OTLY - Oatly: High Growth Potential Despite Unpredictable Construction Timeline

2023-04-10 14:25:54 ET

Summary

- The company restructured its business in 2022 and looks positioned to accelerate its growth in 2023.

- Its gross margin should improve sequentially quarter-over-quarter in 2023, reaching a high-20%s in the fourth quarter.

- Although there are a couple of catalysts to watch, the upside potential is likely constrained by its high WACC.

- We rate the stock as Neutral.

Investment Thesis

Overall, we think the Oatly Group AB ( OTLY ) has strong brands and products and operates in a growing and promising industry. Although there are a couple of catalysts to watch, we believe the upside potential is constrained by its high WACC, and stock volatility as a result of production delays might be substantial. Hence, the risk and rewards don't seem attractive. We rate the stock as Neutral at this time.

Company Profile

The company is the world’s original and largest oat milk company. It offers a range of plant-based dairy products made from oats.

Product Categories (Company's filing)

{kind=link}

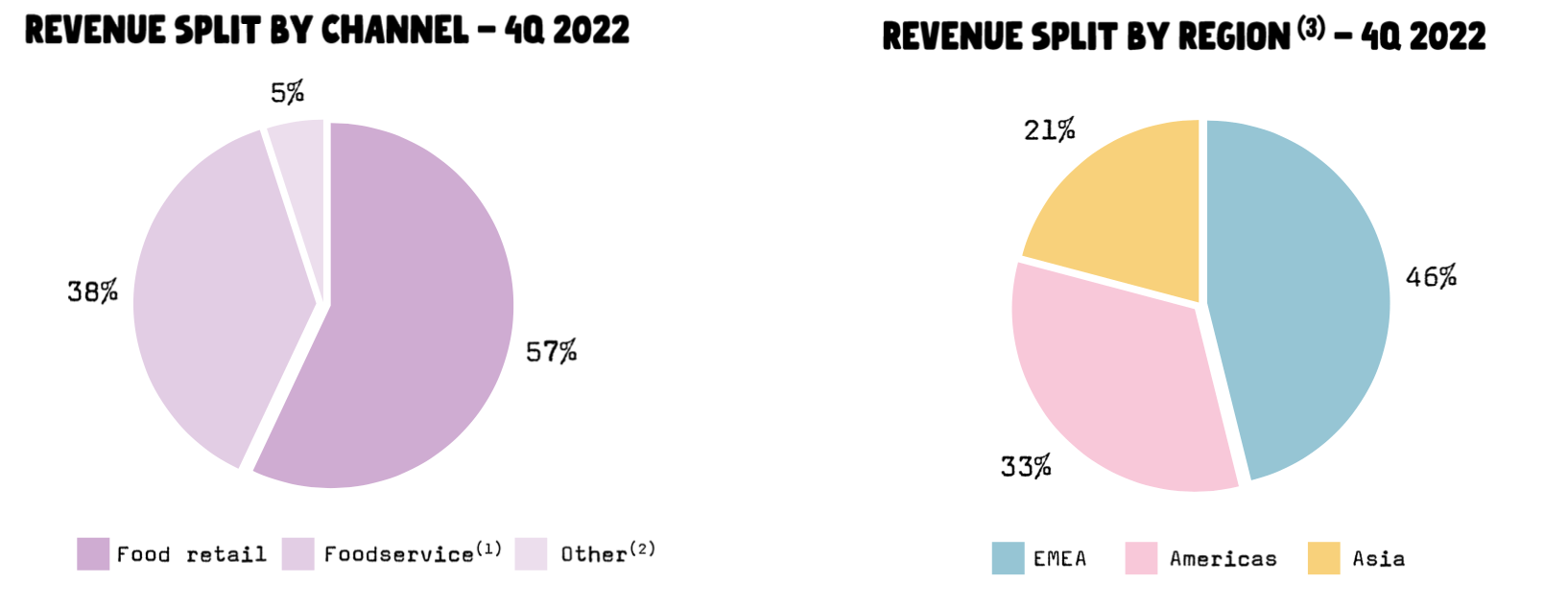

In 2022, the company generated $722 million in revenues. In Q4 2022, the food service channel accounted for 38% of its revenue and the food retail channel accounted for 57% of our revenue.

Revenue breakdowns (Company's presentation)

{kind=link}

Key Takeaways from Q4 2022 Earnings:

Q42022 financials (Company's presentation)

{kind=link}

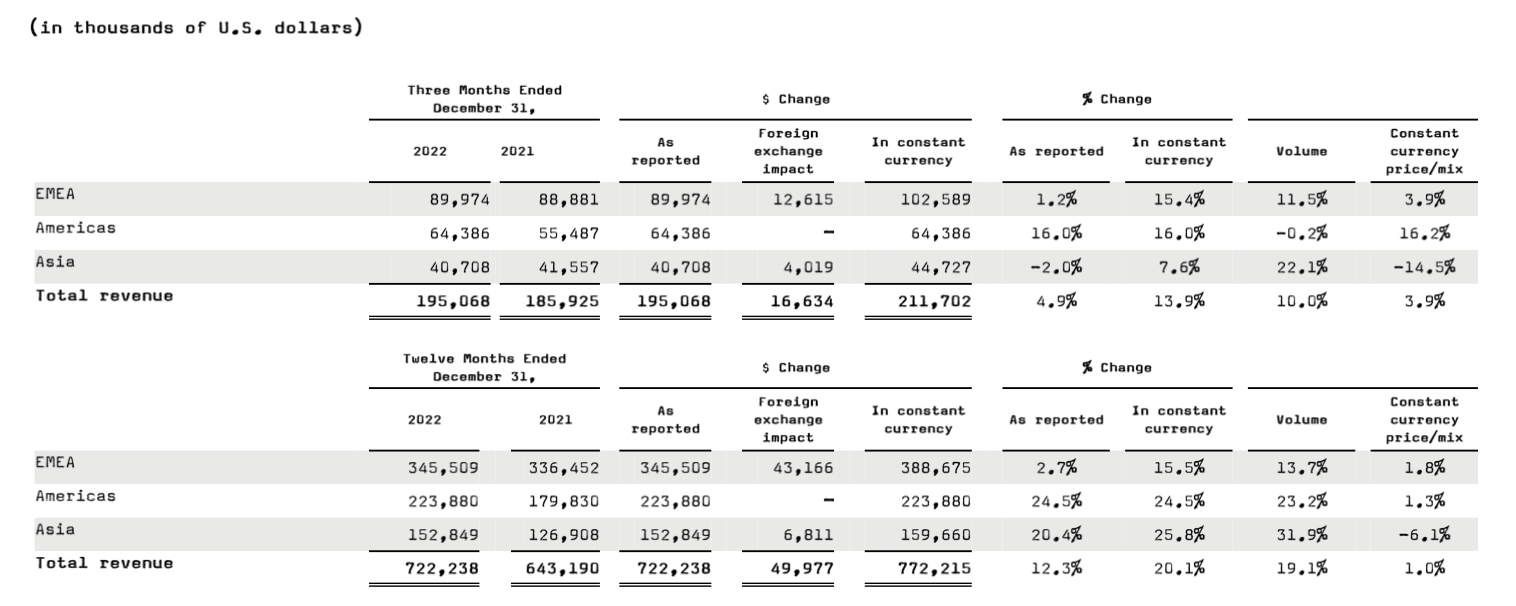

- In Q4 2022, its sales increased by 13.9% to $195 million on a constant currency basis, decelerating from 16.7% in Q3 2022.

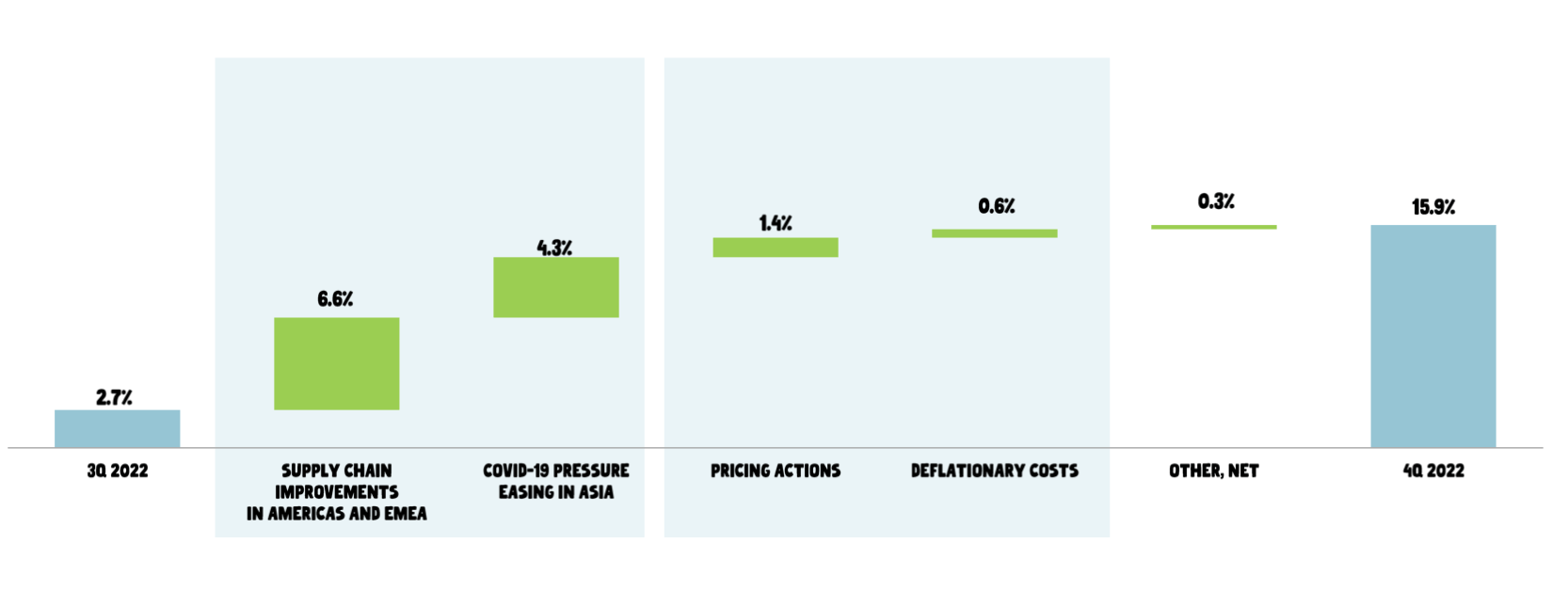

- In Q4 2022, its gross margin remained flat to last year but increased by 1,300 bps compared to Q3 2022, driven by supply chain improvement in the Americas and EMEA and easing from lockdowns in China.

- In Q4 2022, its SG&A% decreased by 900 bps to 55.3%, from 64.3%, due to lower marketing expense.

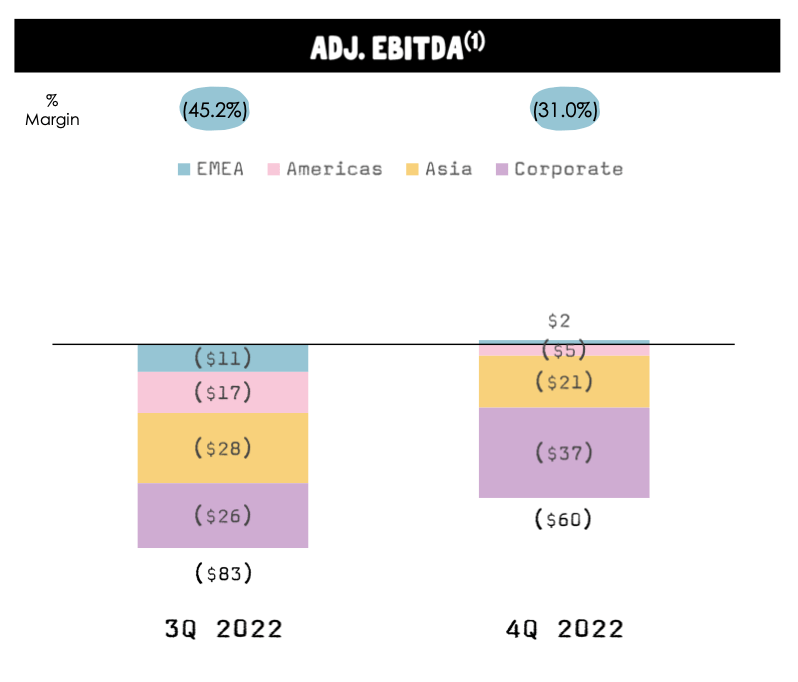

- In Q4 2022, its adj. EBITDA margin increased by 440 bps to -30.8%, from -35.1%.

- As of the end of Q4 2022, its inventories increased by 20% to $114 million, from $95 million.

Gross Margin Step Up (Company's presentation)

{kind=link}

Adj. EBITDA Step Up (Company's presentation)

{kind=link}

The company provided the following 2023 outlook :

- Its sales will grow 23%-28% on a constant currency basis.

- Its gross margin will improve sequentially quarter-over-quarter in fiscal 2023, reaching a high-20%s in the fourth quarter, driven by an increase in utilization rate, price increases, and easing from the COVID lockdowns.

- Its CAPEX will remain flat to down between $180 million and to 200 million.

2023 Gross Margin Outlook (Company's presentation)

{kind=link}

-

Longer-term, the company expects:

Its gross profit margin is expected to reach the range of 35% to 40%.

It will achieve positive adjusted EBITDA in 2024 and its adjusted EBITDA margin increases in the mid-to high-teens long term.

We have the following comments:

- The company restructured its business in 2022 and seems positioned to accelerate its growth in 2023. The company will expand through (1) momentum in EMEA, new product offerings, and increased penetration into the food service market; (2) the Americas will recover after the Utah supply chain disruption has subsided and production will ramp up in the New Jersey plant; and (3) Asia will grow through improved distribution and new product introductions.

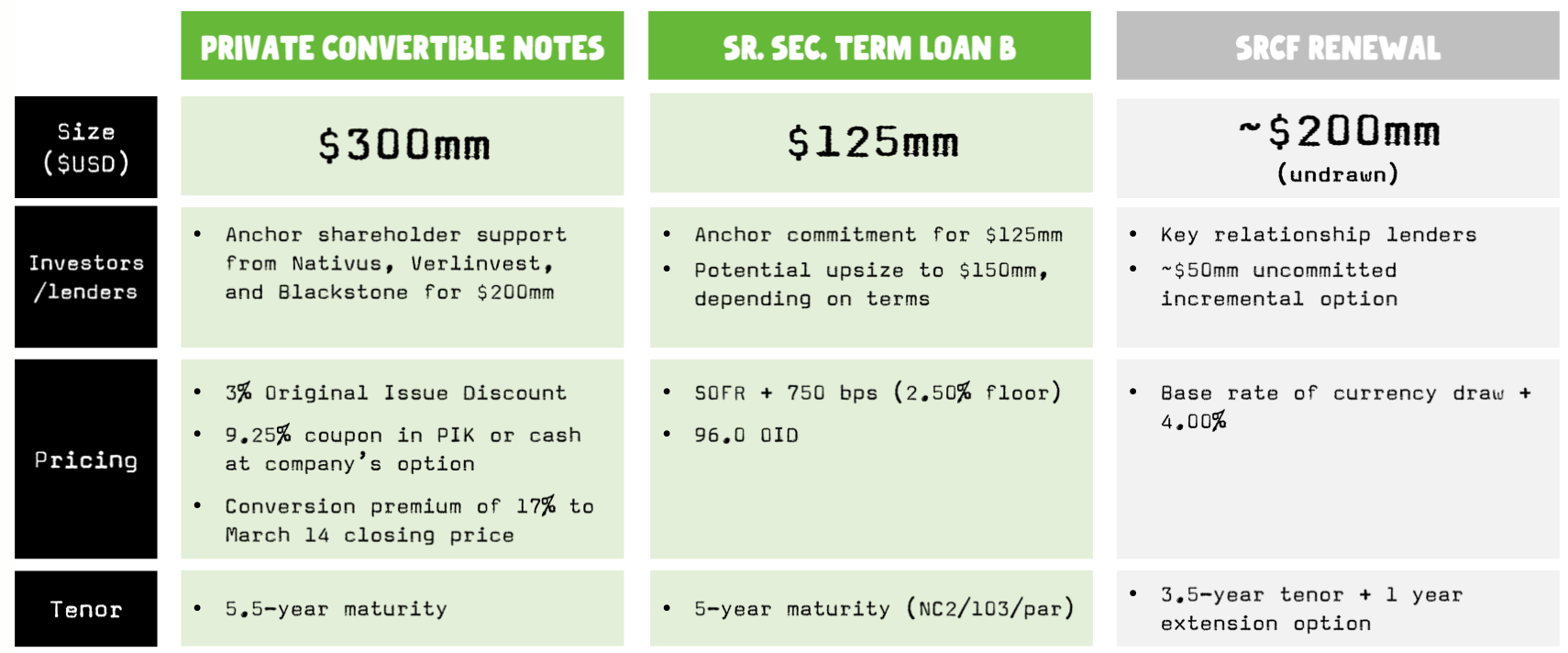

- The company only had around $500 million cash on hand with $200 million revolving facility capacity after the financing transaction and it is expected to incur around $200 million CAPEX in 2023 and achieve adjusted EBITDA breakeven in 2023. We estimated that assuming profitability increases linearly, the company will burn at least $355 million in 2023. The company has bought some time short term but is still not out of the woods yet.

Financing Transaction (Company's presentation)

{kind=link}

Company fundamentals and its manufacturing facilities

The company's strategy is to develop a superior nutritional profile tailored to human needs rather than imitate existing forms of milk.

The company currently works closely with six oat suppliers to source its oats globally.

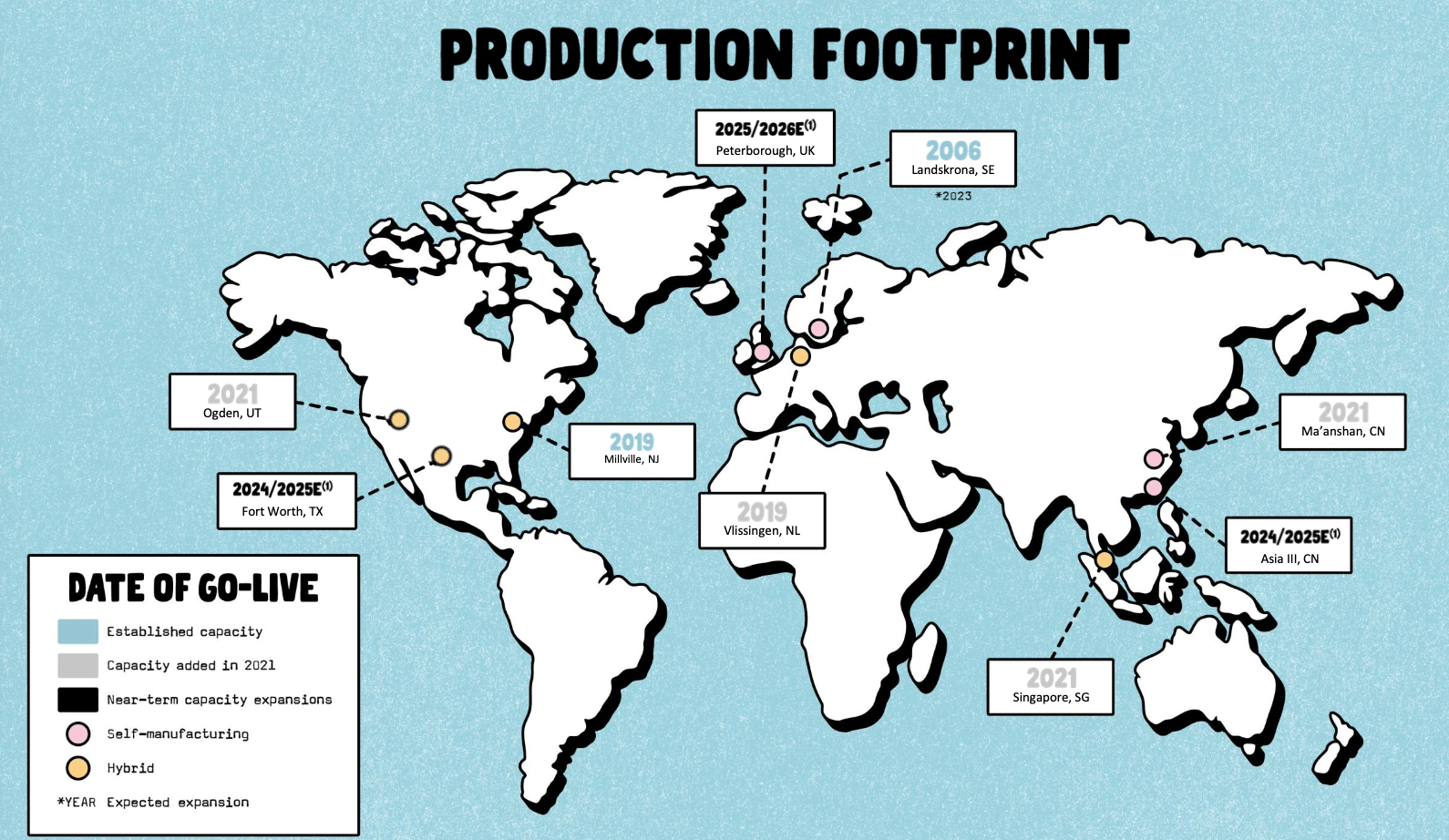

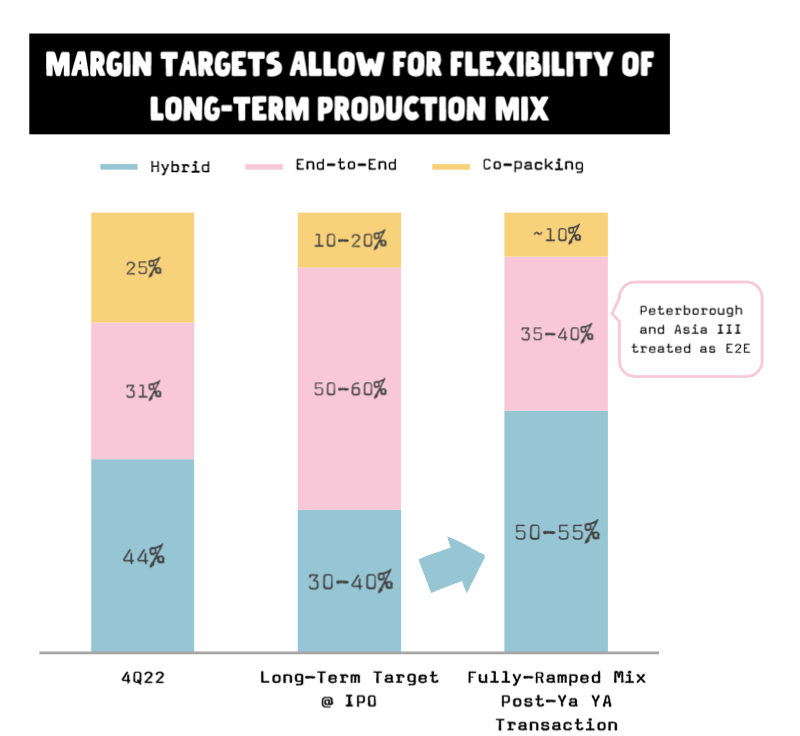

As of Dec 2022, the company had six Oatly factories online and three factories planned or under construction. In 2022, approximately 10% of its products were produced through the co-packing model, 50-55% through a hybrid model, and 35-40% through its own end-to-end self-manufacturing.

In the long term, the company plans to strategically shift towards the hybrid and end-to-end self-manufacturing models, which will provide it with greater flexibility, faster speed-to-market, higher quality control, significant scale efficiencies, and ultimately more favorable economics.

As of Dec 2022, the company had a production capacity of approximately 900 million liters and plans to expand production capacity to approximately 1.3 billion liters by the end of 2023.

Production Facilities (Company's presentation) Manufacturing Facility Expansion Plan (Company's presentation)

{kind=link}

{kind=link}

Industry

In its 20-F , the company provided industry sizes estimated by Euromonitor.

The global plant-based dairy industry retail market was $20 billion in 2021, accounting for 3% of the global dairy market (excluding soy drinks in China). Within the global dairy market, plant-based milk represented approximately 9% of the global dairy milk category (excluding soy drinks in China) in 2021.

We participate in the large global dairy industry, which consists of milk, ice cream, and frozen dessert, yogurt, cream, cheese, and other dairy products. According to Euromonitor, the global dairy industry retail sales were estimated to be $628 billion in 2021 and are expected to reach $818 billion in 2026, growing at a compound annual growth rate (“CAGR”) of 5.4%. In line with retail, foodservice also represents a significant opportunity for us, which we believe expands the total addressable market even further.

Today, we primarily operate in the global milk category, which is the largest subcategory within dairy. According to Euromonitor, the global milk industry retail sales were estimated to be $190 billion in 2021, representing 30% of the global dairy industry 2021. In some developed markets, dairy milk consumption per capita has been steadily declining, with the trend continuing in the last decade as plant-based dairy has increased in popularity. We expect this trend to further accelerate in the coming years, as the growing offering of plant-based dairy across the entire dairy portfolio expands across product categories, including ice cream and yogurt.

The global plant-based dairy industry retail sales were estimated to be $20 billion in 2021, according to Euromonitor, representing approximately 3% of the global dairy industry (excluding soy drinks in China). Within the global dairy industry, plant-based milk represented approximately 9% of the global dairy milk category (excluding soy drinks in China) in 2021. As of 2021, dairy alternatives in other dairy categories have a penetration of less than 1%, highlighting the opportunity ahead across the broader plant-based dairy sector.

Also, the latest update on the industry from Euromonitor is as follows:

Sour milk products, including kefir, are set to be the fastest growing performers globally, with an expected forecast CAGR of 4% in retail value sales. In addition, emerging markets are delivering the fastest growth for cheese, and in particular, Asia Pacific is expected to witness a 7% CAGR over the forecast period, largely set to be driven by strong growth in China.

The company outlined its growth strategies in the 20-F:

Expand Consumer Base through Increased Awareness and Plant-Based Dairy Category Growth

The plant-based dairy market is still in its infancy. Even the most mature market and most mature category—U.S. dairy milk alternatives—has only 9% penetration compared to dairy milk as of 2021, according to Euromonitor, representing significant whitespace for us to grow.

We believe the ability to share the Oatly story with a broader audience is critical to the success of our mission to drive greater plant-based consumption. At precisely the moment when these values are hitting mainstream culture, we are helping to support the breaking down of barriers to adopt plant-based dairy and capturing this interest by engaging consumers with our brand. We believe our brand that is focused on sustainability has helped to drive Oatly’s success across each of our markets. We believe our commercial efforts and proven execution to increase knowledge and awareness of our brand will enable us to convert dairy consumers into Oatly consumers.

Grow Distribution and Velocity in New and Existing Markets

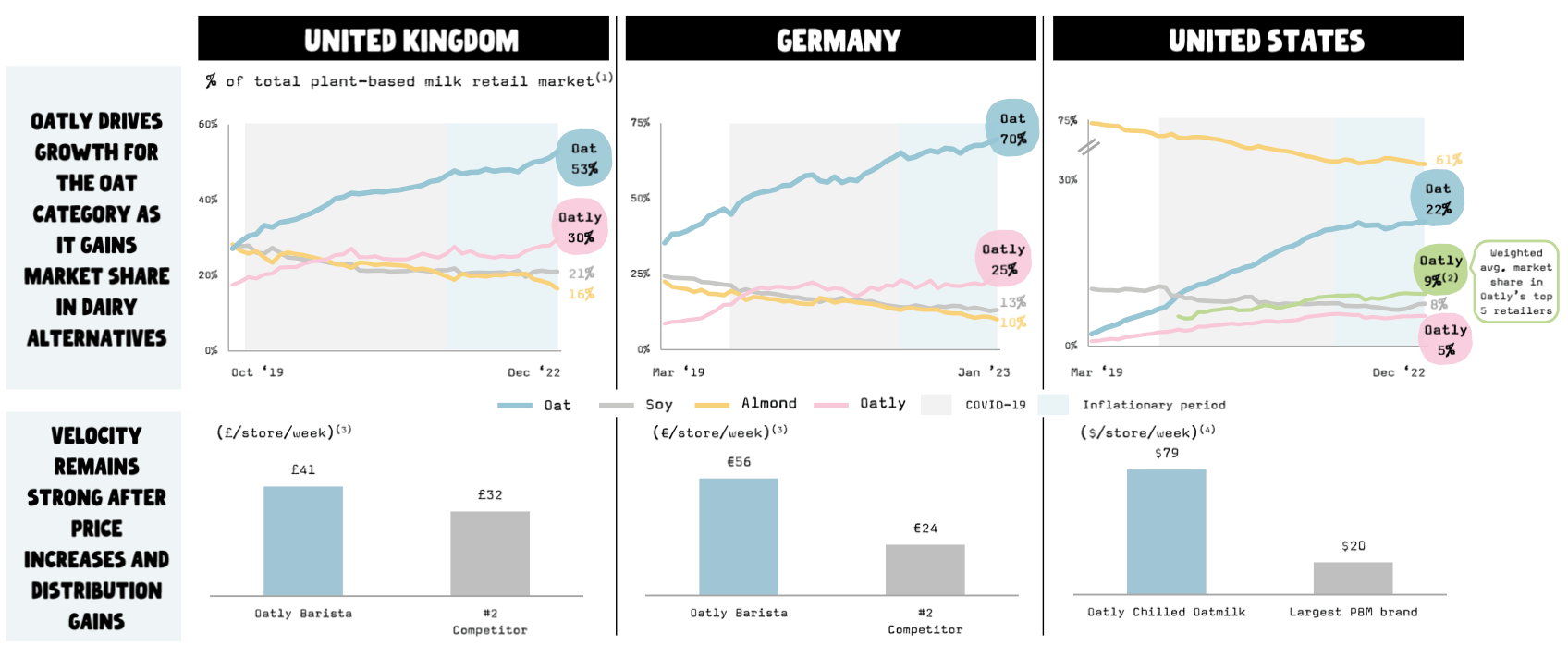

We believe we can continue to grow in existing markets by building on our industry-leading food retail performance by growing velocity and expanding on-shelf presence with Oatly’s full portfolio. Our performance in Germany, the United Kingdom and the United States, where we have demonstrated strong velocity, is indicative of the consumer demand for our products. We believe there is significant whitespace to further expand our foodservice, retail and e-commerce footprint. To illustrate the distribution whitespace opportunity in the retail channel, our total distribution points in Germany and the United Kingdom is approximately one-third of the largest plant-based milk brands in each market, as of December 31, 2021, according to Nielsen and IRI. In the United States, our all-commodity volume, which represents weighted average distribution, was 34% as of December 31, 2021.

Beyond our existing footprint, we believe we have a significant opportunity to expand into new international markets, including in Asia. We believe our established global presence and proven execution in three continents serve as compelling proof points of our ability to successfully enter new markets. In EMEA, we are only in the early stages of development in many of the region’s largest dairy markets: Spain, France and Italy, representing a $48 billion in dairy market retail opportunity as of December 31, 2021. We plan to leverage our proven foodservice-led strategy to encourage trial, generate strong consumer buzz and create strong pull into the retail channel.

Invest in Global Operating Footprint to Support Scaled Growth Opportunity

We believe the greatest constraint on our growth has been production capacity. Historically, global demand for Oatly products has significantly outpaced our supply. In order to meet this demand, we operated six production facilities as of December 2021 and plan to open three additional facilities in 2023. Our strategy is to further execute upon our proven track record and continue to build our production capabilities across each of our regions. By increasing our production capacity, we expect to be able to drive top-line growth and increase our ability to meet the existing consumer demand.

Ultimately, we believe our long-term strategy of operating end-to-end manufacturing facilities allows better control over our footprint that is necessary to meet our speed-to-market, sustainability, economic and innovation goals. Specific competitive advantages of this strategy include secured production capacity in an increasingly competitive market; end-to-end process control ensuring product quality; greater control over equipment and processes related to sustainability; and proximity to consumer end markets to drive attractive production economics. We believe we are still in the early stages of the transition to a plant-based food system and will continue to invest in our production capabilities to spearhead this consumer movement.

Valuation

DCF valuation

We reference Euromonitor's estimation to determine the market size. The industry was anticipated to grow at a stable pace. Hence, our assumption can be seen as more conservative.

According to Euromonitor, the global milk market was $190 billion in 2021, accounting for 30% of the global dairy industry. The plant-based milk represented approximately 9% of the global dairy milk category (excluding soy drinks in China) in 2021.

Market Share Trend (Company's presentation)

{kind=link}

The company had plant-based milk retail market shares of 53% in Sweden, 30% in the U.K., and 25% in Germany, 5% in the U.S. in Q42022.

We make the following assumptions based on the company's financials and current market conditions:

- The global plant-based milk penetration rate reaches 20% of the global dairy milk market. The company has a 25% market share in the plant-based milk market. This implies the company will grow to a 5% market share of the global milk market.

- 20% WACC

- 3% terminal growth rate

- 10% free cash flow margin

- Net debt 343 million (Q4 2022)

- Outstanding shares 592 million (Q4 2022)

Applying the DCF method, we can arrive at an equity value of $593 million ($1 per share), which implies a 56% decline from the current stock price.

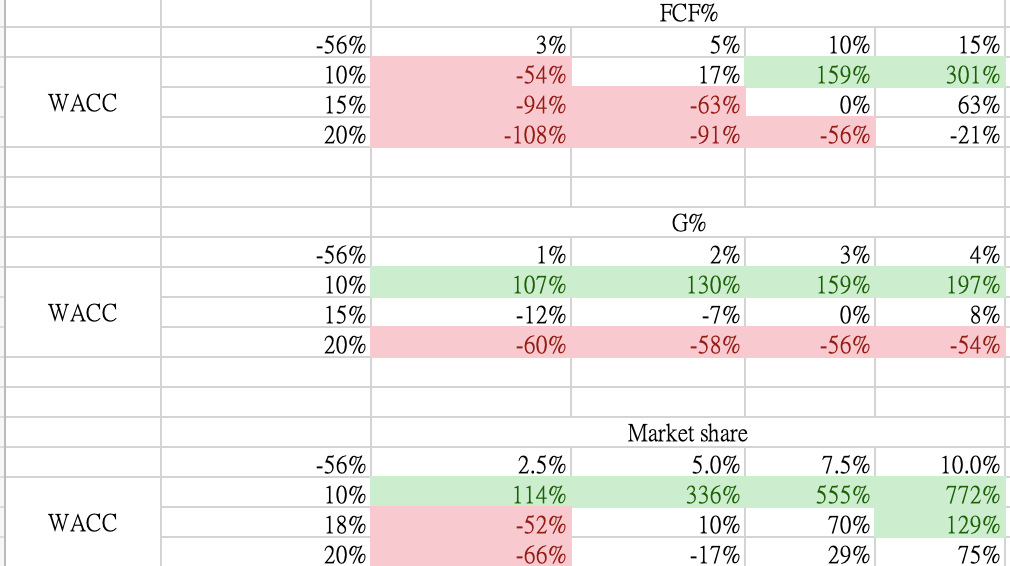

With the sensitivity test below, we can see that the stock is undervalued only if its free cash flow margin increases above 10% and WACC drops below 15%.

Also, the potential return for the stock rises sharply if the plant-based milk becomes more widely consumed or the company secures a larger worldwide market share than we anticipate.

Sensitivity Test (LEL Investment)

{kind=link}

Catalysts

First, the company is projected to meet adj. EBITDA breakeven in 2024. This suggests that it may be too early to anticipate the free cash flow margin expansion as the catalyst for the stock. However, the company has a positive outlook on the industry and believes that the demand for its product still outgrows its supply.

If the company can complete its production expansion to 1.3 billion liters early, before the end of 2023, it will increase its margin sooner. This may serve as a positive catalyst for the stock.

Second, our assumptions on the company's market shares and global penetration of plant-based milk might be conservative.

The company has been able to increase its market shares in multiple countries on a quarterly basis. Furthermore, the oat milk market is still growing, which presents opportunities for the company to expand its market share. So, if the company provides more share gain metrics in future earnings releases, this can trigger the stock to reprice.

Risks

Solvency risk

The company has 3 more manufacturing facilities projects to complete in the next 3 years. The company has delayed its production mix promise and was recently forced to raise additional convertible debt to complete its construction.

The company's net debt was $343 million and it expects to achieve adjusted EBITDA breakeven in 2024. Hence, there is still a risk of solvency. Moreover, there is also a construction risk associated with the company's production expansion projects. As a result, its CAPEX and operating expenses can fluctuate on a quarterly basis, depending on the progress of the production projects. Thus, the volatility in the stock price can be significant. Investors should closely monitor the company's financials and project updates.

Summary

Overall, we think the company has strong brands and products and operates in a growing and promising industry. Although there are a couple of catalysts to watch, the upside potential is constrained by the high WACC. Stock volatility as a result of production delays might be substantial. Hence, the risk and rewards don't seem attractive.

For further details see:

Oatly: High Growth Potential Despite Unpredictable Construction Timeline