OBE - Obsidian Energy Aims To Quadruple Its Heavy Oil Production By 2026

2023-09-24 09:15:43 ET

Summary

- Obsidian Energy plans to grow its production to 50,000 BOEPD in 2026, fueled by Peace River heavy oil development.

- Obsidian aims to increase its Peace River production from around 6,000 BOEPD now to 24,000 BOEPD in 2026.

- Obsidian also intends to nearly eliminate its net debt by the end of 2026 at US$75 oil.

- It has been getting strong results from its Peace River Bluesky wells and is primarily focusing on developing that formation.

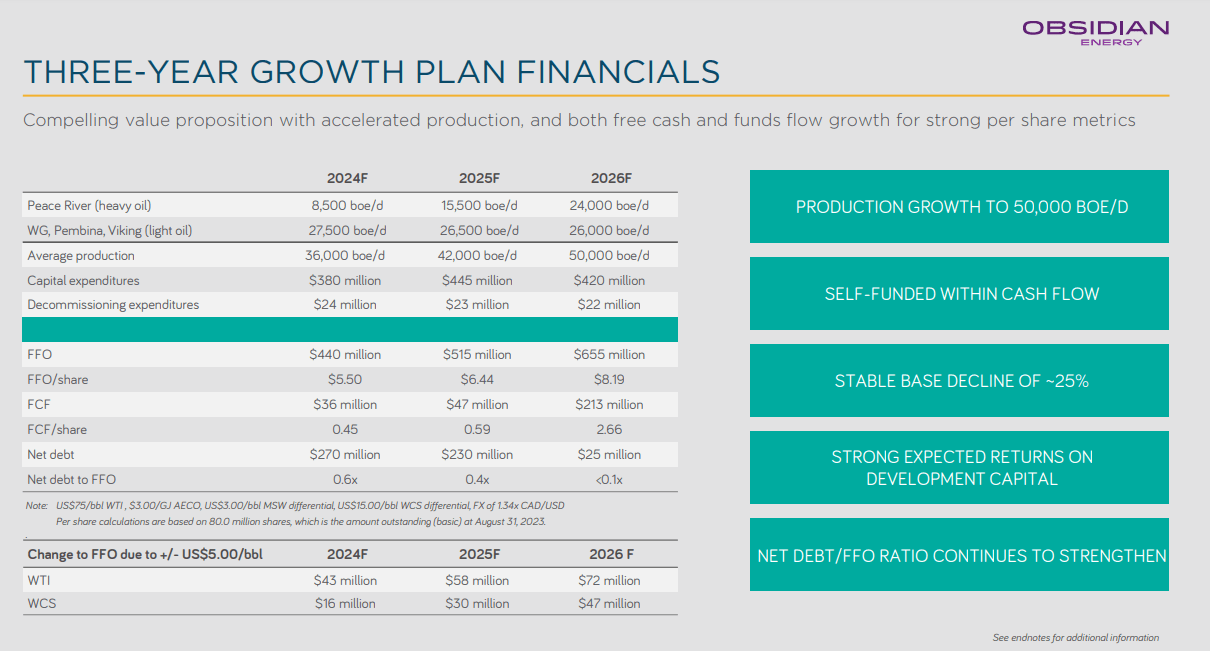

Obsidian Energy ( OBE ) unveiled an ambitious three year plan that aims to grow its production to 50,000 BOEPD in 2026 (about 56% above 2023 levels), fueled by Peace River heavy oil development. Along with that production growth, Obsidian is aiming to nearly eliminate its net debt by the end of 2026 at US$75 WTI oil (along with a US$15 WCS differential).

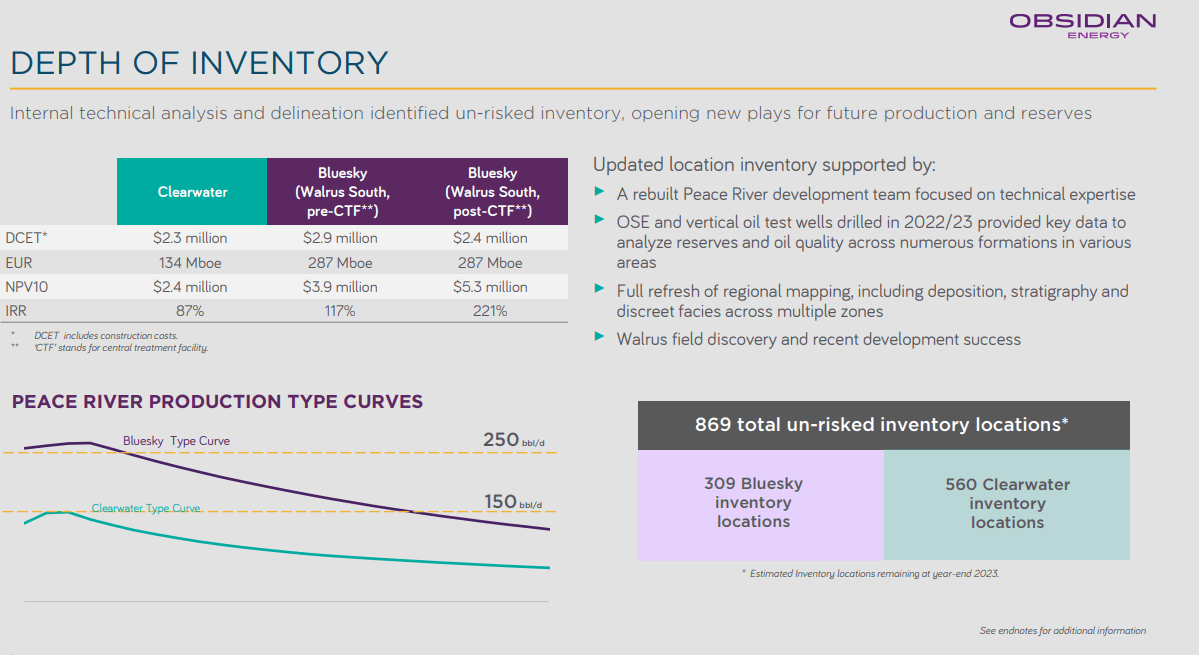

Obsidian has continued to generate strong results from its Peace River Bluesky development, and that formation will be the main focus of its development efforts over the next few years.

It is aiming to roughly quadruple Peace River production from Q2 2023 levels by 2026. There are significant operational risks with that rapid production growth target, but if it can pull that off according to plan, Obsidian would be worth more than double its current price in a long-term US$75 oil scenario.

I am taking a more conservative approach to Obsidian's estimated value for now, and believe that it is worth around US$9 to US$10 per share at long-term (after 2024) $75 WTI oil. This allows for more of a safety margin around operational risk. This estimated value is also a bit higher than when I looked at Obsidian in early August , due to improved near-term oil prices and factoring in part of Obsidian's heavy oil development potential.

This report uses US dollars unless otherwise mentioned, with an exchange rate of US$1.00 to CAD$1.34.

Peace River Focus

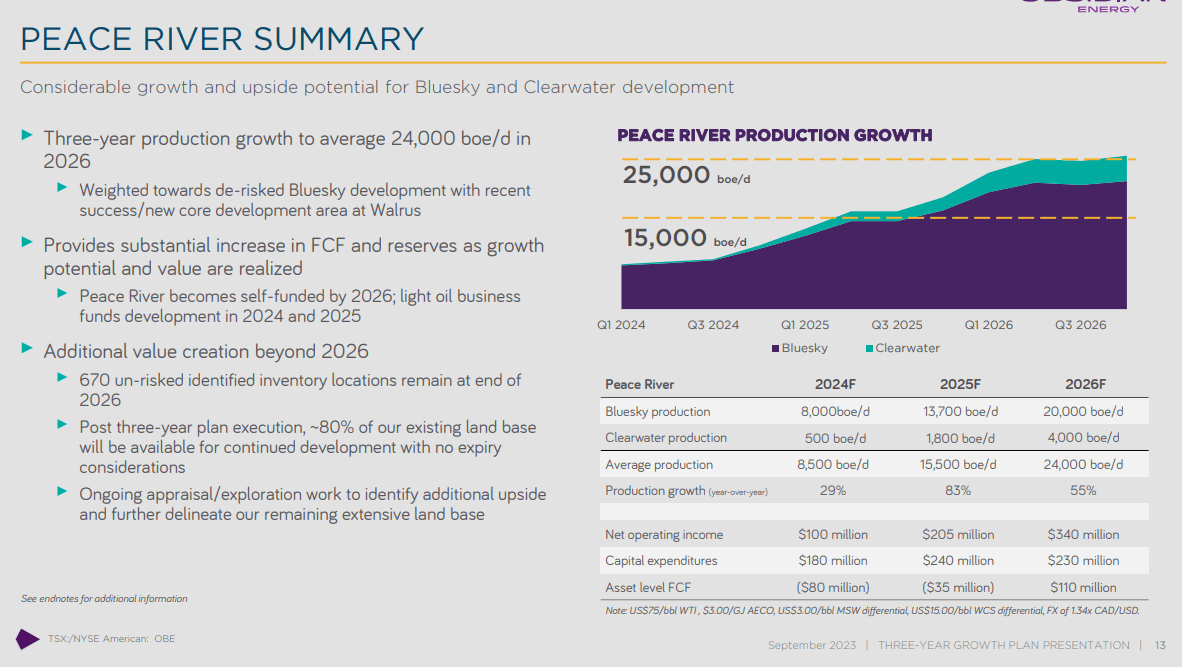

Obsidian is planning on focusing on developing its Peace River assets to grow production to 50,000 BOEPD in 2026. Close to 20% of Obsidian's production currently comes from its Peace River assets. Obsidian is aiming for its Peace River assets to account for approximately 48% of its total production by 2026, with Peace River production roughly quadrupling compared to Q2 2023. Obsidian's light oil assets are expected to have roughly flat production growth over this period.

{kind=link}

Obsidian is aiming to achieve that Peace River production growth with CAD$650 million (US$485 million) in capex between 2024 and 2026, leading to nearly breakeven projected asset-level free cash flow over that combined period.

Obsidian is mainly developing the Bluesky formation within its Peace River asset, which it believes offers better returns than its Clearwater wells. Around 40% of Obsidian's Bluesky inventory will be drilled between 2024 and 2026, compared to approximately 13% of its Clearwater inventory. Bluesky is expected to account for 83% of Obsidian's Peace River production and 40% of Obsidian's total production in 2026.

{kind=link}

This focus on growing heavy oil production makes sense with the Trans Mountain pipeline expansion expected to be completed soon, with a targeted in-service date around the beginning of 2024 (although there still is work to be done to hit that target). Takeaway capacity is a major issue affecting heavy oil economics, and if the WCS differential averages around US$15 (Obsidian's expectations), Obsidian's heavy oil wells should provide quick paybacks at US$75 WTI oil.

At US$75 WTI oil and a US$15 WCS differential, Obsidian may realize around US$47 per barrel for its heavy oil. WCS differentials have gone up to around US$25 to US$30 in the recent past though, and a US$30 WCS differential would slash Obsidian's realized price for heavy oil by over 30% at US$75 WTI oil. Thus the takeaway situation will need to continue to be monitored, although the Trans Mountain pipeline expansion is very helpful for providing additional takeaway capacity.

Potential Overall Results

At US$75 WTI oil and a US$15 WCS differential, Obsidian is projecting net debt of only CAD$25 million (US$19 million) at the end of 2026, while also substantially growing production. This does not factor in any dividend payments (if Obsidian chooses to declare dividends in the future) or additional spending on share repurchases.

{kind=link}

Obsidian's projections are fairly backloaded, with 72% of its projected 2024 to 2026 free cash flow being generated in 2026. It is aiming for CAD$213 million (USD$159 million) in free cash flow in 2026, which would be close to US$2 per share in free cash flow.

Notes On Valuation

If Obsidian can meet its projections over the next few years, I estimate that it would be worth around US$17 to US$18 per share in 2026. This would be based on a 3.0x enterprise value to 2026 FFO multiple and nearly zero net debt. This also assumes that its share count is in the low-80 millions at that time.

There are significant operational risks with trying to grow Peace River production that quickly, so while Obsidian could be worth more than double its current share price in a few years, I can't give full value to its growth plans currently.

I now estimate Obsidian's value at US$9 to US$10 per share in a long-term (after 2024) US$75 WTI oil environment. This is up roughly US$1 from my previous estimate of Obsidian's value. The boost is partly due to increased near-term oil prices (with 2H 2023 and 2024 strip in the low-to-mid $80s). As well, I believe Obsidian has put close to 30 Bluesky wells into production during the past few years, so it has a reasonable sample size to use for making projections.

Conclusion

Obsidian Energy is planning to grow its heavy oil production significantly over the next few years. It is targeting 24,000 BOEPD in Peace River production (mostly from the Bluesky formation) in 2026, up from around 6,000 BOEPD currently.

If things go according to Obsidian's plan, I estimate that it could be worth US$17 to US$18 per share in 2026 at US$75 WTI oil. However, given the significant operational risk involved with growing Peace River production that quickly, I am more comfortable with currently valuing Obsidian at US$9 to US$10 per share in a long-term (after 2024) US$75 WTI oil scenario.

For further details see:

Obsidian Energy Aims To Quadruple Its Heavy Oil Production By 2026