OTLY - Oatly: Earnings Preview For Q4 And Full Year 2022

2023-03-09 12:37:18 ET

Summary

- Oatly's stock price has been crushed over the past 2 years, due in part to deteriorating margins, high CapEx and limited cash on the balance sheet.

- Oatly's cash position has been strengthened by their deal with Ya Ya Foods and can be further boosted by debt. An equity raise remains a risk for shareholders though.

- The current valuation is relatively low, indicating expectations of weak growth and margins in the future or a high probability of bankruptcy.

- If Oatly can build their cash balance, while improving margins, the stock should do well going forward.

Oatly (OTLY) is a leading producer of oat milk, which finds itself in a difficult position due to a combination of rapid growth, a capital intensive business and high inflation. Inflation is abating though, and Oatly's balance sheet is not as weak as it seems. Provided the oat milk category continues to grow, and Oatly can maintain their premium positioning, Oatly should be able to transition to profitability without excessively diluting shareholders.

The Opportunity

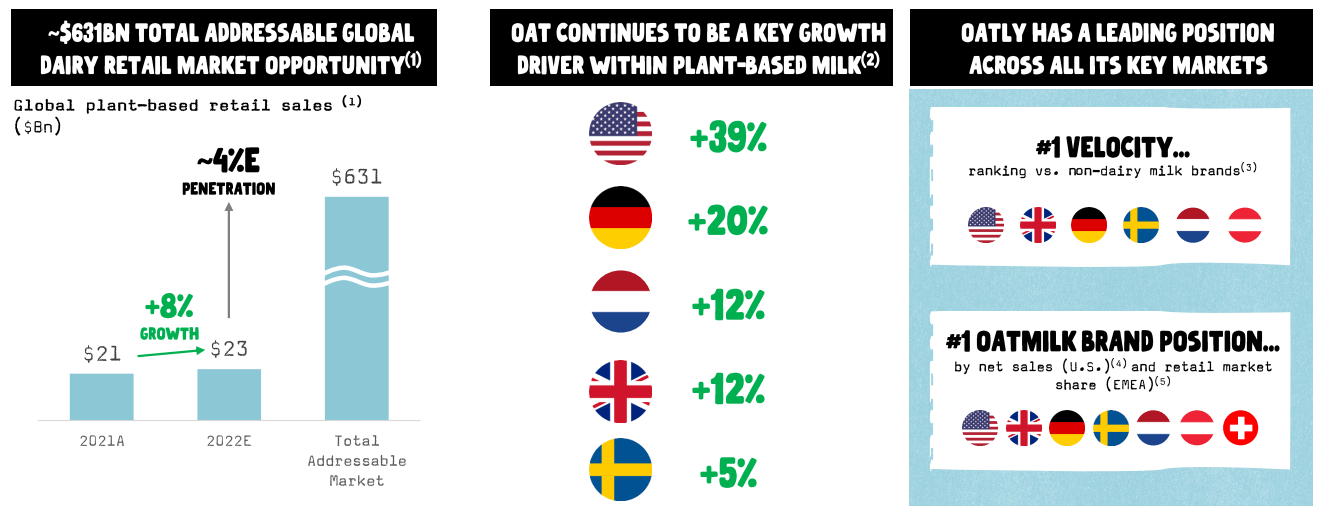

The market for oat-based dairy products is potentially extremely large, but there is currently considerable uncertainty as it is unclear how much penetration of the dairy market will ultimately be achieved. Adoption of oat-based dairy products is one of the keys to understanding Oatly's potential. This issue is exemplified by the plant-based meat category, which has stalled in recent years, despite its relatively meager size. While alternative dairy products have lactose intolerant consumers as a potential captive audience, it may be the case that only a small percentage of the population ultimately converts to alternative dairy products.

Within the category, oat-based products are generally establishing themselves as the preferred choice of consumers, and within oat-based products, Oatly is the clear leader. Oatly's ability to maintain differentiation relative to peers, is also extremely important to the company's future. Oatly has so far been able to achieve rapid growth with premium pricing, but there is a risk of commodification in time.

Figure 1: Oatly Addressable Market and Competitive Positioning (source: Oatly)

{kind=link}

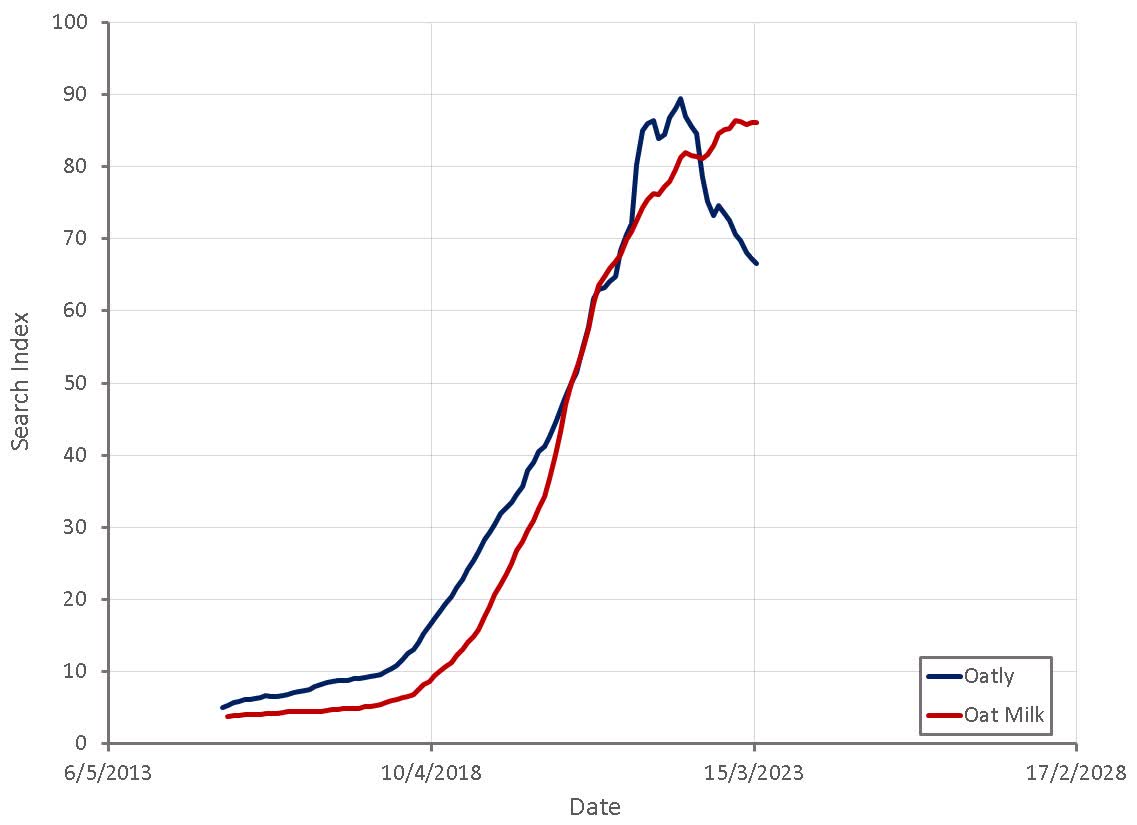

While Oatly has generally attributed slowing growth to supply constraints, there is a clear risk that growth in the oat-based dairy product category is normalizing, and that Oatly's leadership position is weakening.

Figure 2: "Oatly" Search Interest (source: Created by author using data from Google Trends)

{kind=link}

Oatly's Market

Oatly is a clear leader within the oat-based dairy product category, with the number one oat milk SKU and the highest velocities across key markets. Oatly is trying to build on this lead through the rollout of new products and channel expansion. Geographic expansion is also an important driver of growth, as Oatly appears to be underpenetrated outside of their core market in Northern Europe.

The company is currently facing somewhat of a liquidity crisis though, which has necessitated a shift in strategy. Oatly's priorities now include:

- Preparing for continued high growth (capacity expansion)

- Organizational simplification

- Achieving profitability

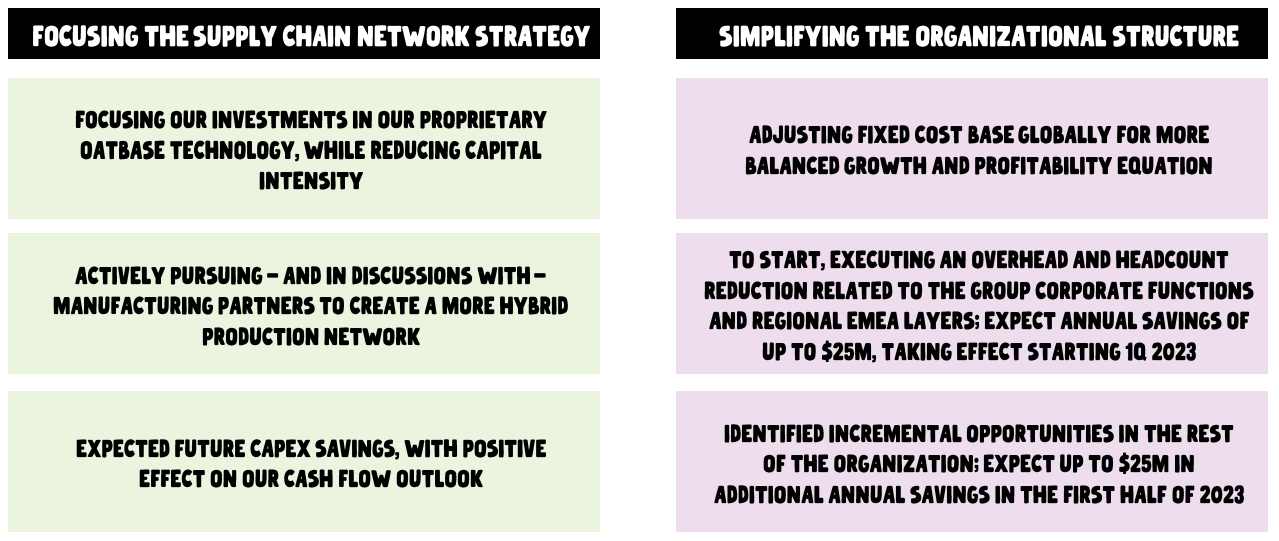

Oatly believes that their proprietary expertise in oat-based technology is a competitive advantage, and they are simplifying their supply chain by focusing on this advantage and outsourcing lower value-add activities. This will reduce the capital intensity of future facilities, although it may also negatively impact margins. Oatly is currently pursuing manufacturing partners to implement this strategy with.

Oatly is also restructuring their organization to try and reduce operating expenses. This involves an overhead and headcount reduction, impacting up to 25% of the costs related to corporate functions and regional EMEA layers. This initiative is expected to result in annual cost savings of up to 25 million USD, starting in 2023. Oatly has also identified incremental opportunities which could result in up to 25 million USD in additional annual savings, beginning in the first half of 2023.

{kind=link}

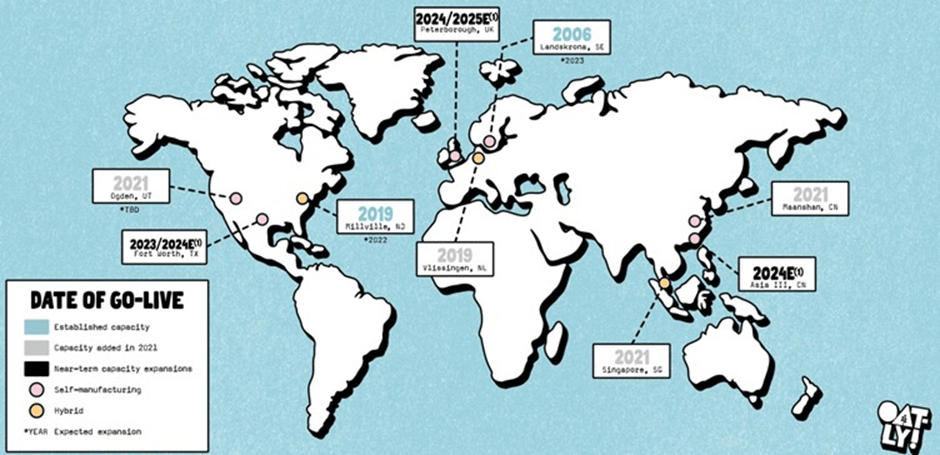

Ensuring production capacity is sufficient to meet demand, while also maintaining high utilization, is critical to Oatly achieving profitable growth. The company is currently in the process of building out a global manufacturing network, but this is capital intensive.

Oatly has suggested that growth has been weak, in part due to the fact that they are supply constrained. Although, this is somewhat at odds with low gross margins that have been attributed to capacity underutilization. Oatly planned on having 900 million liters of finished goods production capacity at the end of 2022.

{kind=link}

Oatly has already partnered with Ya Ya Foods for production at the Ogden and Fort Worth sites to reduce CapEx requirements. Oatly will produce their oat base, which will be transferred to Ya Ya Food for co-packing into Oatly products on-site.

Ya Ya Foods will acquire the majority of the assets at each site and assume the leases for both the Ogden and Fort Worth facilities. Ya Ya Foods will also assume responsibility for the completion of construction at the Fort Worth site.

Oatly will maintain ownership and operation of the oat-based production lines at each facility. Oatly will also receive roughly 72 million USD upfront, along with additional credit for future production at the Ogden facility and credit towards construction at the Fort Worth site.

Oatly's management had previously mentioned wanting to transition the Peterborough plants to a hybrid arrangement as well, and a similar deal for that site may still be in the works.

Management has indicated that the hybrid strategy will reduce gross margins, but has not quantified the impact. They believe that the reduction in gross margins will be offset by a reduction in supply chain and operational complexity. While this may true to an extent, it seems likely that the hybrid approach will result in a net margin reduction. If this was a superior approach, Oatly would almost certainly have pursued it from the beginning. Although, management has stated that it is now easier to find strategic co-packers due to their scale and growth.

Financial Analysis And Outlook

Oatly's financial performance in recent quarters has been characterized by tepid growth and deteriorating margins. Weak growth in the third quarter can in large part be attributed to foreign exchange headwinds, which reduced growth by approximately 10% YoY . COVID related lockdowns in China have also contributed to weak growth, although ecommerce sales there have been strong. Oatly has been supply constrained in the US, which was exacerbated by production issues in the third quarter. Production is expected to continue ramping going forward, which should lead to greater sales and market share gains.

Oatly's Singapore facility began producing at capacity in September and their Maanshan facility in China is ramping production. These facilities should enable Oatly to increase sales in the region.

Management has suggested that the macro environment is worsening, but it is not clear if this is something specific that Oatly is witnessing, or is just a general observation of economic conditions. They have also stated that the category is still very strong, which indicates that alternative dairy products have not been overly impacted by macro conditions.

Oatly guided for around 183 million USD revenue in the fourth quarter, which would represent essentially no growth YoY. The USD weakened somewhat after guidance was given, which should be supportive of higher growth. China also began abandoning its zero-tolerance approach to COVID in early December, which may have provided some unexpected tailwinds.

These factors likely need to be weighed against a weakening consumer balance sheet, which is impacting spending at the margins. For example, a number of companies have pointed towards consumers delaying spending or trading down. As a producer of premium priced products, this could impact Oatly negatively.

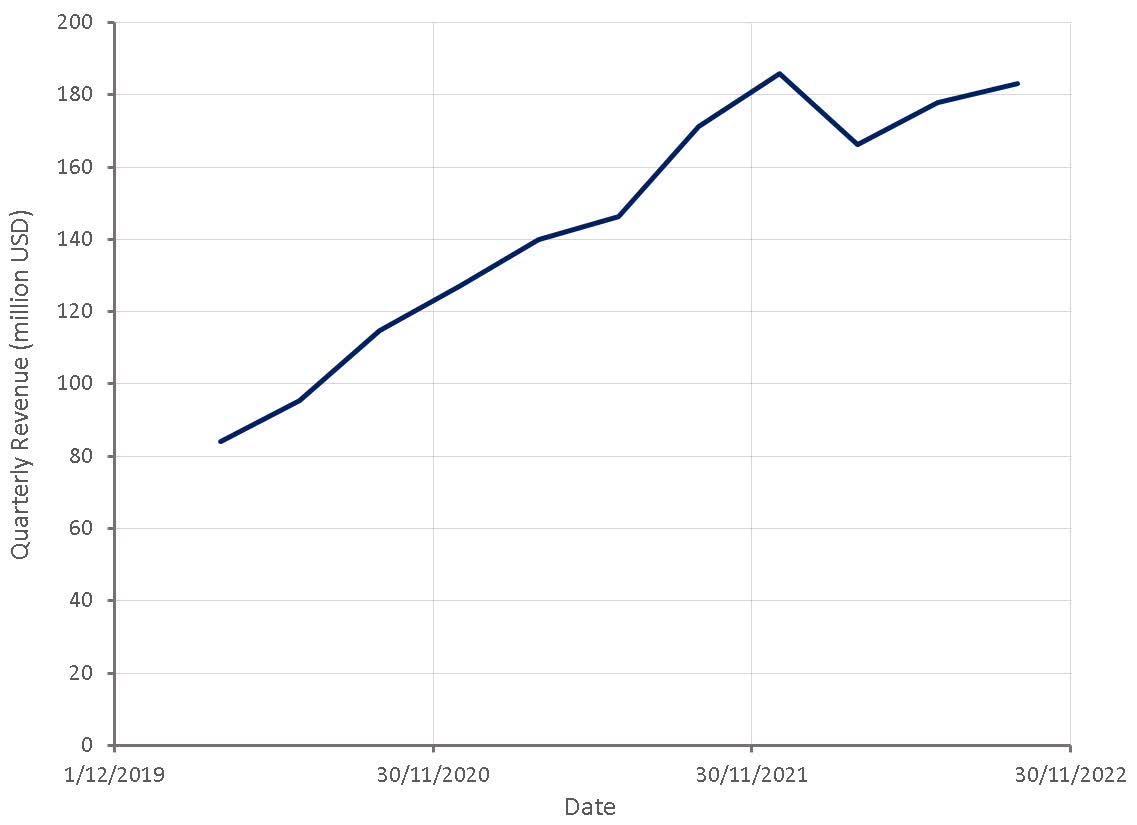

Figure 5: Oatly Revenue (source: Created by author using data from Oatly) Table 1: Oatly YoY Volume Growth in the Third Quarter of 2022 (source: Created by author using data from Oatly)

{kind=link}

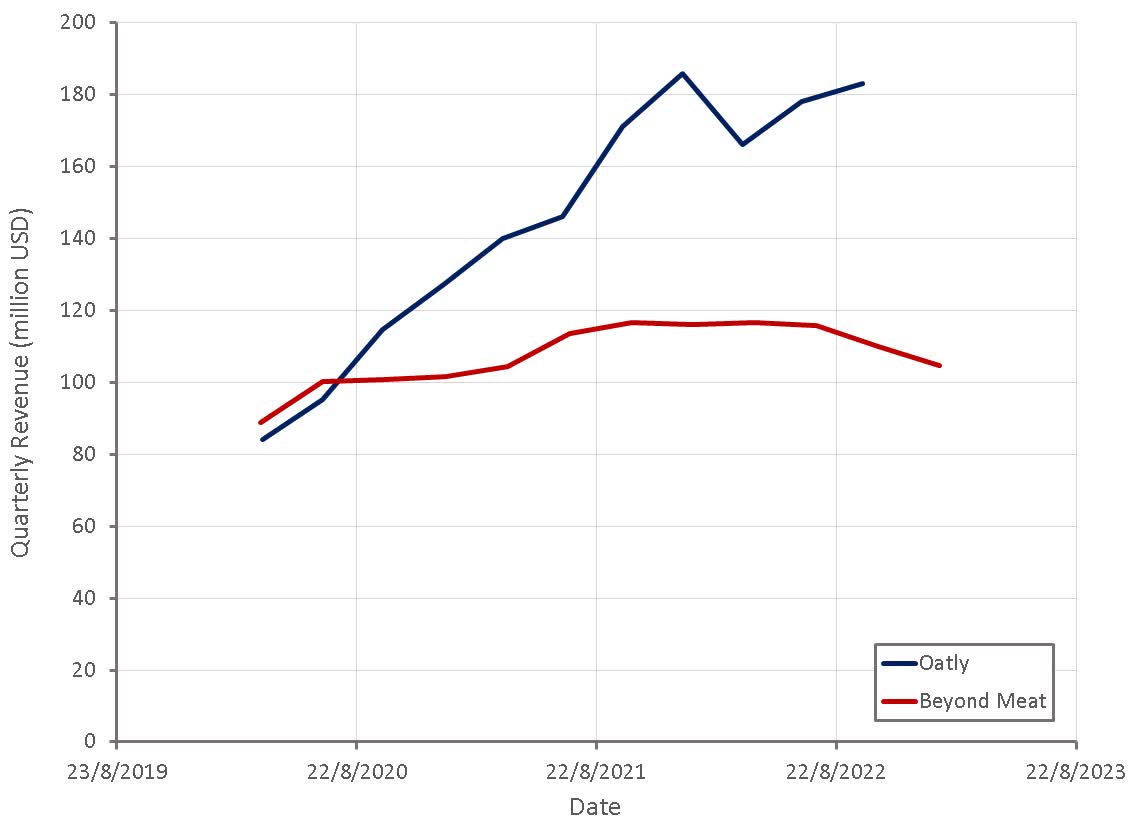

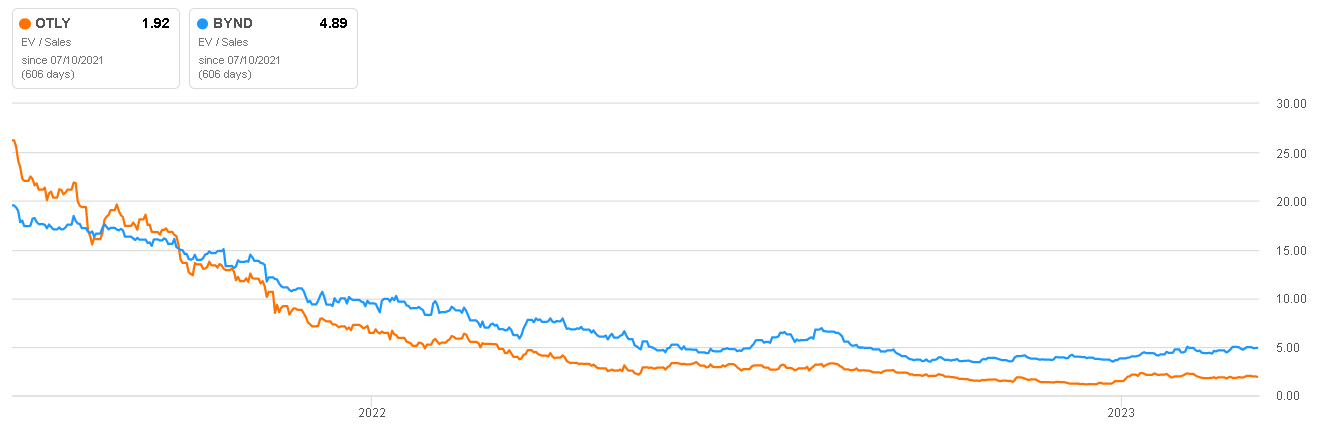

Oatly so far does not appear to be in the same boat as Beyond Meat ( BYND ), which is facing high costs and capacity underutilization, along with declining revenue. This is the bear case for Oatly though, as a lack of growth will make achieving profitability difficult.

Figure 6: Oatly and Beyond Meat Revenue (source: Created by author using data from company reports)

{kind=link}

Oatly's gross profit margins have been negatively impacted by inflation and production facility underutilization, although the company has been able to partially offset this by pricing actions in the Americas and EMEA.

Poor margins in the third quarter were attributed to:

- Facility underutilization in Asia due to COVID restrictions

- Production issues at the Ogden facility

- Macro headwinds in EMEA

Production issues at the Ogden facility resulted in one of the two oat baselines being down for roughly three weeks . In addition to reducing production in the third quarter, inventory was drawn down, which is expected to impact sales in the fourth quarter.

Management guided towards COGS inflation of 3-4% in the fourth quarter , relative to the third quarter. Inflation in 2023 is expected to be in the 6-7% range.

{kind=link}

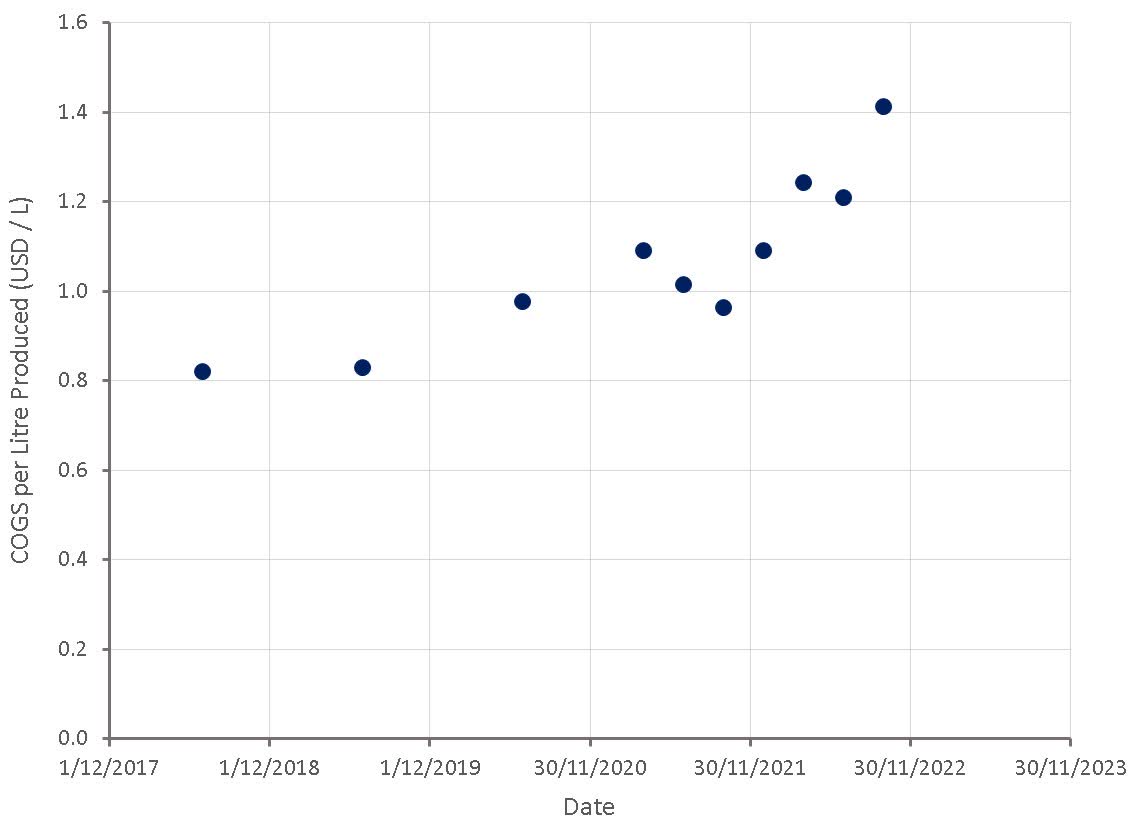

The price of oats has declined significantly over the past eight months, which should help to bring down Oatly's production costs. It is not clear what type of contracts Oatly has in place with suppliers though, and any cost reductions will need to work their way through inventory before showing up on the income statement.

Figure 8: Oatly Production Costs (source: Created by author using data from Oatly)

{kind=link}

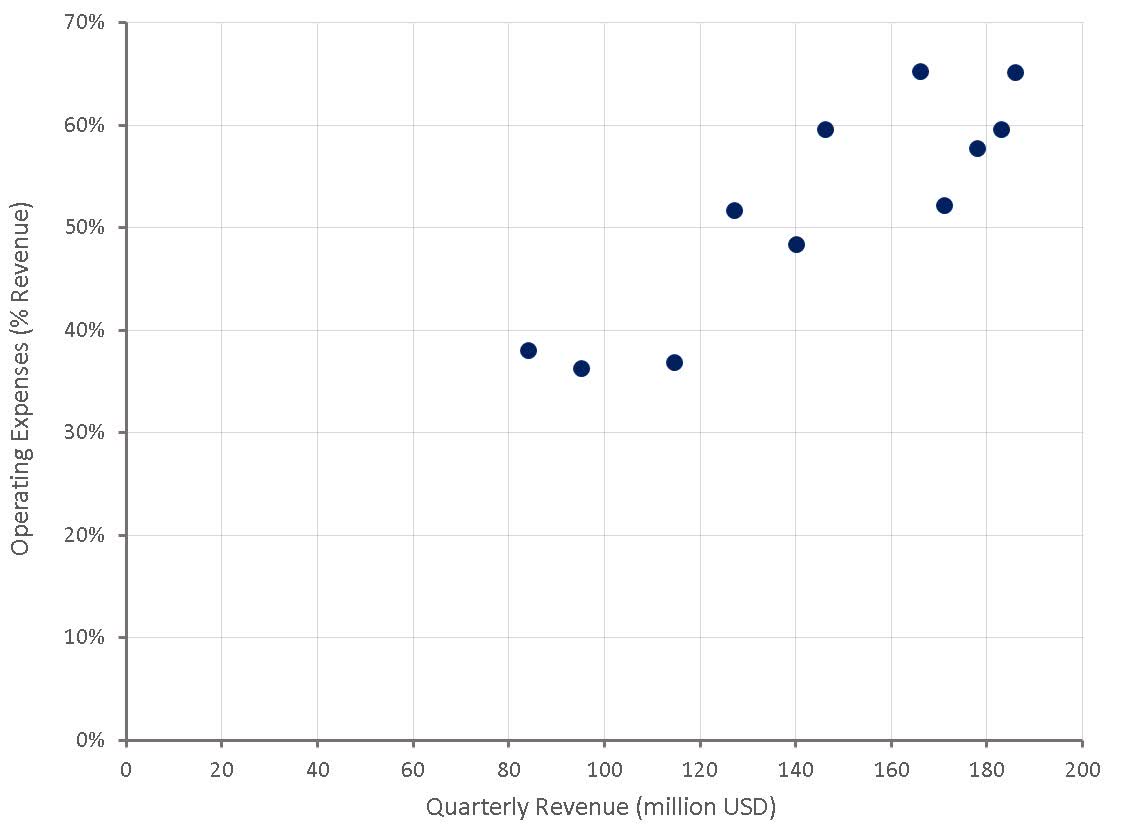

In addition to declining gross margins, Oatly has faced a rising burden from operating expenses. Much of this is likely due to marketing and distribution expenses, along with over hiring. Oatly still needs to drive awareness, which will limit how much costs can be cut, but declining overhead expenses should help move Oatly closer to breakeven. Planned cost reductions are unlikely to have a significant impact in the fourth quarter, and if anything layoffs may temporarily elevate operating expenses. Oatly is targeting adjusted EBITDA breakeven by the end of 2023, which is a big ask from their current position, particularly if growth disappoints.

Figure 9: Oatly Operating Expenses (source: Created by author using data from Oatly)

{kind=link}

While Oatly only had around 120 million USD in liquid assets at the end of the third quarter, the company still had access to a revolving credit facility amounting to approximately 320 million USD. Management also stated that they had lowered the capital raise requirements to 200 million USD and extended the capital raise period until June 30 2023. Oatly's deal with Ya Ya Foods has also strengthened the company's balance sheet, although this will not show up in the fourth quarter. Despite this, significant dilution remains a risk for shareholders. Oatly's recent general meeting potentially set the company up for an issuance of equity or convertible bonds.

Valuation

Oatly's near-term liquidity problems are being over estimated, which could present an opportunity to investors with a healthy risk appetite. Margins should improve significantly over the next 12 months if growth can be maintained, but there is a risk that oat milk adoption stalls or that the oat based milk category becomes commodified.

At the current valuation, little is priced into Oatly's stock in terms of growth or margins. This may be due to an expectation that Oatly will be forced to do a highly dilutionary equity raise at some point in the near future.

{kind=link}

For further details see:

Oatly: Earnings Preview For Q4 And Full Year 2022