OCDDY - Ocado Group: Delays In Tech Play Initiate At Neutral

2023-10-13 09:08:17 ET

Summary

- Ocado Group is an online supermarket that has seen growth during the pandemic but faces competition from discounters and inflationary headwinds.

- Despite challenges, Ocado has been able to grow its customer base and reported improving signs in its retail business in Q3.

- It faces commissioning delays and overcapacity on its technology solutions business and believe the current value provides limited margin of safety. Initiate at Neutral.

Investment Thesis

Ocado Group (OCDGF) has transformed itself into a leading technology solutions provider to retail from just being an online retail player focused on their own deliveries. It derives a majority of its value from the technology solutions business which has been challenged with delays in commissioning and overcapacity leading to the company shedding half of its market value in the last 3 months, despite that, the stock is up 55% over the past year. We initiate at Neutral and ascribe a target price of US$13.0 using an SOTP method.

Company Overview

Ocado Group is an online supermarket player providing home deliveries of groceries and other products to its 960,000+ active customers through a 50:50 JV with Marks and Spencer (MAKSY), Ocado Retail. It has transformed itself into a leading technology and software service provider through its Technology solutions business providing end-to-end solutions of online retailing to various retailers such as Kroger, Sobeys, Lotte, Morrisons as well as its own JV, Ocado Retail.

Struggling Retail Business with Some Positives

Ocado has witnessed an outsize growth during pandemic, with shoppers turning to the online platform to get their share of deliveries from milk to clothing and shampoos. However, with the reopening and significant inflationary headwinds, shoppers started to flock to discounters such as Aldi and Lidl. In addition, the retailer was forced to cut prices to remain competitive with the latest round cutting price on 500 essential items from onions to rice, marking the fourth campaign to reduce prices since July. It had also started a price match program with Tesco (TSCDY) in which customers would get a credit in their next order for any difference in amount with Tesco's prices. However, it has been able to continue growing its customer base through continued customer acquisition and retention efforts, which has led to a sustained growth in its mature customers (customers who have shopped for more than 5 times).

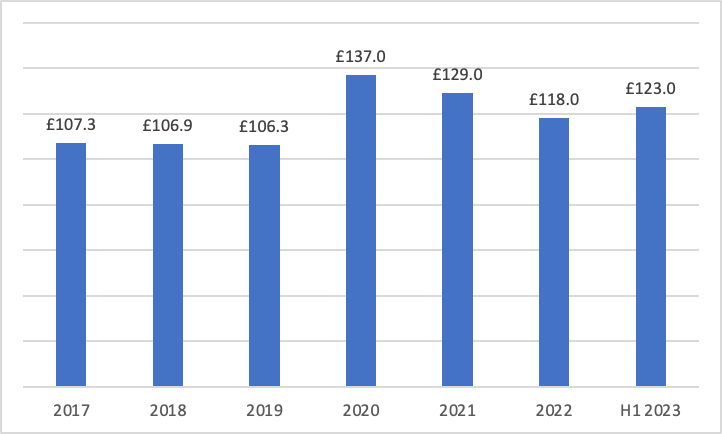

Growing Active Customer Base ('000)

{kind=link}

Its basket signs have shown some stability post the big spike during COVID times and has also moved further higher recently, albeit, primarily driven by price inflation.

{kind=link}

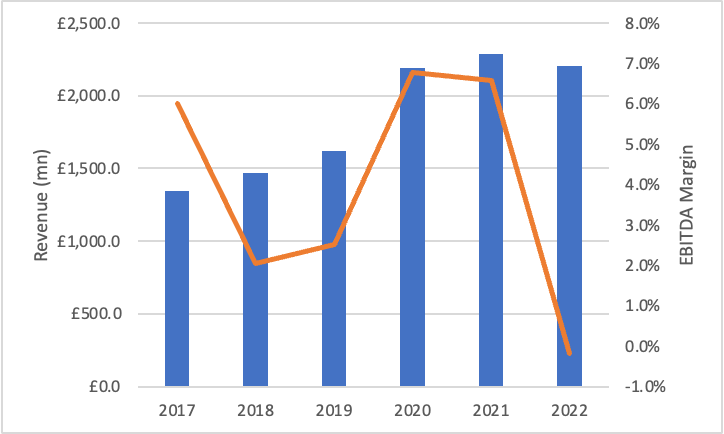

However, its operating profits have declined as a result of shrinking gross margins as the retailer continues to invest in value along with negative inflation on its distribution and fulfillment costs which continues to spike, which led them to report operating losses in FY22.

{kind=link}

Marks and Spencer Chair had publicly denounced that they were not happy with Ocado Retail facing with overcapacity and a reset is underway with turnaround plan including improving the customer experience and product availability and cost-cutting measures.

However, in its latest trading statement for Q3, Ocado reported improving signs in its retail business driven with revenues growing 7% YoY in Q3 with the company exiting Q3 with a positive volume growth. This remains a positive surprise as the street and the management anticipated a volume growth at the back end of Q4. Active customers jumped ~2% YoY to 961k with mature customers up about 7% driven by strong customer retention and offering. Average basket value increased 4% YoY driven by an 8% jump in ASP as a result of higher inflation, while average orders remained flattish at 44 (vs 45 last year). It reiterated its guidance for mid single-digit revenue growth implying a slight deceleration in Q4 with positive EBITDA implying a healthy improvement compared to last year.

Technology Segment Stumbling

Ocado provides technology solutions to wide range of retail partners enabling them to drive an efficient online retail operations, operating through two sub segments: UK and International. UK Logistics focuses on providing technology service to its own Ocado Retail as well as to Morrisons while International partners globally with the likes of Kroger, Aeon and Lotto. UK Logistics have been fairly mature right now while the international segment continues to ramp up. While the capacity utilization ramped up during the pandemic, it suffered from overcapacity with reduced utilization since then. It operates 7 CFCs in UK with a total of 25 sites open with 2 new sites opened in H1 23. It expects to open another CFC in Luton but plans to close down the Hartfield CFC due to underutilization.

Company

In addition, the CFCs for Coles have hit roadblocks and has been delayed further which had been expected to be live by H2 2023 due to additional works to rectify construction issues with the grid identified during the quality control process for the Victorian site. Coles mentioned that the site's incremental ramp up has been delayed and is now expected in mid-2025, one year later than planned.

Valuation

We value Ocado using an SOTP method for its retail and technology solutions business. We value retail business at ~12x EV/Fwd EBITDA at the top end of the quartile given its growth prospects. We assume H2 2023 EBITDA of £11 mn in line with the consensus expectations and further expect H1 2024 EBITDA margin to ramp up to about 3-4% EBITDA margin driven by positive volume growth and stable basket value which translates to H1 2024 EBITDA of £40 mn and NTM EBITDA of £51 mn. We value the retail business at ~£600 mn (US$725 mn) at 12x EV/NTM Fwd EBITDA.

{kind=link}

In addition, we value Ocado technology solutions business (split into UK Logistics and Technology Solutions) using the DCF method. We assume a WACC of 11% with an ERP of 7% and target Debt/Capital of 20%. We assume stable capacity increases over the projected period with EBITDA margins of around 4% on a conservative basis for the mature portfolio. Assuming a PGR of 2.5%, this translates to a present value of ~£340 mn (US$415 mn) for the UK Logistics business.

{kind=link}

We assume an overall capacity OPW of 65,000 for 1 CFC and average order value of £120 inflating to 3% every year. Assuming the ramp up happening in year 3 with 5.5% capacity revenues, we estimate about £300 mn in annual revenue from year 3.

{kind=link}

Assuming a ramp up in EBITDA margins to the mature levels of 70% by year 10 with year 3 margins of around 60%, we estimate the present value per CFC of ~£100. Basis the existing orders, we value the present value of the technology solutions at £4.5 bn (US$5.4 bn) including the potential planned capex required. This translates to a total EV of US$6.5 bn with a potential upside of new sign-ups. However, given the lack of certainty amidst the current environment as well as potential delays in the existing orders including some hold-ups such as in Kroger, we do not assume any additional CFC within our model. We believe the current valuation fairly reflects the risk reward as the shares are up 50% for the year despite the recent stumble in past few months. We initiate at Neutral.

Risks to Rating

1) Continued competitive pressure within its retail business may lead to declining operating margins as a result of price cuts and higher promotional activities

2) Consumers may opt for discount grocers such as Aldi and Lidl which can lead to decline in transaction volume

3) Technology business can suffer from further delays such as in case of Coles which can lead to delay in revenue ramp up

4) Upside risks include addition of new partners or its ability to improve utilization can provide a significant boost to its technology solutions business

Conclusion

Ocado has been on volatile journey this year, with shares up over 50% in last 52 weeks, despite shedding half of its market value in last 3 months as a result of delays in ramping up its technology business. We believe the current levels provides limited margin of safety and we remain on the fence closely tracking its development of its planned CFCs. In addition, management has not provided any guidance for any new potential sign-ups and can be difficult to penetrate particularly within the growing developing economies. We initiate at Neutral.

For further details see:

Ocado Group: Delays In Tech Play, Initiate At Neutral