OCCI - OCCI: Distribution Policy Was Not Inherently Negative But New Policy Is Better

2023-12-06 16:31:02 ET

Summary

- OFS Credit Company Inc is a collateralized loan obligation fund that focuses on CLO equity.

- The old stock-based distribution policy was not inherently negative.

- New cash-based distribution policy is better and should restore investor confidence in the fund.

Author's note: This article was originally written before OCCI's recent announcement of its distribution policy change. The new cash-based distribution policy is a positive and should restore investor confidence in OCCI going forward, as indicated in the original summary section below.

OFS Credit Company, Inc. ( OCCI ) is a collateralized loan obligation, or CLO, fund. CLOs pool together a diversified portfolio of loans, typically consisting of corporate loans or leveraged loans, and then issue different tranches of securities backed by these loans. These tranches have varying levels of risk and return: the senior tranches are considered less risky and have priority in receiving interest and principal payments from the underlying loan portfolio. The junior tranches, on the other hand, carry more risk but also offer higher potential returns. CLOs generate income through the interest payments on the loans in the portfolio which are used to pay interest and principal to the investors in the CLO securities.

OCCI, like its peers Eagle Point Credit Company ( ECC ) and Oxford Lane Capital Corp ( OXLC ), focuses on CLO equity, the riskiest but potentially highest-rewarding tranche of the CLO structure. For more information on CLOs, see Guggenheim's Understanding Collateralized Loan Obligations (CLOs) .

The COVID-19 pandemic in 2020 triggered widespread panic in the global financial systems. As businesses were forced to shut down due to restrictions and uncertainties, investors grew increasingly concerned about the ability of companies to honor their loan obligations. This caused CLO prices to plummet, and ECC and OXLC both cut their distributions in order to preserve cash.

YCharts

On the other hand, OCCI took a different approach. Instead of cutting its distribution, it switched from a monthly payment of $0.1734 to an equivalent quarterly distribution of $0.52, but with an important twist: the distribution will be paid in a mixture of stock and cash. The maximum amount of cash paid in each quarterly distribution will be 20% in cash, split pro-rata among shareholders who elected for cash or partial cash payment. Investors who do not submit an election to their brokers will be paid in new stock, by default.

In the most recent quarterly payout , investors who elected to receive cash for their distribution received approximately 32.5% of the payout in cash, with the remaining 67.5% in newly issued stock.

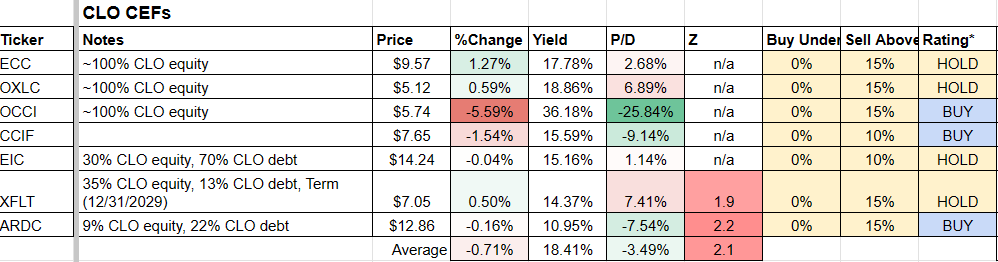

The quarterly distribution has even been increased slightly a few times, and sits now at $0.55/quarter. This represents an extremely high NAV yield of 28.84%, which is boosted to a market yield of 36.18% thanks to OCCI's extremely wide discount of -25.84%, which is by far the highest among the CLO funds. The second-highest yielding CLO fund, OXLC, yields "only" 18.86% by comparison.

From our CEF Watchlist :

{kind=link}

Clearly, there is a significant pessimism among investors regarding the future prospects of OCCI. It is worth pointing out that OCCI had kept pace with ECC and OXLC for most of the last 5 years, including over the COVID crisis, with its performance only diverging recently from ECC and OXLC as its discount widened dramatically.

YCharts

The key question that has to be answered is: what is the effect of the stock-based distribution on OCCI's performance?

1. Stock distribution may be dilutive to NAV/share...

When OCCI is at a discount, the stock-based distribution will be dilutive to NAV/share. For example, in the most recent quarterly distribution , OCCI issued 943,866 shares at $6.98, which was the volume-weighted average price per share of OCCI on October 16, 17 and 18, 2023. With OCCI at a NAV of $7.74 (as of 9/30), the new shares were issued at a -9.82% discount to the NAV. The number of new shares issued in the stock distribution represented 6.30% of the total share count of OCCI prior to the distribution.

As shown in the table below, the act of issuing the stock distribution resulted in about a 5 cent hit to the NAV of OCCI, or a -0.58% decrease in percentage terms. Note that the greater OCCI's discount to NAV, the more dilutive the stock-based distribution would be to the NAV/share.

Income Lab

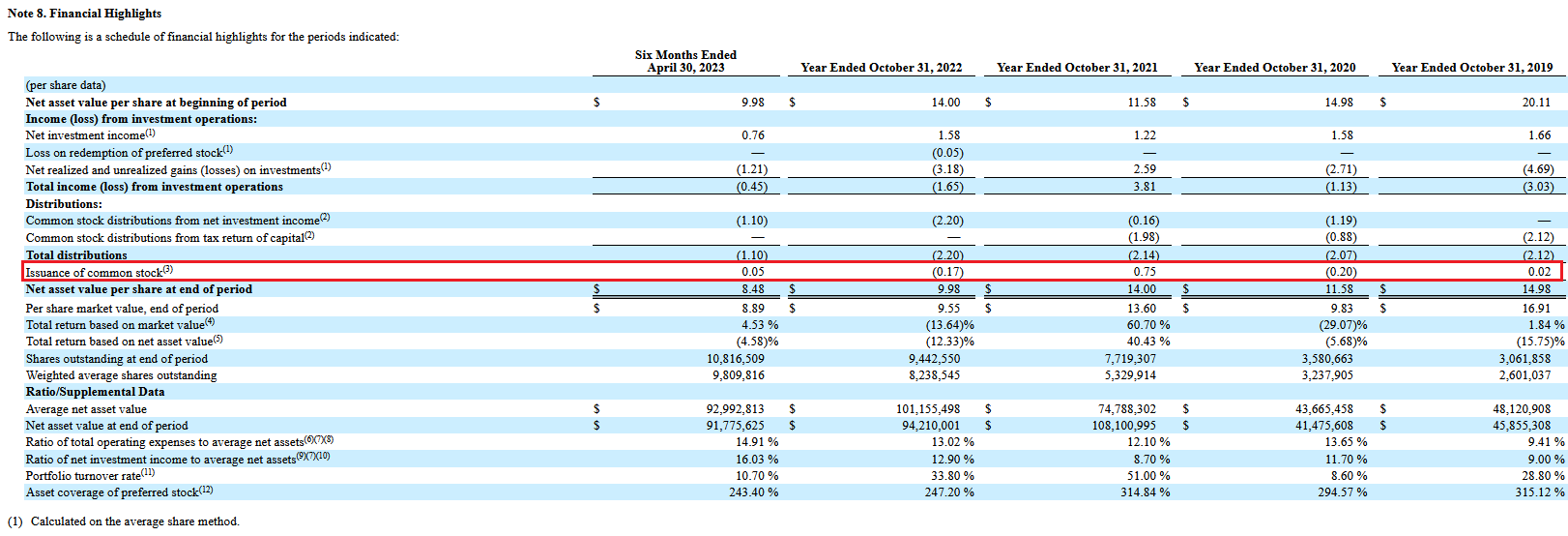

Going back several years, we can see the impact that the stock-based distribution has on the NAV/share by looking at the annual report . In 2022, the total NAV hit was -$0.17 for the entire year, or -1.2% of the starting NAV value. However, in 2021 when OCCI traded at a premium for some part of the year, there was actually a positive $0.75 or +6.5% impact on the NAV/share. In 2020, the impact was negative -$0.20, or -1.3% of the starting NAV in the year.

{kind=link}

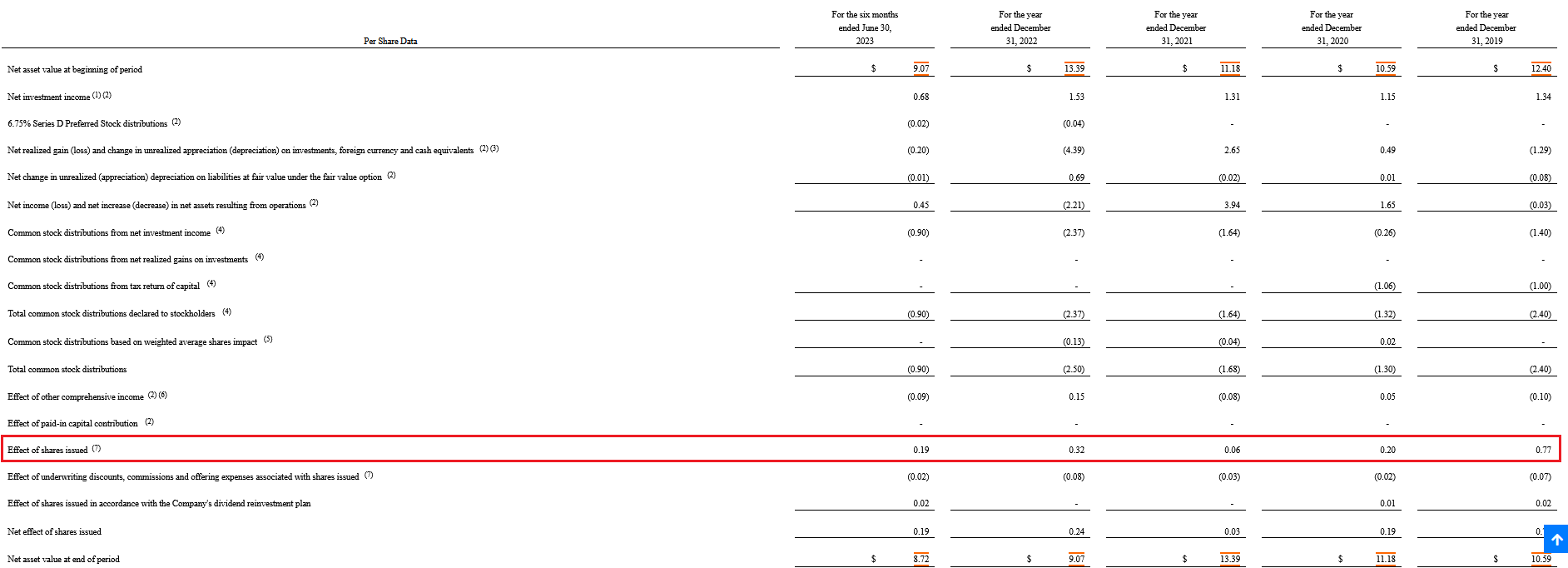

Contrast this to ECC, which has normally traded at a premium. This has allowed its stock issuances to be accretive to NAV for five years running, which is of benefit to all shareholders.

{kind=link}

2. ... but is not a negative per se

It may be assumed that the dilutive stock-based distribution would be a negative for OCCI shareholders, but somewhat paradoxically, that actually isn't the case.

Effectively, a stock-based distribution forces investors to reinvest capital back into OCCI. In other words, they are taking part of the distribution owed to you, and using it to buy newly issued shares of the fund. But since the money that you invest back into OCCI still belongs to you, the shareholder, you essentially break even from that transaction.

To illustrate, here is a simple example:

Imagine you are the sole owner of a closed-end fund, or CEF, with 1,000,000 outstanding shares at a NAV of $10 each, for a total assets under management, or AUM, of $10 million. Over the course of a year, the fund earns 100% in cash returns, so now its AUM is $20 million, or $20 NAV/share.

Now consider the following two scenarios. In the first scenario, you pay out the $10 million in cash to yourself as a single distribution, so the fund's AUM drops back to $10 million and its NAV/share falls back to $10. Your total net worth is still $20 million ($10 million cash + $10 million stock).

In the second scenario, you only pay yourself $2 million in cash while issuing $8 million in new stock at a price of $8 per share. The $8 represents a significant discount to the former NAV of $10/share. As a result of this stock issuance, the fund retains the $8 million, increasing its AUM to $18 million. However, since the $8 million is now spread over 2 million shares (including the newly issued shares), the NAV/share declines to $9 per share, or a -10% hit.

But what is your net worth now? It is still $20 million, consisting of $18 million in stock and $2 million in cash. In other words, paying yourself in cash was no different than paying yourself in newly issued stock, despite the stock distribution being dilutive to NAV/share.

This is actually similar to what happens in a dilutive rights offering. Dilutive rights offerings cause a hit to the NAV/share, but this can be compensated for by the ability to subscribe for new shares at a discount, or alternatively the ability to sell the rights on the open market. Letting the rights expire worthless is generally the worst possible outcome because your holdings become diluted without compensation.

(This is aside from the fact that the premium/discount of a CEF usually decreases over the rights offering period, making a "sell and rebuy" strategy the best tactical play in most circumstances).

A stock-based distribution is basically a mini-rights offering, but where everyone is forced to participate. So although the NAV/share may decrease, the total value of the holdings does not.

3. Diminished discount advantage

While the stock-based distribution is not a negative per se, it should be noted that one key advantage is diminished.

When any CEF that is a discount pays any cash distribution, this generates alpha. This holds true regardless of whether the distribution is sourced from investment income, capital gains, or return of capital. This is because when you receive a cash distribution from a CEF trading at say a -10% discount, you are effectively getting back $1 of cash for every 90 cents of capital put in.

On the other hand, when this distribution is in the form of newly issued stock, this alpha is lost. This is because the newly issued stock also trades at a discount. Thus, you're putting in 90 cents to get 90 cents back.

I created a more realistic example more akin to the situation with OCCI in order to illustrate this situation.

Suppose there is a hypothetical CEF that has 1 million shares outstanding at $10 NAV/share each, for a total AUM of $10 million. However, this CEF constantly trades at a -20% discount, so the market price of the fund is $8. Over the course of a year, the CEF generates a return of 10%, and its intention is to distribute a yield equivalent to 20% of the NAV either in cash or newly issued stock.

After one year, the CEF's AUM increases to $11 million, with a new NAV per share of $11. If the distribution is made in cash, $2.20 per share will be distributed, resulting in a decrease of the NAV to $8.80 per share. Considering the consistent -20% discount, the market price of the CEF falls to $7.04 per share.

Now, let's consider an investor who owned 1000 shares of this CEF at the beginning of the year, which had a market value of $8,000. At the end of the year, the investor would have a total of $9,240, consisting of $7,040 in shares and $2,200 in cash. This represents a total percentage return of +15.5% on the initial cash investment. This outcome demonstrates the alpha derived from investing in CEFs at a discount. Despite the CEF's actual earning capacity of 10% for the year, the investor achieved a significant boost in returns by taking advantage of the discount and receiving cash distributions, allowing investors to outperform the fund's underlying performance.

However, in the case of the stock-based distribution, the CEF would distribute a total of $2.2 million in stock at the prevailing market price of $8.00. This distribution would result in the issuance of 275,000 new shares, and the NAV/share drops to $8.63 due to the dilutive effect of the stock distribution. At a -20% discount, the market price of the fund falls to $6.90.

Let's revisit the same investor who initially held 1000 shares of this CEF at the beginning of the year. After the stock-based distribution, the investor would now own a total of 1275 shares in the fund, which, at the current market price of $6.90, would be valued at $8,800. In this scenario, the investor would earn a return of 10% on the cash initially invested, which is equivalent to the fund's underlying performance. Consequently, the potential benefit of alpha from the discount is lost when the distribution is in the form of newly issued stock.

Income Lab

With OCCI which has historically distributed about 30-40% of the total distribution in cash, this alpha benefit is not completely lost, but it is significantly diminished.

Summary and outlook

OCCI's stock distribution method limits investors' ability to fully capitalize on the alpha gained when any CEF distributes cash to investors. Additionally, its deep discount prevents it from issuing shares in accretive fashion, unlike its peers ECC and OXLC. However, it is important to note that the stock-based distribution itself is not inherently negative, as demonstrated in the examples above.

Going forward, I anticipate that ECC and OXLC will likely outperform OCCI at the NAV level in due to their ability to perform accretive stock issuances. However, OCCI may present an attractive tactical opportunity due to its extremely wide discount. As a result, we're still comfortable with holding onto OCCI in our Tactical Income-100 portfolio. [December 5, 2023 update: We've since added to our OCCI position in our Tactical Income-100 portfolio, believing the new cash-based distribution policy to be a positive one].

In my opinion, OCCI's optimal course of action would be to reduce the distribution to a more sustainable level and transition back to a purely cash-based distribution. This adjustment would instill greater investor confidence in the fund, assuring investors that the asset base would not erode to zero through overdistribution and dilutive stock issuances. Restoring investor confidence is crucial for OCCI to return to a positive premium/discount valuation and be able to issue shares accretively to improve the NAV per share.

Strategy Statement

Our goal aims to provide consistent income with enhanced total returns. Our CEF rotation strategy includes trading between CEFs to exploit fluctuations in valuations. This is because CEF prices are inefficient, with investors often overreacting to both the upside or downside, or being unaware of upcoming corporate actions. This could help capture alpha from CEFs for the nimble investor.

Remember, it's really easy to put together a high-yielding CEF portfolio, but to do so profitably is another matter! Our experience has been that it is very possible to earn profitable returns in CEFs. While there are numerous opportunities in the closed-end fund sector, it is essential to remain vigilant of the associated risks. Blindly chasing yield is not a prudent strategy!

For further details see:

OCCI: Distribution Policy Was Not Inherently Negative, But New Policy Is Better