OCDGF - Ocado: An Underappreciated Online Grocery Tech Pioneer

2023-07-31 11:40:52 ET

Summary

- Ocado is uniquely positioned to export its battle-tested technology leveraging a combination of online grocery, high-end warehouse automation and logistics solutions.

- Ocado's technology applicability to related industries like pharmacies can unlock new sources of revenue for the Group.

- OCDDY / OCDGF historically served as an effective diversifying asset, exhibiting a low-to-negative correlation with major market indices such as the S&P 500 and FTSE 100.

- The Technology Solutions segment revenue growth and improving profitability are the most important figures for investors to scrutinize, in the medium to long-term.

- Ocado's idiosyncratic risks include overextending to international markets and overspending on technology investments.

Editor's note: Seeking Alpha is proud to welcome Andreas Eliades as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Ocado Group plc ( OTCPK:OCDGF , OTCPK:OCDDY ) is a UK-based pioneer operating at the intersection of online grocery, warehouse automation and logistics with no direct competition. The stock has experienced a sharp decline of 85% from its peak in 2021, resulting in attractive valuations as demonstrated by my stock valuation. Also, I will show why I believe Ocado to be one of the most promising UK tech companies in the public markets with considerable potential upside actuated by two main factors:

First, revenue growth, driven by exporting its industry-leading end-to-end eCommerce, fulfilment and logistics platform to leading international retailers including Kroger ( KR ) and improving profitability as economies of scale play out.

Second, multiple expansion, driven by a change in investor sentiment due to increasing demand by international retailers, the horizontal expansion to adjacent businesses, and improving online retail penetration predominantly in developed markets.

Furthermore, I will demonstrate how Ocado stock from a Portfolio Management point-of-view is a diversifying, low-correlation asset.

Identifying The Opportunity

Revenue breakdown

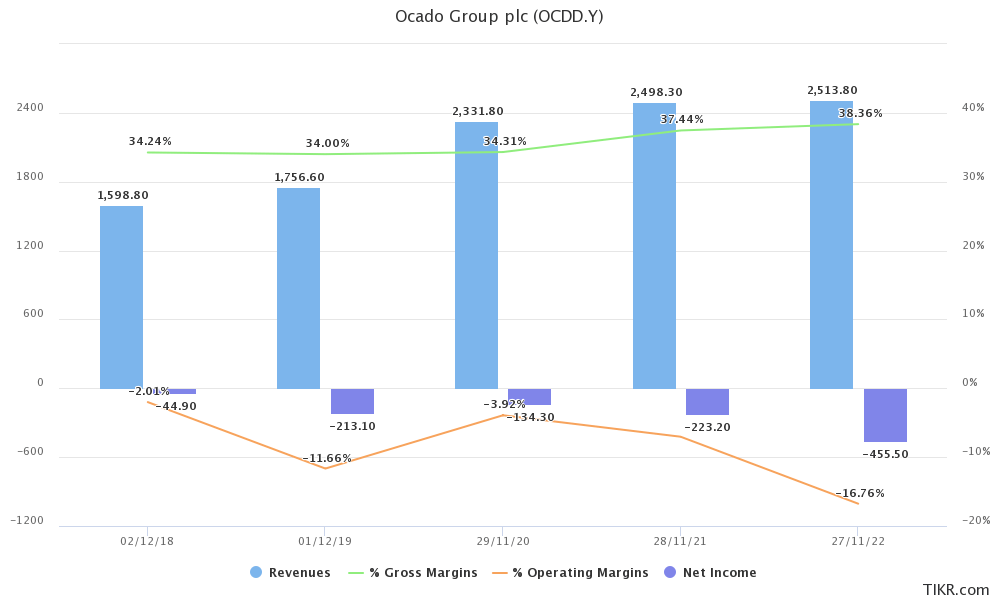

In the last 5 years, FY Ocado sales had a CAGR of 9.47%. Although this does not seem impressive for an "industry pioneer" that I claim this company to be, the overall revenue figure can be deceiving.

Ocado Group Plc Income Statement plot (TIKR.com)

{kind=link}

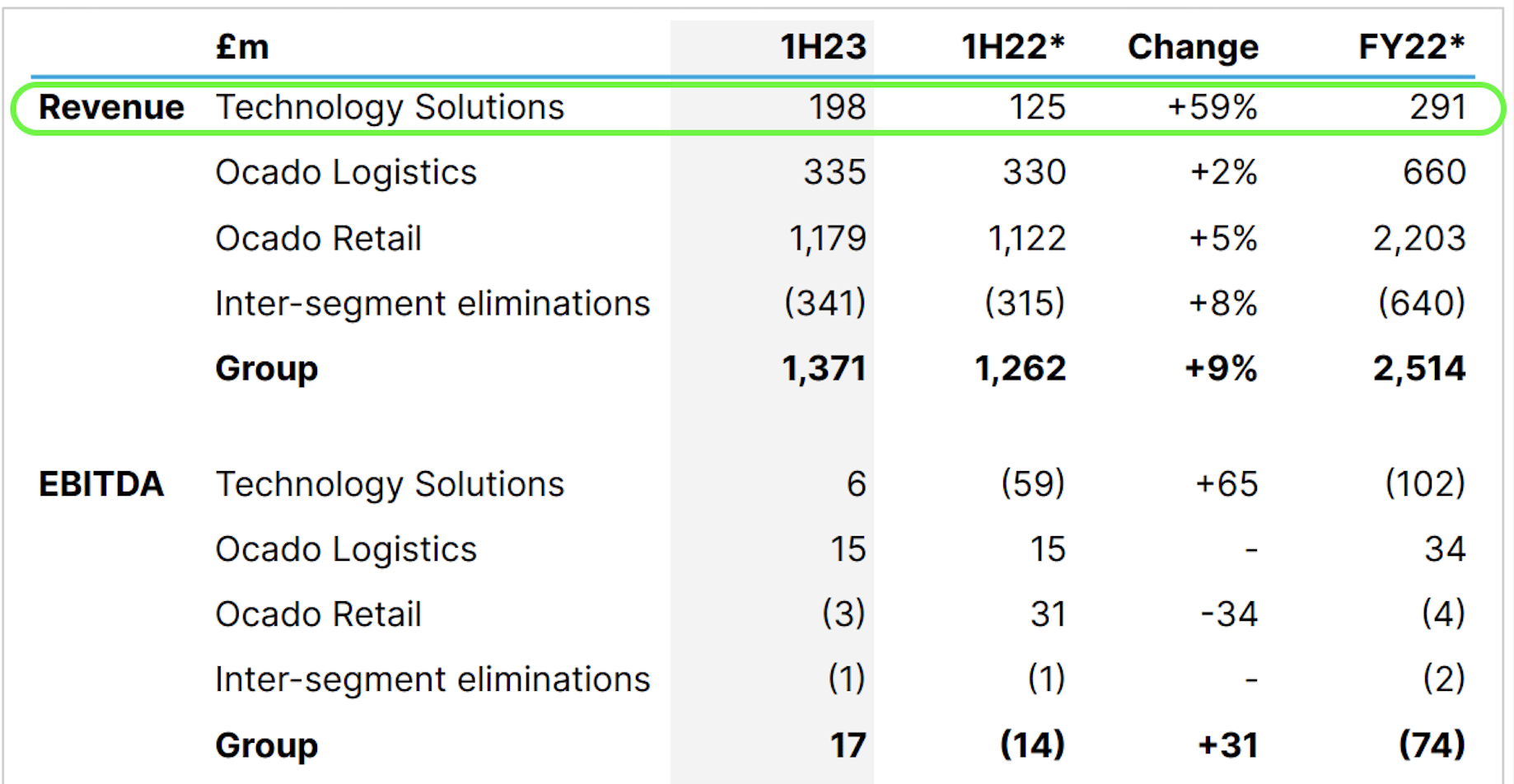

Currently, most of the group's revenues come from Ocado Retail (61%, 1H23), a 50-50 partnership with Marks and Spencer Group ( OTCQX:MAKSF , OTCQX:MAKSY ) and 24% from the UK Logistics business. As stated in 1H23 Results , only 14% of Revenue comes from the Technology Solutions business which includes mostly fees collected from international retail partners.

Ocado Group Plc's Income Statement by Segment (Ocado Group Plc)

{kind=link}

Note: The percentages above were calculated by subtracting the 'Inter-segment eliminations' expense from the 'Retail' part of the business.

This business segment currently shows high top-line YoY growth of 59% and a notable swing in EBITDA to positive territory.

It is worth noting that Ocado Technology Solutions Revenues are particularly sticky. By sticky, I mean that as existing and new partners sign contracts, build and operate Ocado-partnered sites, it is more unlikely and costly to seek alternatives, thus providing Ocado with a very stable stream of recurring revenue.

In 1H23, recurring fees amounted to £175 million ($225 million), up 61% from 1H22, collected from operational partners (inc. Ocado Retail).

Technology Solutions

Technology Solutions is driven by Customer Fulfillment Centres (CFCs) built for partners internationally powered by Online Smart Platform ((OSP)), Ocado's proprietary end-to-end eCommerce, fulfilment and logistics platform. While older CFCs were non-OSP, recent and newly-built OSP-powered CFCs are improving efficiencies and costs for partners and yield bigger fees to Ocado.

The Group's management heavily invests in Technology Solutions, as demonstrated by the capital investment breakdown. In FY22 , only £134m of capital investments were allocated to expand the Ocado Retail business (which contributes 62% of Revenue), while £663m (representing 83% of invested capital) was invested in the Technology Solutions business, currently generating just 12% of the Group's Revenue.

Global demand

The first two International Partner CFCs went live in 2020. By the end of 2022, a total of 10 CFCs were operating globally for international partners. FY2022 saw a total of 12 new CFCs going live, up from just 4 in FY2021.

Table 1: Total and international sites (CFCs & Zoom sites) built and operated with domestic and international partners

| Period |

| Total Sites Live (UK & Int.) |

| Total Sites added during the period |

| International Sites Added during FY |

| FY20 |

| 7 |

| 2 |

| 1x Groupe Casino (France), 1x Sobeys (Canada) |

| FY21 |

| 11 |

| 4 |

| 2x Kroger ((USA)), 1x ICA (Sweden) |

| FY22 |

| 23 |

| 12 |

| 6x Kroger, 1x Sobeys, 1x ICA |

| 1H23 |

| 25 |

| 2 |

| 1x AEON (Japan), 1x Sobeys |

| FY23 (exp.) |

| (29 exp.) |

| (6 exp.) |

| (2x Coles (Australia)) + 2x 1H23 CFCs |

In the first half of 2023, the premiere Customer Fulfillment Center ((CFC)) of AEON, Japan's top retailer as reported by Statista , was launched. This was accompanied by the third Sobeys CFC in Canada. Looking forward to the rest of the Fiscal Year 2023, it is anticipated that Coles will inaugurate its first two CFCs in Australia, accompanied by a new domestic CFC in the UK.

Ocado Group Plc's International Partner Map (Ocado Group Plc)

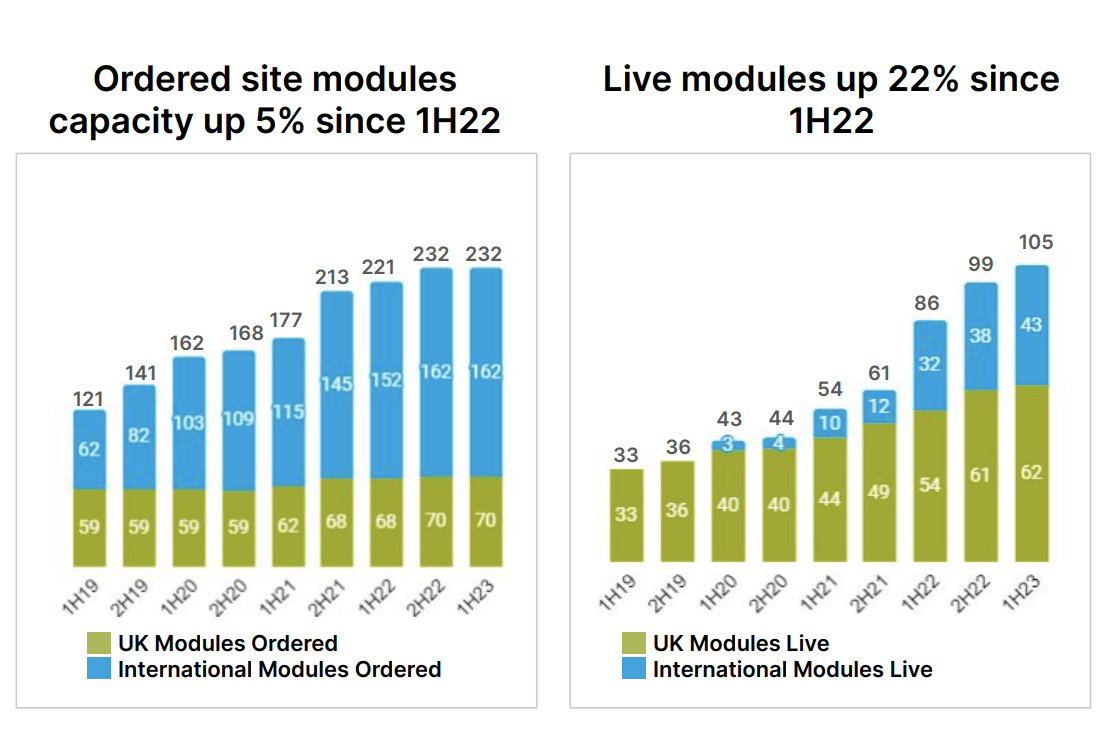

With 12 international partners across 10 countries, Ocado has committed to building and operating 232 modules in the coming years.

Ocado Group Plc's Ordered Site Modules and Live Modules (Ocado Group Plc, 1H23)

{kind=link}

Levelling-up the underlying tech: R&D spending and acquisitions

High spending on Research and Development (R&D), along with acquisitions, are common strategies for companies seeking to improve and expand their offerings, facilitating both organic and inorganic growth.

R&D for FY22 came at £308 million ($396 million), 70% of which goes to improve the Group's and partners' efficiencies and costs. Ocado aims to lower R&D costs in the midterm to around £200 million ($257 million). In 2023, Technology Investment peaked at £149 million ($192 million), up 19.2% YoY and the FY23 CapEx for the group is expected to reach £550 million ($707 million).

Ocado Group Plc recently acquired Shopify's Autonomous Mobile Robot fulfilment solutions provider 6 River Systems (2023), the vertical farming Jones Food Company (2019), the robotics-AI company Kindred and the robotic-arms company Haddington Dynamics (2020), and the material handling startup Myrmex Inc. (2022) . The group also invested in Wayve and Oxbotica to provide a strategic advantage in autonomous vehicle innovation.

Stock Valuation

Valuation approach

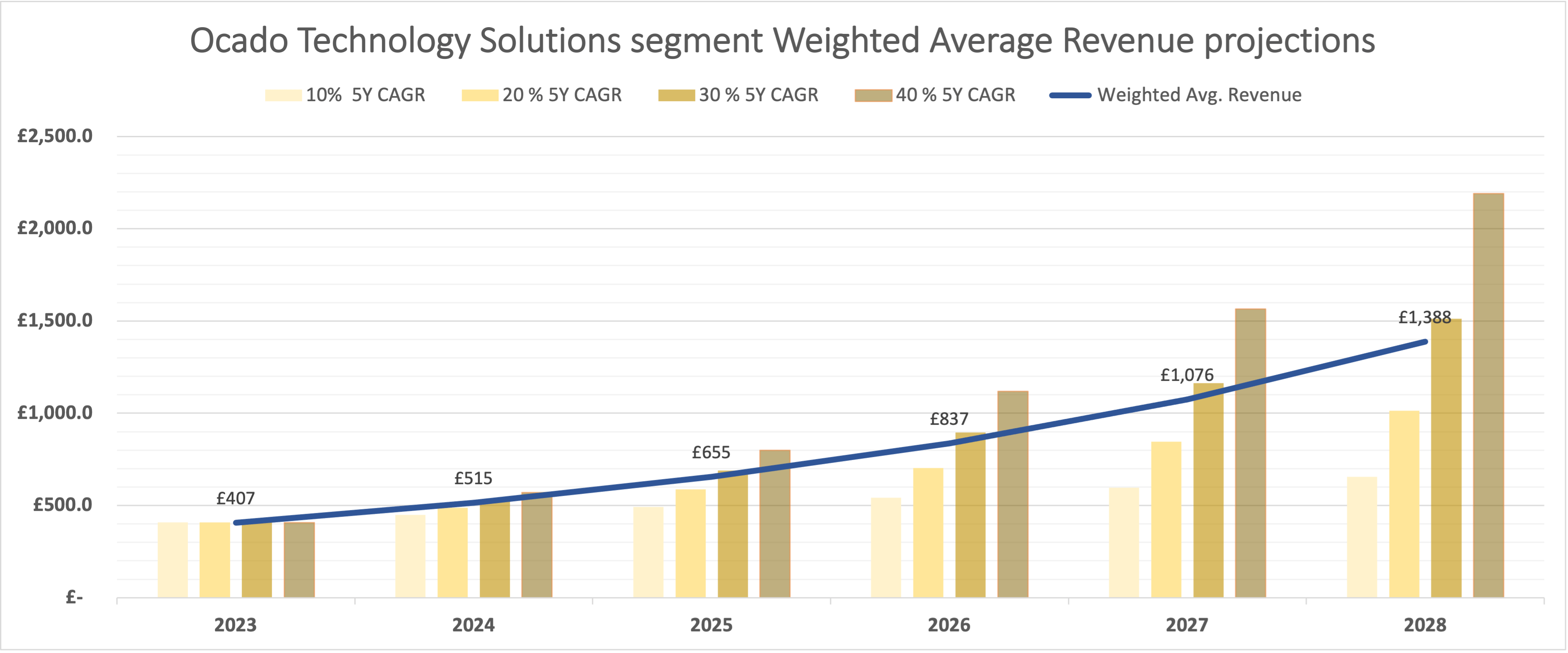

For this valuation, a 5-year window was used, given that projections beyond this period can introduce significant uncertainties. The focus of the assessment is the Technology Solutions segment, with a conservative 2% Compound Annual Growth Rate ((CAGR)) applied to the other components - Ocado Retail, Ocado Logistics, and Inter-segment eliminations. The current market value is then derived using a Price-to-Sales (P/S) multiple, based on the estimated revenue figures. Recognizing the volatile nature of the high-growth Technology Solutions division, I used a weighted average method, incorporating assigned probabilities to generate a credible and plausible sales estimate.

Valuation figures

According to my calculations, the Technology Solutions segment should generate around £1,400 ($1,799) by 2028. This estimate was arrived at using a discrete probability distribution of 0.1/0.35/0.35/0.2 for the respective 5-year CAGRs of 10%/20%/30%/40%. The blue line in the graph below represents the weighted average revenue derived from these calculations.

{kind=link}

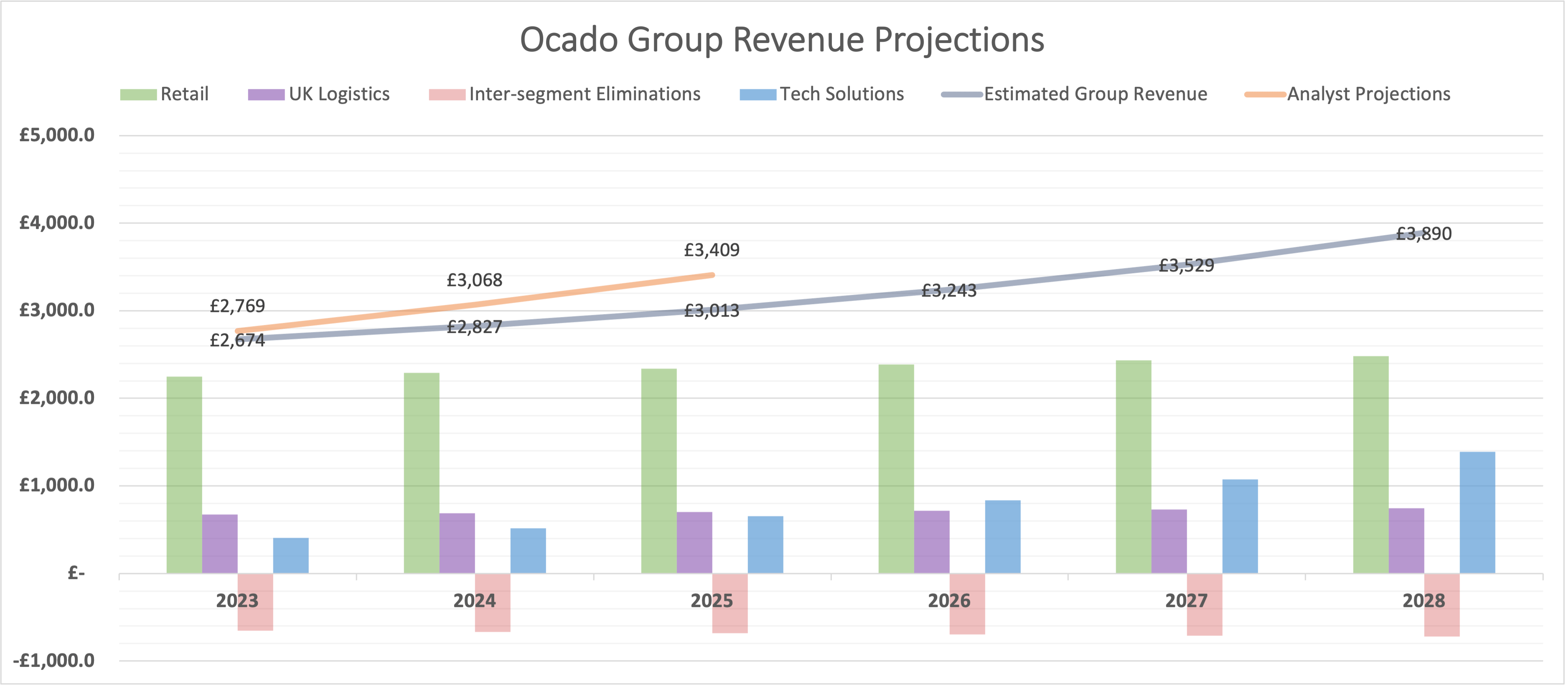

By including each segment's revenue projections, based on the aforementioned assumptions (2% 5Y CAGR for Retail, UK Logistics, and Inter-segment Eliminations), I projected a 2028 Group Revenue of approximately £3.9 billion ($5.0 billion). Note that my estimates appear conservative when contrasted with the more optimistic analyst forecasts, represented by the orange line on the corresponding figure below.

{kind=link}

To derive the present market valuation, I used a weighted average P/S multiple. Specifically, a discrete probability distribution of 0.10/0.30/0.25/0.25/0.10 was applied, corresponding to P/S multiples of 1x/2x/3x/4x/5x over the next five years.

This choice of probability distribution reflects the company's high R&D and CapEx commitments, which generally pay off over the medium to long term and reflects my 'multiple expansion' view mentioned in the introduction. This suggests that economies of scale, combined with accumulated experience and expansion into recently accessed markets (e.g., Japan, Sweden, and Canada) will catalyze revenue growth and enhance profitability over time.

By applying a 5% discount rate for the 5-year period, I calculated the current market value of Ocado Group Plc to be £9,077 million ($11,663 million).

Consequently, this equates to a fair share price of $14.3 (£11.13) for Ocado Group Plc in 2023.

Ocado's Competition and Risks

The competition

Assessing Ocado's competition is quite challenging. I was unable to find a company directly comparable to Ocado, i.e. a company providing end-to-end eCommerce, fulfilment and logistics solutions while operating an online-only grocery business itself.

Due to this, I will compare the company to two differentiated types of businesses: established brick-and-mortar retailers and warehouse automation (hardware & software) companies servicing the online grocery/retail back-end.

Established brick-and-mortar retail competition

Although all big retailers in the UK operate an online grocery business (e.g. Sainsbury Plc ( OTCQX:JSNSF , JSAIY) , Tesco PLC ( OTCPK:TSCDF , OTCPK:TSCDY ), etc.) most do so in a more manual, low-cost and unscalable manner without particular focus on the underlying technology. Tesco, for example, fulfils their online orders from local stores where Tesco employees pick and pack each order manually which is then delivered via delivery vans. As Ocado claims, manual order fulfilment uses ~5x the labour required by Ocado's automated solution.

Warehouse automation competition

The Norwegian-listed robotic and software tech company, Autostore, sells automated warehouse solutions (does not operate an online grocery business), and is trading at a mid double digit Price-to-Sales multiple. Autostore recently lost a high court patent infringement claim to Ocado, paying $257 million of fees to Ocado. The company brings in double Ocado's Technology Solutions revenue, $585 billion in FY22, and is considerably profitable and cash-flow positive (16% profit margin 1Q23, TTM). On the other hand, Autostore is focused on servicing the eCommerce backend and does not operate an online grocery business, offering end-to-end solutions like Ocado.

Alert Innovation , which was acquired by Walmart in 2022, offers an e-grocery micro-fulfilment centre and the Alphabot platform (similar to Ocado's Hive), amongst other solutions. In my opinion, Alert Innovation seems to be behind Ocado's sophistication, technology and experience, evidenced by the single Walmart site operating the technology since 2019. Due to Walmart's WMT capital and experience in the retail sector, Alert Innovation, and consequently Walmart, can turn out to be a formidable competitor in the medium to long term.

Dematic is the world's largest warehouse automation provider as of 2021. They offer a full range of warehouse automation solutions and subsystems including grocery fulfilment solutions.

Potential risks

The company has significant challenges to tackle before taking over the online grocery market. Although companies are required to disclose a number of potential risks to the business, my research draws my attention to the following:

One notable concern is the apparent slowdown in expansion efforts. According to the 2022 10k report, the number of sites scheduled to go live in 2023 for both international and domestic partners has been halved compared to the previous fiscal year. This decline from 12 sites in FY22 to just 6 expected in FY23 could hinder the company's growth prospects. Expecting >20% growth in the technology solutions segment for the medium term, lack of growth in ordered modules/sites and no. of CFCs built will be a significant concern and reason to abolish my bullish investment thesis.

Another troubling aspect is the continuous negative free cash flow coupled with rising research and development (R&D) costs and capital expenditures (CapEx). This was evident during the first half of 2023, as stated in the presentation on pg. 18. Due to the capital-intensive nature of the business, failing to achieve economies of scale can prove catastrophic for the company.

Furthermore, in June 2022, the company raised a substantial amount of funds, including £575 million in equity after a significant decline in stock value, indicating a desperate need for capital to fund its growth.

The competitive landscape poses a formidable threat as well, with retail giants like Walmart actively acquiring competing companies and investing heavily in their growth. This influx of financial resources and human capital could potentially challenge the company's market position and growth trajectory. Although this is not an issue short to medium term, I would keep an eye on rising competitors, especially those funded by cash-rich companies.

Moreover, the company must contend with the uncertainties brought about by the UK's macroeconomic troubles. High inflation and increasing costs may impact the company's profitability, while difficulties in attracting talent and human capital could hinder operational efficiency. Additionally, there is a need for comprehensive foreign exchange ((FX)) management strategies to navigate currency fluctuations effectively.

Lastly, the risk of overextension is a crucial concern. The company's expansion into multiple regions without proper focus and execution, particularly without establishing a solid presence in specific markets with select partners first, may lead to inefficiencies and strain its resources. Significant problems in this area will take the form of a lack of continuing investment from global partners.

Portfolio Management: Correlation

Finding promising uncorrelated return streams is the epitome of investing and PM. The following correlation table demonstrates the 3, 5 and 10-year correlation of Ocado's Close Price to the 3 major indices.

Note: Data fetched and calculated using Python's pandas and yfinance. The correlation figures refer to the daily Pearson correlation.

| Ocado Group Plc |

| S&P 500 (^GSPC ) |

| NASDAQ (^IXIC) |

| FTSE 100 (^FTSE) |

| 1-year Correlation |

| 0.28 |

| 0.15 |

| 0.16 |

| 3-year Correlation |

| -0.18 |

| 0.37 |

| -0.76 |

| 5-year Correlation |

| 0.10 |

| 0.35 |

| -0.60 |

| 10-year Correlation |

| 0.62 |

| 0.71 |

| -0.13 |

Conclusion

Before delving into the final remarks, it's essential to disclose and remind readers that I currently hold a minor stake in Ocado Group Plc within my portfolio. As such, there's an inherent potential for confirmation bias and conflicts of interest. While the goal of this research publication is not to convince anyone to invest in the security discussed, I strive to share my findings and hypotheses transparently, seeking peer scrutiny, critique, and improvement of these ideas.

Here are the crucial takeaways from this analysis:

First, Ocado has a unique position in the market with no direct competitor at the intersection of high-tech automation, online grocery and logistics with the potential to expand horizontally in markets requiring similar solutions (e.g. pharmacies).

Second, the company's most substantial risk lies within the market in which it operates and its ability to organically fund its growth. Although not idiosyncratic, political and macroeconomic uncertainties in the UK may obstruct ambitious tech companies like Ocado.

Third, from a portfolio management perspective, Ocado stock exhibits low to occasionally negative correlation with major indices, including the S&P 500 and FTSE 100, which implies it could serve as an effective diversifying asset in many portfolios. US and foreign investors worried about USD devaluation could benefit further.

Finally, the compass for investors should be Technology Solutions' revenue growth and meaningful moves towards profitability. I would expect YoY growth rates in the 20-40% range for the next 1-2 years. Considerable slowdowns without obvious reasons and lack of execution and expansion in terms of ordered and built international modules/CFCs will be major red flags.

In conclusion, Ocado represents a unique opportunity at the intersection of online retail and technology. Given its unique market position and technological advantage, its potential for future growth is compelling. However, investors should carefully consider the potential risks related to the company's operational market and ability to generate cash to fund its growth. Reaching economies of scale is crucial in the eCommerce business. I suggest using Technology Solutions' revenue growth as guidance for those who choose to invest.

For further details see:

Ocado: An Underappreciated Online Grocery Tech Pioneer