OTLY - Oatly: Improving Margins Versus Growth Headwinds

2023-11-21 18:58:54 ET

Summary

- Oatly's share price response to Q3 earnings was driven by low expectations rather than strong results.

- While Oatly's valuation is low, providing significant upside potential, the company still has significant work to do to reach breakeven.

- The company is reducing costs at the expense of revenues, which may eventually make further margin gains difficult to obtain.

The response of Oatly's ( OTLY ) share price to third quarter earnings was driven by low expectations rather than strong results. While the company is making progress reducing costs, this is coming at the expense of revenues. Current actions are extending Oatly’s runway, but the company is still some way off demonstrating that it can generate profitable growth globally. EMEA continues to be a bright spot, with results in the Americas mixed and Asia dragging on performance. If Oatly can continue to reduce losses, the share price should move higher, but the struggle to expand internationally has undermined the long-term value of the company.

I believe that Oatly represents reasonable value at current prices, but there is a large amount of risk associated with this trade due to Oatly's ongoing losses. I recently suggested that an Oatly long position, offset by a Beyond Meat ( BYND ) short position, would be a reasonable way to take advantage of the valuation and quality spread between these two companies. While some of the valuation spread between the companies has now closed, it should still be far lower.

Market

While some of Oatly's growth headwinds are self-inflicted, concerns about broader adoption of alternative proteins continue to mount, likely driven in large part by health concerns. Pressure on consumer spending is also probably a factor at the moment, causing consumers to shun more expensive options like Oatly.

Competition could also be an issue, although Oatly has a strong brand and data generally points towards stable or increasing market share. In addition, there is little evidence of pricing pressure that would indicate fierce competition.

{kind=link}

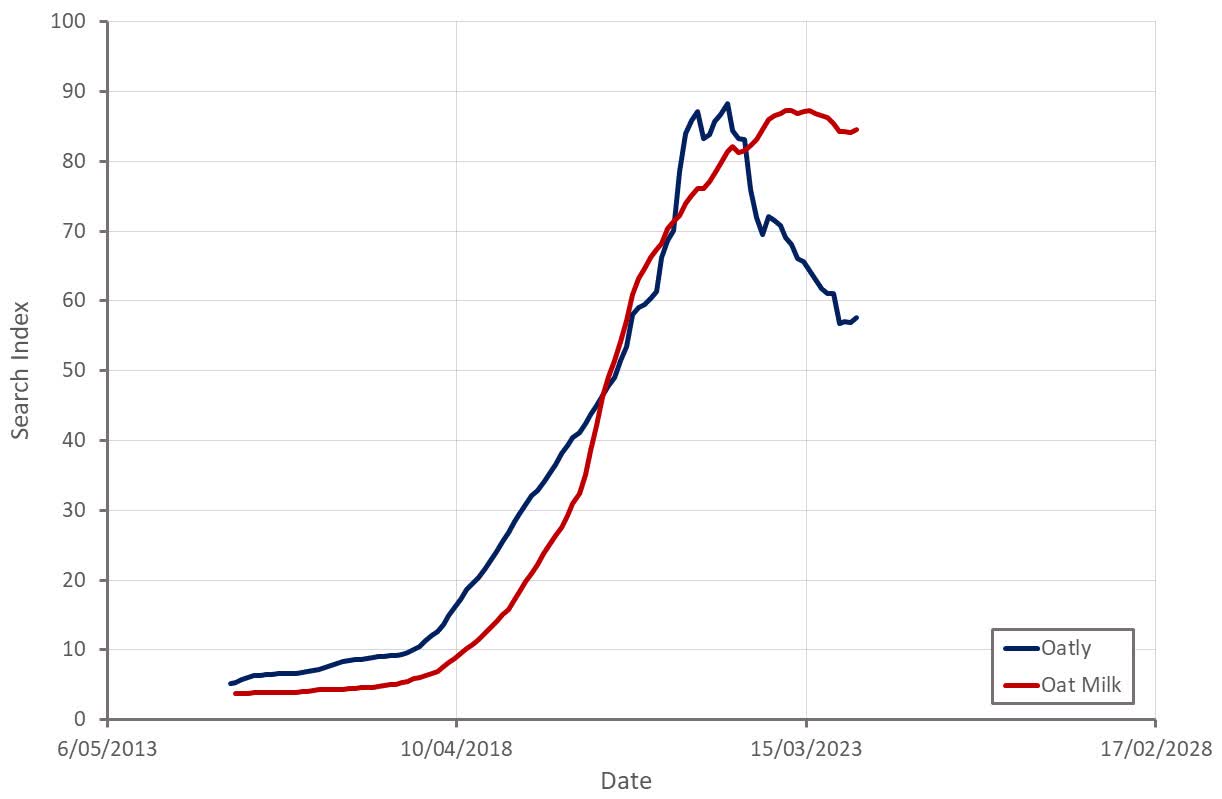

Figure 1: Oatly Search Interest (source: Created by author using data from Oatly)

Plant-based milk market dynamics vary significantly across geographies, broadly reflecting trends observed in plant-based meat. Europe is still an area of strength, but conditions in the Americas and Asia are more difficult.

Figure 2: EMEA YoY Retail Takeaway Sales Growth in Q3 2023 (source: Oatly)

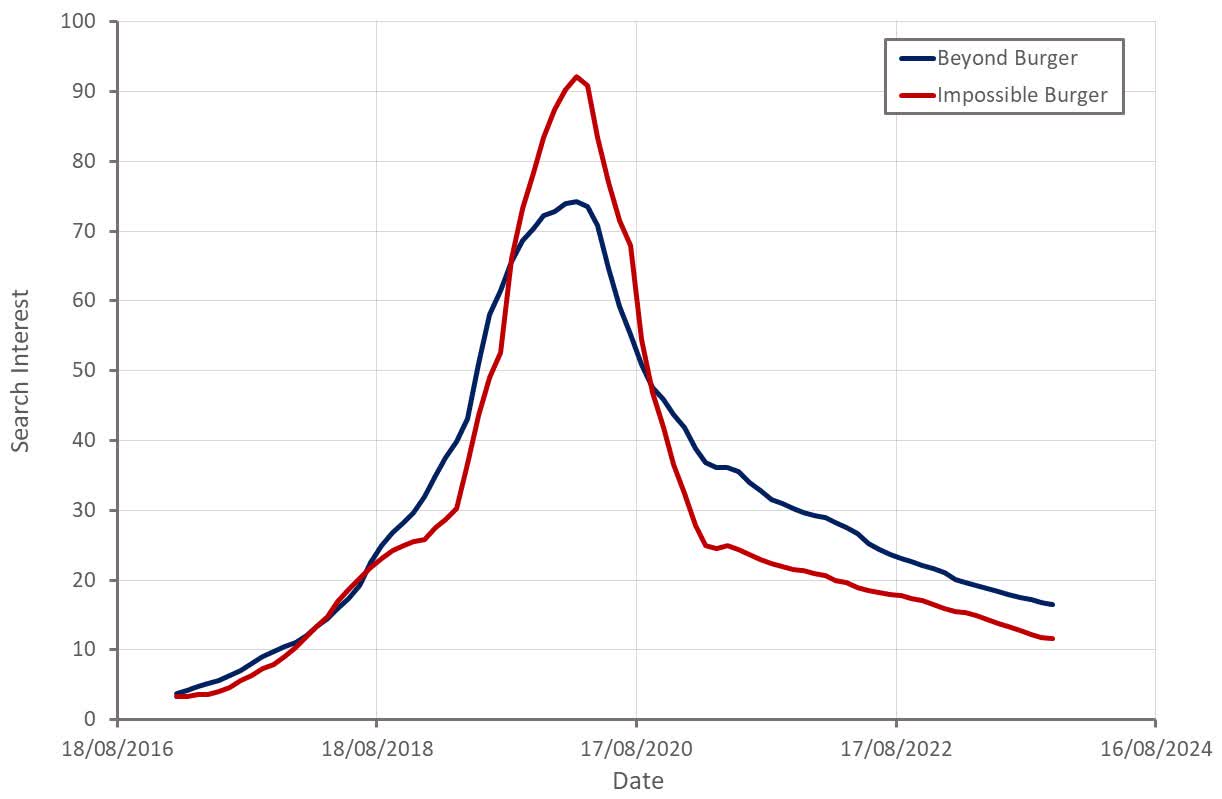

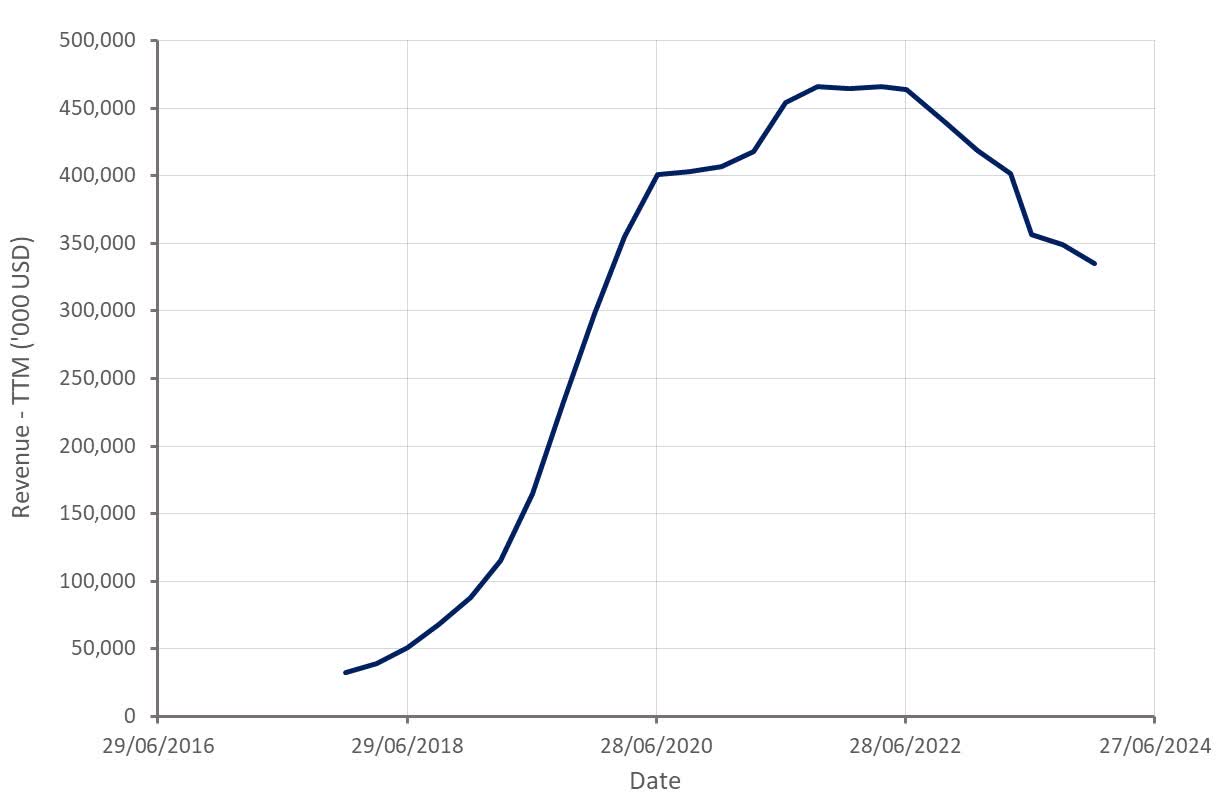

Oatly's current valuation does not require the company to generate significant growth for investors to be rewarded, but recent difficulties across alternative proteins raises questions about the company's long-term potential. Companies like Beyond Meat have also faced weak demand in recent quarters, particularly in North America. Oatly appears to be better placed though as it is not facing the same pricing pressure as Beyond Meat.

{kind=link}

Figure 3: Beyond Burger Search Interest (source: Created by author using data from Google Trends)

{kind=link}

Figure 4: Beyond Meat Revenue (source: Created by author using data from Beyond Meat)

Oatly

Oatly is pursuing an asset-light production model in order to minimize cash burn. This is supported by process improvements that have improved the utilization of its existing facilities. The company also has significant excess capacity at the moment, which has negated the need for CapEx. Oatly currently has roughly 900 million liters of production capacity, compared to around 520 million liters sold over the past four quarters. As a result, Oatly is discontinuing the construction of new manufacturing plants in EMEA and the Americas. While these actions extend Oatly’s runway, it is difficult to view this as a positive. Demand is clearly not meeting the company’s prior expectations, which undermines the company’s value, independent of any near-term profitability or liquidity concerns.

EMEA

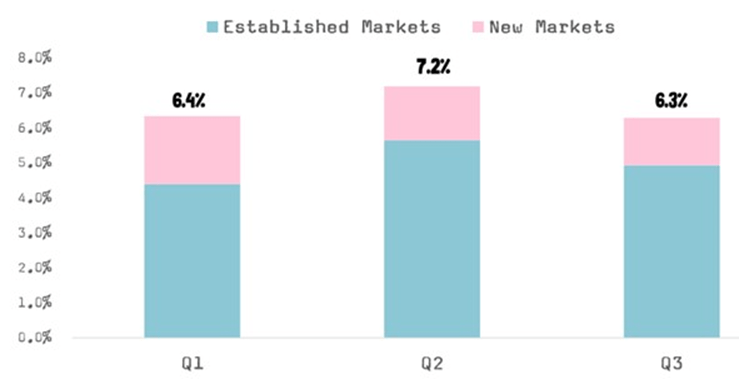

The plant-based milk category continues to expand in EMEA, with oat-milk driving this growth . Oatly’s constant currency net revenue growth in the third quarter was 16% , indicating modest market share gains. Growth in EMEA is being driven by a mix of new and established markets. EMEA was responsible for 54% of Oatly’s third quarter revenue.

Oatly's Go Blue strategy aims to stimulate demand by providing consumers with a product portfolio that is reflective of traditional milk options. The rollout of Go Blue in Germany is reportedly progressing well, with volume increasing 24% net of cannibalization.

{kind=link}

Figure 5: EMEA YoY Volume Growth (source: Oatly)

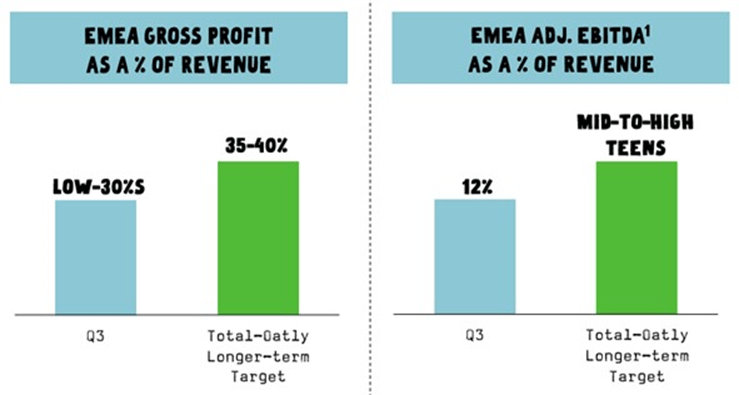

Not only is Oatly's EMEA segment growing, both gross and adjusted EBITDA margins are solid. Oatly believes that margins still have room to expand as capacity utilization is only currently in the low 70s .

{kind=link}

Figure 6: EMEA Margins (source: Oatly)

Americas

45% of Oatly’s Americas revenue was from foodservice in the third quarter, with revenue declining 6% sequentially. Oatly has suggested that this is a result of its pursuit of profitable growth. Excluding the company’s largest customer, Americas foodservice revenue increased 10%.

Oatly is gaining retail market share in the Americas, although the category growth rate has been disappointing. In the last 12-week period, Oatly increased its total distribution points by 18% , with gains at retailers like Meijer, Costco and Walmart. This should help to support growth going forward, even if the category continues to face headwinds.

Co-packer consolidation is helping to support margins in the Americas, with Oatly’s cost of goods sold declining by 10% between Q1 and Q3 2023. The Americas business remains some way off breakeven though, and further growth may be required to achieve this.

Asia Pacific

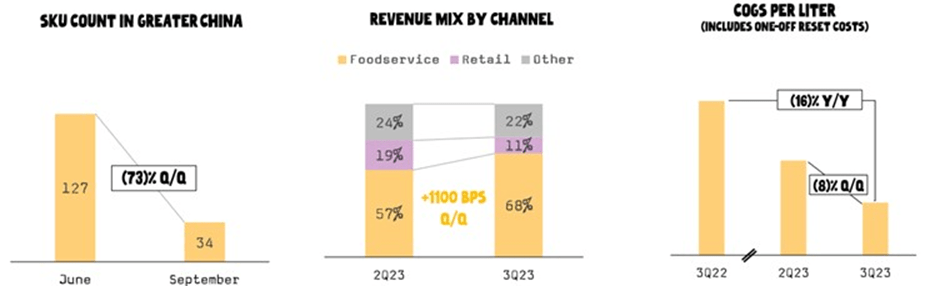

Oatly is also focused on profitability in Asia, which is weighing on the topline at the moment. For example, Oatly is pulling back on certain SKUs, customers, and geographies. More revenue is now coming from the foodservice channel and COGS per liter has declined significantly. As a result, the Asia business improved adjusted EBITDA by 10 million USD YoY . Losses in Asia are still large though and the potential of this business unclear.

{kind=link}

Figure 7: Oatly Asia Pacific SKUs, Revenue Mix and COGS (source: Oatly)

Financial Analysis

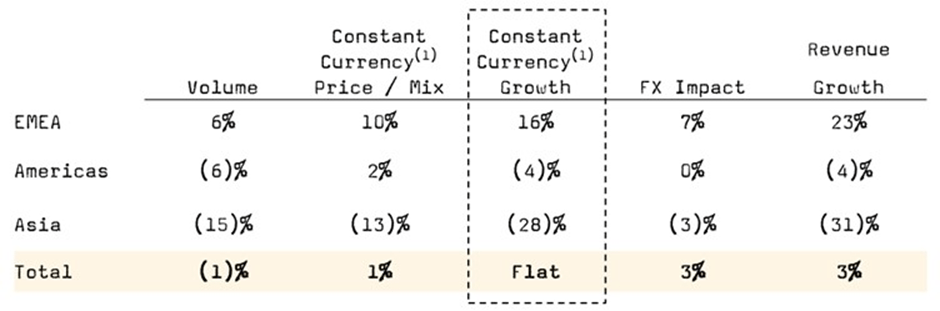

Oatly's revenue growth was only 2.5% YoY in the third quarter of 2023. Volumes declined significantly in the Americas and Asia, although this was somewhat offset by pricing in the Americas. Oatly has suggested that volume declines are the result of a deliberate pursuit of profits, but this is somewhat problematic as it reduces capacity utilization and increases the burden of operating expenses.

{kind=link}

Figure 8: Oatly Growth Breakdown (source: Oatly)

Oatly lowered full year guidance for both growth and gross profit margins, attributing the change to an acceleration of strategic actions . Constant currency revenue growth is now expected to be near the low end of the 7-12% range, and Oatly’s gross profit margin in the fourth quarter is expected to be in the mid-20s compared to a prior expectation of high-20s. The change is largely being attributed to the Americas foodservice business.

Oatly also expects to incur a non-cash impairment charge of 110-150 million USD in the fourth quarter related to the discontinuation of production facility construction in EMEA and the Americas. An additional 40-50 million USD restructuring and exit costs are also anticipated. The net cash impact of these actions over the next 2 years is only anticipated to be around 20 million USD though.

{kind=link}

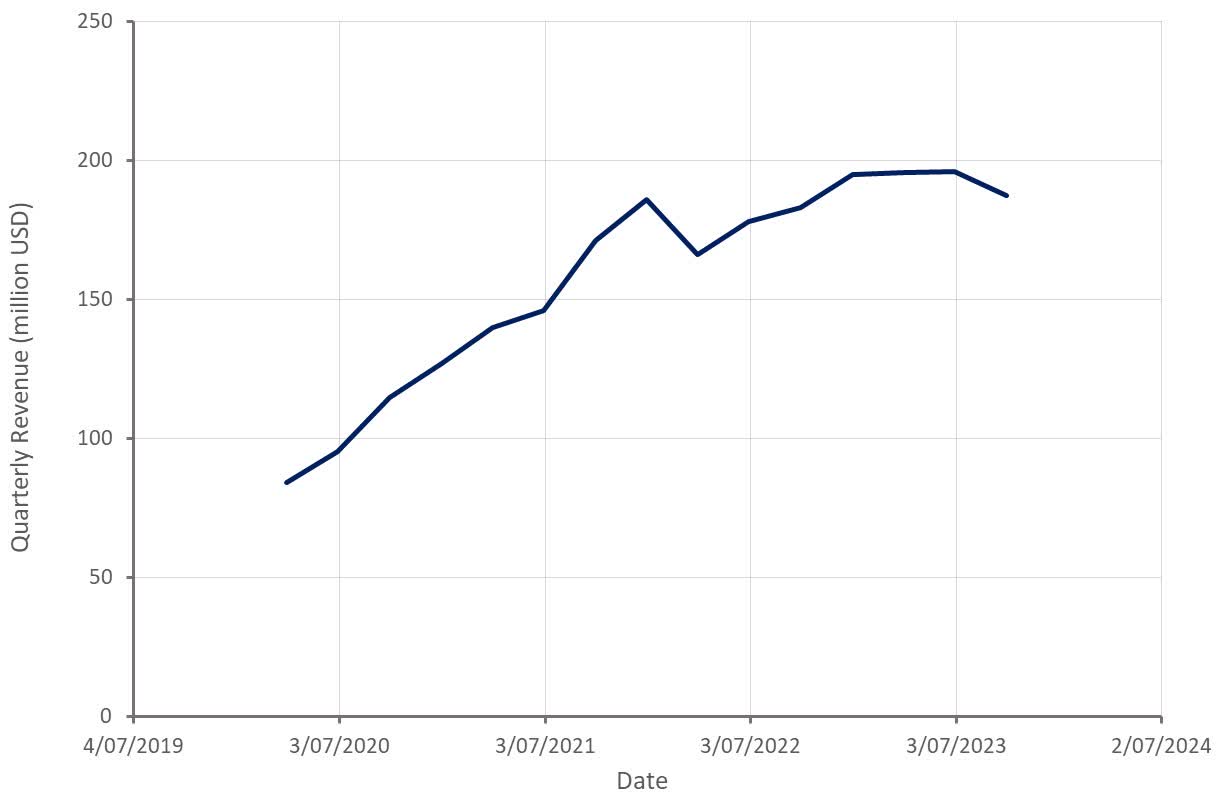

Figure 9: Oatly Revenue (source: Created by author using data from Oatly)

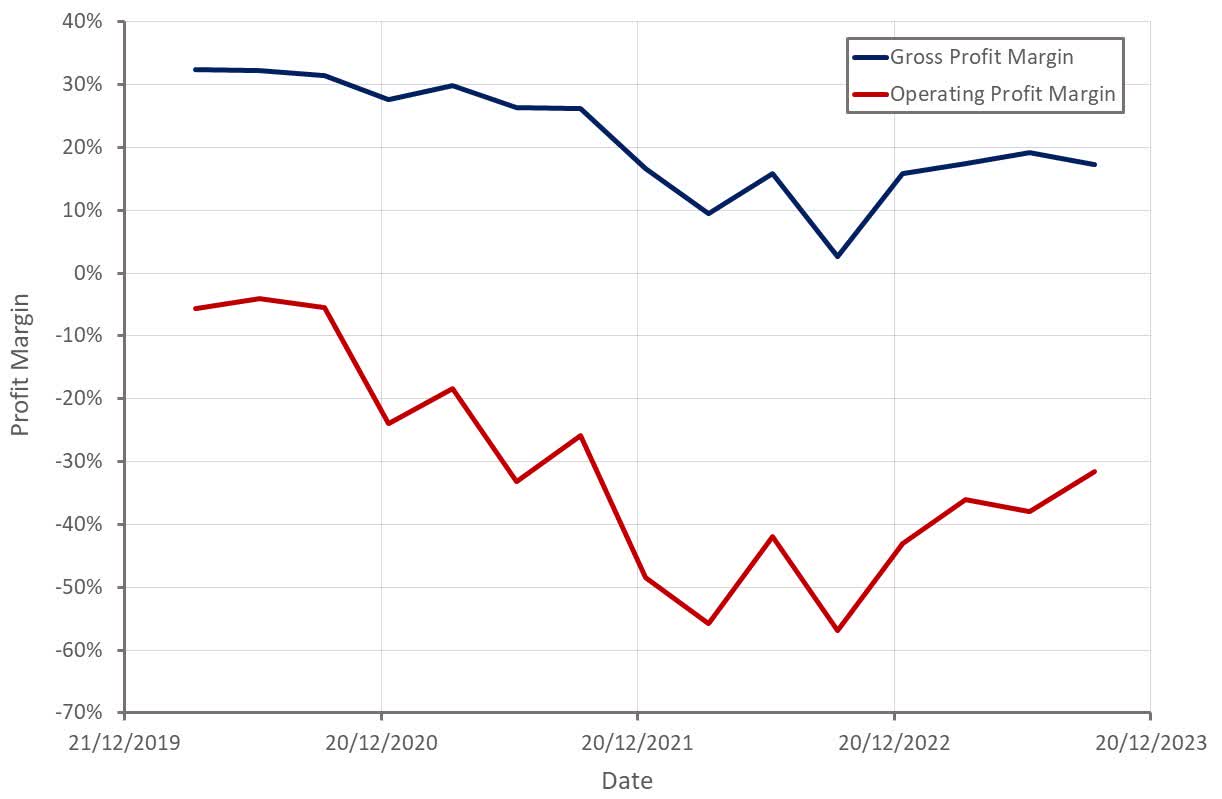

Oatly’s third quarter gross profit included roughly 6 million USD of one-off costs related to actions in Asia, primarily inventory write-offs and co-packer penalties. Excluding this impact, Oatly’s gross profit margin would have been 3.2% higher, demonstrating further sequential gains. Oatly’s adjusted EBITDA also improved sequentially, largely on the back of the 85 million USD cost-saving program announced in the previous quarter.

{kind=link}

Figure 10: Oatly Profit Margins (source: Created by author using data from Oatly)

While adjusted EBITDA margins improved across regions, Asia continues to be a weak spot. Losses in Asia declined significantly YoY, but revenues were also down significantly. Resolving its issues in Asia will go a long way towards helping Oatly reach cash flow breakeven.

Table 1: Oatly Adjusted EBITDA Margin by Region (source: Created by author using data from Oatly)

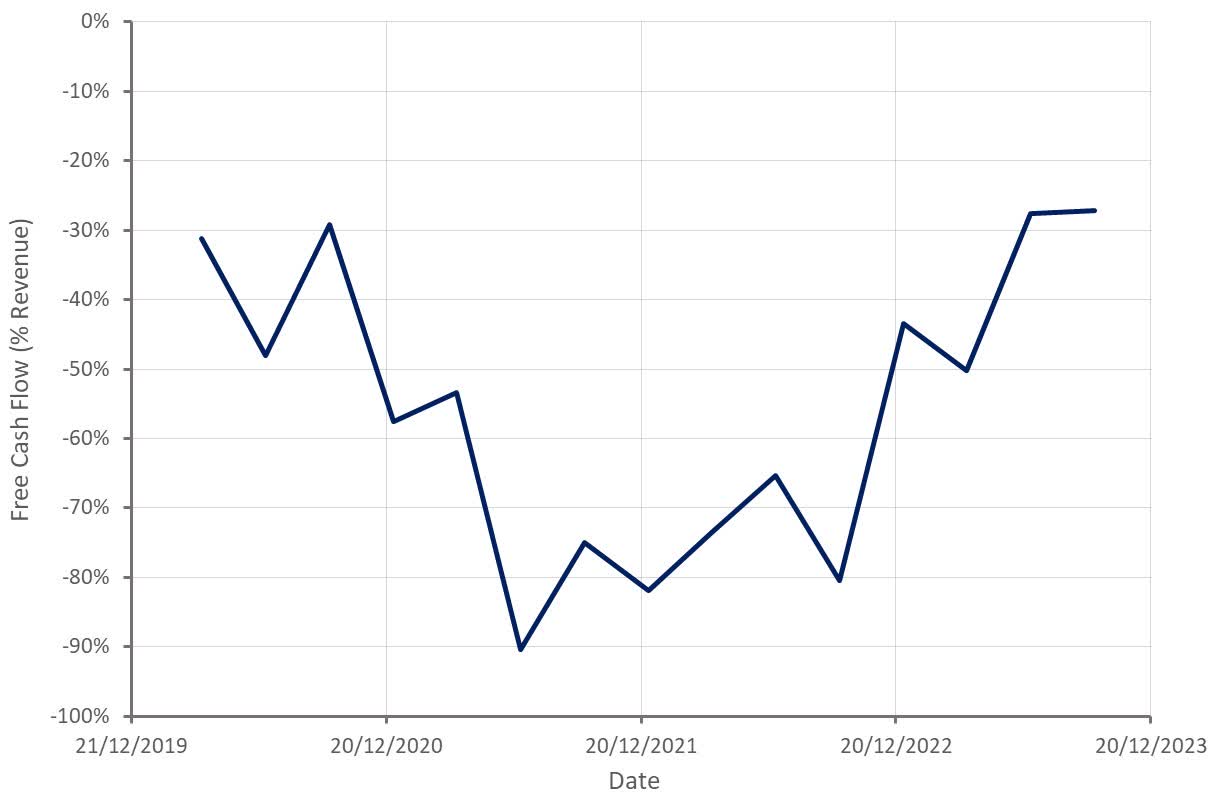

Oatly's cash burn has also been reduced significantly in recent quarters, in part due to reduced CapEx. 2023 CapEx is now expected to be below 75 million USD compared to prior guidance of 110-130 million USD . Oatly has also suggested that 2024 CapEx will be below 75 million USD. This is down significantly from almost 300 million USD CapEx in 2021.

{kind=link}

Figure 11: Oatly Free Cash Flow Margin (source: Created by author using data from Oatly)

While Oatly's cash burn has declined significantly, and the company still has substantial liquidity, there is still work to be done. Oatly has 487 million USD of total liquidity, providing something like 2.5 years runway at the current burn rate. Despite soft growth, Oatly remains confident of achieving positive adjusted EBITDA in 2024.

Figure 12: Oatly Liquidity and Free Cash Flow (source: Oatly)

Conclusion

Despite bouncing significantly after announcing third quarter earnings, Oatly's EV/S multiple is still only around 1. This is reflective of both near-term liquidity concerns and growing doubts about the company's long-term growth prospects. Given that losses are largely due to the Americas and Asia regions, Oatly potentially has a viable oath to profitable growth. This will not be easy though, as the pursuit of profits is weighing on margins, reducing capacity utilization and increasing the burden of operating expenses.

For further details see:

Oatly: Improving Margins Versus Growth Headwinds