OTLY - Oatly: Running Out Of Runway

2023-08-03 10:57:03 ET

Summary

- Oatly's Q2 results were below expectations, largely due to poor performance in China, undermining investor confidence.

- In response, the company is trying to reduce overheads and is focusing resources on its strongest regions and channels.

- Oatly needs growth in order to reduce losses, and this is looking increasingly difficult in the current environment.

Oatly’s ( OTLY ) second quarter results came in below expectations and forward guidance was soft, which appears to largely be the result of poor performance in China. Despite this situation, Oatly still believes it can achieve its 2023 gross margin target and reach adjusted EBITDA breakeven in 2024. Continued poor performance is undermining investor confidence in the strength of the business though. While Oatly's stock is inexpensive, provided the company can transition to profitability and maintain growth, Oatly is currently doing little do demonstrate that this is achievable.

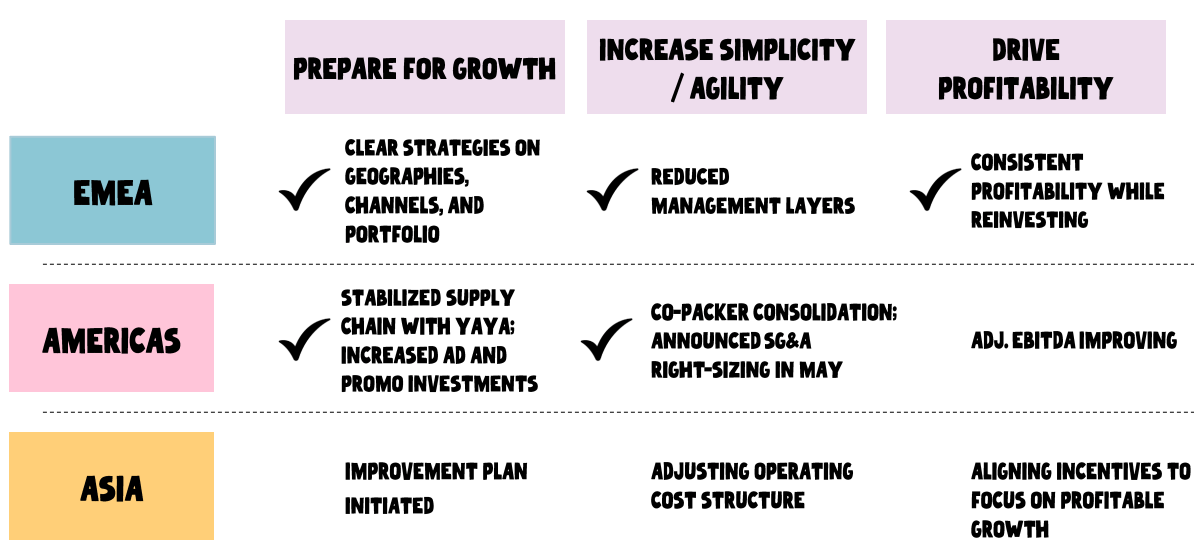

Oatly's tactics appear to have shifted significantly based on the weakness of the second quarter. Much of this is based around reducing overheads while putting resources behind the company's strongest regions and channels.

Figure 1: Oatly Growth/Profitability Initiatives by Geography (source: Oatly)

{kind=link}

EMEA

EMEA is Oatly’s most mature region, and it continues to achieve robust growth with positive adjusted EBITDA. This is somewhat surprising given current economic weakness in Europe, but it demonstrates the potential of Oatly's business. Whether this success can be replicated globally is still unknown though.

Figure 2: EMEA Plant-Based Milk Performance (source: Oatly)

Growth in EMEA continues to be aided by expansion into new markets, with these markets increasing their share of Oatly’s EMEA sales volumes from 4.7% to 5.2% over the past year.

Oatly has introduced new oat milk SKUs in Europe which it believes better replicate dairy options and will to higher margins. Oatly refers to this as its “Go Blue” portfolio:

- Semi – Oatly’s original oat drink with 1.5% fat.

- Whole – Oatly’s creamiest oat drink is designed to replicate full-fat cow’s milk.

- Light – Oat drink with 0.5% fat. Designed to replace low-fat cow’s milk.

- No Sugar – Oatly’s normal production process involves breaking down starch into sugar. This step is omitted from the production of No Sugar oat milk.

The "Go Blue" portfolio is reportedly driving incremental growth for Oaty and the category.

Figure 3: UK "Go Blue" Mix Shift (source: Oatly)

Americas

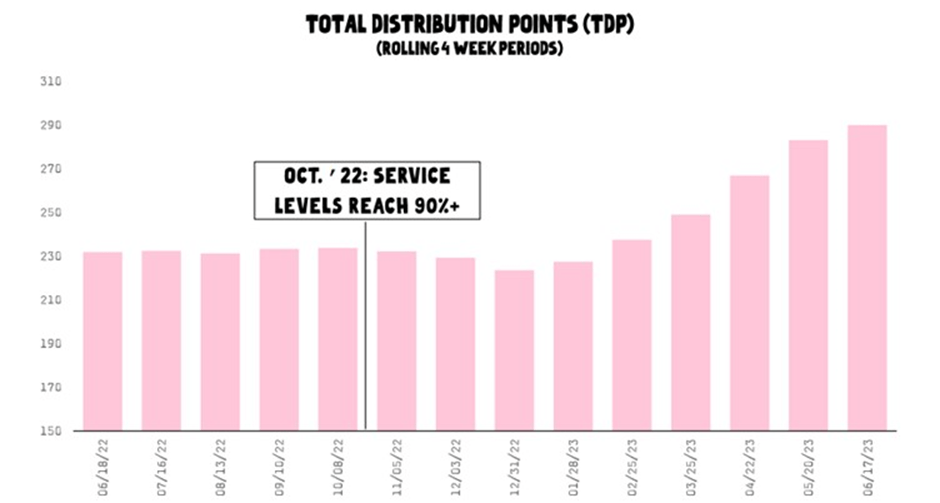

Oatly has increased its retail distribution in the Americas by 24% since its supply chain stabilized, but this distribution build has been below the company's expectations. No real reason has been given for this though and it raises the question of sales performance. Oatly has stated that it is confident it will continue to gain distribution, albeit at a slower pace than originally expected.

Figure 4: Americas Retail Distribution (source: Oatly)

{kind=link}

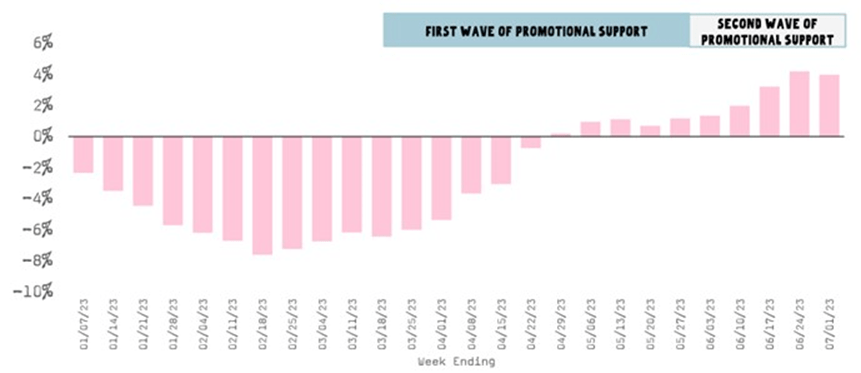

In addition to expanding distribution, Oatly has stepped-up advertising support for its Americas business. This is leading to volume growth, on top of higher pricing, but this growth is modest in light of distribution growth.

Table 1: Americas Ad Spend (source: Created by author using data from Oatly) Figure 5: Americas YoY Growth in Units - Rolling 12 Week Periods (source: Oatly)

{kind=link}

Asia

Oatly had been positioning for a post-pandemic recovery in Asia by investing in things like new products, distribution, in-store promotions, sampling, and advertising. The expected tailwinds have not eventuated though, which appears to be due to a slower than expected recovery in China. The pace of expansion in Asia is now being tempered with the goal of reducing losses. This appears to involve a greater focus on core channels and SKUs with less sales and marketing investments.

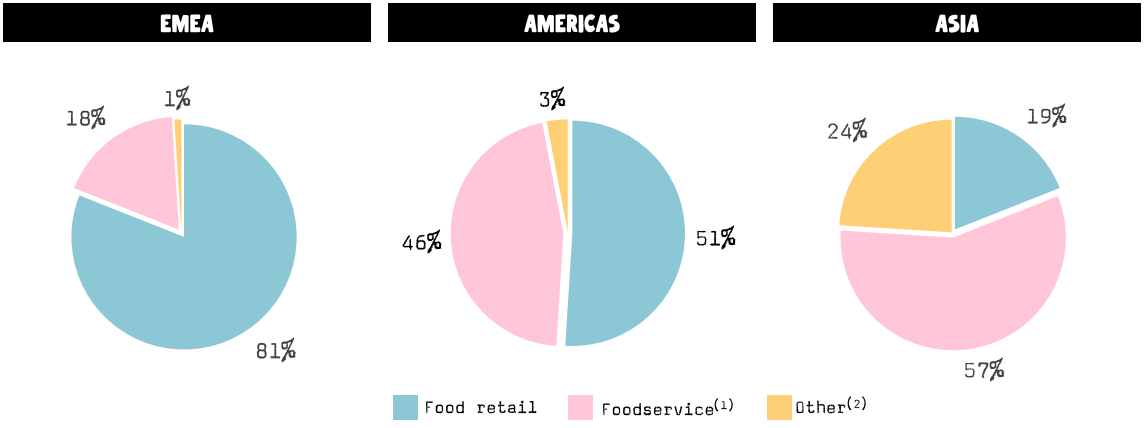

The majority of Oatly's revenue in Asia comes through the foodservice channel and this business is fairly geographically concentrated. Oatly will now focus on expanding its retail presence in those markets to capitalize on brand awareness. Oatly will also be slowing SKU expansion and eliminating many existing SKUs to help control costs.

Figure 6: Oatly Revenue Contribution by Channel (source: Oatly)

{kind=link}

Oatly still believes that the Asia region has huge potential, which appears somewhat questionable at the moment given Oatly’s large losses and modest growth in the region. This may be due to the disproportionately high number of people in the region who are lactose intolerant. It may also reflect Oatly’s prior commitments to the Asia business, having built two production sites and establishing the Oatly brand as a leader in the plant-based market in China.

Financial Analysis

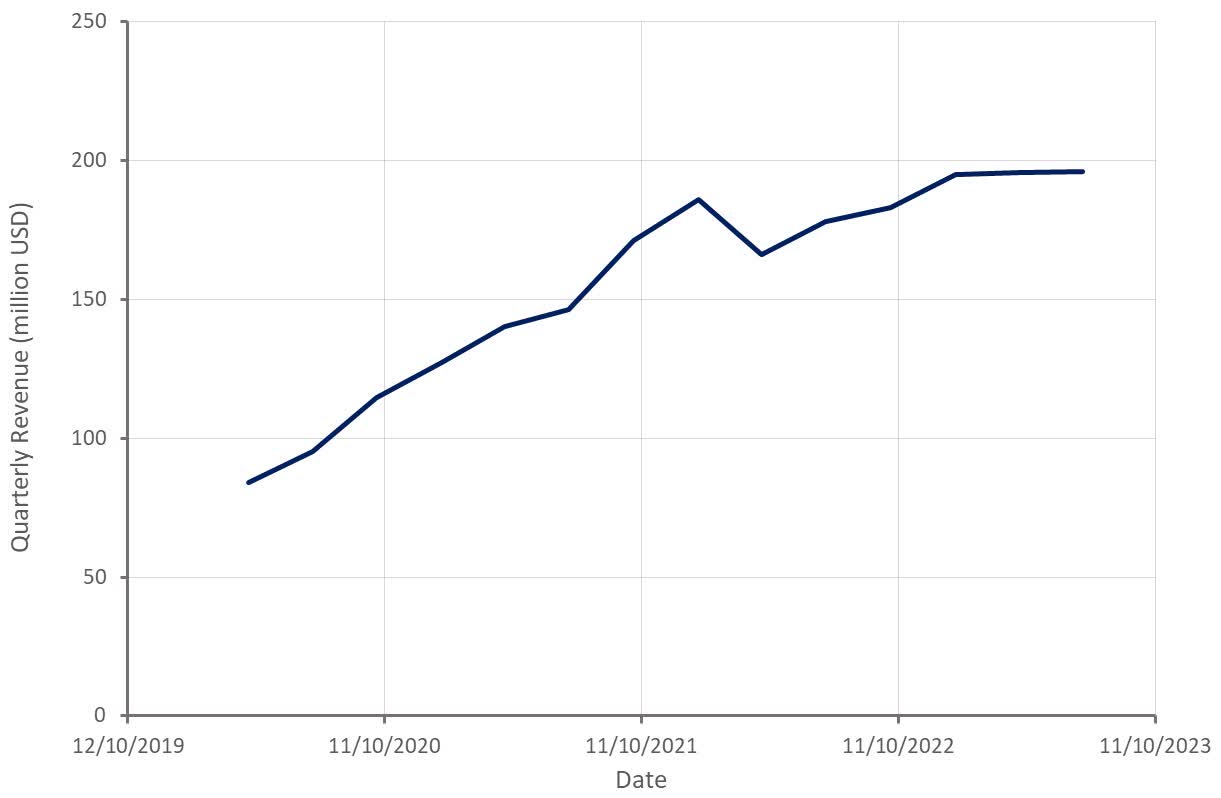

Oatly’s revenue growth decelerated sharply in the second quarter and the company is now expecting revenue to be fairly flat through the remainder of the year, with modest YoY growth. Management has stated that roughly two thirds of the reduction is due to the Asia segment, with the remainder being driven by a more conservative outlook for the Americas. The outlook for the EMEA business remains unchanged.

Figure 7: Oatly Revenue Growth (source: Created by author using data from Oatly)

{kind=link}

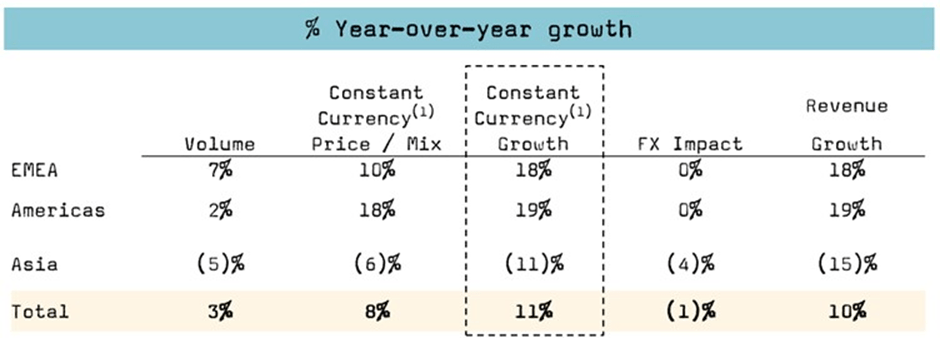

Second quarter growth was strong in EMEA and the Americas, driven in large part by higher prices. Revenue dropped substantially though, offsetting much of this strength. Pricing has been an important growth driver in the Americas over the past year, but Oatly will lap the Americas price increase in August. This will naturally lead to a far lower growth rate in the Americas going forward.

Figure 8: Oatly Second Quarter Revenue Bridge (source: Oatly)

{kind=link}

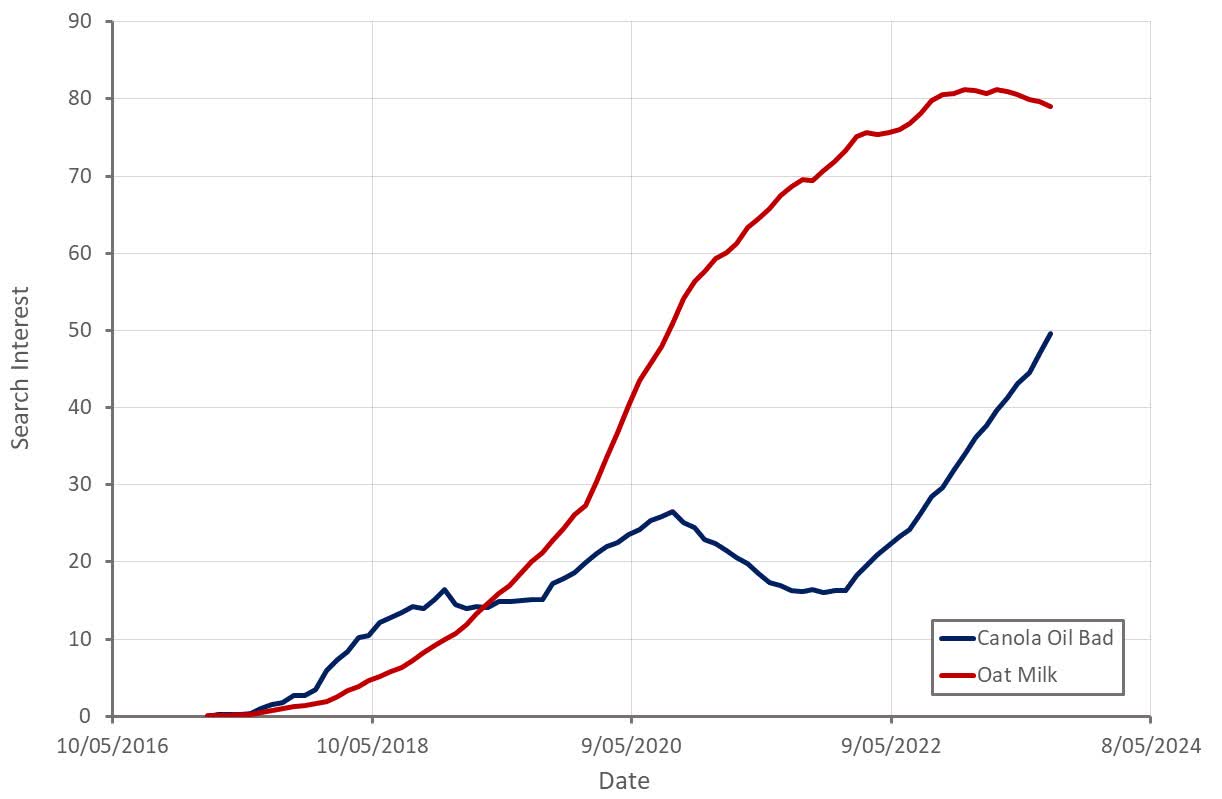

A potential reason for Oatly's flagging growth could be mounting concerns regarding the health impact of plant-based dairy products. Most of these products use a vegetable oil, like canola oil, to help create the right sensory experience.

Canola oil contains elevated levels of omega-6 fatty acids relative to omega-3 fatty acids which contributes to inflammation, something that has been linked to a number of chronic conditions like Alzheimer’s, obesity and heart disease. In addition, over 90% of canola crops in the US are genetically modified, which is a health concern for many people.

This sentiment is potentially being fueled by the dairy industry. Industry groups have previously campaigned against plant-based milks and lobbyists have taken issue with plant-based dairy products referring to themselves as milk. This is nothing new though, with the dairy industry rallying hard against the introduction of margarine over a century ago.

Whether health concerns have any merit and where the concerns come from may not really matter. Plant-based meat and dairy products have been positioned as direct replacements for existing products and are likely to continue facing resistance as they proliferate.

Figure 9: "Oat Milk" and "Canola Oil Bad" Search Interest (source: Created by author using data from Google Trends)

{kind=link}

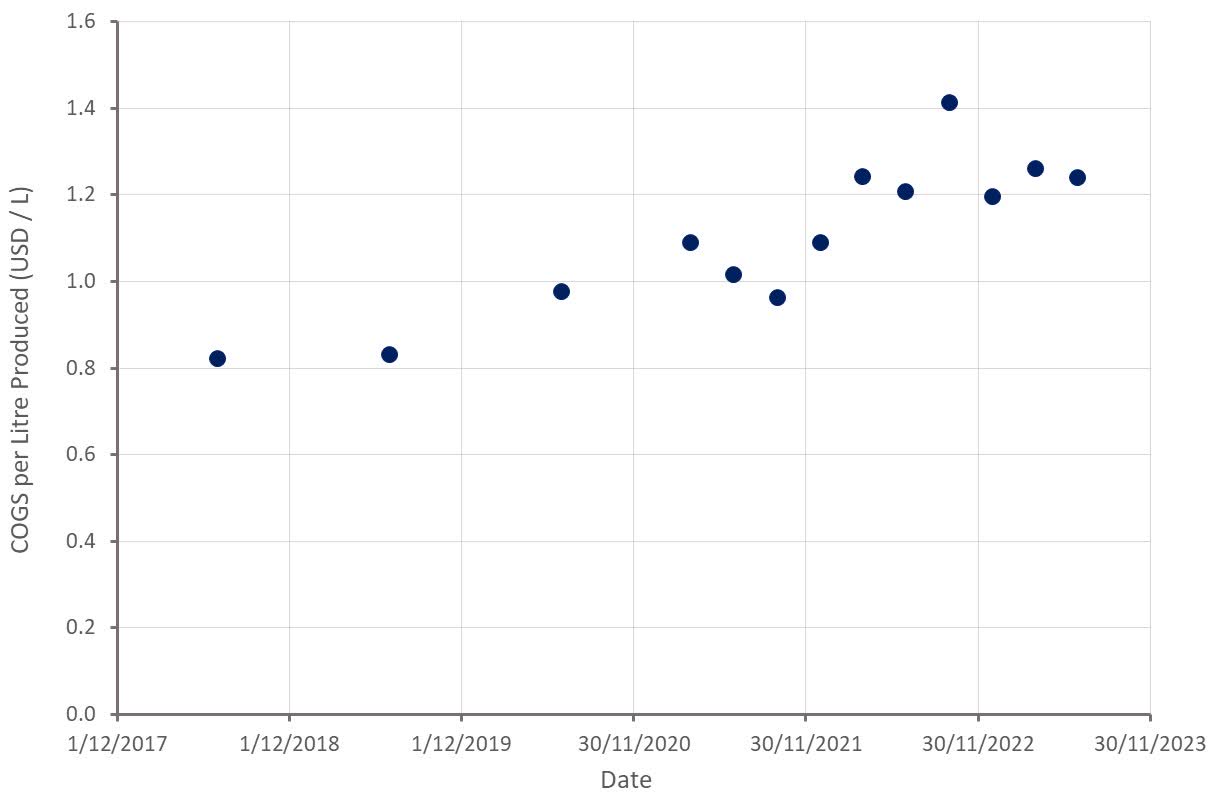

Oatly expects gross profit margins to continue improving throughout 2023 and is still targeting 35-40% gross profit margins long-term. COGS remain elevated relative to pre-COVID levels though, despite supply chain pressures easing and the price of oats falling substantially, meaning that pricing has largely been responsible for the improvement in gross profit margins. Oat prices have rebounded over the past 3 months and there is a risk that this will pressure margins going forward.

Figure 10: Oatly COGS per Litre Produced (source: Created by author using data from Oatly)

{kind=link}

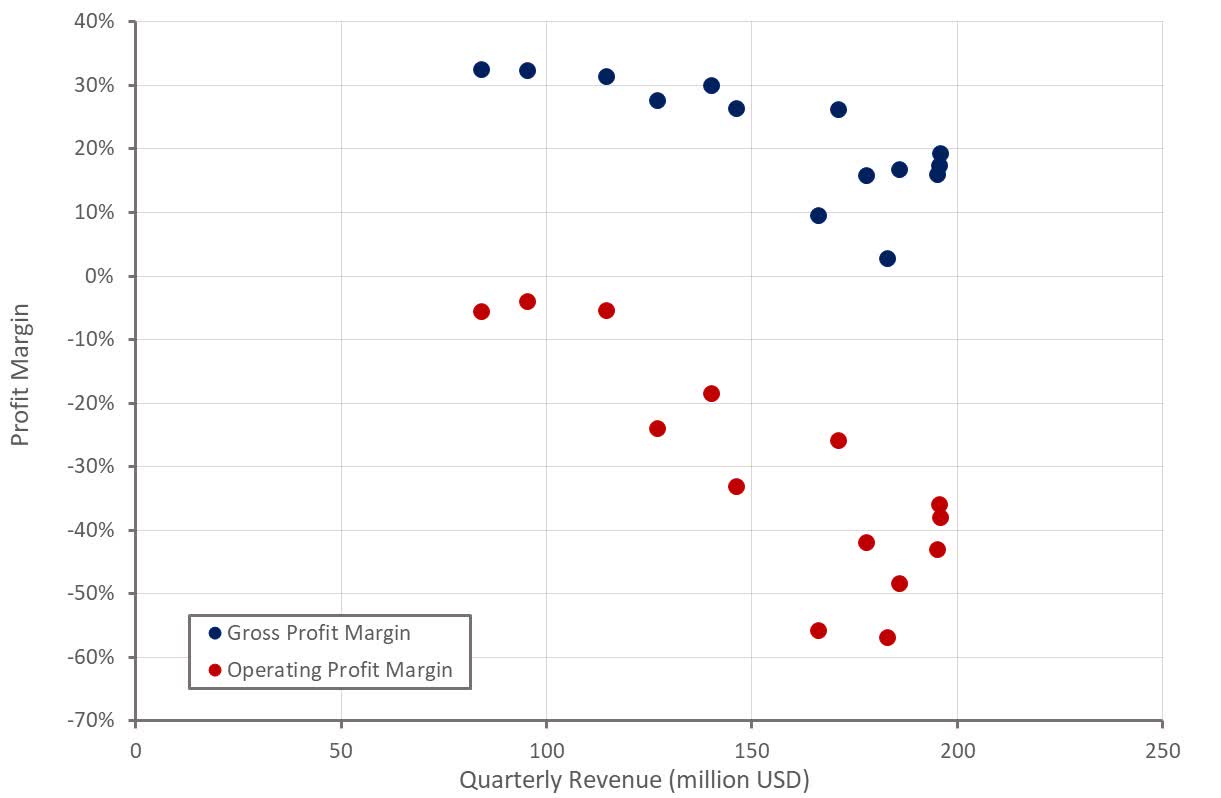

Oatly's operating profit margins have improved in recent quarters but are still low. The company must realize operating leverage to correct this situation, a difficult ask in the current environment.

Figure 11: Oatly Profit Margins (source: Created by author using data from Oatly)

{kind=link}

Oatly's margins vary significantly across regions, with the less mature Americas and Asia businesses driving losses. Even the EMEA business is probably not profitable on a GAAP basis though.

Table 2: Oatly Adjusted EBITDA Margin by Region (source: Created by author using data from Oatly)

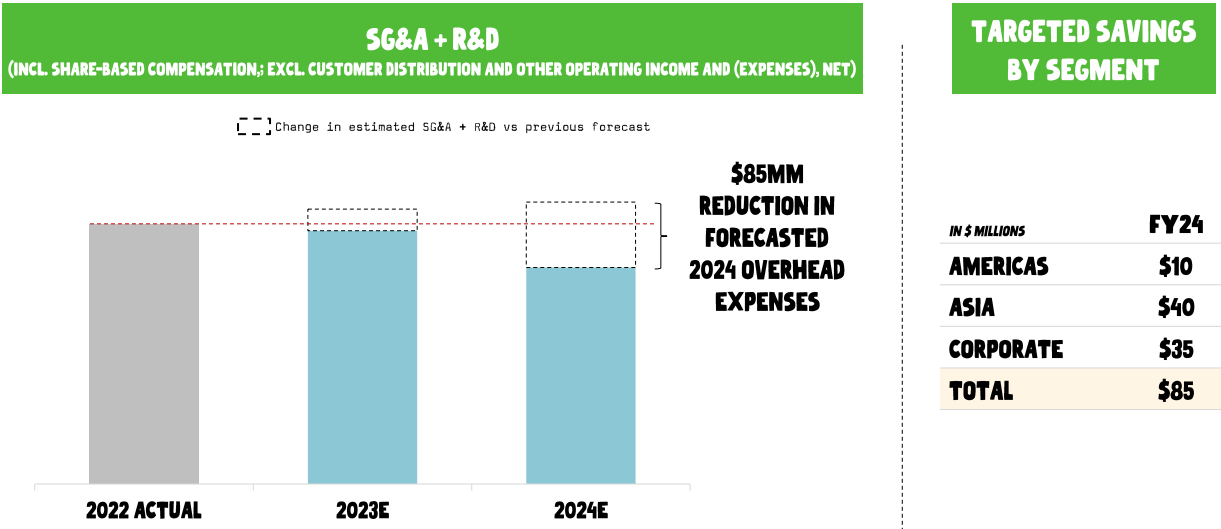

Oatly is conducting an improvement plan in Asia and simplifying its corporate functions and Americas overhead, which it expects will to lead to an 85 million USD reduction in costs by 2024. These savings will primarily come from non-employee expenses but will also involve some eliminated jobs. Oatly is not planning on cutting back on advertising though. It should be noted that these cost reductions will not be sufficient to make Oatly profitable on a GAAP basis in 2024 unless growth is robust.

Figure 12: Oatly Targeted Savings by Region (source: Oatly)

{kind=link}

Oatly raised 465 million USD during the second quarter and had 340 million USD of cash and cash equivalents on its balance sheet at the end of the quarter. Oatly also has access to a 200 million USD revolving credit facility. This means that Oatly probably still has something like 2 years of runway at its current burn rate in which to resolve its issues.

This is doable, but Oatly needs to improve its gross profit margins and operating efficiency while continuing to grow its business. Oatly is now only guiding for 7-12% YoY constant currency revenue growth, which likely means that revenue growth in the fourth quarter will be in the low single digits. The companty reiterated its expectation of achieving a gross profit margin in the high 20% range in the fourth quarter.

CapEx guidance for 2023 has been reduced from 180-200 million USD to 110-130 million. While CapEx expectations have been reduced significantly, this will still require a significant increase in investment in the second half of the year relative to the first.

Conclusion

It is easy to dismiss the plant-based dairy category as a commodity market with little potential, but this ignores the fact that many commodity CPGs develop into strong brands. Oatly's performance in EMEA indicates that this is a possibility, but this success is yet to be replicated globally. While Oatly's ability to handle increased competition long-term remains to be seen, the immediate focus is in on Oatly's cash flows and balance sheet. Oatly's balance sheet gives it a several years to reduce cash burn, but without a return to solid growth this will be difficult.

For further details see:

Oatly: Running Out Of Runway