DELHY - Ocado Group: Q4 Disappointment Paves The Way For More Downside

Summary

- Ocado Group plc missed the mark again in Q4.

- Decelerating growth poses downside risks to the FY23 guidance and beyond.

- The premium valuation could come under pressure alongside more downward revisions.

On the back of another disappointing trading update in Q4, pure-play online grocery retailer Ocado Group plc (OCDGF) could fall short of its medium-term targets. In particular, management's prior guidance for a ramp-up of customer fulfillment center (CFCs) openings for its partners (vs. steady growth prior) contrasts with data indicating capacity is running well ahead of demand.

The increasingly price-sensitive UK consumer environment isn't likely to abate anytime soon, paving the way for downward revisions for Ocado Retail. And with customer acquisition costs also moving higher alongside the inflationary pressures, the risk of a dilution event is elevated - note that any additional debt or equity financing would likely be at unfavorable terms given the higher rate backdrop. While the stock has de-rated in recent months, the current ~2.4x EV/Revenue valuation still isn't cheap, and I see more risk than reward here.

Q4 Misses the Mark as Growth Decelerates

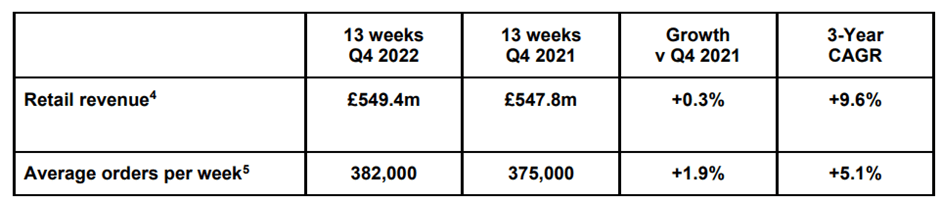

Ocado's recently released retail Q4 trading update (ahead of the full-year results announcement later this month) was a poor one all around. Retail sales were up a sluggish 0.3% YoY at GBP549m, decelerating from the +2.7% YoY growth in Q3, while average basket size declined 1.3% to GBP117. The good news was the +7.6% rise in average prices, though this was offset by an 8.3% decline in the number of units per basket. Per management, Ocado's inflation at +9.4% was well below the rest of the industry (~14% for the major UK supermarkets per management based on a December report by Which? ), but whether this goodwill will translate into improved future sales remains an open question.

{kind=link}

In the meantime, management has kept the FY22 outlook unchanged at close to breakeven EBITDA despite cost headwinds from surplus CFC capacity, as well as elevated marketing and OpEx costs. All in all, this was a weak trading statement for Ocado retail, and though the stock price decline post-release has embedded some of the disappointment, the revenue slowdown and limited operating leverage benefit could still lead to margin downside for FY22.

Downside Risk to the FY23 Guidance Update

Based on the Q4 weakness, the FY23 update looks a tad ambitious - sales are projected to grow by mid-single digits %, and EBITDA is guided to be marginally positive for the full year despite being loss-making in H1 2023. The top-line guidance was likely helped by a strong Christmas trading period, with sales up ~15% in the five days to Christmas. But whether the seasonal strength can sustain into Q1 remains to be seen. Also, the heavily back-end weighted profitability guide is a concern - from a loss-making H1, management expects H2 2023 to turn positive based on improving volumes and higher capacity utilization throughout the year, translating into a lower % of costs relative to sales. Even assuming Ocado hits its FY23 guide, the path to achieving the mid-term GBP3.9bn sales target and regaining mid to high-single-digit EBITDA margins looks challenging for Ocado Retail.

Bulls will contend that a large portion of the current margin pressure is transitory, and as volumes return, operating leverage should kick in alongside capacity utilization. This might be true to an extent, particularly with energy inflation already easing. But customer sentiment shows little sign of reversing from historic lows, and the prospect of labor/services inflation persisting for another year or two will weigh on margins. Elevated marketing costs are another risk given the competitiveness of the UK grocery market - like the rest of the industry, management is rolling out initiatives offering better prices and promotions for customers, entailing more gross margin pressure in FY23. With pressure from all sides of the P&L, the near-term setup isn't compelling.

Mid-Term Targets May Require Additional Financing

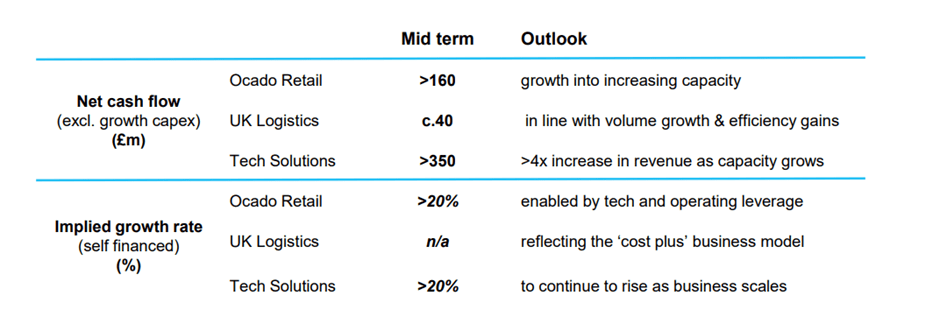

Ocado management raised investor hopes at its last cash flow seminar in November 2022, highlighting a mid-term sales target for the Ocado Retail JV at GBP3.9bn and a >GBP270m EBITDA target (implying a 7% margin vs. 6% prior) from Re: Imagined (a series of innovations to the Ocado Smart Platform). Not only do these targets imply solid growth relative to the FY22 revenue base, but the guidance for margin expansion before the company has even turned EBITDA positive seems ambitious.

{kind=link}

More broadly, Ocado's tech platform, while unique, has yet to prove its structural profitability - thus far, the greater-than-expected costs have led to a history of downward earnings revisions, and it's hard to see this changing anytime soon. The key difference this time around is that access to new capital is more costly, and funding the projected >20% growth rate for both Technology Solutions and the UK JV may necessitate significant equity dilution down the line.

Q4 Disappointment Paves the Way for More Downside

While Ocado Group plc stock suffered a significant drawdown over the last year alongside downward revisions to its earnings, the fwd EV/Sales valuation remains toppish at 2-3x. In contrast, European food delivery players like Delivery Hero ( DLVHF ) and Just Eat ( TKAYF ) trade over one turn lower, reflecting elevated investment needs and more negative profitability/cash flow in the next years.

One reason for the divergence is the lingering optimism embedded in Ocado's consensus estimates - revenue is still projected to grow through a pending 2023/2024 recession, driving an EBITDA positive outcome in a year.

While Ocado Group plc deserves some credit for the tech behind its unique online grocery platform, the Q4 update indicates the P&L challenges are far from over. Execution will be key - the premium valuation implies the market is still underwriting some chance of Ocado Group plc hitting its medium-term targets, so any disappointments here could drive downside. The next potential catalyst for Ocado Group plc will be the FY22 results on 28 Feb, where management will likely provide more color on the near-term guidance.

For further details see:

Ocado Group: Q4 Disappointment Paves The Way For More Downside