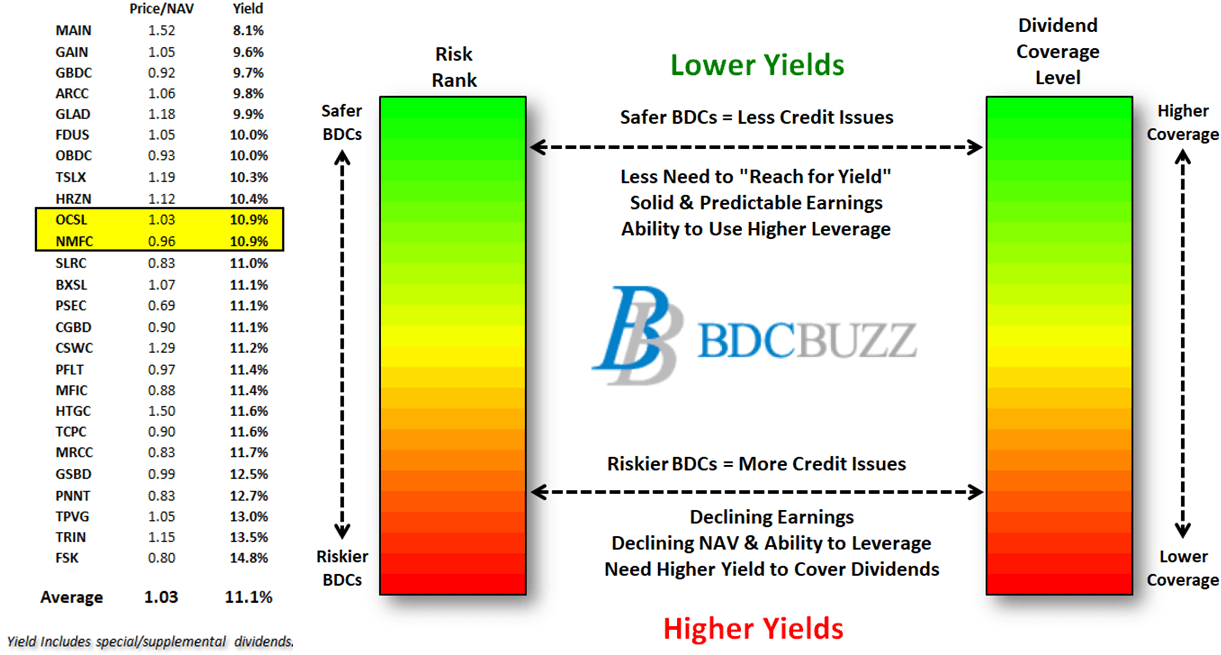

There are very specific reasons for the prices that BDCs trade driving higher and lower dividend yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). BDCs with higher-quality credit platforms and management typically have higher-quality portfolios and investors pay higher prices. This drives higher multiples to NAV and lower yields.

{kind=link}

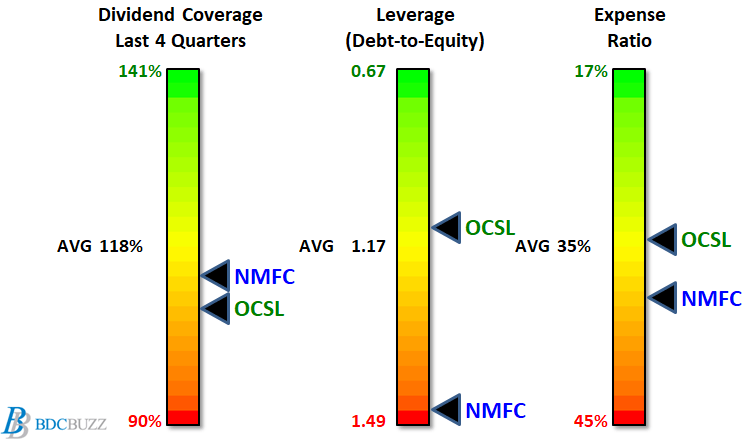

The charts below compare a few metrics for OCSL and NMFC including dividend coverage over the last four quarters, leverage or debt-to-equity, and expense ratios. As mentioned earlier, please do not focus only on historical dividend coverage especially compared to projected coverage. NMFC has slightly better historical coverage but also much higher leverage (debt-to-equity) implying that OCSL has the ability to grow its portfolio and earnings over the coming quarters. Also, OCSL has continually increased its dividend which is partially responsible for lower coverage. For these reasons, I believe that OCSL is the better choice for dividend coverage going forward.

{kind=link}

{kind=link}

OCSL’s watch list investments will be discussed in a following article and currently account for 10.5% of the portfolio (at cost) which includes its non-accrual investments and Athenex, Inc. that remains almost fully valued. However, on May 14, 2023, Athenex filed for Chapter 11 (partially due to the FDA’s rejection of its breast cancer candidate oral paclitaxel) after reaching an agreement with its lenders to move forward with an expedited sale process of its assets. The expedited sales process is expected to conclude by July 1, 2023.

The following chart shows the potential impact on NAV per share for each BDC, assuming that 100% of watch list investments (including non-accruals) defaulted with 0% recovery. This is the worst-case scenario for this group of investments. The largest NAV declines over the last four quarters were mostly BDCs with larger amounts of watch list investments. Subscribers who believe the economy is headed for a "hard landing" with a deep, broad, and/or extended recession should focus on the BDCs closer to the top left corner.

{kind=link}

OCSL Important Considerations:

The following are many of the positive considerations for OCSL, some of which are discussed in this article:

- Consistent historical and projected dividend coverage

- Recent merger was an efficient method of raising equity capital and reducing leverage, as well as improving scale and portfolio diversity, with higher first-lien

- Meaningful reduction in the amount of PIK income, from 7.9% to 4.3% of total income

- $9 million of additional fee waivers starting in Q1 2023

- Increased its regular dividend 11 times, from $0.285 to the current 0.550 per share plus special dividend in Q4 2022

- Potential special dividend in Q4 2023 (likely announced later this year)

- Continued rotation out of lower-yielding assets (reinvested into higher yields)

- Increased returns from its Kemper and Glick joint ventures

- Investment grade ratings by Moody’s (Baa3) Stable, Fitch (BBB-) Stable

- First-lien investments increased from 54% to 75% of the portfolio fair value (last five years)

- NAV per share has increased by 11.6% over the last five years

- Highly diversified portfolio of 165 portfolio companies with the top 10 accounting for around 20% of the portfolio at fair value

- The amount of "watch list" investments remain around 9% of the portfolio fair value (11% at cost) which is better than average

- Excellent history of credit quality and continuing to invest in larger companies that would likely outperform in a recessionary environment

- Clear/transparent management when discussing portfolio credit quality and measured approach when raising and deploying capital

- Likely reduced non-accruals resulting in an upgrade back to "Tier 1"

The following are many of the negative considerations for OCSL, most of which are discussed in this article:

- SiO2 Medical Products and The Avery were added to non-accrual status at around 2.3% of the portfolio fair value (2.4% of debt investments)

- Its watch list investment in Athenex, Inc. filed for Chapter 11 (on May 14, 2023) after reaching an agreement with lenders to an expedited sale process of its assets

- Net realized losses of $9 million or $0.13 per share over the last two quarters, mostly due to exiting some of its watch list investments

- Many of its watch list investments have been marked lower over the last two quarters

- Some of its watch list investments are currently marked slightly higher than other BDCs with the same position

- Relatively higher amount of Level 2 assets (around 10% of the portfolio) resulting in NAV volatility

- 83% of borrowings are at variable rates (a good thing if rates head lower)

- Potential selling pressure related to OSI2 shareholders looking for liquidity

- Lack of ‘total return’ hurdle or "look back" provision when calculating income incentive fees to protect shareholders from capital losses

For further details see:

Oaktree Or New Mountain For Solid 11% Yield?