ECCC - OCCI: 26% Yield But OXLC Might Actually Be Better

2023-07-12 13:08:44 ET

Summary

- OCCI was a hard pass about a year back.

- The "yield" was a mouth-watering 20%, but the numbers that mattered more were eye watering.

- The yield is now up to 26%. "Surely you cannot go wrong here?"

- You can and don't call me Shirley.

On our last coverage of OFS Credit Company Inc. ( OCCI ) we focused on why you won't make anywhere close to the sticker yield of 20%. The fund did better than we expected. No really, it did. The price drop was over 20% but the yield-chasers managed to climb back almost to breakeven. Whew!

Seeking Alpha

What is the outlook for this fund now?

The Fund

OCCI is a non-diversified, CEF investment company. It aims to generate current income, with a secondary objective of generating capital appreciation via investment in collateralized loan obligation ("CLO") equity and debt securities. Anyone who has followed the multitude of CEFs, knows that one out of every 100 succeeds in getting that "capital appreciation". Nine out of 100 manage to keep the NAV flat. 90 out of 100 do a slow motion train wreck on the NAV. OCCI fits into the third category.

While the fund has not been around for that long, it has managed to create a rather nice 45 degree down slope on its net asset value from inception. There was a brief cascade down during COVID-19, but following that recovery, we went back to our regularly scheduled programming. One other point here for those that have already hit the "buy now" button (26% yield??? Take my money!), is that you really don't get your yield in cash.

Reflects annualized distribution rate based on the most recent $0.55 per share distribution declared on the shares of common stock by the Board on June 1, 2023. The distribution will be paid in cash or shares of our common stock at the election of stockholders. The total amount of cash distributed to all stockholders will be limited to 20% of each total distribution, excluding any cash paid for fractional shares. The remainder of each distribution (approximately 80%) will be paid in the form of shares of our common stock. The exact distribution of cash and stock to any given stockholder will be dependent upon his/her/its election as well as elections of other stockholders, subject to the pro-rata limitation.

Source: OCCI

Holdings

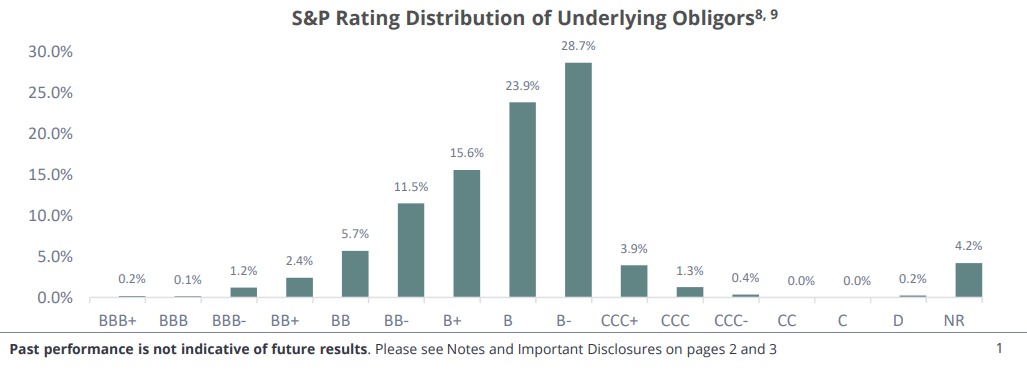

CLO funds can focus on debt or equity and the latter is generally far more risky than the former. On last check OCCI was 84.3% within the equity segment.

OCCI

Of course the equity-debt distinction is meaningless without delving into where the credit rating on these stand. We are glad you asked. OCCI's CLO equities are deep into the B category on average with some CCCs showing up as well.

{kind=link}

OCCI

These of course pay a lot. They also carry as much risk as you can get going into a potential recession.

Returns

We showed you that you made less than nothing over the last 12 months. That holds true even since the inception of the fund. Ok, technically you did make something, but unless your goal was to beat Double-O-7, aka James Bond, you should not be proud of this.

Y-Charts

Outlook

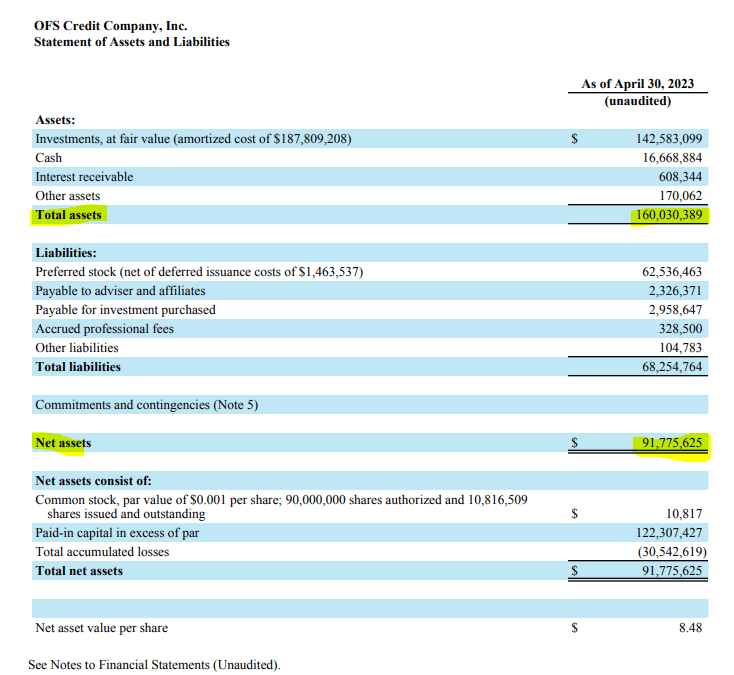

If you needed two reasons to stay away from this fund, you should have got them from the material above. The riskiest tranches of CLO equity in a fund that has not managed even Treasury bill beating returns since inception. But unfortunately there is more than that and we can give you two more reasons to run for the hills. The first one is that we have packaged the riskiest most levered debt structures for this CEF, and added leverage on top of that. Total assets are 75% higher than net assets.

{kind=link}

OCCI

We know, we know. Pretty much everyone has become numb to funds running this level of leverage and consequences have been few and far between. But we think this is important before rolling the dice to capture the 26% yield.

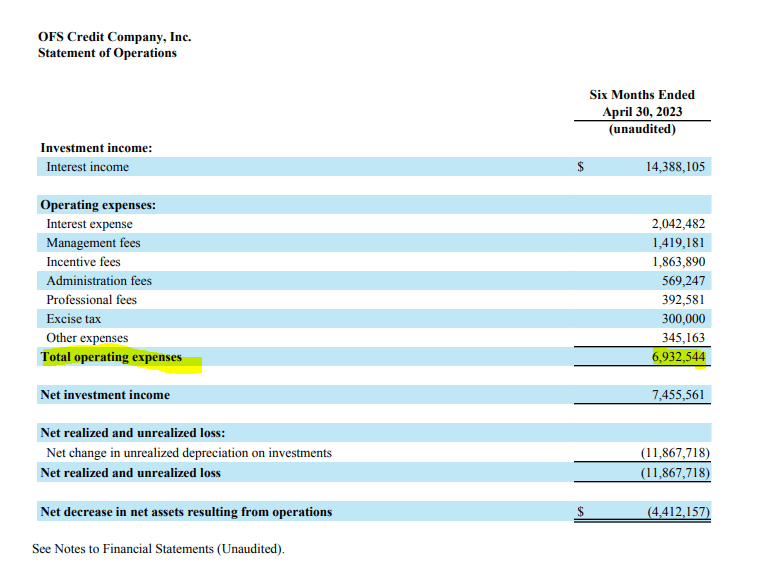

The other problem is the expense ratio. The latest semi-annual report showed that the fund's expenses are almost $7 million for the six months ended April 30, 2023.

{kind=link}

OCCI

The $14 million in annual expenses works out to an expense ratio of about 15%. That is a tall hurdle to climb. This is of course not uncommon in the realm of CLO funds. Oxford Lane Capital Corporation ( OXLC ), Eagle Point Credit Company Inc. ( ECC ) and Eagle Point Income Company Inc. ( EIC ) sport rather high expense ratios. One might argue that this is par for the course. We agree, but we can throw in a fun fact that none of those three have beaten Treasury bills either in the recent past.

Getting back to OCCI, an optimist might focus on the net investment income which works out to almost $15 million ($7.5 million for six months) or 16.4% on NAV. The trouble with that is the history where the fund has had enough losses to wipe that net investment out. We are also starting to see some higher levels of defaults of these types of investments.

Goldman Sachs

So the chances of returns approaching anywhere in the ballpark of even 16% are extremely slim.

Verdict

The fund has done better than what we expected. We really thought we would have a total return of negative 20% at this point and OCCI has managed to cling to the flat line. Of course if you avoided the fund, you have to be happy as you dodged an investment that made you nothing. We think the next 12 months will bear out our thesis and the fund will give that negative 20% return that we have been anticipating. We would stay away and look for better opportunities where you can make an actual positive return. Among the CLO funds, we think all of them will have very poor returns, especially relative to Treasuries yielding 5%. But on a relative basis, we think OXLC should outperform ECC and OCCI .

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

OCCI: 26% Yield, But OXLC Might Actually Be Better