OTLY - Oatly's Cash Burn Crisis: Is This The Ultimate Buy-Low Opportunity? (Rating Upgrade)

2023-11-03 18:54:02 ET

Summary

- Oatly's stock has fallen 77% and is now at a more attractive valuation level, prompting a second look at the company.

- The company reduced its revenue growth guidance and capex outlook for 2023 due to muted performance in its Asia segment.

- Management's focus on core SKUs in Asia aims to generate positive EBITDA by FY 2024.

- Strong pricing power and volume growth in EMEA and Americas regions indicate resilience against inflationary pressures.

- Oatly is in survival mode and its current valuation reflects a distressed asset valuation, but its long-term vision and brand strength make it a convincing investment.

Background: Revisiting Oatly Amidst Market Changes

We started rating Oatly Group AB (OTLY) as neutral in April. Given its strong brand in the plant-based milk category, we believe the company merits a second look. However, at one point, our DCF model suggested a $593 million ($1 per share), a 56% decline from the level at which we wrote the article. In order to keep costs down and meet demand from around the world, the company was at the time rapidly growing its manufacturing capacity. However, we did not believe it was the right time to buy given the possibility of construction delays and an inflated valuation. On November 9, the business was scheduled to release its Q3 earnings. Since April, the stock has fallen 77% and has come to a comparatively attractive valuation level that merits more research from us.

{kind=link}

Recent Events: Oatly's Adjusted Forecasts and Financial Moves

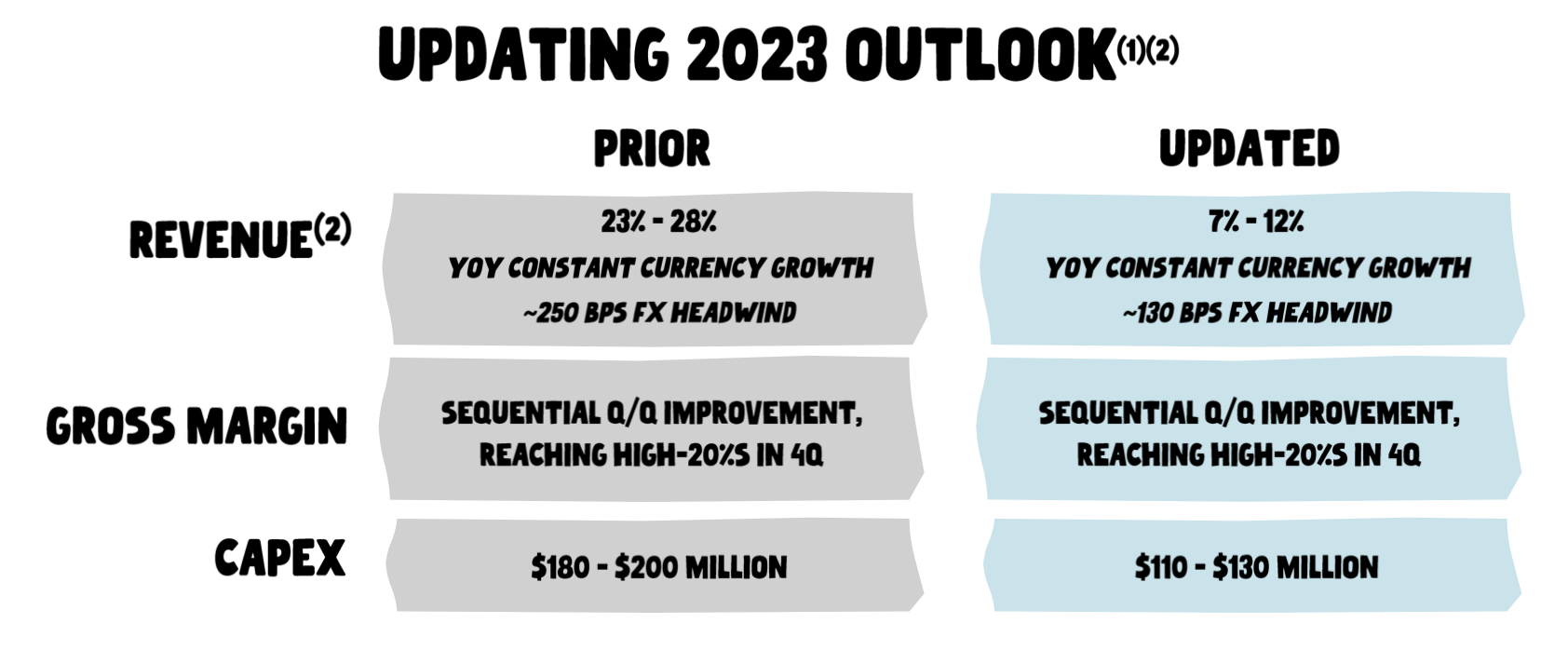

Since then, a lot has changed. In Q2, the company reduced its revenue growth guidance from the range of 23%-28% to 7%-12% and slashed its capex outlook for 2023 by about 40%.

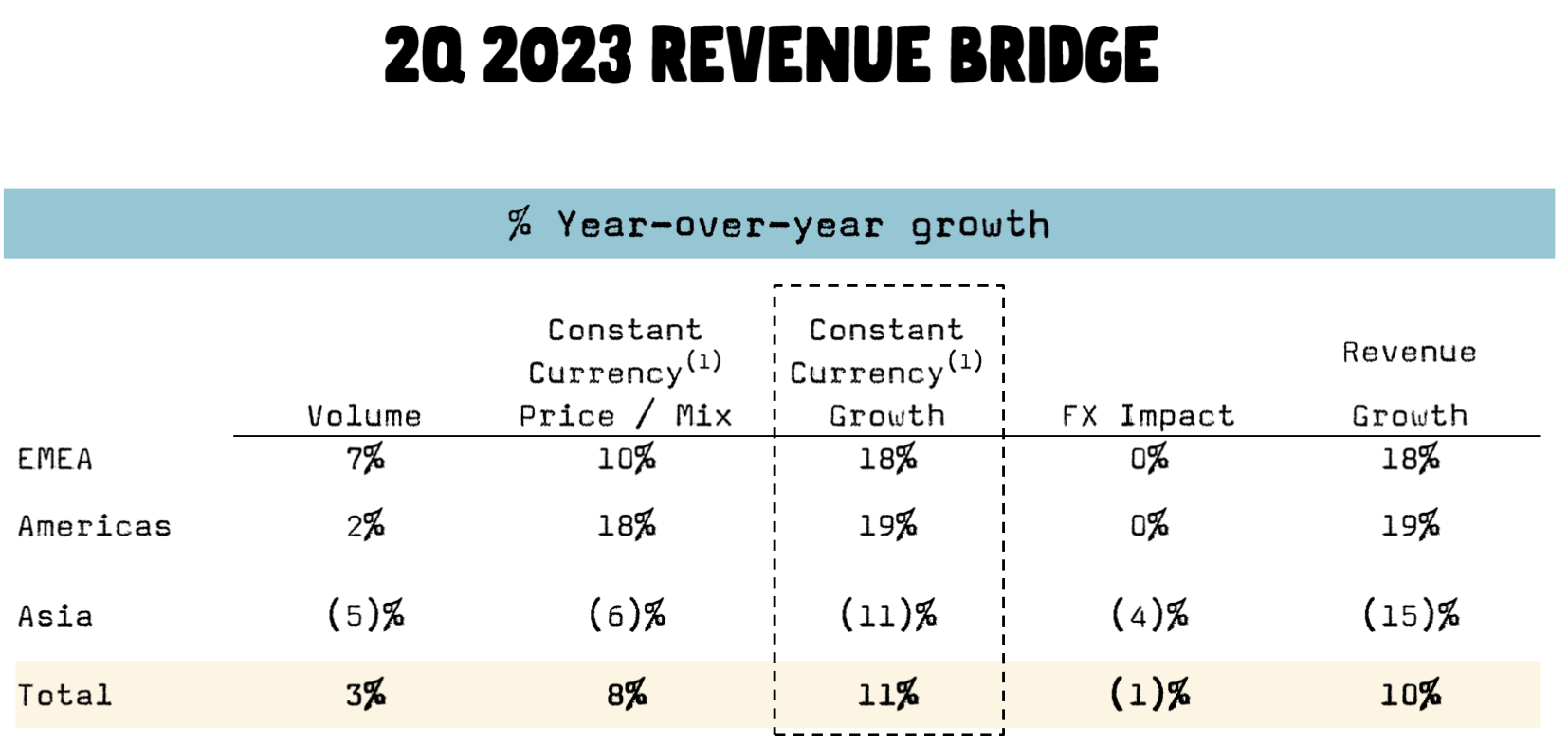

What took place? The revenue growth of the company's Asia segment was muted. Asia revenue declined 14.9% in Q2, a sharp slowdown from Q1's 16.4% growth. The management explained it away as China's post-COVID recovery being slower than anticipated. As a result, its performance in China was still being watched. Despite the fact that its Aisa segment underperformed, its EMEA and Americas segments grew by 17% and 19% over the quarter, respectively, thanks to volume and price.

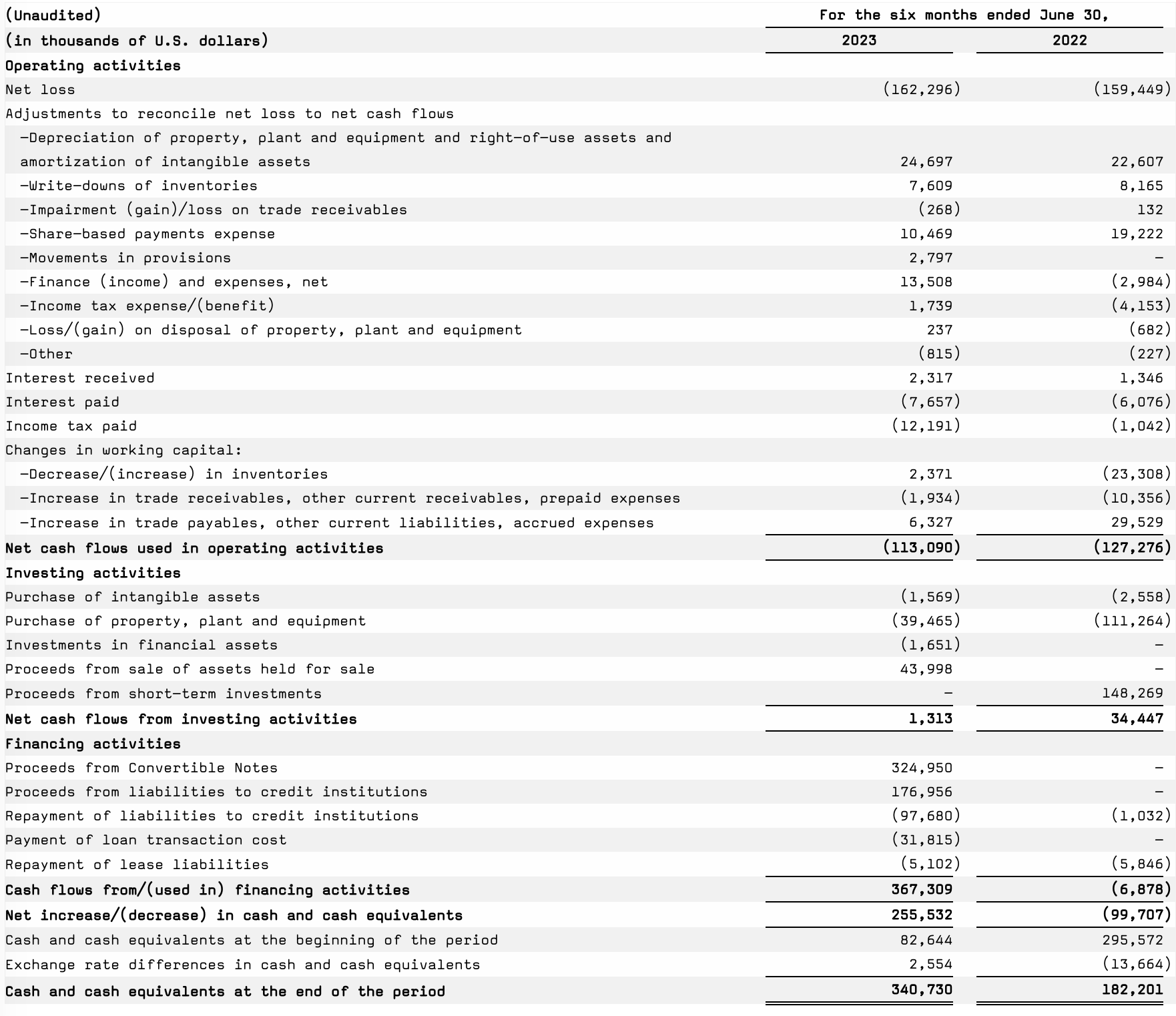

In addition, the company finished an expensive financing of $125 million in the quarter and accumulated cash of $340 million. The company lowered its capex to $40 million in the quarter from $113 million last year through the sale of assets and shift toward the hybrid model, which will lower its capex needs and lessen its cash burn. The company incurred a $113 million cash burn for the H1 2023. Hence, based on current spending patterns, the company is likely to only have sufficient cash to operate for the next 12 months.

{kind=link}

Hence, we think the company is still in survival mode. That also explains its current value of P/B around 0.5x as the market expected it to continue to burn cash for the next couple of quarters. Specifically, the market's current value of $287 million seemed to only incorporate the cash position of $340 million $56 million operating cash outflow, and $40 million capex. So, the valuation does not reflect a discount valuation but a more fair value from distressed asset valuation.

{kind=link}

Risks in Management Outlook: Navigating Through Cost Cuts and Market Dynamics

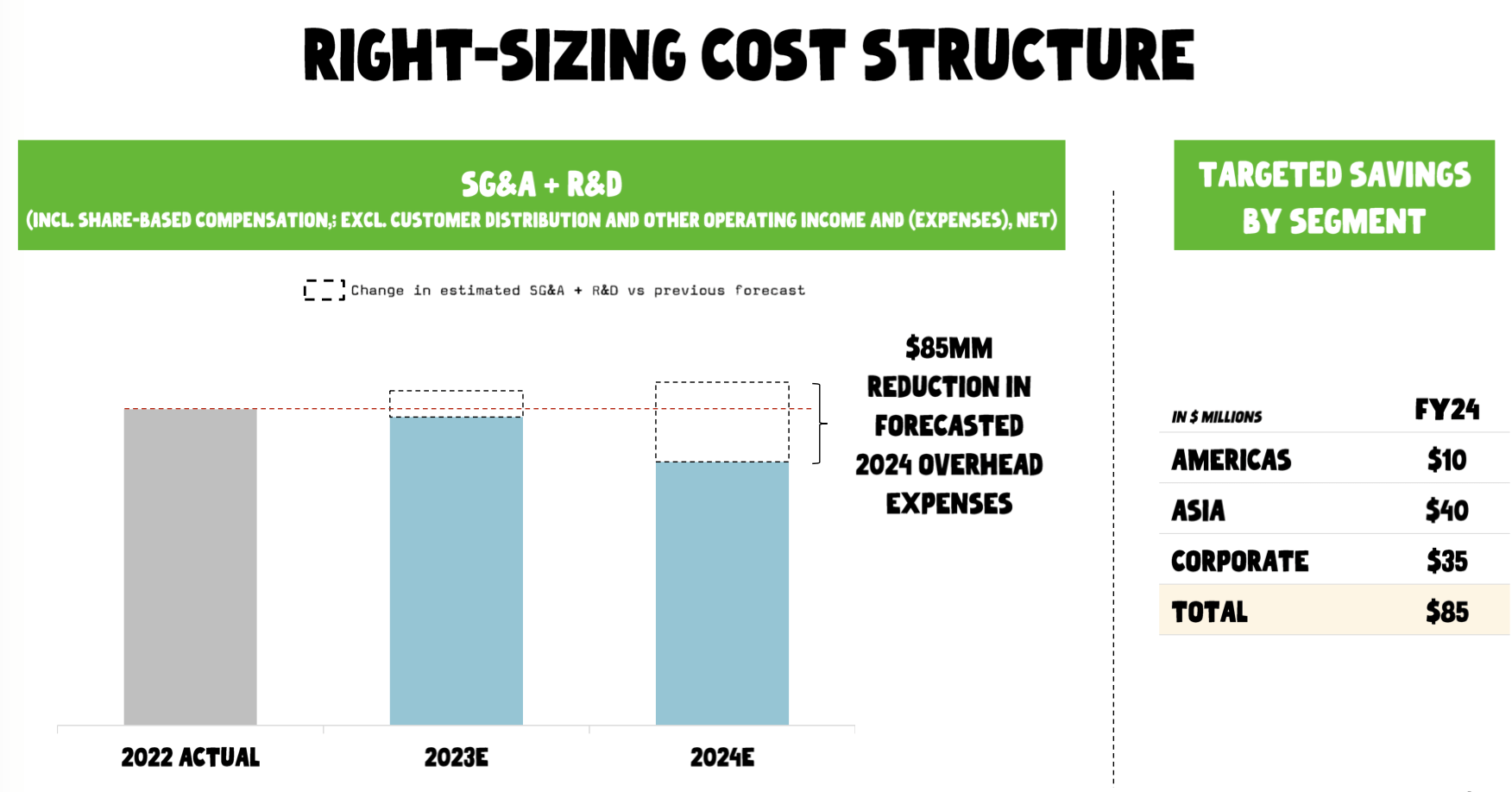

The company continued to make investments to grow its business. Hence, the management expects the company can generate positive EBITDA in FY 2024 primarily through cost-cutting in the Asia segment and corporate. If they successfully execute the cost-cutting plan on track, they should stop the cash burn. Therefore, we can expect the stock to be repriced downward until it stops cash burn.

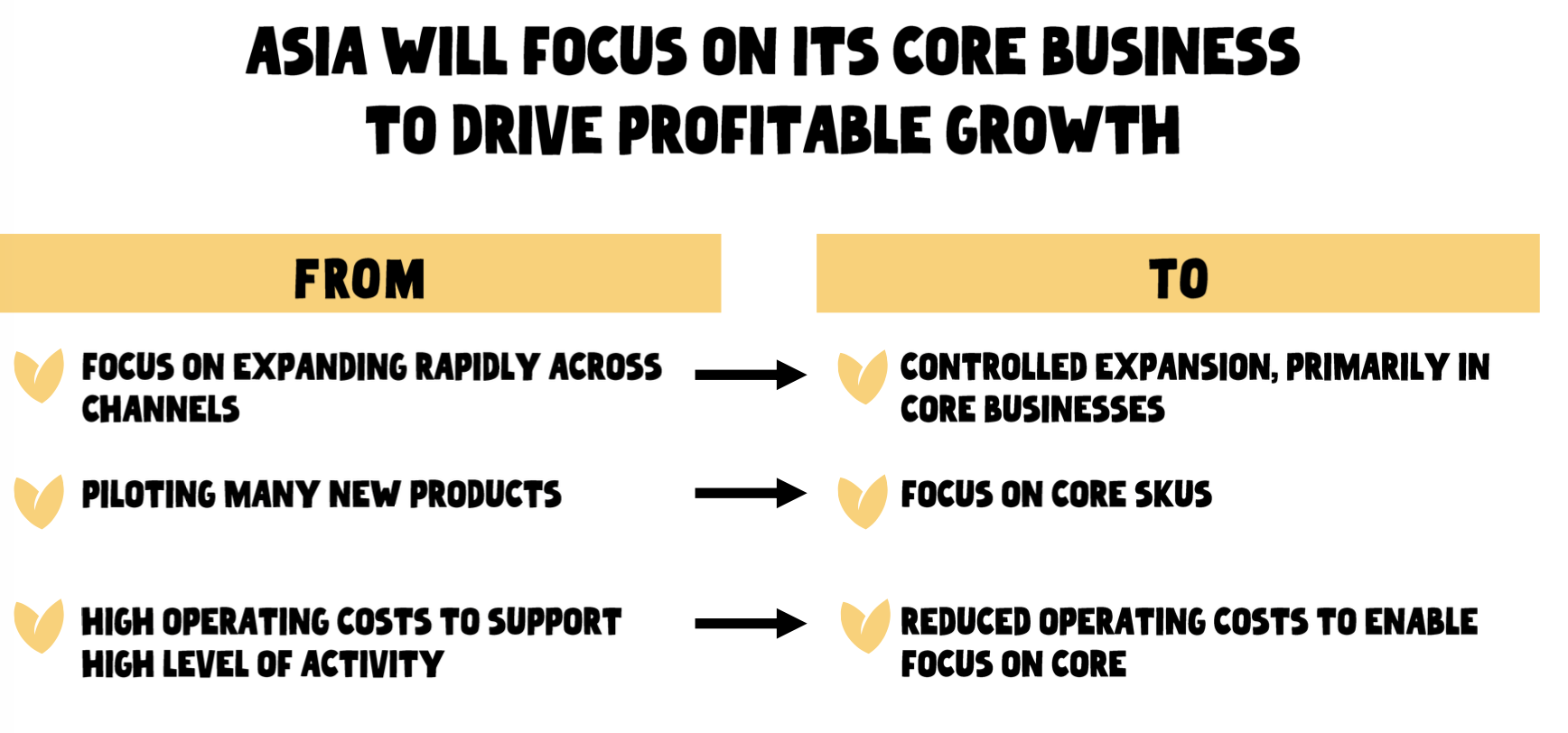

The management expects Asia segment cost cutting from controlled expansion, meaning that they will focus on core SKUs. Our comments on this is that one of the primary reasons the Asia market underperformed is likely due to the weak economy in China as soy milk is the largest non-dairy milk product in China. Oat milk is more consumed by young consumers who are willing to try new things. Given that oat milk is more expensive than soy milk or milk, consumer spending on oat milk is definitely impacted by the weak economy in China. Hence, we do not expect the trend will rebound if China's economy remains weak. However, given that the lactose intolerance percentage population can be as high as 90% , much higher than Western countries of less than 10%, the total addressable market can be larger than Western countries. Hence, the management's long-term vision still makes a convincing argument to us.

{kind=link}

Market Performance and Competitive Edge

From a product development perspective, we continued to expect strong growth in the EMEA and the Americas as a couple of data points support its strong pricing power.

{kind=link}

First, their growth in the EMEA and the Americas is driven by price/mix, which increased double digits in the quarters. The volume also grew by single digits, suggesting that inflation has not caused a severe impact on the traffic.

Further, they generated EMEA and Americas business revenues 81% and 51% from food retail channels and less from food service. This suggested that their brand strength as competition in food retail is more severe.

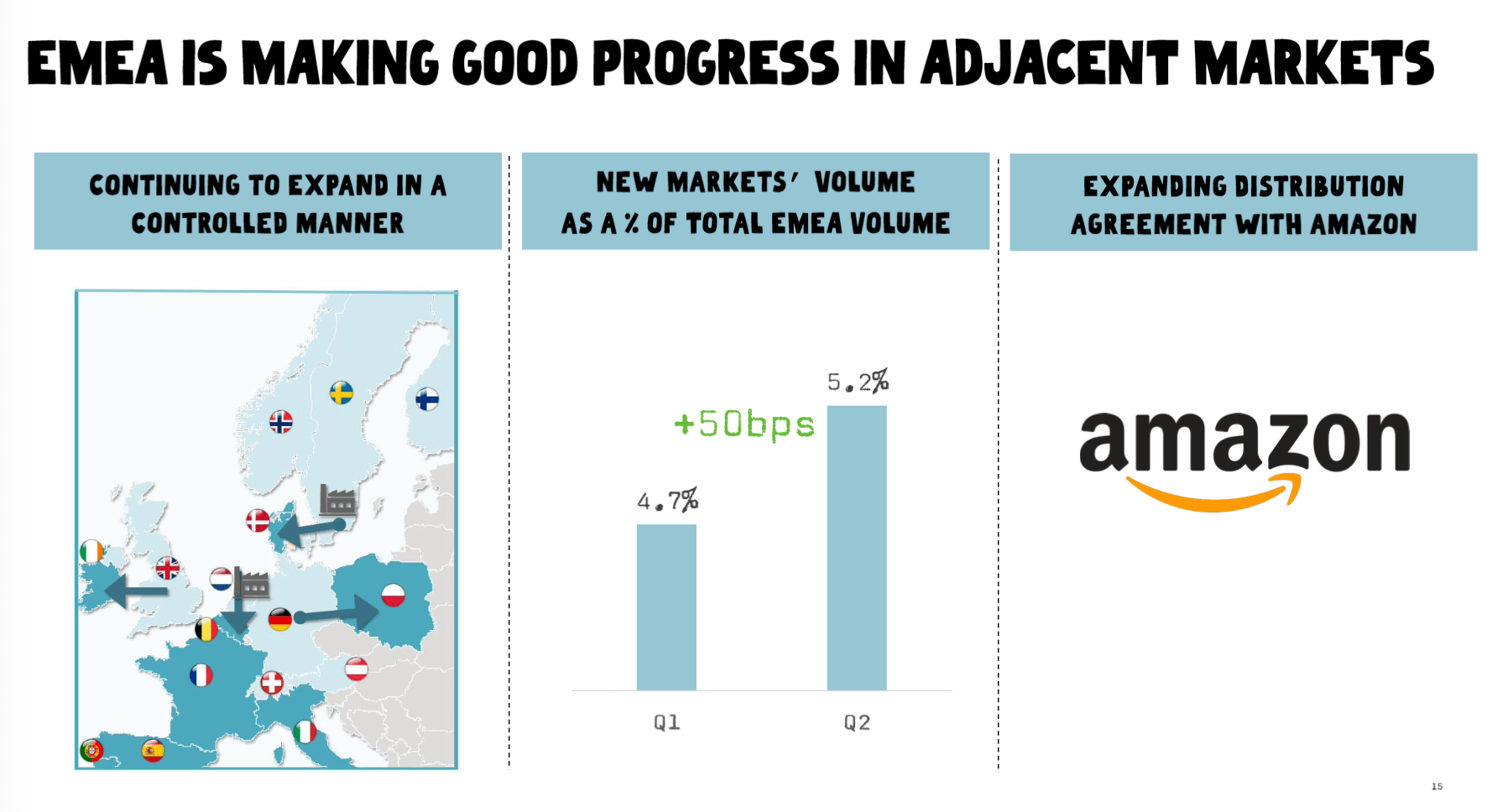

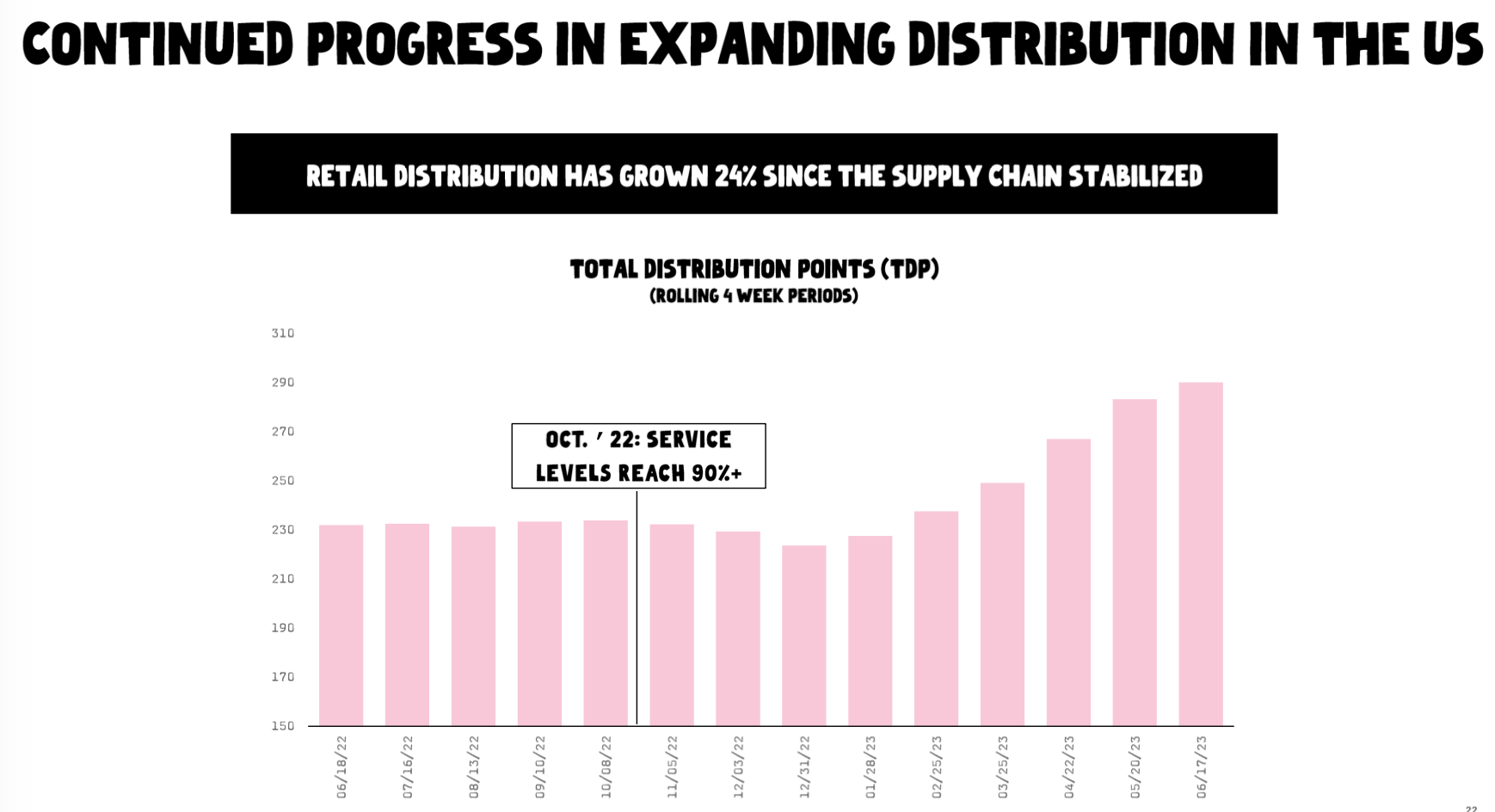

The company's expansion in distribution channel further strengthens the case as there are more retailers that are confident about their products and are willing to show support when the company's stock seems to point to a distressed situation.

{kind=link}

{kind=link}

Valuation

Our DCF model suggested a $1 target price.

Applying the DCF method, we can arrive at an equity value of $593 million ($1 per share), which implies a 56% decline from the current stock price.

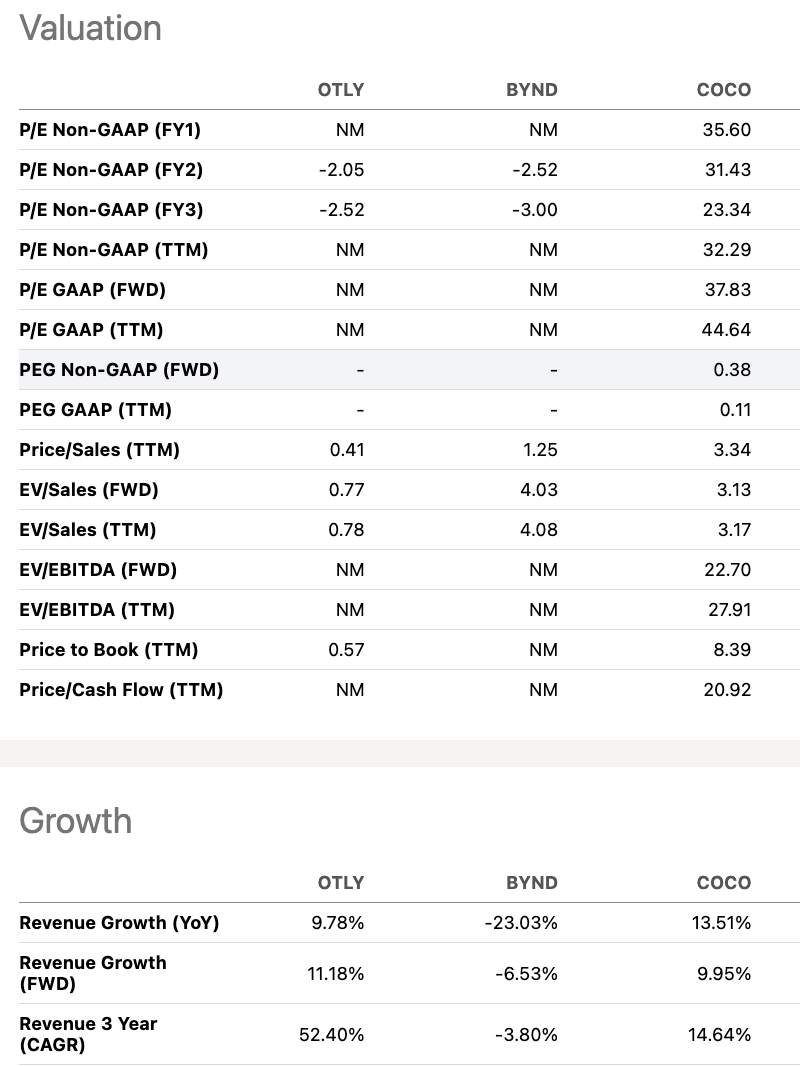

From valuation multiples, the stock is trading at a distress level compared to its similar size peers given its P/S at 0.41x.

{kind=link}

As we discussed above, we think the current market rationale for pricing this stock is driven by cash burn. However, we see their product strength is still intact and their cost-cutting strategy is aligned with creating shareholder value long term.

The worst-case scenario is that the company needs to have another round of equity offering which will dilute shareholder value short term. However, as the company can continue to grow its product, we are not particularly worried about its long-term potential. In fact, its brand strength demonstrated by its pricing power and food retail presence makes us believe that it is a good long-term bet considering all the risk and reward potential.

Conclusion

We value this stock's risk-reward from a long-term perspective and this stock may not be fit for everyone. Please consider your risk and reward profile before investing in this stock. We cannot predict when the management will stop cash burn however we see the brand's strength in EMEA and Americas are intact. Also, from both DCF and multiple analyses, the stock is at an attractive level. Hence, despite there being potential downside risks ahead in the next couple of quarters, we are willing to take the bet with management as we believe the company can be successful long term. We initiate our rating with Buy.

For further details see:

Oatly's Cash Burn Crisis: Is This The Ultimate Buy-Low Opportunity? (Rating Upgrade)