OCDDY - Ocado: Solid Results But Valuation Is Still Demanding

2023-07-26 02:04:39 ET

Summary

- Ocado's recent results show solid performance with revenue and EBITDA in line with expectations, and future CFC deployments holding potential for growth.

- The resolution of a patent dispute with AutoStore is positive news, providing Ocado with a £200 million cash infusion over two years.

- Despite upside suggested by my 15-year DCF model, the recommendation for Ocado remains a hold due to potential risks, including CFC accidents, deployment delays, and sensitivity to interest rates.

Overview

My recommendation for Ocado ( OTCPK:OCDGF ) is a hold rating, as I am not comfortable with the growth assumptions that the market is embedding into valuation today. A large part of OCDGF's value lies in future deployments of CFC, of which we have little visibility, despite them being in the pipeline. Even though I am positive about the industry, I think the share price will only start to react strongly each time OCDGF moves one step closer to deploying the next CFC. Note that I previously gave a neutral rating for OCDGF due to concerns with the longevity of each CFC and the impact on valuation, and the same concern remains.

Recent results & updates

Group revenue for Ocado came in at £1.4bn, which is in line with expectations. Group EBITDA of £17m exceeded expectations, thanks to efficient management of expenses. The company's reiteration of FY23 guidance on all fronts is particularly encouraging, and it gives me cause for optimism regarding FY23 consensus estimates (something that will support share price sentiment in the near-term).

There are a couple of key takeaways from this set of results. To begin, it's important to highlight Ocado Retail's positive EBITDA throughout the entire second quarter thanks to better-than-anticipated cost efficiency. Second, underlying demand is robust as retail activity is up 11% and the basket size has remained relatively constant at around 45 items since October 2022.

Two more CFCs will go live in 1H23, bringing the total to 25 sites and 105 live modules by the end of the period, which is in line with projections for future growth capacity increase. Management also emphasized that partners like Kroger are experiencing observable gains in operational performance. In particular, UPH rates (units picked per labor hour) have increased by 25% at Kroger's warehouses. This is a very compelling piece of evidence, in my opinion, as it demonstrates the potential return on investment Kroger could realize from a company-wide rollout.

In my opinion, these factors are net positives and will help sustain the share price's recent strong rally from below GBP340 to its current level of around GBP785.

Agreement with AutoStore

In other news, Ocado and AutoStore recently issued a joint statement confirming the final resolution of their global patent dispute and the withdrawal of all pending patent litigation claims. Both businesses are free to keep using and selling their existing products without interference from the other, and all pending patent litigation claims are dropped around the world. The most crucial takeaway is that AutoStore must fork over £200 million to Ocado over a two-year period. In my opinion, this is good news for Ocado, not only because a major overhang on the stock has been lifted but also because the company will receive a cash infusion of £200 million that it can use to reinvest or pay off upcoming debt or converts.

Valuation and risk

{kind=link}

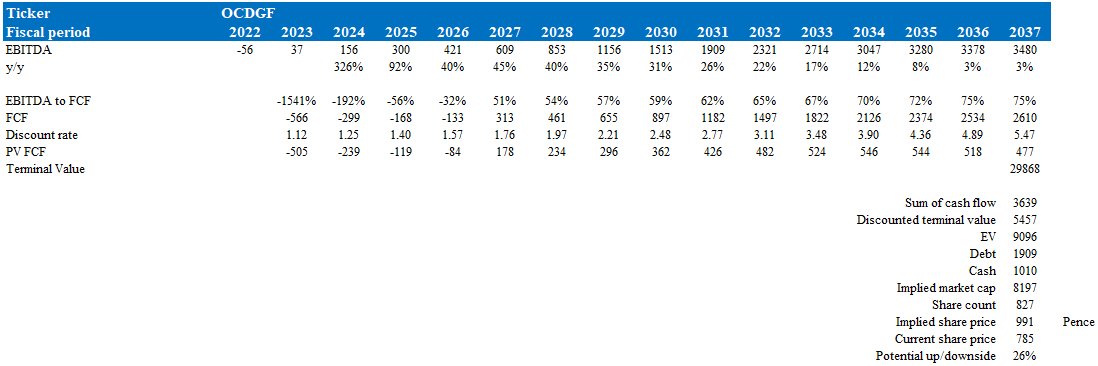

According to my model, OCDGF is valued 991pence today after discounting back to its present value, representing a 26% increase. This target price is based on my 15-year DCF model, which comprises consensus estimates for the first 5 years as I attempt to incorporate what the market thinks of OCDGF financials in the near-term, followed by a gradual deceleration of growth to 3% in the terminal year.

I believe DCF is the best way to value OCDGF given the nature of its business, where each CFC has a predictable lifespan and cash flow. I expect a 3% growth in the terminal year, as I believe the online grocery delivery industry will eventually match the retail industry. At maturity, OCDGF should also gain sufficient scale to pull back on R&D ((CAPEX)), thereby increasing EBITDA to FCF conversion. Finally, I attached a 12% discount rate as a large chunk of value is still in the future when CFCs come online.

With these assumptions, the upside is only at 26%, I would note that this model assumes EBITDA to increase ~100x from FY23E levels to GBP3.5 billion in 15 years. To give more perspective, this assumes OCDGF EBITDA grows to half the size of today’s Kroger. Given that Kroger is the key driver for OCDGF CFC deployment, I wonder if OCDGF is able to capture such a large share from Kroger.

The major risk for OCDGF is another repeat of CFC accidents and fires and the delay of CFC deployments. Given the sensitivity of OCDGF expected cash flow to interest, since all of them are far out into the future, any change in FCF trajectory will have a huge impact on valuation today.

Summary

My recommendation for OCDGF stock remains a hold despite the recent results and updates showing solid performance, as I believe the current valuation is demanding. The company's revenue and EBITDA are in line with expectations, and future CFC deployments hold potential for growth. However, the share price is likely to react more strongly as each new CFC deployment approaches. The agreement with AutoStore is positive news, resolving a patent dispute and providing a cash infusion. My 15-year DCF model suggests a 26% upside, but this assumes significant EBITDA growth, which may be challenging to achieve. Risks include CFC accidents, deployment delays, and sensitivity to interest rates. Considering these factors, I suggest monitoring OCDGF's progress closely before making an investment.

For further details see:

Ocado: Solid Results, But Valuation Is Still Demanding